Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 73.39 Billion |

| Market Size (2030) | USD 98.35 Billion |

| Growth Rate (2025 - 2030) | 6.03% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Adhesives Market Analysis by Mordor Intelligence

The Adhesives Market size is estimated at USD 73.39 billion in 2025, and is expected to reach USD 98.35 billion by 2030, at a CAGR of 6.03% during the forecast period (2025-2030). Demand accelerates as packaging automation scales with e-commerce, infrastructure programs prioritize structural bonding, and automakers increase adhesive volumes to support lightweight multi-material designs. Water-borne chemistries dominate because brands must meet VOC limits, yet hot-melt platforms gain share through solvent-free processing and rapid line speeds. Within resins, acrylics continue to rule high-performance applications, while VAE/EVA lines capture construction volumes thanks to flexibility and cost efficiency. Regional dynamics diverge, with Asia-Pacific supplying volume growth and Europe advancing premium, regulation-ready grades.

Key Report Takeaways

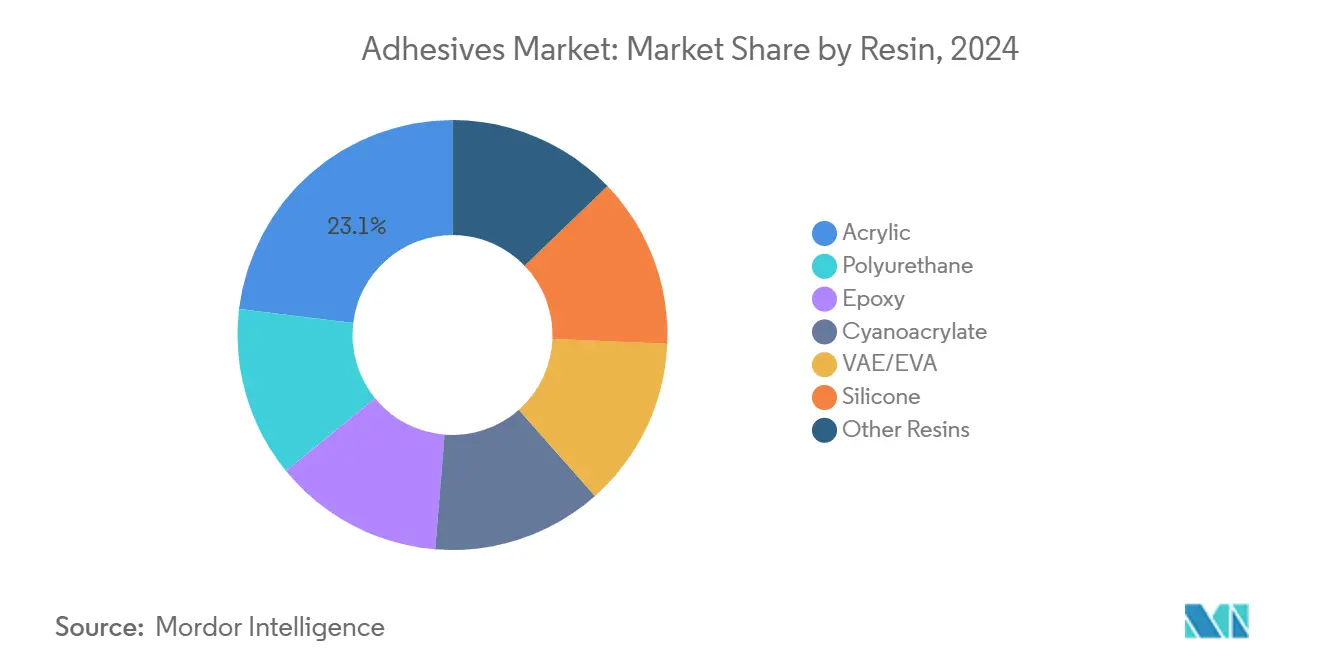

- By resin, acrylic adhesives led with 23.07% revenue share in 2024, and VAE/EVA is forecast to expand at a 6.39% CAGR to 2030.

- By technology, water-borne systems accounted for a 42.52% share of the global adhesives market size in 2024, and hot-melt platforms are projected to grow at a 6.73% CAGR through 2030.

