Market Size of Global Artificial Organ Industry

| Study Period | 2019 - 2029 |

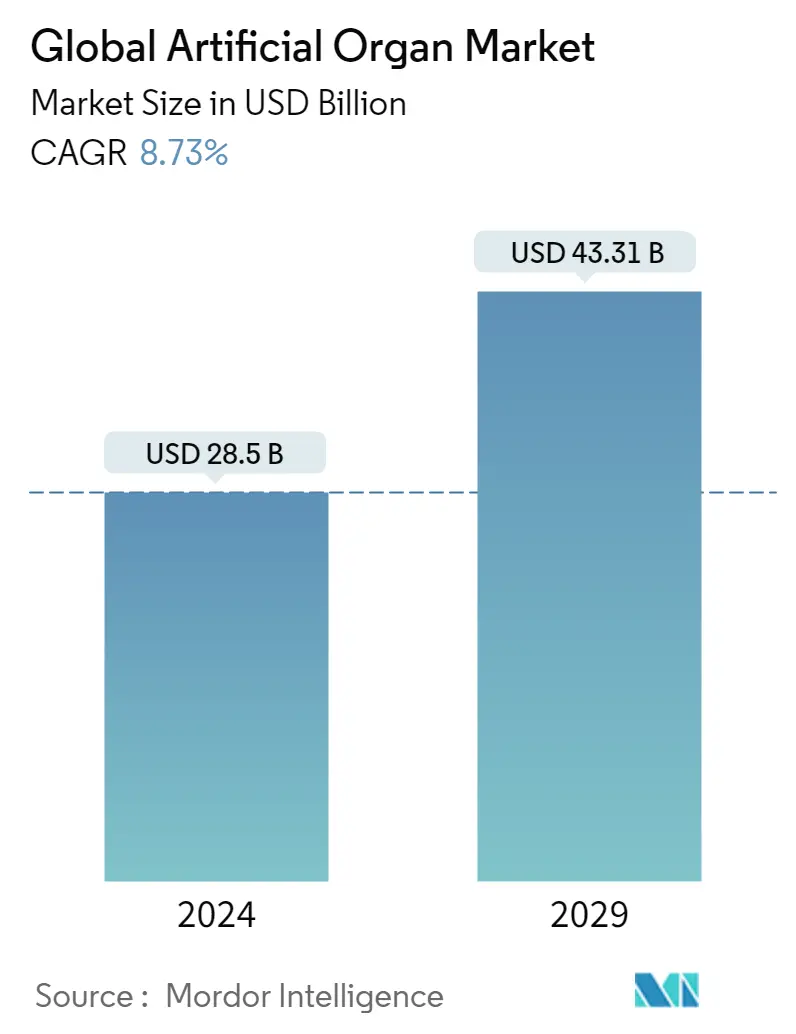

| Market Size (2024) | USD 28.50 Billion |

| Market Size (2029) | USD 43.31 Billion |

| CAGR (2024 - 2029) | 8.73 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players*Disclaimer: Major Players sorted in no particular order |

Artificial Organ Market Analysis

The Global Artificial Organ Market size is estimated at USD 28.5 billion in 2024, and is expected to reach USD 43.31 billion by 2029, growing at a CAGR of 8.73% during the forecast period (2024-2029).

In recent times, countries have faced a huge threat of COVID-19. According to the World Health Organization (WHO), coronavirus is an infectious disease, and most people infected with the COVID-19 virus will experience mild to moderate respiratory illness. The study 'Artificial Lung Helps Investigate How COVID-19 Causes Blood Clots,' published in October 2020, demonstrated that SARS-CoV-2 attacked the outside layer of epithelial cells embarked on a lung-on-a-chip device, just like in natural infection. Within a day, the virus had reached the inner layer of endothelial cells and caused considerable damage over subsequent days, indicating the impact of COVID-19 on the lungs. Such use of artificial lungs in research and development studies is expected to expand the scope during the study period, which will impact the market growth. Also, the study 'Impact of COVID-19 on Pacemaker Implant' published in July 2020 stated that a reduction in the pacemaker implant of 73% was observed during the COVID-19 pandemic period affecting the demand for artificial hearts, thereby impacting the market. Therefore, COVID-19 has a significant impact on the market studied.

Factors driving the market include the rising geriatric population, scarcity of donor organs, and technological advancements in the artificial organ sector.

According to an October 2021 update by the World Health Organization (WHO), by 2030, 1 in 6 people worldwide will be 60 years or above. The same source also reports that by 2050, the world's population of people aged 60 years and older will double (2.1 billion), and the number of persons aged 80 years or older is expected to triple between 2020 and 2050 to reach 426 million. As per the same source, it is now low- and middle-income countries that are experiencing the greatest change, and by 2050, two-thirds of the world's population over 60 years will live in low- and middle-income countries.

According to a study published by the British Heart Foundation in January 2022, there were approximately 7.6 million people with heart disease in the United Kingdom and nearly 160,000 deaths yearly. An average of 460 fatalities daily or one death every three minutes happen in the United Kingdom due to cardiovascular disorders (CVDs). Due to the rising burden of cardiovascular diseases, there is an increasing demand for innovative technologies which can decrease the mortality rates associated with heart failure, thereby increasing the demand for artificial hearts during the study period.

