Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

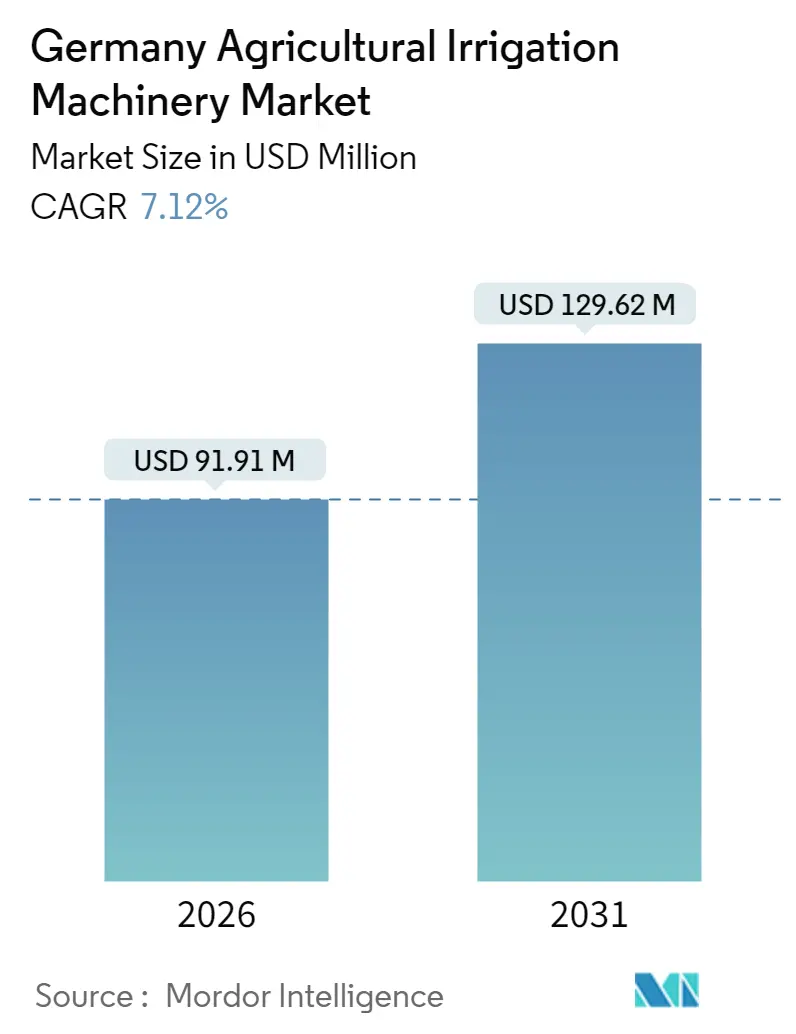

| Market Size (2026) | USD 91.91 Million |

| Market Size (2031) | USD 129.62 Million |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Agricultural Irrigation Machinery Market Analysis by Mordor Intelligence

Germany agricultural irrigation machinery market size in 2026 is estimated at USD 91.91 million, growing from 2025 value of USD 85.80 million with 2031 projections showing USD 129.62 million, growing at 7.12% CAGR over 2026-2031. The market's growth is driven by a record drought in spring 2025, which reduced rainfall between February and mid-April to 40 millimeters, a significant percentage below the 1991-2020 average. This prompted growers to consider irrigation equipment as a necessity rather than an option. Climate-smart subsidies are allocated for water-efficient technologies, thereby increasing demand for drip and fully automated systems. Other factors contributing to market expansion include the rapid growth of greenhouses in North Rhine-Westphalia and Bavaria, rising groundwater salinity in coastal plains, and labor shortages caused by a declining agricultural workforce. Competitive dynamics are evolving as manufacturers integrate hardware with cloud-based decision support systems, generating subscription-based revenue and enhancing brand loyalty.

