| Study Period | 2021 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2021 - 2023 |

| CAGR | 14.32 % |

| Largest Market | Asia-Pacific |

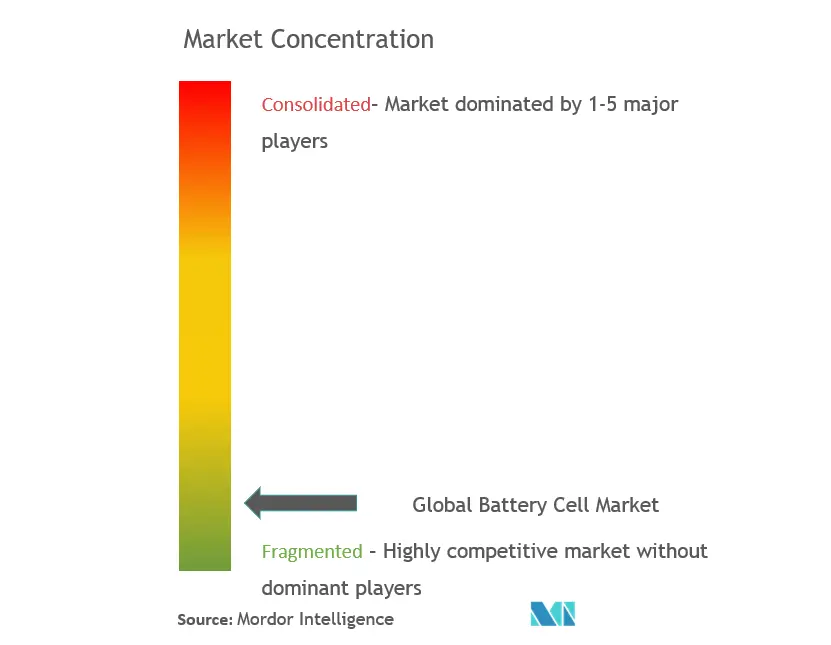

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Battery Cell Market Analysis

The Battery Cell Market is expected to register a CAGR of greater than 14.32% during the forecast period.

The battery cell industry is experiencing transformative changes driven by technological innovations and manufacturing scale-up efforts. According to the International Energy Agency, the demand for EV batteries is projected to surge from approximately 340 GWh in 2021 to over 3500 GWh by 2030, highlighting the massive scale of industry expansion required. Major technological breakthroughs are emerging, such as OneD Battery Sciences' introduction of SINANODE technology in 2023, which promises to triple the energy density of anodes while halving the cost per kWh. These advancements in battery technology are reshaping the industry landscape and driving significant investments in research and development across the value chain.

The industry is witnessing unprecedented levels of manufacturing capacity expansion and vertical integration efforts. China currently dominates the global battery manufacturing landscape, producing 75% of all lithium-ion batteries and controlling 70% of production capacity for cathodes. The country's manufacturing infrastructure continues to expand rapidly, with the number of gigafactories expected to increase from 93 to approximately 130 by 2030. This massive scale-up is accompanied by significant improvements in production efficiency and cost reduction, with lithium-ion battery prices reaching USD 132 per kWh in 2021, marking a crucial milestone for market competitiveness.

Alternative battery chemistries and technologies are gaining traction, diversifying the market landscape beyond traditional lithium-ion configurations. Manufacturers are increasingly exploring zinc-ion batteries, iron-redox flow batteries, and solid-state batteries, each offering unique advantages in terms of safety, performance, and environmental impact. The emergence of these new battery technologies is attracting substantial investment and fostering innovation across the industry, particularly in applications requiring specific performance characteristics or enhanced safety features.

The industry is experiencing a significant shift toward sustainable and circular economy practices, with manufacturers implementing innovative recycling programs and developing more environmentally friendly production processes. Major battery manufacturing companies are investing in closed-loop systems and sustainable material sourcing initiatives, while also focusing on reducing the carbon footprint of their production processes. This transformation is being supported by stringent regulatory frameworks, particularly in Europe, where new battery regulations mandate carbon footprint declarations and set specific recycling targets for critical materials, driving the industry toward more sustainable practices.

