Automobile Rental And Leasing Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

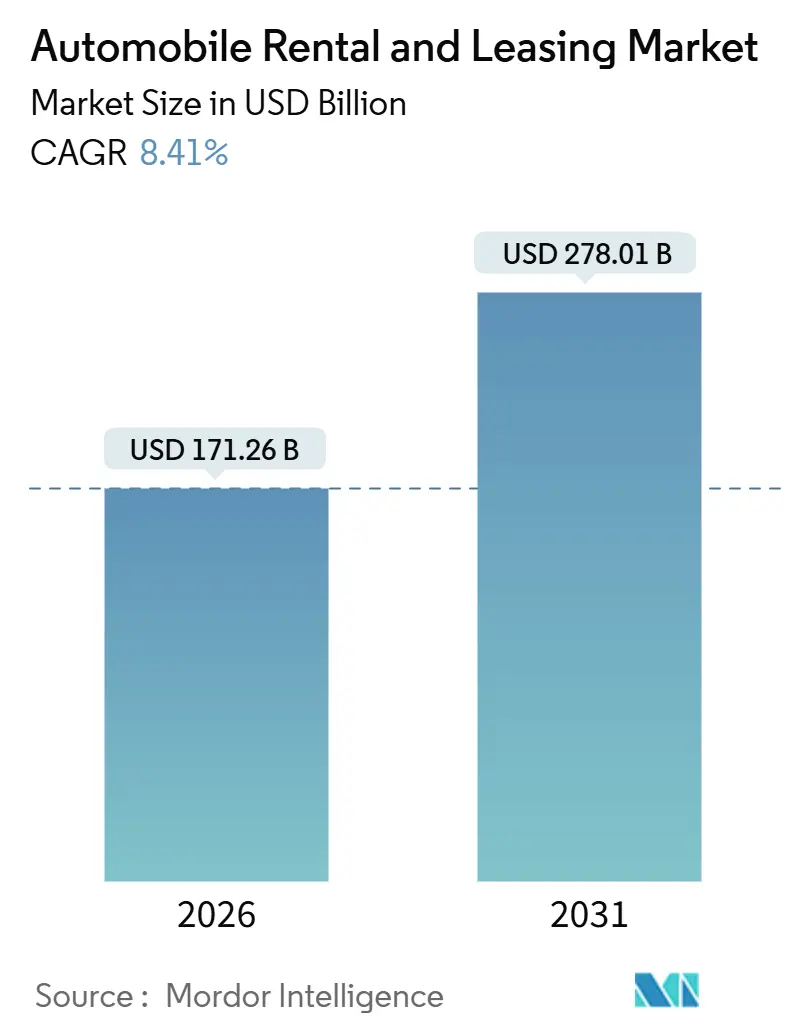

| Market Size (2026) | USD 171.26 Billion |

| Market Size (2031) | USD 278.01 Billion |

| Growth Rate (2026 - 2031) | 8.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automobile Rental And Leasing Market Analysis by Mordor Intelligence

The automobile rental and leasing market size is estimated at USD 171.26 billion in 2026, and is expected to reach USD 278.01 billion by 2031, at a CAGR of 8.41% during the forecast period (2026-2031). Growth rests on structural shifts such as mandatory fleet electrification, vehicle-to-grid pilots that monetize idle assets, and AI-driven yield tools incorporating more than 50 real-time variables. Operators must absorb a decent collapse in electric-vehicle residual values while securing incremental grid-services income and managing a financing environment where fleet acquisition costs rose significantly between 2023 and 2025. Divergent segment dynamics are visible: commercial vehicles outpace passenger cars as e-commerce logistics reshapes last-mile delivery, and leasing expands faster than rentals as corporates seek off-balance-sheet solutions. Competitive intensity has deepened with peer-to-peer platforms capturing a minimum of United States leisure bookings and incumbents launching counter-models.

