Market Size of Germany Health And Medical Insurance Industry

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

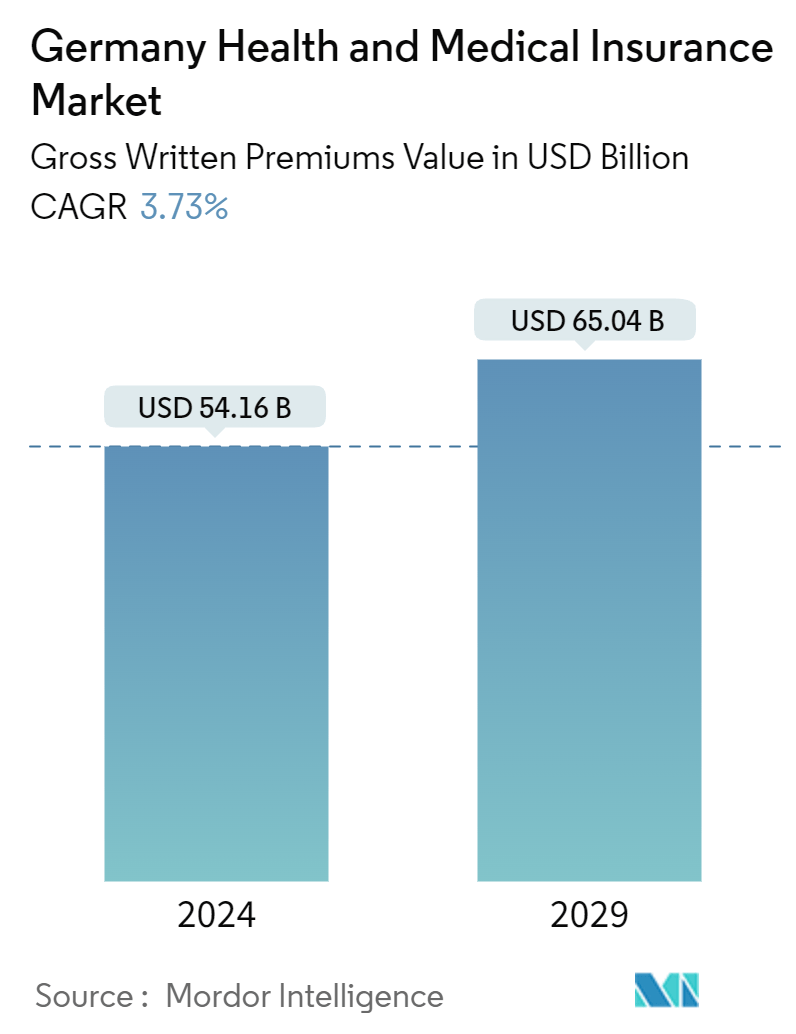

| Market Size (2024) | USD 54.16 Billion |

| Market Size (2029) | USD 65.04 Billion |

| CAGR (2024 - 2029) | 3.73 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Germany Health & Medical Insurance Market Analysis

The Germany Health And Medical Insurance Market size in terms of gross written premiums value is expected to grow from USD 54.16 billion in 2024 to USD 65.04 billion by 2029, at a CAGR of 3.73% during the forecast period (2024-2029).

The COVID-19 pandemic affected the German health and medical insurance industry, as there was an increase in claims during the pandemic. Moreover, some companies leveraged the challenge into an opportunity by inducing insurance policies related to the pandemic in their portfolios.

Health insurance is mandatory in Germany. Approximately 86 percent of the population is enrolled in statutory health insurance, which provides inpatient, outpatient, mental health, and prescription drug coverage. The administration is handled by nongovernmental insurers known as sickness funds. The government has virtually no role in the direct delivery of health care. Sickness funds are financed through general wage contributions (14.6%) and a dedicated supplementary contribution (1% of wages, on average), both shared by employers and workers. Copayments apply to inpatient services and drugs, and sickness funds offer a range of deductibles. Germans earning more than USD 68,000 can opt out of SHI and choose private health insurance instead. There are no government subsidies for private insurance.

The market is driven by an increase in the overall health expenditure and rising medical costs, rising disposable incomes across different economic classes, increasing stress on the public to attain Universal Health Care coverage to meet all kinds of healthcare needs, increasing demand from the healthcare sector, population growth, demographic shifts, and the unhealthy lifestyle of the public.

The increased use of modern technologies to improve claim management services allows insurance firms to speed up the patient's payment lifecycle more efficiently and prevent fraudulent claim settlement activities. In addition, an increase in the number of diseases and accidents and a rise in awareness of health insurance in rural regions are driving the industry forward. Many operational challenges within the private insurance sector lead to inequalities in healthcare coverage.