Battery Cell Market Trends

Increasing EV Adoption

The rapid adoption of electric vehicles globally has become a primary driver for the battery cell market, particularly for prismatic cell and cylindrical cell types. The demand for EV battery cells has been directly influenced by the significant reduction in lithium-ion battery prices, which reached approximately USD 132 per kWh in 2021. According to the International Energy Agency, the demand for EV batteries is projected to surge from 340 GWh in 2021 to over 3,500 GWh by 2030 in the Announced Pledges Scenario (APS). This massive increase in demand has led to substantial investments in battery manufacturing facilities worldwide, with major automotive manufacturers establishing dedicated battery production plants.

Major automotive manufacturers are increasingly adopting prismatic cells for their EV production. For instance, Volkswagen announced that up to 80% of its electric vehicles would use prismatic batteries by 2030, leading to the establishment of their first automotive battery cell factory in Salzgitter, Germany. The plant, nicknamed SalzGiga, is expected to commence production by 2025 with an annual capacity of 40 GWh, sufficient to power approximately 500,000 electric vehicles. The integration of battery energy storage systems (ESS) in EV charging infrastructure has further boosted the demand for battery cells, as these systems enable more cost-effective charging by drawing energy during low-demand periods and releasing power during peak demands.

Understand The Key Trends Shaping This Market

Download PDF

Rising Renewable Energy Generation Leading to Increasing Adoption of Battery Energy Storage Systems

The growing integration of renewable energy sources into power grids has created substantial demand for energy storage cell systems, driving the battery cell market growth. As renewable resources like solar and wind generate power intermittently and at varying levels, modern energy storage systems have become indispensable for renewable energy projects. Battery energy storage systems, particularly those utilizing prismatic cells, have gained popularity over traditional pumped storage systems due to their smaller land footprint, declining costs, and improved efficiency in managing grid stability.

The utility segment is expected to dominate the global battery storage capacity, accounting for nearly 66% of the total capacity by 2026. These systems play a crucial role in grid firming capacity, stabilizing grids with high renewable integration, and providing virtual power plant (VPP) services. Large utility-scale battery farms have evolved as alternatives to conventional fossil-fuel power plants, offering Frequency Control and Ancillary Services (FCAS) and stable baseload capacity. The prismatic cell technology dominates the battery ESS segment due to its longer cycle life, lower cost compared to cylindrical cells, and enhanced safety features, which are particularly crucial for residential BESS systems.

Growing Consumer Electronics Demand

The proliferation of portable consumer electronic devices has significantly driven the demand for battery cells, particularly in the prismatic cell and cylindrical cell segments. Prismatic lithium-ion cells have become the preferred choice for portable devices such as laptops and mobile phones, as their sandwiched and pressed layer design optimizes space utilization, achieving 90-95% packaging efficiency. This superior space efficiency makes them particularly suitable for modern slim devices where weight and form factor are crucial considerations. Major manufacturers are continuously innovating in this space, with companies like Samsung working on electric vehicle battery technology for next-generation smartphones, implementing stacking methods to increase battery density by 10%.

The demand for data centers and telecommunication infrastructure has further amplified the need for reliable battery systems. The exponential growth in data creation, estimated at 600 zettabytes of new data annually (equivalent to 600 trillion gigabytes), has led to increased demand for uninterruptible power supply systems utilizing battery cells. The telecommunications sector's expansion, particularly with the rollout of 5G networks, has created additional demand for backup power solutions. Prismatic cells are predominantly used in these applications due to their high energy density and reliable performance characteristics, making them ideal for both consumer electronics and industrial applications requiring consistent power backup solutions.

Segment Analysis: Type

Prismatic Segment in Battery Cell Market

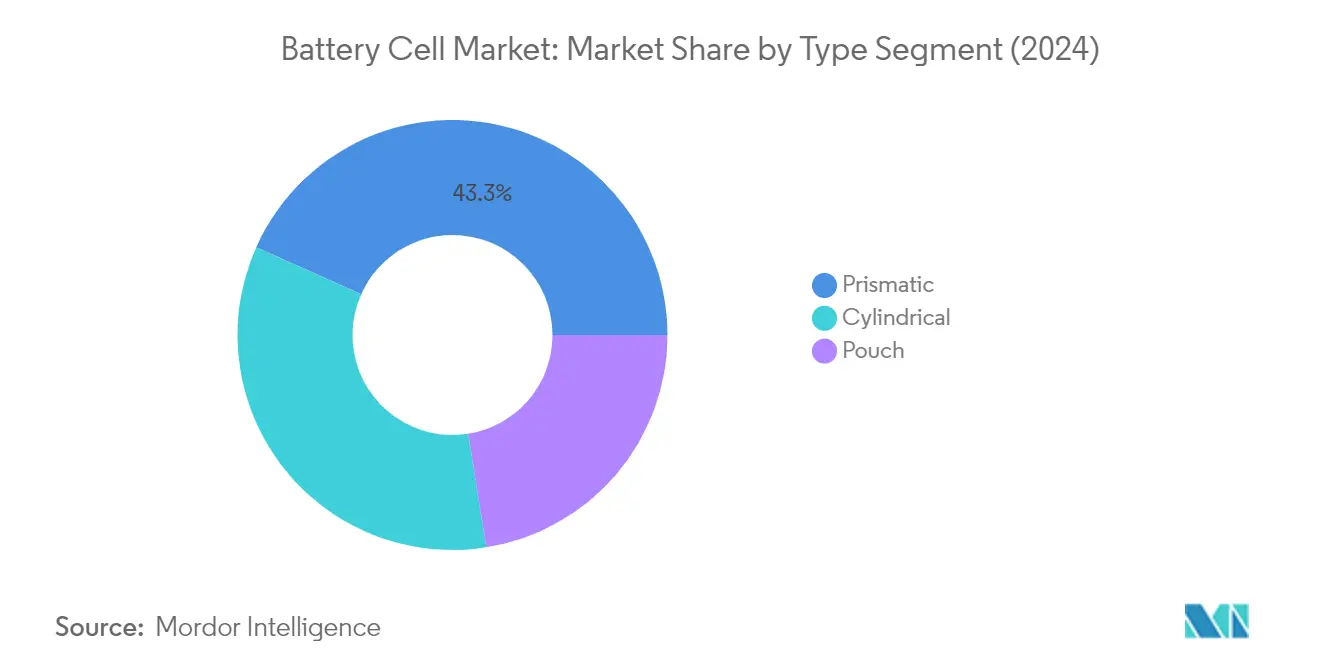

The prismatic cell segment dominates the global battery cell market, holding approximately 43% market share in 2024. This significant market position is primarily driven by the widespread adoption of prismatic cells in electric vehicles and energy storage systems (ESS). Prismatic cells are particularly favored in these applications due to their larger capacity in a small footprint and ability to store more energy per hour compared to other cell types. Major automotive manufacturers like Volkswagen have announced that up to 80% of their electric vehicles will use prismatic batteries, demonstrating the strong industry preference for this technology. The segment's dominance is further reinforced by its extensive use in mobile phones, laptops, and industrial applications, where space optimization and energy density are crucial factors.