- By end-user, packaging captured 42.80% of the global adhesives market share in 2024, while automotive applications are poised for the fastest 6.40% CAGR to 2030.

- By geography, Asia-Pacific held 36.74% of global revenue in 2024, and Europe is set to record the highest 6.43% CAGR to 2030.

Global Adhesives Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom enlarging demand for secure, high-speed packaging adhesives | +1.2% | Global, strongest in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Global construction upcycle raising consumption of structural and flooring adhesives | +1.8% | Asia-Pacific core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Lightweighting and EV platforms accelerating automotive adhesive penetration | +0.9% | North America and Europe, expanding in Asia-Pacific | Medium term (2-4 years) |

| AI-driven formulation optimisation cutting research and development timelines and bonding costs | +0.7% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Near-shoring of acrylic monomer supply in the United States post-2025 tariffs | +0.4% | North America with global ripple effects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

E-commerce Boom Enlarging Demand for Secure, High-Speed Packaging Adhesives

Online retail warehouses rely on hot-melt and pressure-sensitive grades that cure in milliseconds yet sustain box integrity through conveyor impacts and multi-modal shipping. Fulfilment centers report double-digit order growth, driving 15-20% volume increases for packaging adhesives in key e-commerce corridors. India’s online retail sector alone lifted packaging-adhesive offtake by 18% in 2024 as brand owners mandated tamper-evident bonds suitable for tropical climates. Sustainability goals add momentum for water-borne and bio-sourced options compatible with paper recycling streams. Packagers now specify easily removable grades that leave substrates clean, easing secondary fiber recovery.

Global Construction Upcycle Raising Consumption of Structural and Flooring Adhesives

Megaproject pipelines in Asia-Pacific accelerate uptake of high-strength, fast-set formulations for concrete, steel, and composite bonding where mechanical fasteners are slow or prone to failure. Large-format tiles and pre-fabricated panels need shear-resistant adhesives that shorten installation cycles and enhance structural integrity. Wacker Chemie expanded VAE capacity in Nanjing and Calvert City during 2024 to serve rising construction-adhesive demand in tile and insulation systems. Energy-retrofit incentives in Europe and North America sustain airflow-sealant and insulation-adhesive volumes, while updated building codes champion bonded joints for seismic resilience and thermal-bridge reduction.

Lightweighting and EV Platforms Accelerating Automotive Adhesive Penetration

Each battery-electric vehicle now contains 15-20 kg of specialty adhesives, nearly double that of internal-combustion counterparts. Structural acrylics replace spot welds in aluminum frames, cutting weight and improving crash-energy absorption. Thermally conductive silicone and epoxy grades manage heat within cell packs, as seen in new battery architectures that demand chemical resistance and dielectric strength. Adhesive solutions simplify multi-material joining across carbon fiber, high-strength steel, and composites, aligning with automakers’ CO₂ targets and safety regulations.

Near-Shoring of Acrylic Monomer Supply in the United States

Tariffs enacted in 2025 catalyze new acrylic-acid capacity in the Gulf Coast, shortening supply lines and stabilizing resin pricing for North American adhesive converters. Localized feedstock reduces currency-driven cost swings and freight emissions, while surplus volumes migrate to Latin America, moderating global pricing volatility. Producers expect inventory buffers to drop, freeing working capital and improving service levels for regional customers.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petro-feedstock price volatility squeezing adhesive manufacturer margins | -1.1% | Global, with higher impact in regions dependent on imported feedstocks | Short term (≤ 2 years) |

| Escalating VOC and chemicals regulation curbing solvent-borne adhesive sales | -0.8% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Global shortage of senior adhesive formulators slowing commercialisation cycles | -0.6% | Global, with acute impact in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Petro-Feedstock Price Volatility Squeezing Manufacturer Margins

Crude-linked monomers such as ethylene and propylene account for up to 60% of adhesive raw-material cost. Acrylic-acid prices swung 25-30% during 2024, forcing quarterly surcharges that erode margins, especially for smaller converters without hedging power. Currency shakiness multiplies the burden for firms that source globally but invoice locally. To blunt volatility, producers adopt dual-sourcing and inventory-risk strategies, yet these raise logistics complexity and working-capital needs.

