| Study Period | 2021 - 2030 |

| Market Size (2025) | USD 4.40 Billion |

| Market Size (2030) | USD 9.00 Billion |

| CAGR (2025 - 2030) | 15.41 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

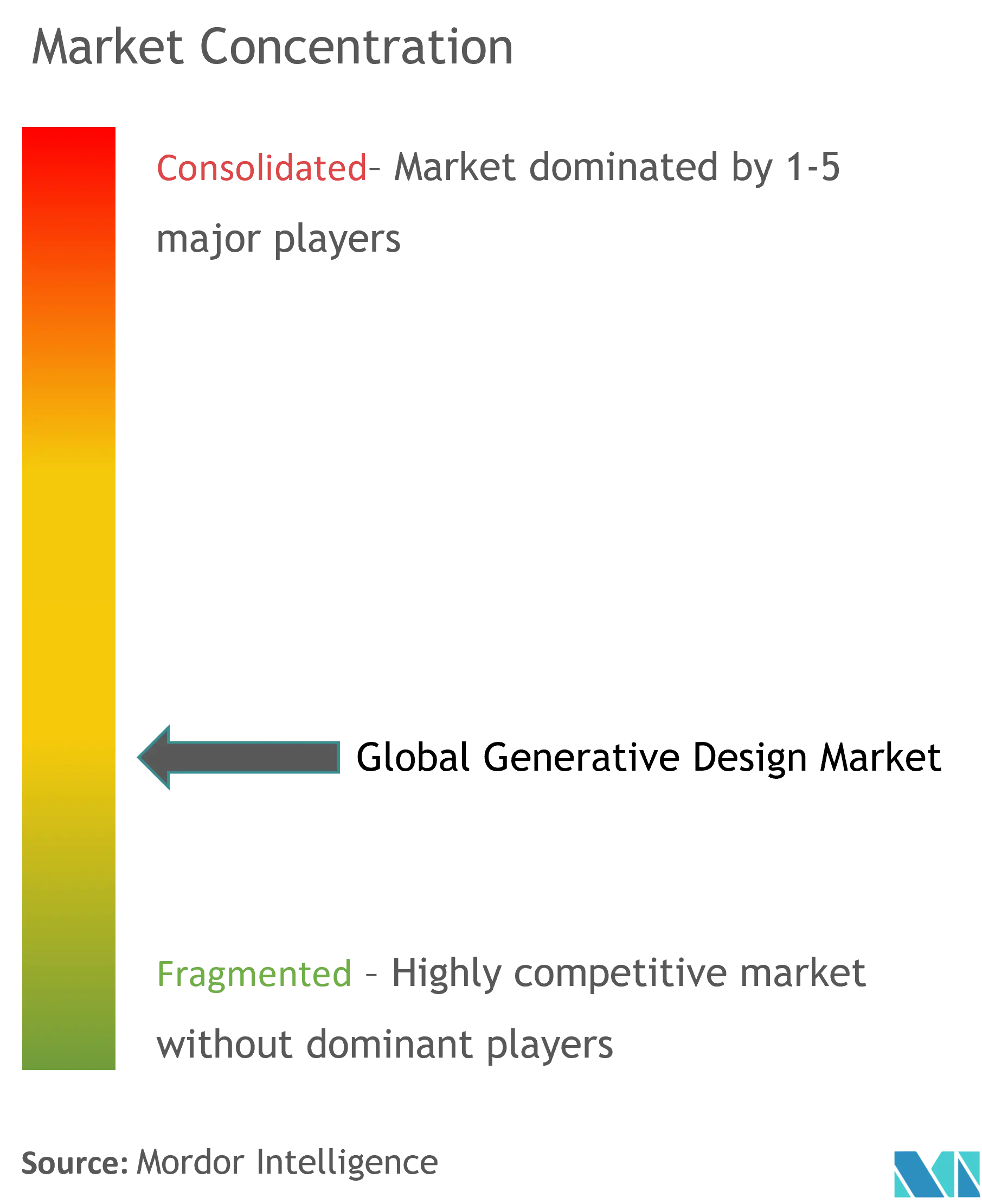

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Generative Design Market Analysis

The Generative Design Market size is estimated at USD 4.40 billion in 2025, and is expected to reach USD 9.00 billion by 2030, at a CAGR of 15.41% during the forecast period (2025-2030).