Key Report Takeaways

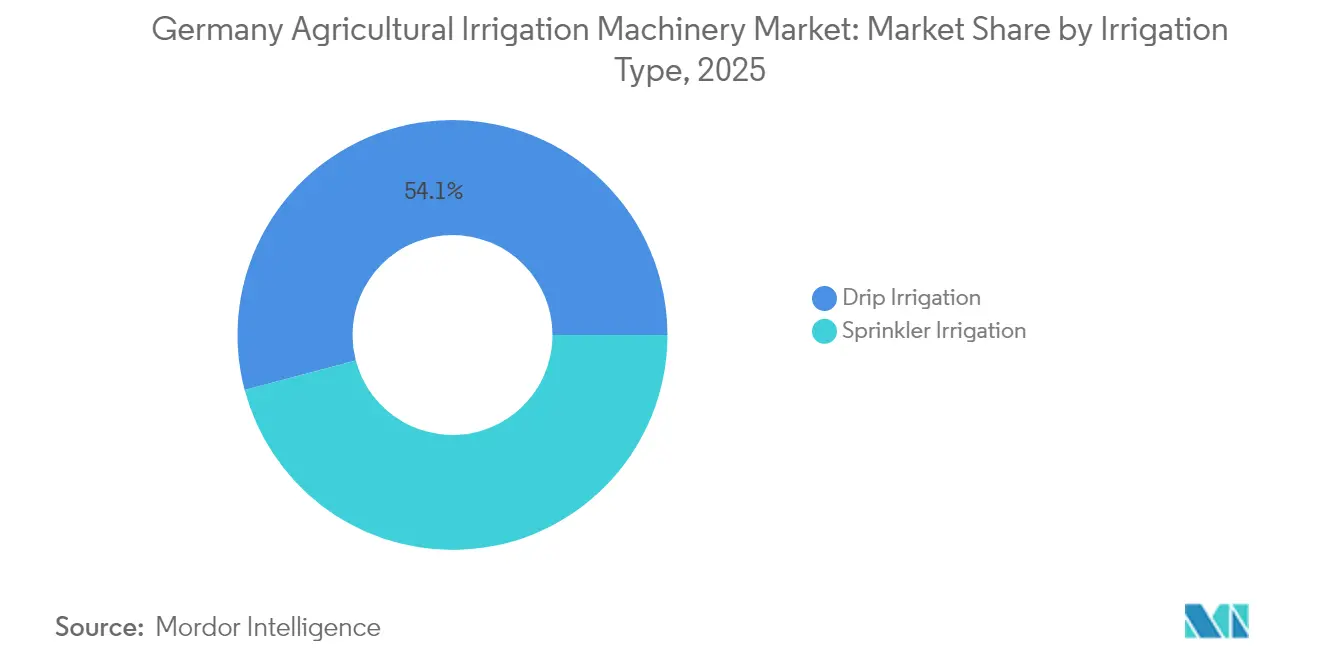

- By irrigation type, drip systems held 54.12% of Germany agricultural irrigation machinery market share in 2025, and is projected to grow at a CAGR of 11.68% through 2031.

- By crop type, vegetables and protected crops captured 37.74% of the Germany agricultural irrigation machinery market size in 2025, and the same segment is forecast to post an 11.26% CAGR to 2031.