Escalating VOC and Chemicals Regulation Curbing Solvent-Borne Sales

The European Union updated REACH listings in 2025 to include new silicone and phosphite additives, triggering expensive reformulations and potential authorization hurdles[1]SGS, “EU regulates PFHxA and PFHxA-related substances under REACH,” sgs.com . California’s CARB limits and Shanghai’s municipal rules further compress allowable solvent levels, prompting converters to shift toward water-borne, UV, and hot-melt options. PFHxA restrictions under REACH add compliance layers for foam and textile applications, elevating testing costs. Integrated producers with in-house regulatory teams absorb these demands more smoothly, while SMEs face higher per-unit expenses.

Segment Analysis

By Resin: Acrylic Leadership Amid VAE/EVA Acceleration

Acrylic systems held a 23.07% share of the global adhesives market in 2024, supported by weather-resistant performance across construction façades, automotive trim, and pressure-sensitive labels. VAE/EVA lines are growing at a 6.39% CAGR through 2030, propelled by flexible flooring, tile-setting, and packaging-film lamination. Polyurethane grades stay entrenched in transportation and aerospace where high bond strength, chemical resistance, and elasticity are critical. Epoxies serve electronics and wind-blade joints that face extreme heat and fatigue, though their growth lags due to longer cure cycles. Hybrid chemistries now combine acrylic UV resistance with polyurethane toughness or VAE flexibility with epoxy rigidity, widening formulator toolkits.

Continuous resin innovation keeps the global adhesives market expanding as converters fine-tune performance for specific substrates and service environments. Acrylic players invest in self-crosslinking emulsions that boost water whitening resistance, while VAE suppliers ramp polar-monomer content to enhance adhesion to low-surface-energy films. Demand for bio-based feedstocks rises, yet cost and supply scalability limit rapid penetration. Strategic resin selection increasingly balances regulatory compliance, service temperature, and total applied cost, enabling manufacturers to differentiate within commoditized end uses.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Technology: Water-Borne Dominance Challenged by Hot-Melt Innovation

Water-borne platforms commanded a 42.52% share in 2024, underpinning the global adhesives market through their low-VOC profile and compatibility with automated coating lines. Hot-melt systems, however, exhibit the fastest 6.73% CAGR to 2030 as packagers chase instant green strength and solvent-free processing that eliminates drying zones. Reactive chemistries, including polyurethanes and silane-terminated polymers, retain niche strength in structural bonding where aging resistance and environmental durability are paramount.

UV-cured technologies grow in electronics, medical, and optical devices thanks to pinpoint curing that avoids thermal stress. Solvent-borne volumes continue to decline under stricter emission caps, although they remain relevant for porous substrates needing deep penetration and extended open time. Technology choice is increasingly dictated by lifecycle footprint and operator safety rather than unit cost. As LED lamps reduce energy draw and expand UV-curing window profiles, converters re-evaluate capital projects to boost throughput while edging closer to net-zero targets.

By End-User Industry: Packaging Scale Versus Automotive Innovation

Packaging applications captured 42.80% of revenue in 2024, reinforcing the global adhesives market as corrugated converters and flexible-film laminators cater to online retail and consumer-goods demand. Brands now specify repulpable, compostable, or easily delaminated bonds to meet circular-economy goals. Automotive use cases are projected to grow at 6.40% CAGR through 2030 as battery-electric platforms multiply bonding points in body-in-white, battery, and interior modules. Building and construction form a consistent third pillar, driven by sealants for insulation, façade cladding, and flooring.

Aerospace remains a high-margin niche where certification barriers and performance extremes anchor volumes. Healthcare applications benefit from aging populations and minimally invasive devices that rely on skin-friendly or sterilization-stable grades. Woodworking and footwear segments experience mixed fortunes as synthetic substrates rise, yet artisan and high-performance niches sustain premium offerings.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Asia-Pacific holds 36.74% of the global adhesives market thanks to concentrated manufacturing clusters and public infrastructure spending across China, India, and Southeast Asia. China’s urban rail and residential projects spur demand for structural acrylics, while India’s tile-adhesive segment grows more than 15% annually on rapid urban housing. Regional suppliers, including new Henkel and tesa plants, enhance local availability and cut lead times. Overcapacity concerns persist, particularly in EVA and acrylic emulsions, where planned expansions risk surplus inventory if downstream uptake slows.