Key Report Takeaways

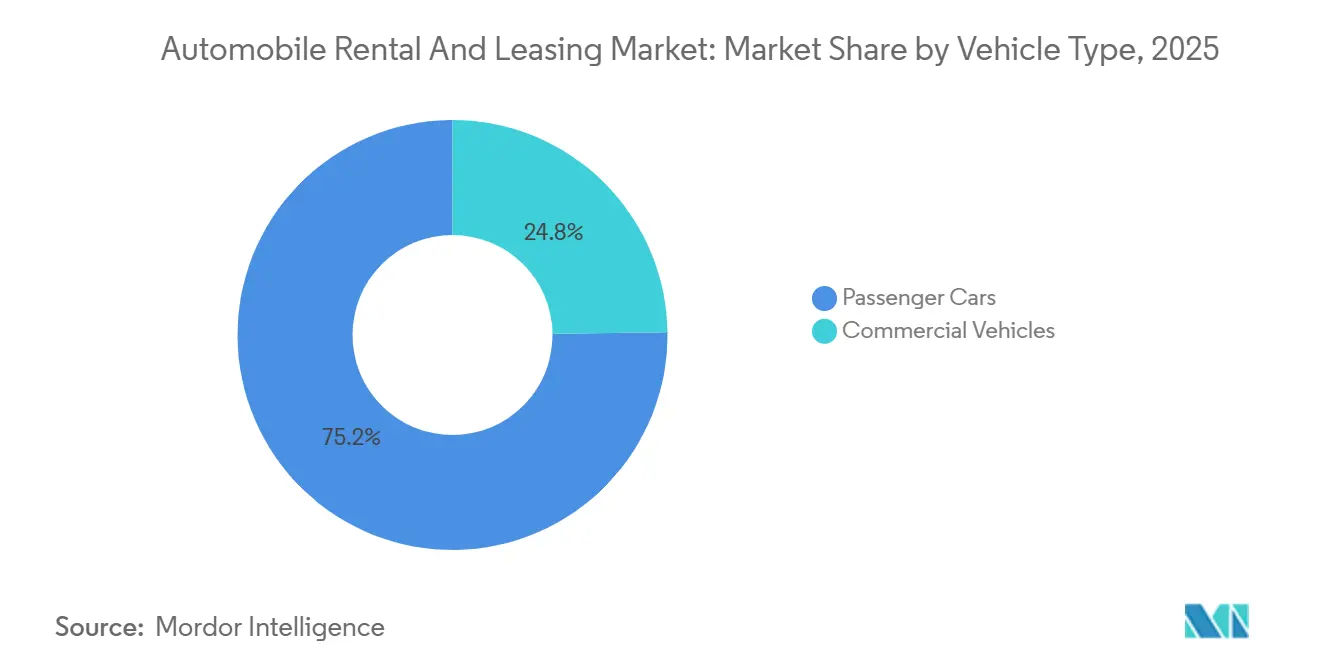

- By vehicle type, passenger cars led with 75.16% revenue share in 2025; commercial vehicles are forecast to expand at an 8.43% CAGR to 2031.

- By service type, rental services held 67.37% of the automobile rental and leasing market share in 2025, while leasing recorded the highest projected CAGR at 8.51% through 2031.

- By mode of booking, online channels accounted for 63.23% of transactions in 2025 and are advancing at an 8.45% CAGR through 2031.