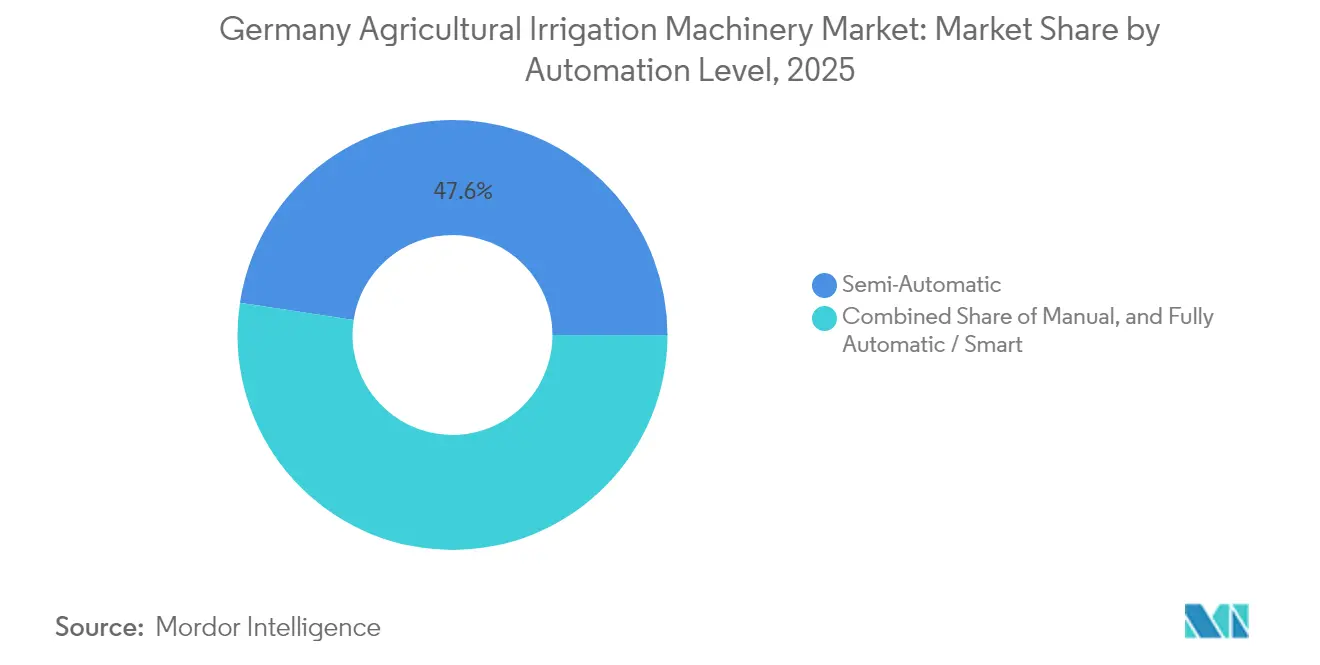

- By automation level, semi-automatic units led with 47.60% share in 2025, while fully automatic/smart systems are projected to expand at 10.52% CAGR through 2031.

- By power source, electric dominated the market with a 51.55% share in 2025, and the solar segment is anticipated to grow at a CAGR of 9.74% during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Agricultural Irrigation Machinery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-smart subsidy programs | +1.6% | Nationwide, higher in Bavaria, North Rhine-Westphalia, and Lower Saxony | Medium term (2-4 years) |

| Rising groundwater salinity in North German plains | +0.9% | Lower Saxony, Mecklenburg-Vorpommern, and Schleswig-Holstein | Long term (≥ 4 years) |

| Expansion of greenhouse horticulture clusters | +1.3% | North Rhine-Westphalia, Bavaria, and Baden-Württemberg | Medium term (2-4 years) |

| Adoption of solar-powered pump retrofits | +1.2% | Nationwide, early gains in Brandenburg, and Saxony-Anhalt | Short term (≤ 2 years) |

| Aging farm labor force driving automation | +1.1% | Nationwide, strongest where consolidation is rapid | Medium term (2-4 years) |

| Growth of carbon-credit funded irrigation projects | +0.7% | Nationwide, pilot focus on peatlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Climate-Smart Subsidy Programs

Approximately EUR 6.2 billion (USD 6.7 billion) in federal and state Common Agricultural Policy funding is allocated annually to resource-efficient equipment through 2027, with similar allocations proposed for 2028-2032[1]Source: Bundesministerium für Ernährung und Landwirtschaft, “CAP 2023-2027 Funding Factsheet,” BMEL.DE. Under the Agrarumwelt und Klimamaßnahmen framework, drip installations receive priority scoring, leading to a decline in approval rates for sprinkler upgrades. Subsidies now require on-farm telematics capable of transmitting water-use data, driving the adoption of IoT-ready controllers that are compatible with systems such as Netafim GrowSphere and the John Deere Operations Center. Bavaria and North Rhine-Westphalia approve over three times the national average of climate-adaptation applications due to co-financing rates of up to 60%, compared to Saxony, where rates rarely exceed 35%. Subsidy rollover provisions also allow growers to combine grants with low-interest KfW loans, reducing payback periods to less than four years. As many farm successors consider digital compliance a standard business practice, subsidy structures are projected to remain performance-linked rather than area-based.

Expansion of Greenhouse Horticulture Clusters

Germany produces 12.5% of its tomatoes, 10.4% of its cucumbers, and 3.9% of its peppers, while domestic demand continues to outpace imports. In response, investors are constructing multi-hectare greenhouses near logistics hubs in North Rhine-Westphalia and Bavaria. These facilities utilize advanced technologies, including closed hydroponic systems, subsurface drip laterals, and sensor-guided fertigation, to enhance labor and water efficiency. Research conducted by the German Agricultural Society has demonstrated that combining underground drip irrigation with solar-powered pumps reduces water usage by 35% while maintaining consistent yields over five consecutive growing seasons[2]Source: German Agricultural Society (DLG), “Subsurface Drip Demonstration Project,” DLG.ORG. Builders incorporate heating, ventilation, and air conditioning (HVAC) heat-recovery systems to recycle condensation for irrigation, further reducing freshwater consumption by 8-10%. Given the capital-intensive nature of greenhouse irrigation, operators often rely on subscription-based service contracts to ensure system uptime, making them consistent customers for original equipment manufacturer (OEM) software updates.

Aging Farm Labor Force Driving Automation

The number of German farms decreased by 7,800 between 2020 and 2024, with DZ Bank forecasting a further decline to approximately 100,000 farms by 2040, compared to 255,000 in 2024[3]Source: Statistisches Bundesamt, “Irrigation in German Agriculture,” DESTATIS.DE. The agricultural labor force also contracted by 7%, reaching 876,000 workers, with significant reductions in manual roles such as valve operation. As a result, growers increasingly consider fully automatic irrigation systems essential for expanding acreage without the need for additional hiring. These smart systems utilize soil moisture probes, real-time weather data, and cloud-based analytics to automate irrigation schedules. Lindsay’s 2024 acquisition of a 49.9% stake in Pessl Instruments enables FieldNET users to integrate sensor data into pump scheduling processes, resulting in a 75% reduction in manual inspections. Evidence from Lower Saxony indicates that farms transitioning from semi-automatic to smart irrigation systems reallocate 0.9 full-time labor positions per 100 hectares to higher-value agronomy tasks.

Rising Groundwater Salinity in North German Plains

Coastal aquifers in Lower Saxony and Mecklenburg-Vorpommern are experiencing conductivity levels exceeding 1.5 millisiemens per centimeter, surpassing the tolerance thresholds for crops such as sugar beet and lettuce. This increase in salinity is attributed to sea-level rise and prolonged over-extraction of groundwater. Drip irrigation systems equipped with inline filtration and automated flushing help reduce salt accumulation, driving demand for corrosion-resistant materials. T-Systems has installed LTE-M groundwater monitoring devices across 30 wells in Diepholz, providing growers with alerts when salinity levels rise. This enables them to switch to alternative water sources or adjust blending ratios. Regulators are drafting restrictions on summer water abstraction volumes, which is anticipated to indirectly accelerate the adoption of water-efficient technologies.

Restraints Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy permitting for on-farm wells | -0.8% | Baden-Württemberg, Hesse, Rhineland-Palatinate, nationwide spillover | Medium term (2-4 years) |

| Preference for leased versus owned machinery | -0.6% | Nationwide, especially 50-200 hectare farms | Short term (≤ 2 years) |

| Volatility of electricity tariffs | -0.5% | Regions that rely on grid-powered pumps | Short term (≤ 2 years) |

| Supply chain dependence on imported microchips | -0.4% | Nationwide exposure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lengthy Permitting for On-Farm Wells

In Baden-Württemberg, agricultural water extraction exceeding 5,000 cubic meters annually requires an environmental impact assessment. This process involves aquifer modeling, drawdown projections, and ecological studies[4]Source: Umweltministerium Baden-Württemberg, “Groundwater Permit Procedures,” UM.BW.DE. The processing time ranges from six to eighteen months, delaying capital investments and leading growers to explore alternatives such as rented water rights or costly municipal supplies. While irrigation activities are exempt from the state’s EUR 0.051 (USD 0.055) per cubic meter groundwater fee, small growers often incur additional costs by hiring consultants to manage the paperwork, increasing project expenses by approximately 10%. Similar challenges are observed in Rhineland-Palatinate, where groundwater usage is charged at EUR 0.06 (USD 0.065) per cubic meter. Conservation offsets can reduce this fee by half. Legal rulings, such as the Currenta and Nordheide cases, have established stricter regulations to protect ecological flows. As a result, obtaining well approvals is projected to become increasingly stringent.