Europe is forecast to post the fastest 6.43% CAGR through 2030 as regulations push converters toward recyclable, low-emission systems. The EU Packaging and Packaging Waste Regulation, effective in 2026, will require adhesives that separate cleanly in mechanical recycling streams and eliminate PFAS content[2]European Parliament, “Texts adopted – Packaging and packaging waste,” europarl.europa.eu . Germany’s EV transition drives demand for thermally conductive and flame-retardant adhesives, while France’s building-retrofit subsidies stimulate insulation-bond volumes.

North America records steady momentum as tariff-induced monomer investments bolster supply security. Gulf Coast acrylic-acid capacity coming online from 2025 lessens reliance on imports and supports regional formulators with shorter transit times. Mexico’s role as an automotive export hub lifts demand for structural and hem-flange bonding systems, whereas Canada’s cold-weather construction codes favor freeze-resistant adhesives for panelized housing. The trajectory hinges on infrastructure-bill progress and automotive production cycles but remains positive amid reshoring and sustainability commitments.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The global adhesives market is fragmented. Henkel, 3M, and Sika leverage integrated resin supply, regional plants, and technical service labs to secure key accounts. Mid-tier specialists target niches such as medical devices, EV battery sealing, and extreme-temperature aerospace applications where deep formulation know-how commands premiums. Commodity segments endure price rivalry that triggers consolidation among smaller firms lacking feedstock leverage. Disruptors deploy modular reactors and cloud-based design platforms to prototype custom bonds quickly, challenging incumbents in high-mix, low-volume spaces. Future battlegrounds include EV thermal management, fully recyclable packaging, and construction adhesives tolerant of extreme climates.

Adhesives Industry Leaders

-

3M

-

H.B. Fuller Company

-

Henkel AG & Co. KGaA

-

Sika AG

-

Arkema

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: Henkel opened an Application Engineering Center in Chennai and confirmed a new electronics-adhesive plant at its Kurkumbh site in Maharashtra.

- January 2024: Saint-Gobain completed the USD 1.2 billion acquisition of FOSROC International, expanding construction chemicals and adhesive technologies across Asia-Pacific and the Middle East.

Global Adhesives Market Report Scope

Aerospace, Automotive, Building and Construction, Footwear and Leather, Healthcare, Packaging, Woodworking and Joinery are covered as segments by End User Industry. Hot Melt, Reactive, Solvent-borne, UV Cured Adhesives, Water-borne are covered as segments by Technology. Acrylic, Cyanoacrylate, Epoxy, Polyurethane, Silicone, VAE/EVA are covered as segments by Resin. Asia-Pacific, Europe, Middle East & Africa, North America, South America are covered as segments by Region.

By Resin

| Polyurethane |

| Epoxy |

| Acrylic |

| Cyanoacrylate |

| VAE/EVA |

| Silicone |

| Other Resins |

By Technology

| Water-borne |

| Solvent-borne |

| Reactive |

| Hot Melt |

| UV Cured Adhesives |

By End-user Industry

| Building and Construction |

| Packaging |

| Automotive |

| Aerospace |

| Woodworking and Joinery |

| Footwear and Leather |

| Healthcare |

| Other End-user Industries |

By Geography

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Malaysia | |

| Singapore | |

| Thailand | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Resin | Polyurethane | |

| Epoxy | ||

| Acrylic | ||

| Cyanoacrylate | ||

| VAE/EVA | ||

| Silicone | ||

| Other Resins | ||

| By Technology | Water-borne | |

| Solvent-borne | ||

| Reactive | ||

| Hot Melt | ||

| UV Cured Adhesives | ||

| By End-user Industry | Building and Construction | |

| Packaging | ||

| Automotive | ||

| Aerospace | ||

| Woodworking and Joinery | ||

| Footwear and Leather | ||

| Healthcare | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Malaysia | ||

| Singapore | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Need A Different Region or Segment?

Customize Now

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the adhesives market.

- Product - All adhesive products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF