| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 4.00 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Glass Substrates Market Analysis

The Glass Substrate Market is expected to register a CAGR of greater than 4% during the forecast period.

The glass substrate industry is experiencing significant transformation driven by technological advancements in consumer electronics and display glass technologies. The integration of advanced display technologies in smartphones and other consumer devices continues to evolve, with global smartphone adoption projected to reach 79% by 2025, creating sustained demand for high-quality glass substrates. This evolution has prompted manufacturers to invest in research and development of innovative specialty glass formulations that offer enhanced durability, improved optical properties, and better thermal stability.

The telecommunications sector has emerged as a crucial growth catalyst for the glass substrate market, particularly with the ongoing global 5G network deployment. With 5G mobile subscriptions expected to reach 3,515 million by 2026, there is increasing demand for specialized electronic glass substrates in advanced antenna systems and network infrastructure components. The industry is witnessing a shift toward thinner, more durable thin glass substrates that can meet the stringent requirements of next-generation telecommunications equipment while maintaining optimal performance characteristics.

The electronics industry continues to dominate the glass substrate market, driven by the proliferation of advanced display technologies and semiconductor applications. Manufacturers are increasingly focusing on developing ultra-thin electronic display glass substrates that can support higher pixel densities and improved display performance while reducing overall device thickness. This trend is particularly evident in the development of flexible and foldable display technologies, where specialized advanced glass substrates play a crucial role in ensuring durability and optimal optical performance.

The Asia-Pacific region has established itself as the global manufacturing hub for glass substrates, supported by the presence of major electronics manufacturers and robust supply chain infrastructure. The industry is witnessing significant investments in advanced manufacturing facilities, particularly in countries like China, Japan, and South Korea. These investments are focused on expanding production capacity and implementing advanced manufacturing technologies to meet the growing demand for high-quality specialty glass substrates across various applications, including consumer electronics, automotive displays, and telecommunications equipment.

Glass Substrates Market Trends

Growing Electronics Industry and Semiconductor Applications

The glass substrate market is experiencing substantial growth driven by its extensive applications across the electronics industry, particularly in semiconductor glass manufacturing. The material's versatility enables its use in crucial electronic components, including complementary metal-oxide-semiconductor (CMOS), micro-electro-mechanical systems (MEMS), image sensors, LEDs, logic ICs, power components, micro-batteries, and optoelectronics. This broad application spectrum has made specialty glass substrates an indispensable material in the electronics manufacturing sector, with demand rising as manufacturers seek high-performance, reliable materials for increasingly complex electronic devices.

The electronics manufacturing landscape is undergoing significant transformation with the increasing presence of Original Equipment Manufacturers (OEMs) globally. These manufacturers are rapidly digitizing their operations to achieve end-to-end integration, leading to increased demand for high-quality technical glass substrates. The trend toward outsourcing production has further amplified this demand, as companies seek cost-effective yet high-performance materials for their electronic components. Additionally, the low cost and high availability of raw materials, coupled with advancing manufacturing capabilities, have made precision glass substrates an attractive choice for electronics manufacturers looking to optimize their production processes while maintaining product quality.

Understand The Key Trends Shaping This Market

Download PDF

Expanding Healthcare and Medical Device Manufacturing

The healthcare sector's technological advancement has emerged as a significant driver for the glass substrate market, particularly in the manufacturing of sophisticated medical devices and equipment. The increasing focus on developing high-tech medical devices for treating chronic and age-related diseases has created substantial demand for advanced glass substrates, which are essential components in various medical imaging and diagnostic equipment. The material's unique properties, including its stability, transparency, and compatibility with biological materials, make it ideal for medical device applications.

The medical devices sector is witnessing unprecedented growth, with governments worldwide prioritizing health innovation and increasing investments in medical device manufacturing. This growth is particularly evident in the development of advanced diagnostic equipment, monitoring devices, and therapeutic instruments, all of which require high-quality technical glass substrates. The trend toward miniaturization and increased functionality in medical devices has further accelerated the demand for specialized precision glass substrates that can support these advanced applications while maintaining reliability and performance standards. The integration of electronic components in medical devices, from simple monitoring equipment to complex diagnostic tools, continues to drive innovation in semiconductor glass substrate technology and manufacturing.