Supply Chain Dependence on Imported Microchips

Smart controllers depend significantly on Asian semiconductor foundries. Lead times, which peaked at 40 weeks in 2022, are projected to reduce to 18-22 weeks by 2024. Original equipment manufacturers continue to maintain additional inventory equivalent to three months of production. Components constitute 10-15% of a smart system’s bill of materials, meaning a 12% tariff increase or freight disruptions could directly impact margins. To mitigate these risks, companies such as Netafim, Valmont, and Lindsay are qualifying secondary suppliers in Singapore and the United States. Re-designing tooling extends product development cycles and increases research and development expenditures. While no Germany-specific shortages are anticipated for 2024-2025, board-level risk committees continue to rank silicon availability as one of the top three risks for the upcoming planning period.

Segment Analysis

By Irrigation Type: Drip Systems Hold the Lead

Drip irrigation accounted for 54.12% of the Germany agricultural irrigation machinery market share in 2025 and is projected to grow at a CAGR of 11.68% through 2031. This growth is set to surpass that of sprinkler systems, driven by the retrofitting of legacy infrastructure in greenhouse horticulture clusters in North Rhine-Westphalia and Bavaria, as well as the adoption of subsurface drip systems by field-crop growers in water-stressed regions to comply with groundwater extraction limits. The segment's expansion is supported by climate-smart subsidy programs that prioritize water-efficient technologies. Netafim's GrowSphere operating system, introduced at the International Exposition of Machinery for Agriculture and Gardening (EIMA) 2024, integrates drip hardware with fertigation control, soil-moisture feedback, and agronomic decision support, highlighting the industry's shift toward bundled solutions that secure growers into multi-year service agreements.

Sprinkler irrigation, including mobile reel-mounted systems and center-pivot installations, remains widely used for field crops such as potatoes, sugar beets, and cereals. Lower Saxony, which accounts for 48% of Germany's 560,000 hectares of irrigated land, predominantly utilizes sprinklers due to their lower initial costs and ease of relocation across rental parcels. The adoption of sprinkler systems faces challenges from increasing electricity tariffs, which reached 20.16 cents per kilowatt-hour for industrial users in April 2024, and regulatory measures aimed at reducing nitrate leaching, a problem exacerbated by over-application associated with sprinkler systems.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Crop Type: Vegetables and Protected Crops Drive Premium Equipment Demand

Vegetables and protected crops accounted for 37.74% of the German agricultural irrigation machinery market size and are projected to grow at a CAGR of 11.26% through 2031. This growth reflects Germany's structural vegetable deficit and the concentration of greenhouse clusters in North Rhine-Westphalia and Bavaria, where the use of drip irrigation is mandatory for climate-controlled production. Greenhouse operators are facing significant labor shortages, with agricultural employment projected to decline by 7% to 876,000 workers in 2024. As a result, fully automated fertigation platforms that integrate nutrient dosing, pH adjustment, and soil-moisture feedback have become essential for operational sustainability. Tomatoes, cucumbers, and peppers dominate the demand for protected-crop irrigation, with self-sufficiency rates of 12.5%, 10.4%, and 3.9%, respectively. These low self-sufficiency rates create a structural incentive for domestic capacity expansion, benefiting premium drip irrigation suppliers such as Netafim, Rivulis, and Irritec.

Fruits and vineyards, primarily located in Baden-Württemberg, Rhineland-Palatinate, and Bavaria, are increasingly adopting drip and micro-sprinkler systems. These systems are valued for their frost protection, fertigation precision, and water-use efficiency. Deere's Smart Apply LiDAR-based sensing technology has demonstrated a 28% reduction in chemical and water usage during pilot trials in Sonoma County, a result that has garnered interest from German viticulture regions.

The turf and ornamentals segment represents a niche market driven by municipal landscaping, sports facilities, and nursery operations, with demand concentrated in urban centers. This segment predominantly utilizes rotator sprinklers and drip tape, which offer precise coverage and low maintenance requirements.

By Power Source: Solar Gains as Grid Costs Climb

Electric power sources accounted for 51.55% of the market share in 2025, underscoring the prevalence of grid-connected pumps in established irrigation regions. Solar power represents the fastest-growing segment, with a CAGR of 9.74% projected through 2031. This growth is driven by rising electricity tariffs, which reached 20.16 cents per kilowatt-hour for industrial users in April 2024, and are projected to continue increasing due to the socialization of transmission and distribution infrastructure costs. Solar-powered pump retrofits eliminate recurring energy expenses and benefit from accelerated depreciation under Germany's renewable energy incentives, offering a payback period of 3 to 5 years for systems designed to meet peak irrigation demands.

Regions such as Brandenburg and Saxony-Anhalt are leading in solar pump adoption due to higher solar irradiance and lower land costs, which facilitate the installation of ground-mounted arrays near well sites. In contrast, Western states prefer roof-mounted panels on barn structures. The integration of solar pumps with smart controllers enables demand-response irrigation, allowing for pumping during peak solar hours. This reduces battery capacity requirements and lowers system costs by 20-25%. Diesel power sources, although declining in market share, remain essential for high-flow applications and remote locations without access to a grid. Mobile sprinkler systems often rely on diesel engines for portability and independence from fixed infrastructure. Diesel faces increasing regulatory challenges due to emissions standards and carbon pricing. Germany's CO2 levy on fossil fuels adds EUR 0.10 to 0.15 (USD 0.11 to 0.16) per liter to the cost of diesel, diminishing its cost advantage over electricity in areas with moderate tariffs.

By Automation Level: Smart Systems Capture Labor-Scarce Farms

Semi-automatic systems accounted for a 47.60% market share in 2025, highlighting their balance of affordability and functionality. These systems are particularly suitable for mid-sized farms, as they provide an effective solution for managing daily valve adjustments and manual fertigation mixing. They offer a cost-effective alternative to fully automated systems while maintaining the flexibility and control required for efficient farm operations. Semi-automatic systems are easier to install and maintain compared to fully automated counterparts, making them a practical choice for farmers with limited technical expertise. Their adaptability to varying farm sizes and operational needs further enhances their appeal, contributing to their widespread adoption in the market.

Fully automatic and smart irrigation systems are projected to grow at a CAGR of 10.52% through 2031. This growth is driven by the contraction of Germany's farm count, which decreased by 7,800 operations since 2020, reaching 255,000 in 2024, alongside a 7% decline in agricultural employment to 876,000 workers. These trends underscore the economic necessity of labor-saving automation. Fully automatic irrigation systems, equipped with features such as soil moisture feedback, weather station integration, and remote smartphone control, eliminate the need for human intervention in irrigation scheduling and execution. These systems reduce labor requirements by 60% to 80% compared to semi-automatic alternatives, enabling growers to manage larger areas with fewer workers. Lindsay's acquisition of a 49.9% stake in Pessl Instruments (METOS) in 2024 aimed at integrating IoT sensors with FieldNET irrigation management. This move highlights the industry's transition toward comprehensive automation solutions that combine hardware, connectivity, and decision-support software into subscription-based models.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Lower Saxony accounts for nearly half of Germany's 560,000 hectares of irrigated land, driven by sandy soils and intensive potato and vegetable rotations that require reliable water delivery systems. The state's proximity to salt-prone coastal aquifers has heightened interest in pressure-compensating drip lines and corrosion-resistant fittings. Local pilot projects integrating T-Systems groundwater sensors with Netafim controllers demonstrated a 14% yield increase in 2024 by bypassing salinity spikes in real-time.

North Rhine-Westphalia and Bavaria follow as key regions, supported by greenhouse clusters expanding to address the nation's vegetable self-sufficiency gap. Subsidies in these states cover over 60% of eligible expenses, accelerating the adoption of fully automated systems that integrate irrigation, nutrient delivery, and climate controls. Bavaria's relatively simple well-permit process enables growers to install solar pumps alongside drip networks more rapidly than in Hesse. Conversely, growers in Rhineland-Palatinate face groundwater fees of EUR 0.06 (USD 0.065) per cubic meter, driving the adoption of water-saving technologies even in areas with lower yield potential.

In eastern states such as Brandenburg and Saxony-Anhalt, high solar irradiance combines with fragmented land ownership. Approximately 52% of Brandenburg's farmland is owned by non-agricultural personal investors, complicating long-term investment projects. Despite this, solar pump retrofits are increasingly common due to the lack of grid connection requirements. Mecklenburg-Vorpommern is projected to increase irrigation demand from 4.1 million to 10.2 million cubic meters by 2050, necessitating the use of drip and recirculation technologies to address rising salinity levels. In Schleswig-Holstein, regulatory decisions, such as the Nordheide precedent, have led to tighter annual caps on well allocations, indirectly encouraging the adoption of closed-loop systems and desalination pilot projects.

Competitive Landscape

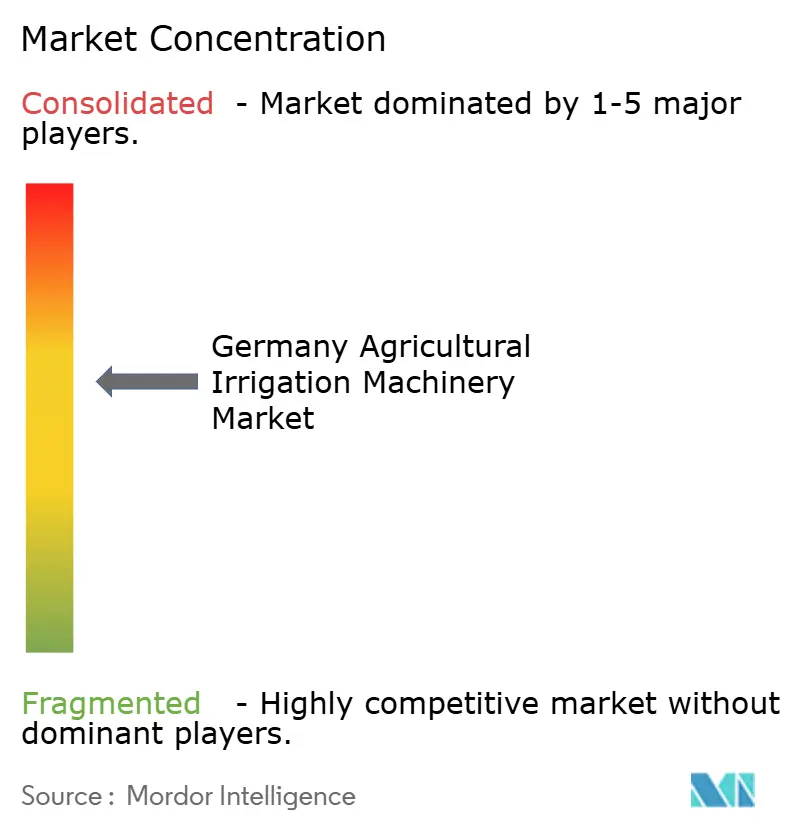

The market concentration in Germany's agricultural irrigation machinery sector is moderate. The top five companies, Netafim Limited (An Orbia Business), Valmont Industries, Inc., Lindsay Corporation, Rain Bird Corporation, and The Toro Company, collectively hold the majority market share in 2024. This moderate concentration is attributed to the presence of strong regional dealers offering niche sprinkler brands and greenhouse integrators specifying custom European pumps. Netafim's strategy focuses on GrowSphere, an operating system launched in late 2024, which generates revenue through subscription fees and services, including agronomic optimization and predictive maintenance.

Valmont Industries and Lindsay Corporation have integrated telematics into their offerings, binding growers to multiyear software plans. Lindsay's 49.9% investment in Pessl Instruments enhances its FieldNET platform by providing a proprietary sensor pipeline, which reduces decision latency and minimizes customer churn. In March 2024, Valmont joined the European Irrigation Association to influence future standards and expand its reach in aftermarket parts. Both companies report resilient sales in the EMEA region, despite a decline in aggregate equipment volumes, indicating a shift in revenue focus from hardware to services.