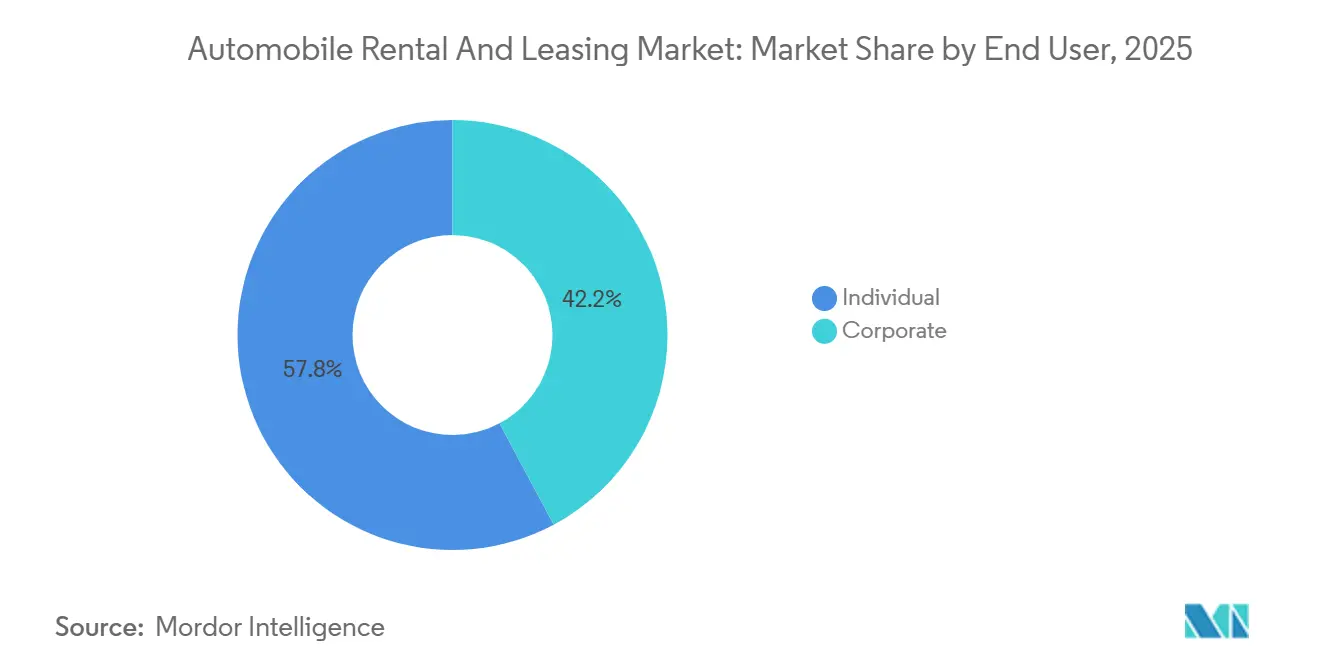

- By end user, individual customers represented 57.75% of 2025 revenue, whereas corporate demand is forecast to rise at an 8.54% CAGR to 2031.

- By propulsion, internal-combustion vehicles made up 81.26% of the 2025 fleet inventory; electric vehicles are growing fastest at an 8.56% CAGR through 2031.