Pouch Segment in Battery Cell Market

The pouch cell segment is emerging as the fastest-growing segment in the battery cell market from 2024 to 2029. This growth is attributed to its innovative design features, including low space requirements and lightweight construction, resulting in 90-95% packaging efficiency and increased energy density. Pouch cells are increasingly being adopted in next-generation performance batteries to accelerate the electrification needs of EVs. Major manufacturers are investing in pouch cell technology, as evidenced by SK On's decision to produce pouch-type LFP batteries and their partnership with Hyundai Motor and Kia to develop new pouch-type battery cells for hybrid electric vehicles. The segment's growth is further supported by its applications in consumer electronics, military equipment, and automotive sectors where weight reduction and space optimization are critical factors.

Remaining Segments in Battery Cell Market Type

The cylindrical cell segment continues to maintain a significant presence in the battery cell market, particularly in applications requiring established and proven technology. These cells are widely used in medical instruments, laptops, e-bikes, power tools, and even space exploration applications. The segment's strength lies in its mature manufacturing processes, cost-effectiveness, and robust mechanical stability. Notable manufacturers like Tesla have historically favored cylindrical cells for their electric vehicles, though the industry is witnessing a gradual shift towards other cell formats. The cylindrical format's standardized dimensions and well-established production methods continue to make it a reliable choice for various applications where cost and reliability are primary considerations.

Segment Analysis: Application

Automotive Batteries Segment in Battery Cell Market

The automotive battery cell segment dominates the global battery cell market, commanding approximately 67% of the total market share in 2024. This significant market position is primarily driven by the accelerating adoption of electric vehicles (EVs) worldwide. Major automotive manufacturers are increasingly investing in battery manufacturing facilities, with several new gigafactories being established across North America, Europe, and Asia-Pacific regions. The segment's growth is further supported by favorable government policies and incentives promoting electric vehicle adoption in key markets like China, Europe, and the United States. The development of advanced battery technologies, particularly in prismatic and cylindrical cells, along with the continuous efforts to improve energy density and reduce costs, has strengthened this segment's market leadership.

Industrial Batteries Segment in Battery Cell Market

The industrial batteries segment is experiencing rapid growth in the battery cell market, driven by increasing demand for uninterrupted power supply systems and energy storage solutions. The segment's expansion is particularly notable in data center applications, telecommunications infrastructure, and renewable energy integration projects. The growing focus on grid stability and energy security has led to increased adoption of battery energy storage systems (BESS) in industrial applications. Major technology companies are investing heavily in data center expansions, while telecommunications providers are upgrading their infrastructure to support 5G networks, creating substantial demand for industrial battery solutions. The segment is also benefiting from the rising adoption of renewable energy sources, which require efficient energy storage systems for optimal operation.

Remaining Segments in Application

The battery cell market's other significant segments include portable batteries, power tools batteries, SLI batteries, and other miscellaneous applications. The portable batteries segment maintains a strong presence in consumer electronics, including smartphones, laptops, and wearable devices. Power tools batteries serve the construction and DIY markets, with increasing demand for cordless tools driving growth. The SLI (Starting, Lighting, and Ignition) batteries segment, while traditional, continues to serve conventional automotive applications, though its share is gradually declining with the shift toward electric vehicles. These segments collectively contribute to the market's diversity and cater to specific application needs across various industries.

Battery Cell Market Geography Segment Analysis

Battery Cell Market in North America

The North American battery cell market holds approximately 21% of the global market share in 2024, establishing itself as a crucial region in the global landscape. The region's dominance is primarily driven by substantial investments in electric vehicle battery manufacturing facilities and energy storage systems. The United States leads the market with its robust research and innovation capabilities, particularly in developing advanced battery technology. The region's market is characterized by a strong presence of both prismatic cell and cylindrical cell types, serving diverse applications including electric vehicles, data centers, consumer electronics, and manufacturing activities. The market benefits from supportive government policies promoting clean energy adoption and electric vehicle infrastructure development. Additionally, the presence of major automotive manufacturers and their increasing focus on electric vehicle production continues to drive demand for battery cells in the region. The establishment of multiple battery gigafactories and the growing emphasis on domestic battery manufacturing capabilities further strengthens North America's position in the global battery cell market.