Disruptive entrants are reshaping the market. NORMA Group acquired Teco Srl in December 2023 to gain access to micro-irrigation technology. In December 2024, Phytech partnered with Rivulis and Netafim to integrate plant-stress sensing with hydraulic telemetry, enabling predictive models that adjust irrigation before visible signs of plant stress appear. Meanwhile, John Deere is considering exiting its drip irrigation division, a move that could release valuable assets sought by greenhouse specialists aiming for tighter European distribution networks. Larger suppliers are investing in dual sourcing of semiconductors to mitigate the risks associated with geopolitical disruptions. Smaller German manufacturers face challenges in funding similar strategies, suggesting potential market consolidation over the next decade.

Germany Agricultural Irrigation Machinery Industry Leaders

Netafim Limited (An Orbia Business)

Valmont Industries, Inc.

Rain Bird Corporation

Lindsay Corporation

The Toro Company

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2024: Orbia’s Precision Agriculture business, Netafim, and Bayer expanded their strategic collaboration to introduce new digital farming solutions for fruit and vegetable growers. These solutions simplify primary data collection and provide a system capable of generating tailored recommendations based on the collected data.

- February 2024: Rivulis has introduced the D4000 PC drip irrigation system, a thin-wall pressure-compensated drip line. This system is designed to enable drip irrigation on land previously unsuitable for such methods, helping growers enhance productivity and profitability.

- May 2024: WiseConn introduced the RF-V1 field device in Europe, including Germany, to enhance its DropControl irrigation system. This device aims to improve water efficiency and increase crop yields for farmers in the region.

Germany Agricultural Irrigation Machinery Market Report Scope

Irrigation systems that are used to supply water to agricultural and industrial land, and lands used for other purposes, to promote hydration and growth, are categorized as irrigation machinery. The Germany agricultural irrigation machinery market is segmented by irrigation type into sprinkler irrigation (pumping unit, tubing, coupler, spray/sprinkler heads) and drip irrigation (valves, backflow preventer, pressure regulator and valves, fittings, and accessories, filters, emitters, mainline, sub-main). The report offers market estimation and forecast of the irrigation machinery market in terms of value in (USD) for the above-mentioned segments.

By Irrigation Type

| Sprinkler Irrigation | Pumping Unit |

| Tubing | |

| Coupler | |

| Spray / Sprinkler Heads | |

| Other Components | |

| Drip Irrigation | Valves |

| Back-flow Preventers | |

| Pressure Regulators | |

| Fittings and Accessories | |

| Filters | |

| Emitters | |

| Mainline | |

| Sub-main | |

| Other Components |

By Crop Type

| Field Crops |

| Fruits and Vineyards |

| Vegetables and Protected Crops |

| Turf and Ornamentals |

By Power Source

| Electric |

| Diesel |

| Solar |

By Automation Level

| Manual |

| Semi-automatic |

| Fully Automatic / Smart |

| By Irrigation Type | Sprinkler Irrigation | Pumping Unit |

| Tubing | ||

| Coupler | ||

| Spray / Sprinkler Heads | ||

| Other Components | ||

| Drip Irrigation | Valves | |

| Back-flow Preventers | ||

| Pressure Regulators | ||

| Fittings and Accessories | ||

| Filters | ||

| Emitters | ||

| Mainline | ||

| Sub-main | ||

| Other Components | ||

| By Crop Type | Field Crops | |

| Fruits and Vineyards | ||

| Vegetables and Protected Crops | ||

| Turf and Ornamentals | ||

| By Power Source | Electric | |

| Diesel | ||

| Solar | ||

| By Automation Level | Manual | |

| Semi-automatic | ||

| Fully Automatic / Smart | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Germany agricultural irrigation machinery market in 2026?

It is valued at USD 91.91 million and is projected to rise to USD 129.62 million by 2031.

Which irrigation technology currently dominates German farms?

Drip systems lead with 54.12% share and enjoy the fastest long-term growth due to subsidy preferences and water-saving performance.

Why are German growers moving toward solar-powered pumps?

Industrial electricity tariffs exceed 20 cents per kilowatt-hour, so solar systems deliver three-year payback and qualify for accelerated depreciation.

Which states show the most potential for new irrigation investment?

Lower Saxony for field crops, North Rhine-Westphalia and Bavaria for greenhouses, and Mecklenburg-Vorpommern for salinity-resistant drip installations.