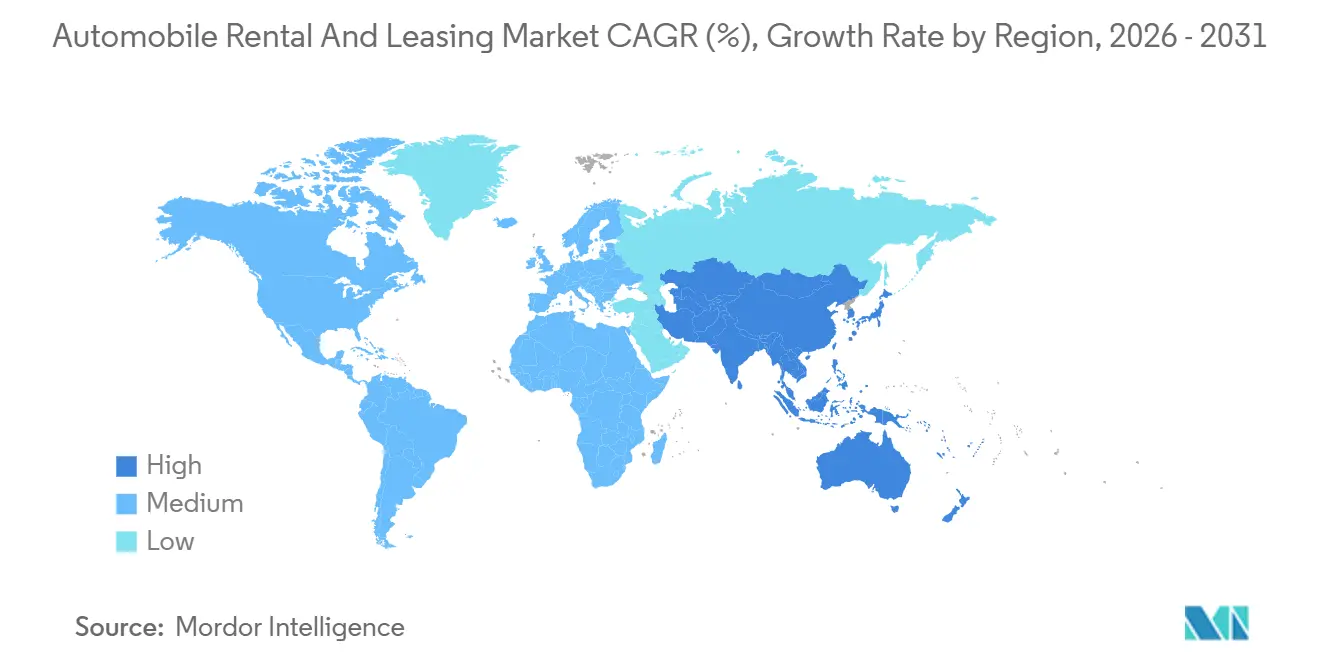

- By geography, North America led with 32.37% of 2025 revenue, while Asia Pacific is set to grow at an 8.47% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automobile Rental And Leasing Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovery in Global Business and Leisure Travel | +1.5% | Global, with North America and Europe leading business travel normalization | Short term (≤ 2 years) |

| Government Incentives Accelerating Fleet Electrification | +1.2% | North America (IRA credits), Europe (Clean Vehicles Directive), China (NEV mandate) | Medium term (2-4 years) |

| E-Commerce-Led Demand | +1.0% | North America and Europe for last-mile delivery; Asia Pacific tier-2/3 cities | Medium term (2-4 years) |

| Mobile/Online Booking Penetration Surge | +0.8% | Global, with Asia Pacific core showing highest conversion rates, spill-over to Middle East and Africa | Short term (≤ 2 years) |

| AI-Enabled Dynamic Pricing and Predictive Maintenance | +0.7% | Global, early gains in North America and Western Europe | Long term (≥ 4 years) |

| Vehicle-To-Grid (V2G) Revenue Streams Turn Rental Fleets | +0.5% | National pilots in California, NYC, Balearic Islands; early commercial deployment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recovery in Global Business and Leisure Travel

By mid-2025, business trips nearly returned to pre-pandemic levels. In contrast, leisure journeys not only recovered but also exceeded previous benchmarks. This increase in leisure travel has driven corporate daily rates significantly higher than leisure rates [1]“2025 Air Passenger Market Update,” International Air Transport Association, iata.org. Fleet managers are now leveraging AI forecasting, repositioning vehicles well in advance of major events. A prominent European operator, after integrating predictive rebalancing, reported a notable improvement in asset utilization. Saudi Arabia, with its Vision 2030 initiative, aims to attract a substantial number of visitors by the end of the decade. This ambitious target, combined with relatively low rental penetration compared to more developed markets, indicates strong multi-year demand. While recovery is uneven, China's domestic traffic has fully rebounded, yet international arrivals remain significantly below pre-pandemic levels.

Government Incentives Accelerating Fleet Electrification

The U.S. Inflation Reduction Act provides commercial electric vehicles (EVs) with significant subsidies, leading to a notable reduction in their five-year total cost of ownership [2]“Inflation Reduction Act of 2022,” U.S. Congress, congress.gov . Under Europe’s Clean Vehicles Directive, a substantial portion of public procurements must be zero-emission within the next few years. This mandate is pushing private lessors to electrify their fleets to maintain airport concessions. In China, a dual-credit policy is set to effectively prohibit new internal combustion engine (ICE) rentals in major cities in the near future. Meanwhile, California is bolstering the case for electrification by offering competitive peak-hour vehicle-to-grid (V2G) tariffs [3]“Vehicle-Grid Integration Tariffs,” California Air Resources Board, arb.ca.gov . As a result, operators are strategically timing their deployments in areas with the most lucrative subsidies, leading to a significantly higher ratio of EVs to ICEs in California compared to rural Midwest regions.

E-Commerce-Led Demand for Flexible Truck and Van Leasing

In recent years, a major North American lessor experienced a significant increase in short-term van contracts, influenced by Amazon's commitment to deploy a substantial number of electric vans by the end of the decade. A major deal finalized in the middle of the decade is set to provide thousands of electric vans to regional carriers across the United States and Canada. Leasing durations in smaller cities have notably decreased over time, reflecting the rising demand for flexibility. With stricter environmental regulations anticipated in the near future, the ownership risk is increasingly shifting towards lessors.