Rising Demand for Consumer Electronics and Advanced Technologies

The proliferation of consumer electronics and the continuous evolution of technology have created sustained demand for electronic glass substrates in various applications. The material plays a crucial role in manufacturing displays, sensors, and other components essential for smartphones, tablets, wearable devices, and other consumer electronic products. The advancement of technologies such as 5G, the Internet of Things (IoT), and artificial intelligence has further intensified the need for high-performance specialty glass substrates that can support these sophisticated applications while meeting stringent quality and reliability requirements.

The trend toward more integrated and multifunctional devices has led to increased complexity in electronic component design and manufacturing, driving innovation in glass substrate technology. Manufacturers are developing advanced glass substrate that can support higher component density, improved performance, and enhanced durability while maintaining cost-effectiveness. The growing demand for smart devices and connected technologies has also spurred the development of specialized precision glass substrates that can accommodate various sensors, processors, and communication components within increasingly compact form factors. This technological evolution continues to create new opportunities and applications for glass substrate in the consumer electronics sector.

Segment Analysis: By Application

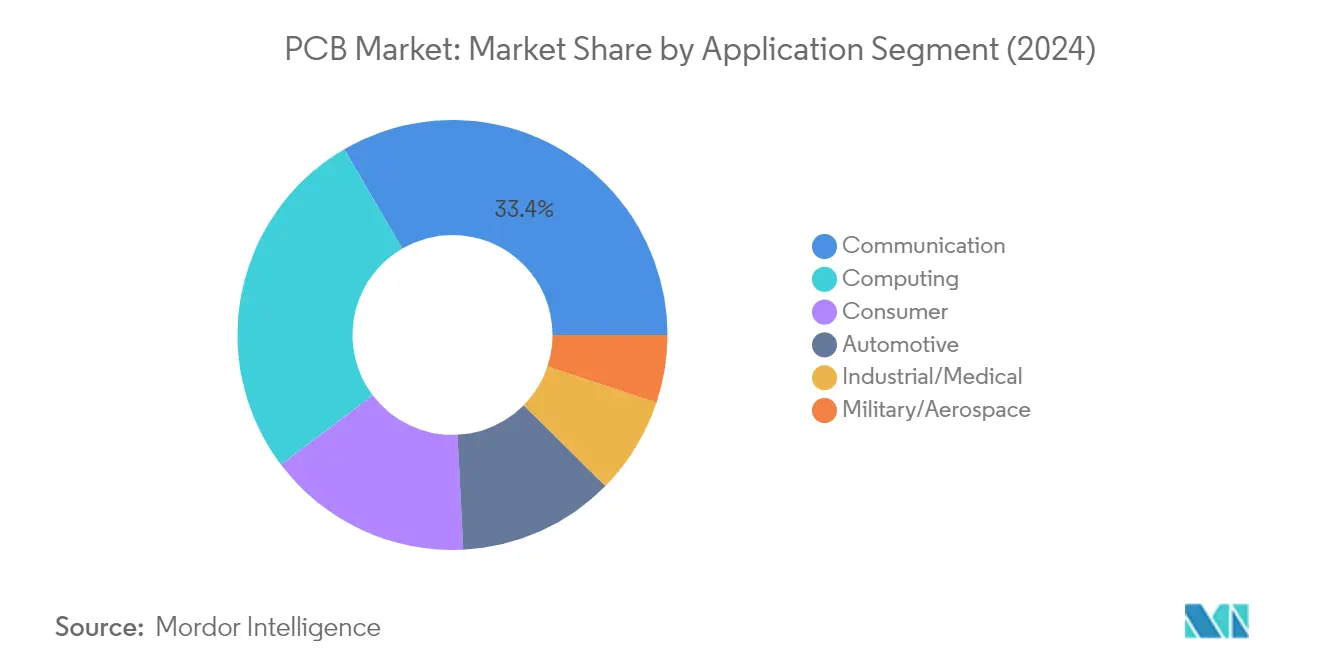

Communication Segment in PCB Market

The communication segment maintains its dominant position in the global PCB market, commanding approximately 33% market share in 2024. This significant market presence is driven by the increasing deployment of wireless networks, including Wi-Fi, WiMAX, and ultra-wideband technologies, which require both centralized and decentralized base stations and complex telecommunication network infrastructure. The segment's growth is further bolstered by the rising trends in virtualization and cloud computing that are driving up internet traffic globally, leading to improved infrastructure spending by service providers. PCBs play a crucial role in various communication network infrastructure equipment, from wireline and enterprise network equipment to data center servers and subscriber equipment.

Automotive Segment in PCB Market

The automotive segment is emerging as the fastest-growing sector in the PCB market, with a projected growth rate of approximately 5% during 2024-2029. This accelerated growth is primarily driven by the increasing incorporation of electronics in vehicles, particularly in advanced driver assistance systems (ADAS), electric vehicle powertrains, and infotainment systems. The segment's expansion is further fueled by stringent safety regulations mandating the implementation of electronic safety features in vehicles, alongside the growing demand for hybrid and battery electric vehicles. The trend toward autonomous driving and connected vehicles is creating additional demand for sophisticated PCBs that can support complex electronic systems while maintaining reliability in harsh automotive environments. Additionally, the use of electronic glass in automotive displays is becoming more prevalent, enhancing the functionality and aesthetics of vehicle interiors.

Remaining Segments in PCB Market

The computing segment represents a substantial portion of the market, primarily driven by data centers, high-power computing, and edge computing applications. The consumer electronics segment continues to evolve with the integration of PCBs in smartphones, personal computers, and home appliances. The industrial/medical segment showcases steady growth through applications in manufacturing equipment and medical devices, while the military/aerospace segment, though smaller, maintains its significance through specialized applications requiring high-reliability PCBs for critical defense and space applications. Each of these segments contributes uniquely to the market's diversity and overall growth trajectory. The use of LCD glass and TFT glass in consumer electronics is notable, as these materials are integral to the development of high-definition displays and touchscreens.

Segment Analysis: By Applications

Communication Segment in PCB Market

The communication segment dominates the global PCB market, commanding approximately 33% market share in 2024. This segment's prominence is driven by the increasing deployment of wireless networks, including Wi-Fi, WiMAX, and ultra-wideband technologies, which require both centralized and decentralized base stations and complex telecommunication network infrastructure. The rising trends in virtualization and cloud computing are driving up internet traffic globally, leading to improved infrastructure spending by service providers. PCBs play a crucial role in various communication network infrastructure equipment, from wireline network equipment to enterprise network equipment, data center servers, subscriber equipment, and cable/multiservice operator equipment.

Automotive Segment in PCB Market

The automotive segment is emerging as the fastest-growing segment in the PCB market, with a projected growth rate of approximately 5% during 2024-2029. This remarkable growth is attributed to the increasing incorporation of electronics in vehicles, particularly in advanced driver assistance systems (ADAS), electric vehicle powertrains, and infotainment systems. The segment's growth is further fueled by stringent safety regulations and the rising adoption of electric and hybrid vehicles. The automotive industry's shift toward autonomous driving capabilities, connected vehicle technologies, and electrification is creating unprecedented demand for sophisticated PCBs that can withstand harsh automotive environments while delivering reliable performance. The integration of OLED glass in vehicle displays is enhancing the visual experience and functionality of automotive interfaces.

Remaining Segments in PCB Market

The PCB market encompasses several other significant segments including computing, consumer electronics, industrial/medical, and military/aerospace. The computing segment remains crucial for data centers and high-performance computing applications, while the consumer electronics segment drives innovation in smartphones, tablets, and wearable devices. The industrial/medical segment serves critical applications in manufacturing automation and healthcare devices, benefiting from Industry 4.0 initiatives. The military/aerospace segment, though smaller, maintains its importance in specialized applications requiring high-reliability PCBs for defense and space applications, contributing to the market's overall technological advancement and diversification. The use of glass substrate in these applications is critical for ensuring the durability and performance of electronic components.

Glass Substrates Industry Overview

Top Companies in Glass Substrate Market

The glass substrate market is characterized by significant investments in research and development activities, with leading companies focusing on developing advanced manufacturing processes and innovative product offerings. Companies in the specialty glass industry are increasingly emphasizing operational agility through strategic manufacturing locations and automated production facilities to meet evolving customer demands. Major players are expanding their geographical presence through strategic partnerships, acquisitions, and the establishment of new production facilities, particularly in emerging Asian markets. The industry witnesses continuous technological advancement in areas like miniaturization, functional integration, and performance enhancement, with companies investing in next-generation manufacturing capabilities. Market leaders are also strengthening their positions through vertical integration and the development of specialized solutions for high-growth applications like 5G, automotive electronics, and IoT devices.

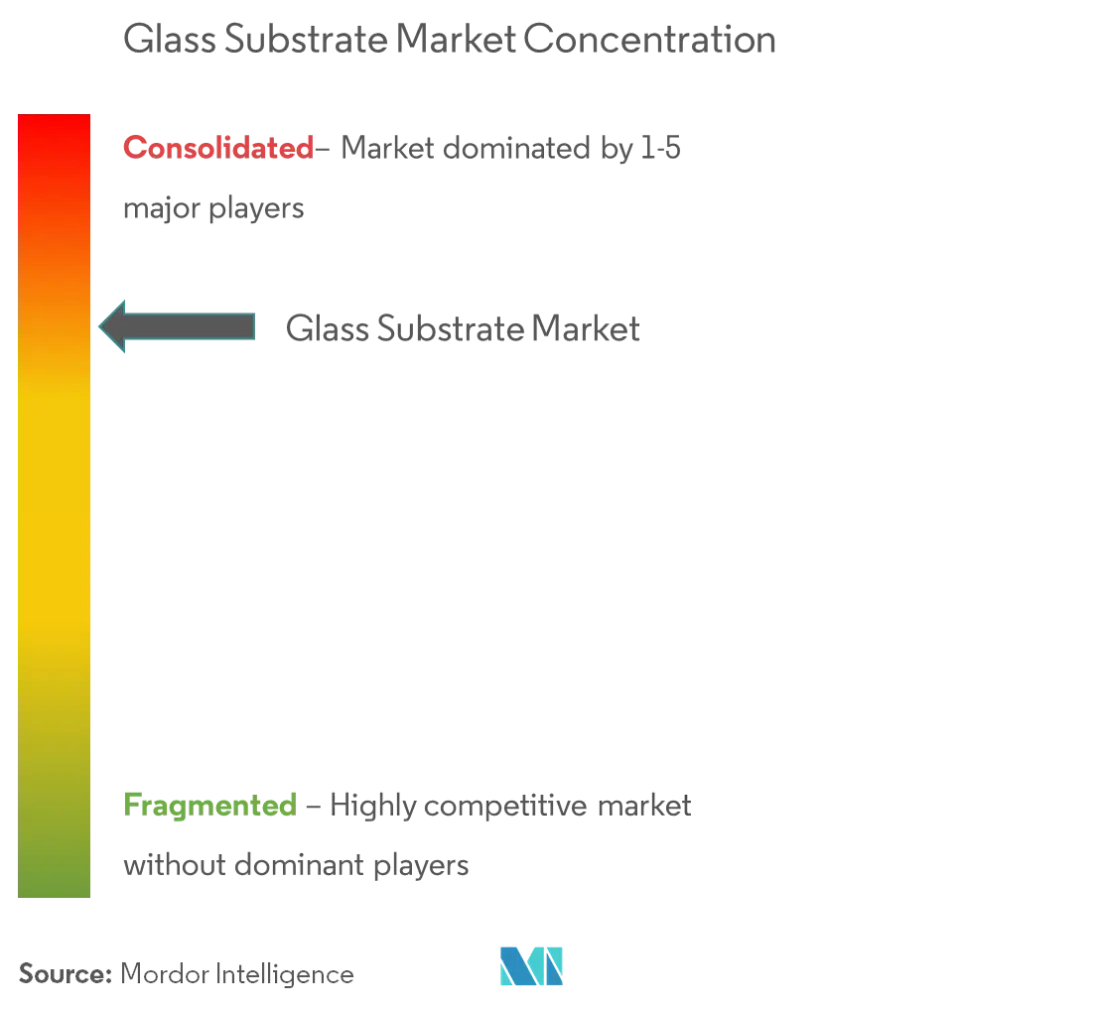

Consolidated Market with Strong Regional Players

The market structure exhibits a mix of global conglomerates and specialized regional manufacturers, with Asian companies, particularly from Japan, South Korea, and Taiwan, holding significant market share. These established players leverage their technological expertise, extensive manufacturing capabilities, and strong customer relationships to maintain their competitive positions. The specialty glass market is experiencing ongoing consolidation through strategic mergers and acquisitions, as companies seek to expand their technological capabilities, achieve economies of scale, and strengthen their market presence in key regions.

The competitive landscape is characterized by high entry barriers due to substantial capital requirements, technical expertise needs, and established customer relationships. Major players are increasingly focusing on developing comprehensive solution portfolios rather than standalone products, while also investing in advanced manufacturing processes and quality control systems. The market shows a trend toward strategic collaborations between manufacturers and end-users, particularly in emerging applications like flexible electronics and advanced packaging solutions.

Innovation and Adaptability Drive Market Success

Success in the advanced glass industry increasingly depends on companies' ability to innovate and adapt to rapidly evolving technological requirements and customer demands. Market leaders are strengthening their positions through investments in advanced manufacturing capabilities, development of proprietary technologies, and expansion of their product portfolios to serve diverse applications. Companies are also focusing on building strong relationships with key customers in high-growth sectors, while maintaining flexibility to address changing market dynamics and technological requirements.

For new entrants and smaller players, success lies in identifying and focusing on specific market niches where they can develop specialized expertise and competitive advantages. Companies need to carefully manage their exposure to end-user concentration risks while maintaining sufficient scale to remain competitive in terms of cost and technology. The regulatory environment, particularly regarding environmental standards and quality requirements, continues to influence market dynamics and competitive strategies, with successful companies demonstrating strong compliance capabilities and sustainable practices.

Glass Substrates Market Leaders

-

AGC Inc.

-

Nippon Electric Glass Co., Ltd.

-

SCHOTT AG

-

Corning Incorporated

-

LG Chem

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Glass Substrates Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Growing Usage of LCDs in Consumer Electronics

- 4.1.2 Other Drivers

-

4.2 Restraints

- 4.2.1 Unfavorable Conditions Arising Due to COVID-19 Outbreak

- 4.2.2 High Manufacturing Costs

- 4.3 Industry Value Chain Analysis

-

4.4 Porters Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION

-

5.1 Type

- 5.1.1 Borosilicate

- 5.1.2 Silicon

- 5.1.3 Ceramic

- 5.1.4 Quartz

- 5.1.5 Others

-

5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.2 Aerospace and Defense

- 5.2.3 Healthcare

- 5.2.4 Solar Power

- 5.2.5 Electronics

- 5.2.6 Others

-

5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)/Ranking Analysis**

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 AGC Inc.

- 6.4.2 AvanStrate Inc.

- 6.4.3 Corning Incorporated

- 6.4.4 HOYA GROUP

- 6.4.5 IRICO Group New Electronics Company Limited

- 6.4.6 LG Chem

- 6.4.7 Nippon Electric Glass Co.,Ltd.

- 6.4.8 Nitta Haas Incorporated

- 6.4.9 SCHOTT AG

- 6.4.10 The Tunghsu Group

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Glass Substrates Industry Segmentation

The Glass Substrate market report includes:

| Type | Borosilicate | ||

| Silicon | |||

| Ceramic | |||

| Quartz | |||

| Others | |||

| End-user Industry | Automotive | ||

| Aerospace and Defense | |||

| Healthcare | |||

| Solar Power | |||

| Electronics | |||

| Others | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Glass Substrates Market Research FAQs

What is the current Glass Substrate Market size?

The Glass Substrate Market is projected to register a CAGR of greater than 4% during the forecast period (2025-2030)

Who are the key players in Glass Substrate Market?

AGC Inc., Nippon Electric Glass Co., Ltd., SCHOTT AG, Corning Incorporated and LG Chem are the major companies operating in the Glass Substrate Market.

Which is the fastest growing region in Glass Substrate Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Glass Substrate Market?

In 2025, the Asia Pacific accounts for the largest market share in Glass Substrate Market.

What years does this Glass Substrate Market cover?

The report covers the Glass Substrate Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Glass Substrate Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Glass Substrate Market Research

Mordor Intelligence provides a comprehensive analysis of the glass substrate market. We leverage our extensive expertise in the specialty glass and advanced glass industries. Our detailed report examines various segments, including borosilicate glass, precision glass, and technical glass applications across multiple sectors. The analysis covers crucial developments in electronic glass technology, such as LCD, OLED, and TFT glass implementations. It also addresses emerging applications in the semiconductor glass and photovoltaic glass sectors.

Stakeholders gain valuable insights through our thorough examination of display glass trends, cover glass innovations, and thin glass technologies. The report is available as an easy-to-download PDF and provides detailed analysis of specialty glass industry developments and advanced glass market size metrics. Our research encompasses the entire value chain, from electronic display glass manufacturing to end-user applications. This offers stakeholders a comprehensive understanding of both established and emerging market dynamics in the advanced glass industry. The analysis particularly focuses on photovoltaic glass market opportunities and innovations in the display glass market, providing actionable intelligence for strategic decision-making.