Advances in medicine and technology and increased awareness about organ donation and transplantation have contributed to a record number of transplants. Moreover, launching products in the market is a crucial factor driving market growth. For instance, in May 2020, ALung Technologies, Inc. initiated the commercial development of its next-generation artificial lung, which expands the Company's focus on highly efficient gas exchange devices and also broadens its applicable market.

Also, the article 'New Artificial Heart Shows Promising Results in 'Auto-Mode'' published in June 2021, stated that the Carmat Total Artificial Hart (C-TAH) Auto-Mode with built-in pressure sensors effectively produces appropriate physiological responses reflective of changing patients' daily needs and thus provides almost physiological heart replacement therapy. Therefore, such technological innovations in the market will fuel its growth.

Therefore, owing to the aforementioned factors, the studied market is expected to grow significantly during the study period. However, the high cost of treatment and risk associated with them is expected to hinder the market growth during the study period.

Artificial Organ Industry Segmentation

An artificial organ is a medical device implanted or integrated into the body to replicate or augment the natural function of the organ. As per the scope of the report, artificial organs include implantable devices, such as entirely artificial hearts and pacemakers, along with organ support machines, such as dialysis and extracorporeal membrane oxygenation (ECMO) machines. The Artificial Organ Market is segmented by Organ Type (Artificial Heart, Artificial Kidney, Artificial Pancreas, Artificial Lungs, Cochlear Implants, and Other Organ Types) and Geography (North America, Europe, Asia - Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD million) for the above segments.

| By Organ Type | |||||

| |||||

| Artificial Kidney | |||||

| Artificial Pancreas | |||||

| Artificial Lungs | |||||

| Cochlear Implants | |||||

| Other Organ Types |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Global Artificial Organ Market Size Summary

The artificial organs market is poised for significant growth, driven by factors such as the increasing geriatric population, scarcity of donor organs, and technological advancements in the sector. The market is experiencing a surge in demand due to the rising prevalence of chronic diseases, particularly cardiovascular disorders, which necessitate innovative solutions like artificial hearts and lungs. The COVID-19 pandemic has further influenced the market, highlighting the importance of artificial organs in research and treatment, although it also led to a temporary decline in certain procedures like pacemaker implants. The market is characterized by continuous product launches and advancements, with companies focusing on developing next-generation devices to enhance patient outcomes.

North America currently leads the artificial organs market, supported by a robust healthcare infrastructure, high adoption of advanced technologies, and significant investments in research and development. The United States, in particular, is witnessing substantial growth due to the high incidence of heart diseases, driving the demand for artificial hearts and related technologies. The market is moderately competitive, with major players holding significant shares, yet mid-size and smaller companies are gaining traction by offering innovative solutions at competitive prices. Ongoing collaborations and government support, such as grants for developing artificial organs, are expected to further propel market growth, making it a dynamic and evolving industry landscape.

Global Artificial Organ Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Rising Geriatric Population

-

1.2.2 Scarcity of Donor Organs

-

1.2.3 Technological Advancements in the Artificial Organ Sector

-

-

1.3 Market Restraints

-

1.3.1 Expensive Procedures

-

1.3.2 Risks Associated With Artificial Organs

-

-

1.4 Industry Attractiveness - Porter's Five Forces Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION (Market Size by Value - in USD Millions)

-

2.1 By Organ Type

-

2.1.1 Artificial Heart

-

2.1.1.1 Prosthetic Heart Valves

-

2.1.1.2 Ventricular Assist Devices

-

2.1.1.3 Cardiac Pacemakers

-

-

2.1.2 Artificial Kidney

-

2.1.3 Artificial Pancreas

-

2.1.4 Artificial Lungs

-

2.1.5 Cochlear Implants

-

2.1.6 Other Organ Types

-

-

2.2 Geography

-

2.2.1 North America

-

2.2.1.1 United States

-

2.2.1.2 Canada

-

2.2.1.3 Mexico

-

-

2.2.2 Europe

-

2.2.2.1 Germany

-

2.2.2.2 United Kingdom

-

2.2.2.3 France

-

2.2.2.4 Italy

-

2.2.2.5 Spain

-

2.2.2.6 Rest of Europe

-

-

2.2.3 Asia-Pacific

-

2.2.3.1 China

-

2.2.3.2 Japan

-

2.2.3.3 India

-

2.2.3.4 Australia

-

2.2.3.5 South Korea

-

2.2.3.6 Rest of Asia-Pacific

-

-

2.2.4 Middle East & Africa

-

2.2.4.1 GCC

-

2.2.4.2 South Africa

-

2.2.4.3 Rest of Middle East & Africa

-

-

2.2.5 South America

-

2.2.5.1 Brazil

-

2.2.5.2 Argentina

-

2.2.5.3 Rest of South America

-

-

-

Global Artificial Organ Market Size FAQs

How big is the Global Artificial Organ Market?

The Global Artificial Organ Market size is expected to reach USD 28.50 billion in 2024 and grow at a CAGR of 8.73% to reach USD 43.31 billion by 2029.

What is the current Global Artificial Organ Market size?

In 2024, the Global Artificial Organ Market size is expected to reach USD 28.50 billion.