Mobile/Online Booking Penetration Surge

In 2025, digital channels dominated bookings, with a significant portion facilitated through mobile apps. Super-apps in the Asia Pacific region demonstrated much higher conversion rates compared to standalone sites, primarily due to their bundled itineraries. Contactless pick-up has become a standard expectation; for instance, one global brand's app significantly reduced transaction times, leading to notable labor cost savings. Using proprietary algorithms, upsell offers are enhanced by real-time weather, events, and browsing signals, resulting in a substantial year-over-year increase in ancillary revenue per rental. However, capital expenditure remains a challenge, as telematics and software subscriptions incur considerable costs annually for each vehicle.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Vehicle Acquisition and Financing Costs | -0.9% | Global, with acute pressure in North America and Europe due to elevated interest rates | Short term (≤ 2 years) |

| Intensifying Competition from Ride-Hailing and P2P Car-Sharing | -0.7% | North America and Europe urban markets; emerging in Asia Pacific tier-1 cities | Medium term (2-4 years) |

| EV Residual-Value Volatility and Repair-Cost Uncertainty | -0.6% | North America and Europe, where EV adoption is concentrated | Medium term (2-4 years) |

| Heightened Cybersecurity and Data-Privacy Liabilities | -0.4% | Global, with regulatory focus in EU (GDPR) and North America (CCPA, state laws) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle Acquisition and Financing Costs

Over the forecast period, fleet prices experienced significant growth, driven by rising interest rates, which reached their peak in mid-2024. Each substantial increase in interest rates added notable annual interest costs per vehicle, exerting pressure on EBITDA margins. Original-equipment makers raised fleet list prices due to inflation in battery material costs, while smaller operators, lacking the advantage of volume leverage, were forced to pay full sticker prices. To manage capital expenditures, fleets have extended their average hold periods. However, this strategy has led to higher maintenance expenses and increased exposure to residual-value risks.

EV Residual-Value Volatility and Repair-Cost Uncertainty

In 2024, prices for used electric vehicles (EVs) experienced a significant decline. This drop was driven by rapid technological advancements that surpassed the demand for resales. As a result, a prominent operator faced substantial financial losses after selling off a large number of units. Repairing EVs has become notably more expensive compared to internal combustion engine (ICE) vehicles, primarily due to the need for specialized labor and limited availability of parts. Additionally, replacing an EV battery can impose a considerable financial burden, especially for vehicles owned for a short period. On the insurance front, premiums for EVs are noticeably higher than those for ICE vehicles, reflecting uncertainties in risk assessment. While original equipment manufacturers (OEMs) are beginning to offer residual-value guarantees—such as a minimum value assurance on popular models—these guarantees remain limited in scope.

Segment Analysis

By Vehicle Type: Commercial Demand Accelerates on Last-Mile Logistics

Passenger cars captured 75.16% of 2025 revenue, whereas commercial vehicles are forecast to advance at an 8.43% CAGR, eclipsing overall automobile rental and leasing market growth. E-commerce giants and regional couriers are driving the surge, opting for flexible leases to navigate seasonal peaks. A significant contract, finalized recently, will deploy thousands of electric vans with last-mile carriers across North America, highlighting the industry's shift towards electrified fleets. In rural tier-3 cities, where volumes fluctuate, shorter leases—averaging a little over two years—are becoming the norm. While passenger cars maintain a dominant market share, they're feeling the pinch from peer-to-peer services that undercut daily rates, especially in dense urban areas where parking costs deter ownership.

Passenger vehicles are reaping the benefits of a travel resurgence, commanding premium daily rates from corporate clients. However, their market dominance belies a growing vulnerability: urban hubs like Manhattan and London have witnessed a noticeable dip in short-term rentals over the past couple of years, a decline somewhat balanced by growth in suburban and leisure markets. On the commercial front, clients are gravitating towards bundled services—maintenance, telematics, and driver training—creating switching barriers that peer-to-peer models struggle to overcome. With stricter environmental regulations complicating compliance, many are turning to specialist lessors for outsourcing.

By Service Type: Leasing Gains Ground as Corporations Seek Balance-Sheet Relief

Rental captured 67.37% of 2025 spend, but leasing expands at an 8.51% CAGR, outperforming the broader automobile rental and leasing market. Enterprises gravitate toward leases that shift rising interest-rate exposure and residual risk to service providers. In recent times, a newly merged European lessor, overseeing a large fleet of vehicles, revealed that a significant portion of its contracts featured early-termination flexibility, marking a notable increase compared to previous years. Meanwhile, in North America, inquiries for electric vehicle (EV) leases experienced substantial growth, driven by tax credits that effectively reduced acquisition costs.

Rentals continue to play a pivotal role for both leisure and short-term business travelers. This trend is bolstered by AI-driven pricing strategies, which significantly boosted one company's revenue per available vehicle. However, the short hold periods of these rentals have led to pronounced shocks from EV depreciation. A testament to this is a major operator's substantial financial write-down following the sale of its used electric sedans. On a different note, subscription models are gaining traction. A prominent pilot program in Germany exemplifies this trend, offering customers the flexibility to swap cars multiple times a month for a flat fee, blending the agility of rentals with the predictability of leasing.

By Mode of Booking: Digital Channels Dominate as Super-Apps Scale

Online channels controlled 63.23% of 2025 deals and are set to widen their lead at an 8.45% CAGR, outpacing the overall automobile rental and leasing market. Super-apps in the Asia Pacific region are achieving impressive conversion rates by seamlessly integrating car bookings into comprehensive door-to-door itineraries. Recognizing the value of app users, a leading global operator made a significant investment into mobile-centric loyalty features, having discovered that these users come with notably reduced acquisition costs and enhanced lifetime value.

Despite the digital surge, offline bookings retain their significance, especially in regions where digital adoption is still catching up or where regulations mandate in-person validations. In recent times, older travelers have constituted a substantial portion of offline reservations. Airport desks have become a crucial backup, stepping in when digital bookings falter or when upgrades are sought. However, the push for capital upgrades remains unyielding: smaller fleets are feeling the strain of consistent expenditures on telematics and contactless technologies.

By End User: Corporate Demand Surges Under Electrification Mandates

Individuals provided 57.75% of 2025 revenue, but corporate clients will climb faster at an 8.54% CAGR through 2031. Europe’s Corporate Sustainability Reporting Directive requires large companies to disclose their Scope 3 travel emissions, encouraging them to adopt electrified rental and leasing solutions. In 2024, the majority of new European contracts specified vehicle-swap flexibility to manage macro uncertainty.

Peer-to-peer services attract price-sensitive leisure segments, while corporates prioritize data security and regulatory compliance. Operators holding ISO 27001 certification now win fleet tenders at minimal premiums, a clear moat as telematics proliferate. Cyber insurers reinforce the gap by hiking premiums for non-certified providers.

By Propulsion Type: EVs Grow Fastest Despite Depreciation Risk

The automobile rental and leasing market size tied to internal-combustion vehicles remained dominant in 2025 with 81.26% share; however, electric vehicles represent the fastest-growing segment, projected to scale at an 8.56% CAGR. U.S. tax credits, EU directives, and China’s dual-credit scheme underpin uptake.

Yet, 2024’s plunge in used-EV prices—and repair bills that can run up to half of those for higher ICE equivalents—exposes fleets to depreciation shocks. OEM residual guarantees and battery-health monitoring offer partial relief, while V2G pilots demonstrate potential to earn USD 800 per vehicle annually and shave charging bills by one-fifth.

Geography Analysis

North America produced 32.37% of 2025 revenue and matches the overall CAGR as market maturity limits upside. The Inflation Reduction Act accelerates EV adoption, and California’s V2G tariffs reward bidirectional charging. Peer-to-peer penetration reached a minimum of leisure bookings, prompting incumbents to launch counter-platforms. The 2024 ransomware incident that froze 15,000 sites drove a wave of ISO 27001 certifications as corporate buyers harden cybersecurity requirements.

Asia Pacific is the fastest-growing region, advancing at an 8.47% CAGR. China’s dual-credit rules will bar fresh ICE rentals in key cities after 2027, while India’s corporate leasing grows despite charging-infrastructure gaps. Super-apps such as Grab and WeChat triple booking conversion rates. However, regulatory fragmentation—like India’s differential GST—complicates cross-border fleet allocation. Europe shows steady expansion fueled by electrification mandates. Subscription schemes proliferate in Germany and the UK, where customers can swap cars three times a month. Seasonal volatility in Southern Europe inflates idle-fleet costs up to two-fifths off-peak, spurring adoption of dynamic pricing tied to local event calendars. A 200-vehicle V2G project in Spain’s Balearic Islands stabilized the grid during tourist surges.

South America remains concentrated, with a Brazilian operator holding majority of regional share. Currency-hedged leasing shields corporate customers from real and peso volatility. Elevated interest rates—Brazil’s Selic at decent position in mid-2025—curb fleet financing, though e-commerce drives van leasing. The Middle East and Africa gain structural support from Saudi Arabia’s plan to attract 100 million visitors by 2030. Rental duration averages 12 days, triple the global mean. The UAE capitalizes on high-net-worth tourism, expanding luxury and electric catalogs, while South Africa contends with crime-related insurance premiums. Turkey is emerging as a regional hub, blending tourism and cross-border rentals.

Competitive Landscape

Enterprise, Hertz, Avis, Sixt, and Europcar, the top five providers, collectively account for a significant portion of global revenue, indicating a moderately concentrated market. While incumbents focus on fleet electrification and AI-driven yield management to protect their margins, peer-to-peer disruptors have carved out a notable share of United States leisure bookings, leveraging price leadership and hyper-local availability. Technology is becoming a crucial differentiator; fleets boasting ISO 27001 accreditation are securing corporate contracts at significant premiums, a trend driven by intensified scrutiny on cybersecurity.

OEM alliances are becoming increasingly strategic. For instance, a prominent German OEM is now offering a substantial guarantee on the residual value of its crossover vehicles leased to commercial fleets, effectively transferring the depreciation risk. Meanwhile, specialists in commercial vehicles are capitalizing on emerging opportunities: a North American lessor recorded a significant surge in short-term van contracts, and a major multiyear agreement is set to provide a large number of electric vans to regional carriers.

There's a noticeable acceleration in platform convergence. For example, a Florida-based pilot program from an established player allows private owners to list their vehicles, echoing the economics of disruptors. Additionally, another operator has teamed up with a leader in autonomous driving, launching self-driving rentals in both Phoenix and San Francisco, aiming for round-the-clock utilization and reduced labor expenses. In the Asia Pacific, consolidation is evident as a leading Chinese firm expands its new-energy fleet, while an Indian counterpart is navigating liquidity challenges and considering strategic partnerships.

Automobile Rental And Leasing Industry Leaders

Enterprise Holdings

The Hertz Corporation

BlueLine Rental

LeasePlan

Avis Budget Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: The peer-to-peer provider Turo introduced a monthly trip product across the United States, Canada, and Australia, offering flexible bookings as an alternative to ownership.

- June 2025: DHL, in collaboration with commercial vehicle rental provider hylane, secures 30 Mercedes-Benz eActros 600 trucks. This development highlights a significant move in the rental market, as hylane utilizes a "pay per use model" for leasing, charging DHL based on kilometers driven. The partnership was formalized at the "Transport Logistic" trade fair in Munich, showcasing the growing adoption of flexible rental solutions in the commercial vehicle segment.

Global Automobile Rental And Leasing Market Report Scope

The scope of the report includes Vehicle Type (Passenger Cars and Commercial Vehicles), Service Type (Rental and Leasing), Mode of Booking (Online and Offline), End User (Individual and Corporate), Propulsion Type (Internal Combustion Engine and Electric Vehicles), and Geography.

| Passenger Cars |

| Commercial Vehicles |

| Rental |

| Leasing |

| Online |

| Offline |

| Individual |

| Corporate |

| Internal Combustion Engine (ICE) |

| Electric Vehicles (EVs) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| By Service Type | Rental | |

| Leasing | ||

| By Mode of Booking | Online | |

| Offline | ||

| By End User | Individual | |

| Corporate | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | |

| Electric Vehicles (EVs) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global automobile rental and leasing revenue be by 2031?

Revenue is projected to reach USD 278.01 billion by 2031, expanding at an 8.41% CAGR from 2025.

Which region is set to grow fastest through 2031?

Asia Pacific leads with an expected 8.47% CAGR, propelled by electrification mandates and super-app integration.

Why are corporates shifting from renting to leasing vehicles?

Leasing shifts residual-value and interest-rate risk to the lessor, offers flexible swap terms, and unlocks tax incentives for electric fleets.

What is driving commercial-vehicle leasing demand?

E-commerce logistics requires short-duration van capacity, and new Euro 7 standards make ownership riskier, so operators prefer flexible leases.

How are operators mitigating electric-vehicle depreciation risk?

Strategies include OEM residual-value guarantees, battery-health monitoring, longer holding periods, and monetizing idle EVs through vehicle-to-grid programs.