Germany Health & Medical Insurance Industry Segmentation

Health insurance is an insurance product that covers an insured individual's medical and surgical expenses. It reimburses the expenses incurred due to illness or injury or pays the care provider of the insured individual directly. Medical insurance offers limited coverage for hospitalization expenses and treatment for pre-specified ailments and accidents. Medical insurance does not offer any add-on coverage like health insurance. The report covers a complete background analysis of the German health and medical insurance industry, which includes an assessment of the national health accounts and economy, emerging market trends by segments, significant changes in market dynamics, and a market overview.

Germany's health and medical insurance market is segmented by product type (statutory health insurance, private health insurance), term of coverage (short-term, long-term), channel of distribution (single-tied or insurance group intermediaries, brokers and multiple agents, credit institutions, direct selling, other channels of distribution), and income level (employed annual income less than EUR 64,350, employed annual income greater than EUR 64,350, self-employed, civil servants).

The market size and forecasts are provided in terms of value (USD) for all the above segments.

| By Product Type | |

| Statutory Health Insurance | |

| Private Health Insurance |

| By Term of Coverage | |

| Short-term | |

| Long-term |

| By Channel of Distribution | |

| Single Tied or Insurance Group Intermediaries | |

| Broker and Multiple Agents | |

| Credit Institutions | |

| Direct Selling | |

| Other Channels of Distribution |

| By Income Level | |

| Employed Annual Income < EUR 64,350 | |

| Employed Annual Income > EUR 64,350 | |

| Self-employed | |

| Civil Servants |

Germany Health And Medical Insurance Market Size Summary

The health and medical insurance market in Germany is poised for significant growth over the forecast period, driven by various factors including rising health expenditures, increasing medical costs, and demographic shifts. The mandatory health insurance system in Germany, primarily through statutory health insurance (SHI), covers a vast majority of the population, with private insurance options available for those with higher incomes. The market is experiencing a transformation due to the integration of modern technologies such as artificial intelligence and machine learning, which are enhancing claim management processes and improving the efficiency of insurance operations. The adoption of wearable devices is also contributing to market expansion by providing insurers with valuable health data, thereby streamlining claim processing and offering more personalized insurance solutions.

Legislative changes and technological advancements are key drivers of the German health and medical insurance market's growth. Recent reforms have facilitated the use of telemedicine and electronic health records, which are expected to enhance healthcare delivery and insurance coverage. The market is characterized by the presence of major players like AOK, Techniker Krankenkasse, and Allianz, who dominate the landscape, although mid-size and smaller companies are increasingly gaining market share through innovation and strategic partnerships. The ongoing development of new technologies and the focus on improving healthcare solutions are likely to sustain the market's growth trajectory, with significant investments in research and development playing a crucial role in shaping the future of health insurance in Germany.

Germany Health And Medical Insurance Market Size - Table of Contents

-

1. MARKET DYNAMICS AND INSIGHTS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.3 Market Restraints

-

1.4 Industry Attractiveness: Porter's Five Forces Analysis

-

1.4.1 Bargaining Power of Suppliers

-

1.4.2 Bargaining Power of Buyers

-

1.4.3 Threat of New Entrants

-

1.4.4 Threat of Substitutes

-

1.4.5 Intensity of Competitive Rivalry

-

-

1.5 Insights into Technological Advancements in the Industry

-

1.6 Insights on Various Regulatory Trends Shaping the Market

-

1.7 Insights on Statutory Health Insurance (SHI) and the Factors Considered by Germans to Procure any Private Health Insurance (PHI)

-

1.8 Impact of COVID-19 on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Product Type

-

2.1.1 Statutory Health Insurance

-

2.1.2 Private Health Insurance

-

-

2.2 By Term of Coverage

-

2.2.1 Short-term

-

2.2.2 Long-term

-

-

2.3 By Channel of Distribution

-

2.3.1 Single Tied or Insurance Group Intermediaries

-

2.3.2 Broker and Multiple Agents

-

2.3.3 Credit Institutions

-

2.3.4 Direct Selling

-

2.3.5 Other Channels of Distribution

-

-

2.4 By Income Level

-

2.4.1 Employed Annual Income < EUR 64,350

-

2.4.2 Employed Annual Income > EUR 64,350

-

2.4.3 Self-employed

-

2.4.4 Civil Servants

-

-

Germany Health And Medical Insurance Market Size FAQs

How big is the Germany Health and Medical Insurance Market?

The Germany Health and Medical Insurance Market size is expected to reach USD 54.16 billion in 2024 and grow at a CAGR of 3.73% to reach USD 65.04 billion by 2029.

What is the current Germany Health and Medical Insurance Market size?

In 2024, the Germany Health and Medical Insurance Market size is expected to reach USD 54.16 billion.