Battery Cell Market in Asia-Pacific

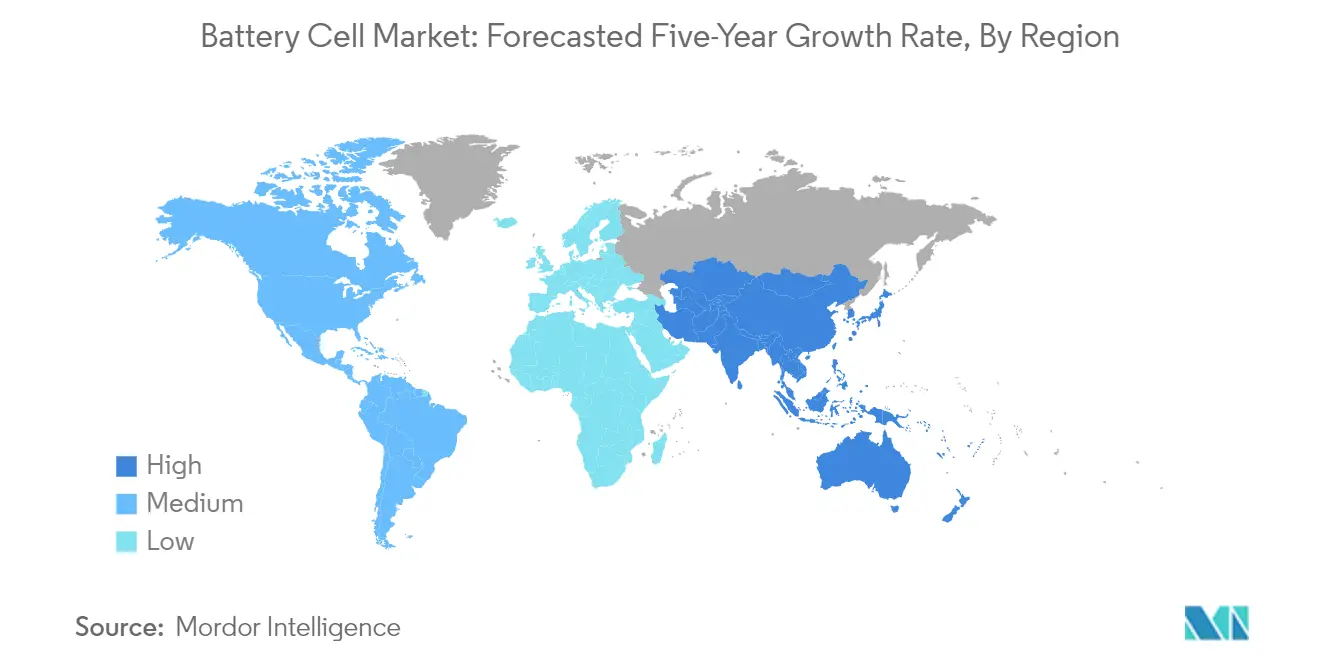

The Asia-Pacific battery cell market has demonstrated remarkable growth, recording an impressive compound annual growth rate of approximately 11% from 2019 to 2024. The region maintains its position as the global manufacturing hub for battery cells, with significant production capabilities across various cell types including prismatic, cylindrical, and pouch cells. The market's robust growth is underpinned by the region's strong presence in consumer electronics manufacturing and the rapid adoption of electric vehicles. The region benefits from advanced technological capabilities, well-established supply chains, and strategic advantages in battery material processing. The presence of leading battery cell companies and their continuous investments in research and development has strengthened the region's competitive position. Furthermore, the increasing focus on renewable energy integration and energy storage solutions has created additional demand drivers for battery cells. The region's market is also characterized by strong government support through favorable policies and incentives promoting clean energy adoption and electric vehicle manufacturing.

Battery Cell Market in China

The Chinese battery cell market is projected to grow at a robust compound annual growth rate of approximately 19% from 2024 to 2029, highlighting its pivotal role in the global battery industry. China's market dominance is reinforced by its comprehensive battery supply chain, from raw material processing to cell manufacturing and battery assembly. The country's battery cell industry benefits from significant government support through strategic initiatives and favorable policies promoting electric vehicle adoption and renewable energy integration. The market is characterized by strong domestic demand driven by the world's largest electric vehicle market and growing energy storage requirements. China's battery manufacturers continue to invest heavily in research and development, focusing on improving battery performance and reducing costs. The country's strategic focus on developing advanced battery technologies and expanding manufacturing capabilities positions it as a key player in shaping the future of the global battery cell industry.

Battery Cell Market in South Korea

The South Korean battery cell market demonstrates significant strength in technological innovation and manufacturing excellence, particularly in the development of advanced battery technologies. The country's market is driven by its strong presence in the global electric vehicle battery supply chain and its expertise in consumer electronics. South Korean manufacturers are known for their high-quality battery cells across all formats - prismatic, cylindrical, and pouch cells. The market benefits from substantial private sector investments in research and development, focusing on improving battery performance and safety features. The country's strategic focus on developing next-generation battery technologies and expanding manufacturing capabilities strengthens its competitive position. Additionally, the growing domestic demand for energy storage systems and electric vehicles provides a stable foundation for market growth. The market also benefits from strong government support through various initiatives promoting clean energy adoption and technological innovation.

Battery Cell Market in Europe

The European battery cell market is experiencing significant transformation driven by the region's ambitious clean energy goals and electric vehicle adoption targets. The market is characterized by increasing investments in domestic battery manufacturing capabilities to reduce dependency on imports and establish a robust regional supply chain. European manufacturers are focusing on developing sustainable and innovative battery technologies, with particular emphasis on environmental considerations and circular economy principles. The region's market benefits from strong regulatory support through initiatives like the European Battery Alliance and various government incentives promoting clean energy adoption. The growing demand for energy storage solutions, driven by increasing renewable energy integration, further supports market growth. The market also benefits from the presence of leading automotive manufacturers and their commitment to electric vehicle production. The region's focus on research and development in advanced battery technologies positions it well for future growth in the global battery cell market.

Battery Cell Market in Middle East & Africa

The Middle East & African battery cell market is emerging as a promising growth region, driven by increasing investments in renewable energy infrastructure and growing adoption of electric vehicles. The market is characterized by rising demand for energy storage solutions, particularly in regions with developing power infrastructure. Countries in the region are increasingly focusing on diversifying their energy sources and implementing sustainable energy solutions, creating opportunities for battery cell applications. The market benefits from growing investments in smart city projects and telecommunications infrastructure, which drive demand for backup power solutions. The region's automotive sector is gradually embracing electric vehicles, particularly in urban areas, creating additional demand for battery cells. Furthermore, the industrial sector's growing need for reliable power solutions contributes to market growth. The market also benefits from increasing awareness about clean energy solutions and supportive government initiatives promoting sustainable development.

Battery Cell Market in South America

The South American battery cell market is witnessing steady growth, driven by increasing adoption of renewable energy solutions and growing demand for energy storage systems. The region's market benefits from its rich lithium reserves, positioning it strategically in the global battery supply chain. The market is characterized by growing investments in electric vehicle infrastructure and increasing adoption of clean energy solutions. Countries in the region are implementing supportive policies to promote electric vehicle adoption and renewable energy integration, creating opportunities for battery cell applications. The market also benefits from growing industrial activities and increasing demand for reliable power solutions. The telecommunications sector's expansion and the need for backup power solutions further drive market growth. Additionally, the region's focus on developing domestic manufacturing capabilities and reducing import dependency creates opportunities for market expansion.