The generative design industry is experiencing a fundamental transformation as manufacturing processes become increasingly complex and digitalized. Traditional design and manufacturing approaches are being revolutionized by the integration of artificial intelligence (AI) and machine learning (ML) capabilities into design toolsets. This shift is particularly evident in the automotive sector, where manufacturers face the challenge of managing approximately 30,000 different parts in an average vehicle, necessitating sophisticated supply chain and manufacturing solutions. The industry's evolution is driven by the need to optimize these complex processes while maintaining high quality and efficiency standards.

The aerospace and defense sector is emerging as a crucial adopter of generative design technologies, with projected commercial aircraft deliveries expected to reach 43,110 units by 2039. Leading companies like Airbus are leveraging generative design not only for component optimization but also for broader applications such as factory layout planning and logistics optimization. These implementations demonstrate the versatility of generative design in addressing both product-specific challenges and broader operational efficiencies, particularly in industries where weight reduction and performance optimization are critical factors.

The integration of generative design with additive manufacturing and 3D printing technologies is creating new possibilities for product innovation and manufacturing efficiency. Companies are increasingly utilizing these combined technologies to create complex, organic-looking shapes that would be impossible or prohibitively expensive to produce using traditional manufacturing methods. This convergence is enabling manufacturers to reduce part counts, optimize material usage, and create stronger, lighter components while maintaining or improving performance characteristics.

The industry is witnessing a significant shift toward cloud-based design simulation solutions, enabling greater collaboration and accessibility across global design teams. Software providers are developing more sophisticated platforms that incorporate multiple design and computation tools, allowing for more comprehensive analysis and design optimization of design alternatives. This evolution is particularly beneficial for small and medium-sized enterprises, as it reduces infrastructure costs and provides access to advanced computational capabilities previously available only to larger organizations. The trend is supported by major industry players who are continuously enhancing their software capabilities to include features such as automated workflow generation and real-time design optimization.

Generative Design Market Trends

Growing Demand for Advanced Technologies to Drive Product Innovation and Production Efficiency

The increasing integration of advanced technologies like artificial intelligence (AI), machine learning (ML), the Internet of Things (IoT), and big data analytics is revolutionizing product development and manufacturing processes across industries. These technologies are reducing industry fragmentation, improving operational efficiency, and addressing the challenges of excessive costs due to inadequate interoperability. The automotive sector exemplifies this transformation, where manufacturers face the complexity of managing over 30,000 parts in an average car through intricate supply chains and manufacturing processes. Companies like General Motors have demonstrated the power of these advanced technologies by partnering with software providers to revolutionize their design approach, resulting in innovative solutions like their redesigned seat bracket that achieved a 40% weight reduction while improving strength by 20% through generative design technology.

The adoption of advanced technologies is particularly evident in the electric vehicle (EV) sector, where manufacturers are leveraging generative design to address critical challenges in vehicle efficiency and performance. Companies like Volkswagen Group are showcasing the potential of these technologies through initiatives like their retrofitted VW Microbus project, which utilizes design optimization to optimize component weight while maintaining structural integrity. Similarly, Arcimoto Inc.'s collaboration with ParaMatters to redesign components for their Fun Utility Vehicle (FUV) demonstrates how AI design software can create alternative parts that maintain performance characteristics while significantly reducing weight. This technological advancement is particularly crucial for EV manufacturers, as weight reduction directly impacts vehicle range and energy efficiency, which are primary considerations for consumers. The integration of these advanced technologies with generative manufacturing and 3D printing capabilities is further accelerating innovation, allowing manufacturers to produce complex, organic-looking shapes that were previously impossible or cost-prohibitive to manufacture using traditional methods.

Understand The Key Trends Shaping This Market

Download PDF

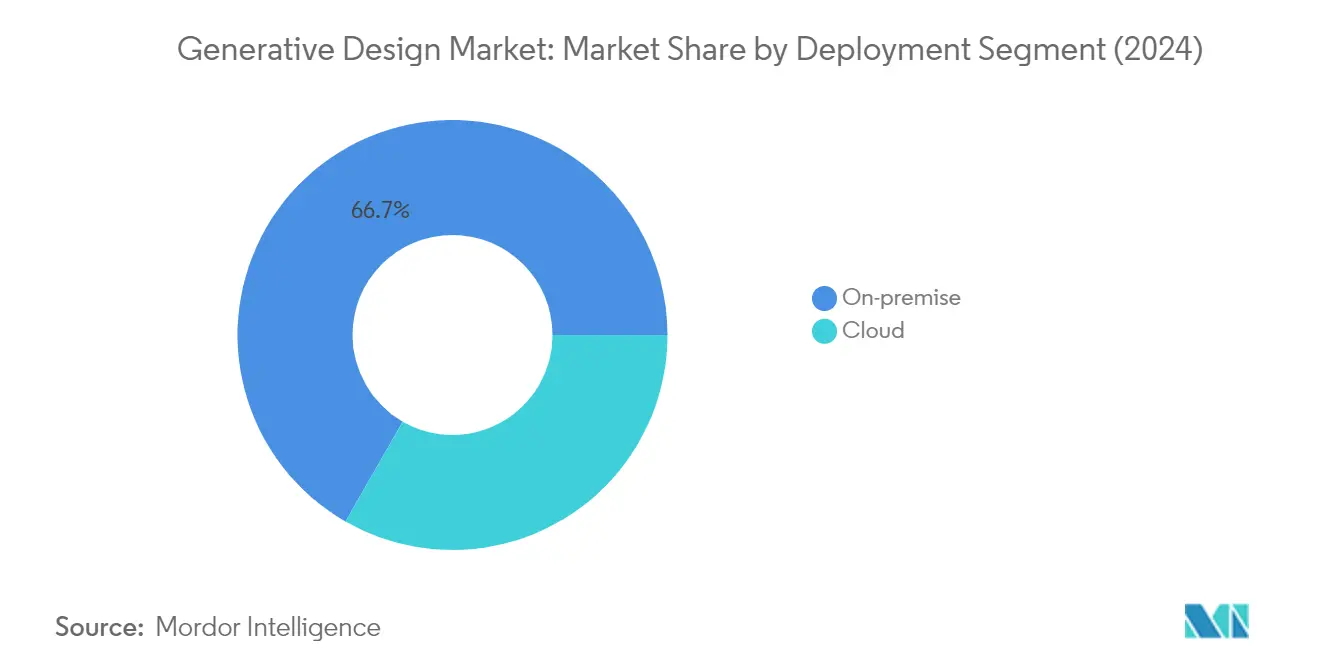

Segment Analysis: By Deployment

On-premise Segment in Generative Design Market

The on-premise deployment segment continues to dominate the generative design market, holding approximately 67% of the market share in 2024. This significant market position is primarily driven by organizations' preferences for maintaining complete control over their data, business processes, and internal policies. On-premise solutions offer enhanced data security, privacy, and the flexibility to customize software according to specific organizational requirements. Many large enterprises, particularly in sectors like aerospace, defense, and automotive, prefer on-premise deployment due to the sensitive nature of their design data and intellectual property. The segment's strength is further reinforced by existing investments in hardware infrastructure, servers, networks, and enterprise software applications, making it more economically viable for organizations to leverage these investments through on-premise deployments.

Cloud Segment in Generative Design Market

The cloud deployment segment is experiencing rapid growth in the generative design market, with an expected growth rate of approximately 18% during 2024-2029. This accelerated growth is driven by the increasing adoption of cloud solutions by small and medium-sized enterprises (SMEs) seeking to reduce infrastructure costs and improve operational flexibility. Cloud-based generative design solutions are gaining traction due to their ability to provide seamless integration with design platforms, lower capital expenditure requirements, and easier deployment options. The segment's growth is further fueled by digital transformation initiatives worldwide and the rising demand for remote collaboration capabilities. Cloud solutions aim to keep all functionalities, including design optimization, design simulation, design, and manufacturing, under one platform, providing a comprehensive solution for users while eliminating the overheads involved in installation, maintenance, and license management.

Segment Analysis: By End-User Vertical

Automotive Segment in Generative Design Market

The automotive segment continues to dominate the generative design market, holding approximately 41% market share in 2024. This significant market position is driven by the increasing adoption of generative design tools by major automotive manufacturers to optimize vehicle components, reduce weight, and improve overall performance. The technology is particularly crucial in electric vehicle development, where manufacturers are leveraging generative design to create lightweight components that enhance battery efficiency and vehicle range. Leading automotive companies are utilizing these tools to redesign traditional parts, resulting in components that are both lighter and stronger than conventional designs, while simultaneously reducing the total number of parts required in vehicle assembly.

Architecture and Construction Segment in Generative Design Market

The architecture and construction segment is emerging as one of the fastest-growing sectors in the generative design market for the period 2024-2029. This rapid growth is driven by the increasing demand for sustainable building designs, optimization of space utilization, and the need to improve building performance while reducing operational costs. The segment's expansion is further fueled by the integration of generative design with Building Information Modeling (BIM) technology, enabling architects and engineers to explore thousands of design alternatives while considering various parameters such as energy efficiency, material costs, and structural integrity. The adoption is particularly accelerating in smart city projects and large-scale commercial developments, where generative design tools are helping create more efficient and environmentally conscious architectural solutions.

Remaining Segments in End-User Vertical

The aerospace and defense sector represents a significant portion of the generative design market, with manufacturers utilizing the technology to optimize aircraft components and defense equipment designs. The industrial manufacturing segment continues to leverage generative design for creating more efficient production processes and optimizing product designs across various applications. These segments are particularly focused on using generative design to achieve weight reduction, improve performance, and enhance manufacturing efficiency. The technology's ability to create complex geometries and optimize material usage has made it increasingly valuable across these sectors, particularly in applications requiring high performance and precision manufacturing.

Generative Design Market Geography Segment Analysis

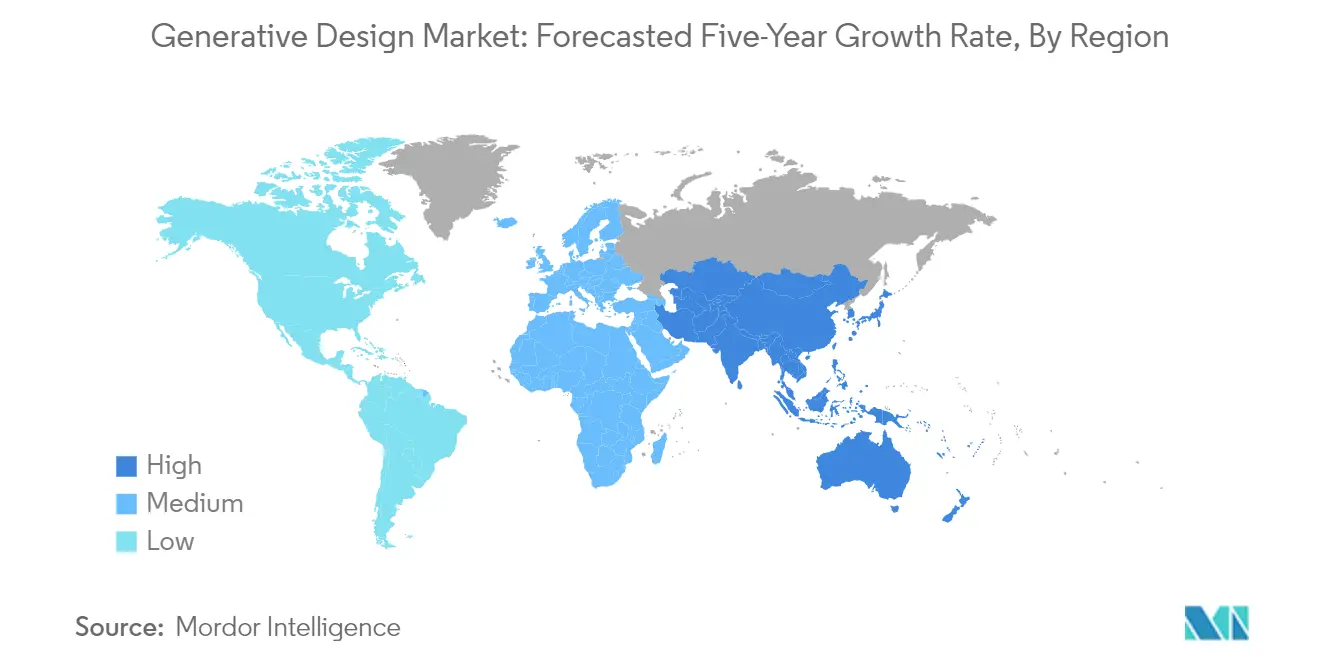

Generative Design Market in North America

North America continues to dominate the global generative design market, holding approximately 38% of the market share in 2024. The region's leadership is primarily driven by the strong presence of major technology companies and early adopters of advanced manufacturing technologies. The automotive and aerospace sectors in the United States and Canada are particularly active in implementing design automation solutions to optimize product development and reduce material waste. The region's robust research and development infrastructure, coupled with substantial investments in industrial automation and digital transformation initiatives, further strengthens its market position. Additionally, the presence of leading software vendors and a mature ecosystem of system integrators and service providers creates a favorable environment for market growth. The increasing focus on sustainable manufacturing practices and the need for cost-effective production solutions continue to drive the adoption of generative design tools across various industries in the region.

Generative Design Market in Europe

Europe has established itself as a significant hub for generative design innovation, demonstrating approximately 12% growth from 2019 to 2024. The region's market is characterized by strong adoption across its robust automotive, aerospace, and manufacturing sectors. The European market benefits from the presence of well-established industrial automation infrastructure and a strong focus on Industry 4.0 initiatives. The region's commitment to sustainable manufacturing practices and circular economy principles has been a key driver for generative design adoption. European manufacturers are increasingly leveraging these tools to optimize product designs for both performance and environmental impact. The presence of stringent regulatory frameworks promoting sustainable manufacturing practices has further accelerated the adoption of design synthesis solutions. The region's strong emphasis on research and development, particularly in countries like Germany, France, and the United Kingdom, continues to drive innovation in generative design applications.

Generative Design Market in Asia-Pacific

The Asia-Pacific region represents the fastest-growing market for generative design solutions, with a projected growth rate of approximately 19% from 2024 to 2029. The market is being driven by rapid industrialization and increasing adoption of advanced manufacturing technologies across emerging economies. Countries like China, Japan, and South Korea are leading the regional adoption of generative manufacturing solutions, particularly in their manufacturing and automotive sectors. The region's growing focus on digital transformation and smart manufacturing initiatives provides a strong foundation for market expansion. The presence of a large manufacturing base, coupled with increasing investments in research and development activities, creates significant opportunities for digital manufacturing design implementation. The region's automotive and aerospace sectors are increasingly adopting these solutions to enhance their design capabilities and maintain a competitive advantage in the global market. Additionally, government initiatives supporting industrial automation and smart manufacturing are creating a favorable environment for market growth.

Generative Design Market in Rest of the World

The Rest of the World region, encompassing Latin America and the Middle East & Africa, is witnessing growing adoption of generative design solutions, albeit at a more measured pace. The market in these regions is primarily driven by increasing investments in manufacturing infrastructure and growing awareness of advanced design technologies. In Latin America, the automotive and aerospace sectors are showing increasing interest in generative design solutions to enhance their manufacturing capabilities. The Middle East region, particularly the United Arab Emirates and Saudi Arabia, is witnessing growing adoption in its construction and infrastructure development sectors. The increasing focus on diversifying economies and modernizing industrial infrastructure is creating new opportunities for generative design implementation. The region's emerging startup ecosystem and growing investments in digital transformation initiatives are expected to further drive market growth. Additionally, the increasing presence of global technology vendors and system integrators is helping to establish a stronger market foundation in these regions.

Get Analysis on Important Geographic Markets

Download PDF

Generative Design Industry Overview

Top Companies in Generative Design Market

The generative design market features established technology leaders like Autodesk, Dassault Systèmes, ANSYS, and Altair Engineering alongside emerging specialists like Desktop Metal, nTopology, and Paramatters. These generative design companies are driving innovation through continuous R&D investments in advanced algorithms, cloud capabilities, and AI integration for their generative design platforms. Strategic partnerships with manufacturing technology providers, particularly in additive manufacturing, have become crucial for expanding solution capabilities. Companies are increasingly focusing on developing user-friendly interfaces and automated workflows to make generative design more accessible across industries. The market is characterized by frequent product launches incorporating enhanced simulation capabilities, improved optimization algorithms, and broader compatibility with various manufacturing processes.

Dynamic Market with Strong Consolidation Trends

The generative design market structure reflects a mix of large technology conglomerates and specialized software providers, with global players dominating the landscape through their comprehensive solution portfolios and established customer relationships. Market consolidation is actively progressing through strategic acquisitions, as demonstrated by larger players acquiring specialized startups to enhance their technological capabilities and expand their market presence. The competitive dynamics are shaped by companies' abilities to integrate generative design capabilities with existing CAD/CAM systems and manufacturing workflows, creating comprehensive end-to-end solutions for customers.

The market exhibits strong partnership ecosystems, with companies forming alliances across the value chain, including CAD software providers, manufacturing equipment suppliers, and industry-specific solution providers. These collaborations are essential for developing integrated solutions that address specific industry needs and manufacturing requirements. The competitive landscape is further influenced by regional market dynamics, with companies establishing local partnerships and development centers to better serve specific geographic markets and industry clusters.

Innovation and Integration Drive Market Success

Success in the generative design market increasingly depends on providers' ability to deliver comprehensive solutions that combine powerful optimization capabilities with intuitive user experiences and seamless integration into existing workflows. Incumbent players are focusing on expanding their industry-specific expertise, developing specialized solutions for sectors like automotive, aerospace, and construction, while also investing in cloud-based delivery models to improve accessibility and scalability. Companies are also emphasizing the development of automated validation tools and manufacturing feasibility analysis capabilities to ensure that generated designs are practical and manufacturable.

For new entrants and challenger companies, success lies in identifying and addressing specific market niches or technological gaps while building strong partnerships with established players in related domains. The market shows relatively high end-user concentration in traditional manufacturing sectors, making industry expertise and specialized solutions crucial for success. Regulatory considerations, particularly in sectors like aerospace and medical devices, are becoming increasingly important, requiring providers to ensure their solutions comply with industry standards and certification requirements. The risk of substitution remains relatively low due to the complex nature of generative design technology and its growing integration into core product development processes. The development of design optimization software and intelligent design software is pivotal in advancing the capabilities of generative design, enabling more efficient and innovative solutions.

Generative Design Market Leaders

-

Altair Engineering Inc.

-

Autodesk Inc.

-

ANSYS inc.

-

Dassault Systèmes SE

-

Hexagon AB

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Generative Design Market News

- August 2022 - The provider of generative design software for additive manufacturing, ParaMatters, was acquired by Carbon, a company that develops technology for 3D printing. This acquisition would add topology optimization to Carbon's present software capabilities. Carbon could use the ParaMatters software to increase its generative design capabilities for additive manufacturing.

- January 2022 - A funding round between Saffelberg Investments and Diabatix NV, a scale-up based in Leuven, Belgium, which specializes in AI-driven generative thermal design, has been successfully closed. Based on a reference client portfolio, this investment will enable the business to accelerate the growth of its Coldstream platform. Diabatix can quickly and effectively design, analyze, and optimize heat sinks and cold plates through AI and generative design.

Generative Design Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter Five Forces

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Industry Stakeholder Analysis

- 4.4 Impact of COVID-19 on the Industry Ecosystem

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Rise in latest technology in automobile segment to boost the market

- 5.1.2 Growing Demand for Advanced Technologies to Drive Product Innovation and Production Efficiency

-

5.2 Market Challenges

- 5.2.1 Complexity in Using Generative Design Software

6. MARKET SEGMENTATION

-

6.1 Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud

-

6.2 End User Vertical

- 6.2.1 Automotive

- 6.2.2 Aerospace and Defense

- 6.2.3 Architecture and Construction

- 6.2.4 Industrial Manufacturing

- 6.2.5 Other End User Verticals

-

6.3 Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.1.3 Rest of North America

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.2.4 Spain

- 6.3.2.5 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.4.1 Brazil

- 6.3.4.2 Argentina

- 6.3.4.3 Rest of Latin America

- 6.3.5 Middle East and Africa

- 6.3.5.1 UAE

- 6.3.5.2 Saudi Arabia

- 6.3.5.3 South Africa

- 6.3.5.4 Rest of Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 Altair Engineering Inc.

- 7.1.2 Bentley Systems, Inc.

- 7.1.3 Autodesk Inc.

- 7.1.4 ANSYS inc.

- 7.1.5 Desktop Metal Inc.

- 7.1.6 Dassault Systèmes SE

- 7.1.7 MSC Software Corporation (Hexagon AB)

- 7.1.8 nTopology, Inc.

- 7.1.9 Paramatters

- 7.1.10 Diabatix

- 7.1.11 Caracol AM

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. MARKET OUTLOOK

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Generative Design Industry Segmentation

Engineering software known as generative design automatically develops high-performance design iterations based on performance or space requirements, manufacturing processes, materials, and costs. It uses artificial intelligence (AI) algorithms to create highly customized complicated structures and internal lattices that are impossible to construct using traditional manufacturing techniques.

The Generative Design Market is segmented by Deployment (On-premise, Cloud), End User Vertical (Automotive, Aerospace and Defense, Architecture and Construction, Manufacturing Machinery), and Geography.

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Deployment | On-premise | ||

| Cloud | |||

| End User Vertical | Automotive | ||

| Aerospace and Defense | |||

| Architecture and Construction | |||

| Industrial Manufacturing | |||

| Other End User Verticals | |||

| Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Rest of Asia-Pacific | |||

| Latin America | Brazil | ||

| Argentina | |||

| Rest of Latin America | |||

| Middle East and Africa | UAE | ||

| Saudi Arabia | |||

| South Africa | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Generative Design Market Research FAQs

How big is the Generative Design Market?

The Generative Design Market size is expected to reach USD 4.40 billion in 2025 and grow at a CAGR of 15.41% to reach USD 9.00 billion by 2030.

What is the current Generative Design Market size?

In 2025, the Generative Design Market size is expected to reach USD 4.40 billion.

Who are the key players in Generative Design Market?

Altair Engineering Inc., Autodesk Inc., ANSYS inc., Dassault Systèmes SE and Hexagon AB are the major companies operating in the Generative Design Market.

Which is the fastest growing region in Generative Design Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Generative Design Market?

In 2025, the North America accounts for the largest market share in Generative Design Market.

What years does this Generative Design Market cover, and what was the market size in 2024?

In 2024, the Generative Design Market size was estimated at USD 3.72 billion. The report covers the Generative Design Market historical market size for years: 2021, 2022, 2023 and 2024. The report also forecasts the Generative Design Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Generative Design Market Research

Mordor Intelligence offers a comprehensive analysis of the generative design industry. We leverage expertise in computational design and parametric design methodologies. Our research covers emerging technologies, including topology optimization, algorithmic design, and advanced AI design software solutions. The report, available as a convenient download in PDF format, provides detailed insights into design automation trends, design simulation practices, and automated design processes that are transforming industrial capabilities.

Stakeholders benefit from our thorough analysis of generative architecture applications, generative manufacturing innovations, and generative engineering developments. The report examines cutting-edge design synthesis methods, CAD automation technologies, and design optimization software implementations across industries. Our research particularly focuses on digital manufacturing design trends. It incorporates insights about intelligent design software and digital design automation strategies, providing actionable intelligence for decision-makers in the design optimization space.