Get Analysis on Important Geographic Markets

Download PDF

Battery Cell Industry Overview

Top Companies in Battery Cell Market

The battery cell market features prominent players like CATL, Samsung SDI, LG Energy Solution, BYD, and Panasonic, leading technological advancement and market expansion. These battery cell companies are heavily investing in research and development to improve battery technology, particularly focusing on next-generation technologies like sodium-ion batteries and solid-state batteries. Strategic collaborations and joint ventures with automotive manufacturers have become increasingly common to secure long-term supply agreements and develop customized solutions. Manufacturing capacity expansion through new facility establishments across multiple geographies demonstrates the industry's focus on localizing production and reducing supply chain dependencies. Companies are also emphasizing sustainable production methods and circular economy principles while simultaneously working on reducing production costs through economies of scale and improved manufacturing processes.

Dynamic Market with Strong Growth Potential

The battery cell market exhibits a relatively consolidated structure with a few global conglomerates dominating the landscape, particularly in the electric vehicle and energy storage segments. These major players leverage their extensive research capabilities, established supply chains, and strong financial positions to maintain their market leadership. Regional players, especially in Asia-Pacific, are gradually gaining prominence through specialized offerings and strategic partnerships with local automotive manufacturers and energy companies. The market has witnessed significant merger and acquisition activity, with established players acquiring innovative startups to enhance their technological capabilities and expand their product portfolios.

The competitive dynamics are further shaped by vertical integration strategies, with many manufacturers controlling multiple stages of the supply chain from raw material processing to final battery assembly. Joint ventures between battery manufacturers and automotive companies have become increasingly prevalent, creating strong barriers to entry for new players. The market also sees active participation from government-backed entities, particularly in regions focusing on developing domestic battery manufacturing capabilities, leading to a complex interplay between private enterprise and state-supported initiatives.

Innovation and Adaptability Drive Market Success

Success in the battery cell market increasingly depends on companies' ability to balance technological innovation with cost-effective manufacturing processes. Established players are focusing on developing proprietary technologies while maintaining strong relationships with key customers in the automotive and energy storage sectors. The ability to secure stable raw material supply chains, particularly for critical materials like lithium, cobalt, and nickel, has become crucial for maintaining competitive advantage. Companies are also investing in automated manufacturing processes and quality control systems to ensure consistent product quality while reducing production costs.

For new entrants and smaller players, success lies in identifying and serving niche market segments with specialized battery solutions. The development of alternative battery chemistries and innovative cell designs presents opportunities for differentiation. Regulatory compliance, particularly regarding safety standards and environmental regulations, continues to shape market dynamics and investment decisions. The increasing focus on sustainability and recycling capabilities is becoming a critical factor for long-term success, with companies needing to demonstrate their commitment to environmental stewardship while maintaining competitive pricing structures. Additionally, the integration of battery material and battery component innovations is pivotal in advancing the industry's sustainability goals.

Battery Cell Market Leaders

-

LG Chem Ltd

-

Contemporary Amperex Technology Co. Limited

-

BYD Company Limited

-

GS Yuasa Corporation

-

Panasonic Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Battery Cell Market News

In October 2022, Panasonic decided to produce 30 GWh of battery cells during the first phase of its new Kansas factory, expected to supply Tesla's vehicle production. The construction of the factory was expected to begin in November 2022.

In December 2021, SK Innovation started using pouch cells in the lithium iron phosphate (LFP) battery. The battery spinoff from SK Innovation is anticipated to start commercial production of a pouch-type LFP battery for electric vehicles during the second half of 2022.

Battery Cell Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2027

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

-

4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

-

4.7 Porter's Five Force Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 By Type

- 5.1.1 Prismatic

- 5.1.2 Cylindrical

- 5.1.3 Pouch

-

5.2 By Application

- 5.2.1 Automotive Batteries (HEV, PHEV, EV)

- 5.2.2 Industrial Batteries (Motive, Stationary (Telecom, UPS, Energy Storage Systems (ESS), etc.)

- 5.2.3 Portable Batteries (Consumer Electronics etc.)

- 5.2.4 Power Tools Batteries

- 5.2.5 SLI Batteries

- 5.2.6 Other Applications

-

5.3 By Geography

- 5.3.1 North America

- 5.3.2 Asia-Pacific

- 5.3.3 Europe

- 5.3.4 Middle East and Africa

- 5.3.5 South America

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Collaborations, and Joint Ventures

- 6.2 Strategies Adopted by Key Players

-

6.3 Company Profiles

- 6.3.1 BYD Co. Ltd

- 6.3.2 Contemporary Amperex Technology Co. Limited

- 6.3.3 Duracell Inc.

- 6.3.4 EnerSys

- 6.3.5 GS Yuasa Corporation

- 6.3.6 Shenzhen ACE Battery Co. Ltd

- 6.3.7 LG Energy Solution Ltd

- 6.3.8 Panasonic Corporation

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Battery Cell Industry Segmentation

A battery can be defined as an electrochemical device (consisting of one or more electrochemical cells) that can be charged with an electric current and discharged whenever required. Batteries are usually devices made up of multiple electrochemical cells connected to external inputs and outputs.

The battery cell market is segmented by type, application, and geography. By application, the market is segmented into automotive batteries (HEV, PHEV, EV), industrial batteries (motive, stationary (telecom, UPS, energy storage systems (ESS), etc.), portable batteries (consumer electronics, etc.), power tools batteries, SLI batteries, and other applications. By type, the market is segmented into prismatic, cylindrical, and pouch. The report also covers the market size and forecasts across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD billion).

| By Type | Prismatic |

| Cylindrical | |

| Pouch | |

| By Application | Automotive Batteries (HEV, PHEV, EV) |

| Industrial Batteries (Motive, Stationary (Telecom, UPS, Energy Storage Systems (ESS), etc.) | |

| Portable Batteries (Consumer Electronics etc.) | |

| Power Tools Batteries | |

| SLI Batteries | |

| Other Applications | |

| By Geography | North America |

| Asia-Pacific | |

| Europe | |

| Middle East and Africa | |

| South America |

Need A Different Region or Segment?

Customize Now

Battery Cell Market Research FAQs

What is the current Battery Cell Market size?

The Battery Cell Market is projected to register a CAGR of greater than 14.32% during the forecast period (2025-2030)

Who are the key players in Battery Cell Market?

LG Chem Ltd, Contemporary Amperex Technology Co. Limited, BYD Company Limited, GS Yuasa Corporation and Panasonic Corporation are the major companies operating in the Battery Cell Market.

Which region has the biggest share in Battery Cell Market?

In 2025, the Asia-Pacific accounts for the largest market share in Battery Cell Market.

What years does this Battery Cell Market cover?

The report covers the Battery Cell Market historical market size for years: 2021, 2022, 2023 and 2024. The report also forecasts the Battery Cell Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Battery Cell Market Research

Mordor Intelligence provides a comprehensive analysis of the battery cell industry. We leverage our extensive expertise in battery technology and battery manufacturing research. Our detailed report examines various cell configurations, including prismatic cell, pouch cell, and cylindrical cell technologies, alongside traditional lead acid cell solutions. The analysis covers crucial aspects of battery component development. This includes battery electrode design, battery electrolyte composition, and battery separator innovations. These insights are crucial for understanding the evolving battery manufacturing industry.

Stakeholders across the value chain, from battery cell companies to end-users, benefit from our thorough examination of automotive battery cell and EV battery cell applications. The report, available as an easy-to-download PDF, offers detailed analysis of battery material trends, energy storage cell developments, and emerging battery technology market dynamics. Our research encompasses both primary battery cell and rechargeable battery cell segments. We focus on the battery material market, battery electrolyte market, and battery separator market, providing actionable insights for strategic decision-making in this rapidly evolving industry.