Gene Vector Market Size

| Study Period | 2019 - 2029 |

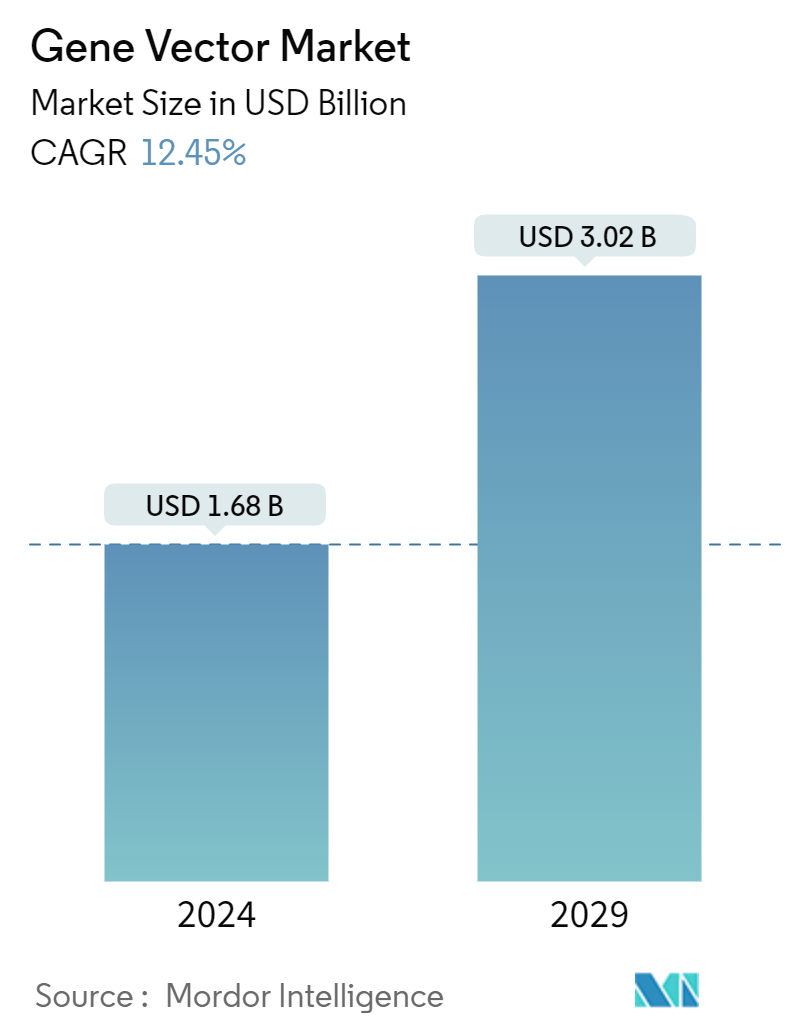

| Market Size (2024) | USD 1.68 Billion |

| Market Size (2029) | USD 3.02 Billion |

| CAGR (2024 - 2029) | 12.45 % |

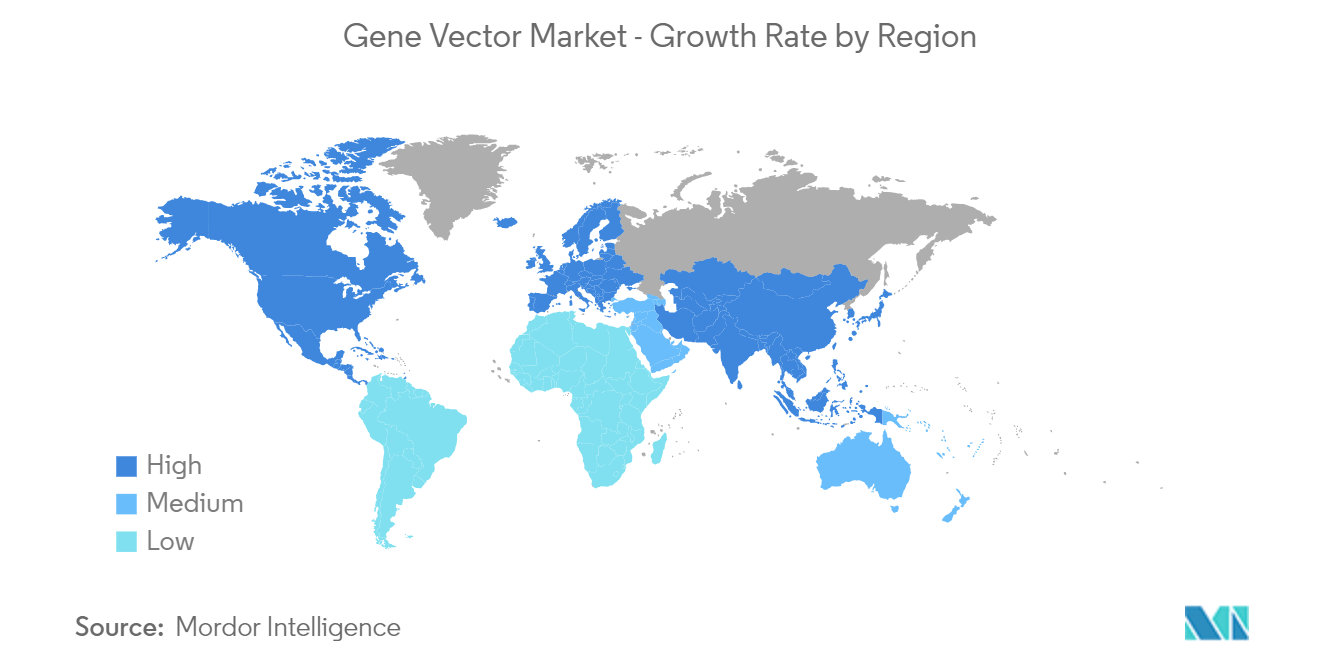

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

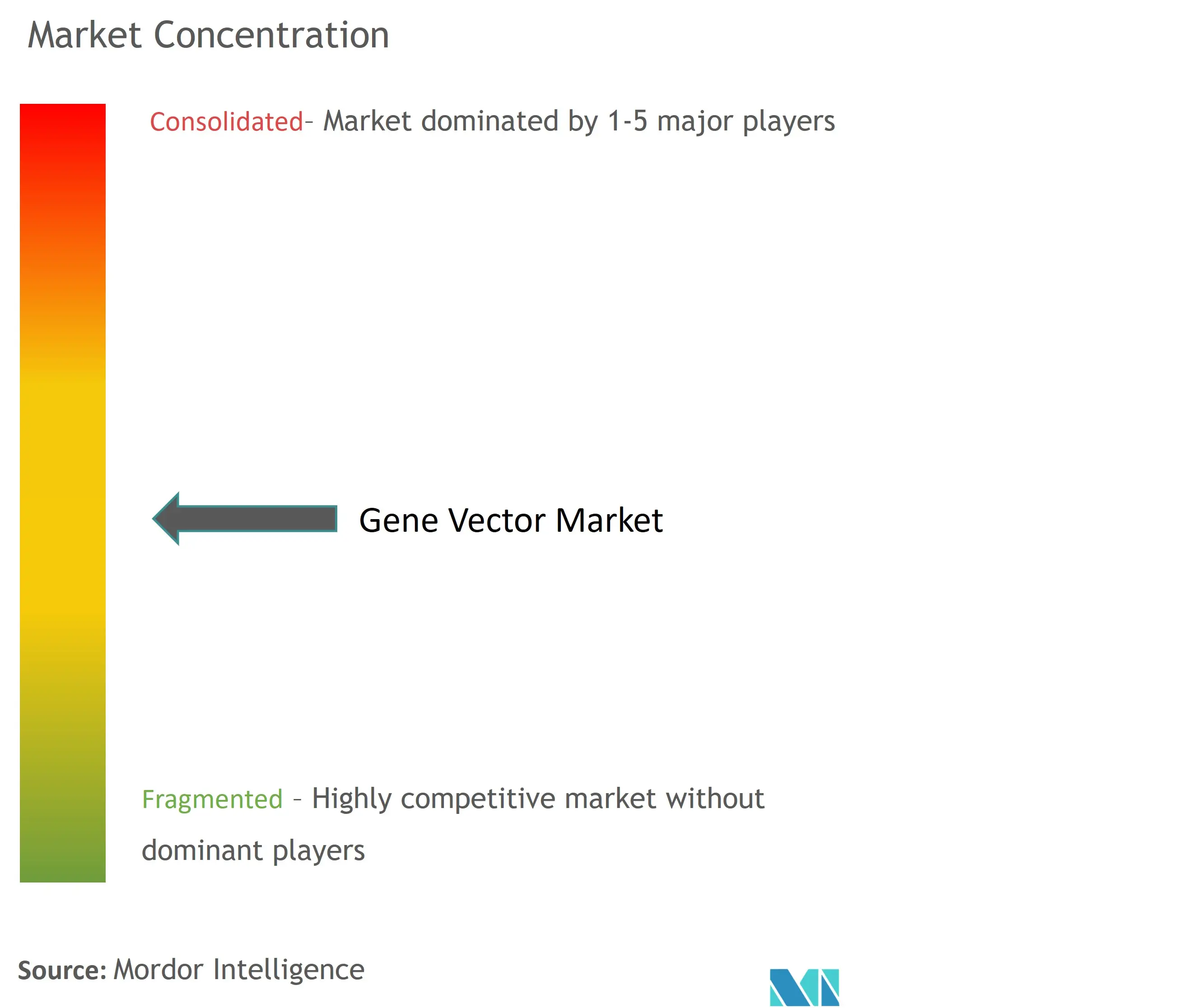

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Gene Vector Market Analysis

The Gene Vector Market size is estimated at USD 1.68 billion in 2024, and is expected to reach USD 3.02 billion by 2029, growing at a CAGR of 12.45% during the forecast period (2024-2029).

Gene vectors are fundamental tools for transmitting specific genes into host cells. In gene therapy, vectors are often utilized to modify the function of erroneous proteins by adjusting their genetic code. The rapid rise in genetic disorders globally has strongly promoted the demand for gene therapy drugs, necessitating the application of gene vectors to develop and manufacture such drugs. Data from different regulatory bodies indicate the rising number of genetic disorders globally. As per June 2023 data from the Centers for Disease Control and Prevention (CDC), congenital disabilities affected one in every 33 babies (about 3% of all babies) born in the US each year on average. Similarly, as per data from the Australian Institute of Health and Welfare (AIHW), 4,500 (or 1.7%) of Australian babies are born with congenital disabilities each year. The April 2024 data from the European Commission's EUROCAT suggested that genetic anomalies were witnessed in 20.26 cases per 10,000 births in 2022, compared to 19.6 cases per 10,000 births in 2017. With the rising population, the frequency of such defects is also rising, leading to the growing demand for research on gene therapy to tackle such defects. It is directly promoting the application of gene vectors for such research.

Gene therapy's ability to replace or inactivate disease-causing genes enables its application in treating various acquired and genetic diseases. Many gene therapies rely on small, nonpathogenic viruses known as adeno-associated viral vectors (AAVs) to deliver genes into cells. However, very few regulatory body-approved AAV gene therapies are presently available globally, including Elevidys, Hemgenix, Luxturna, Roctavian, and Zolgensma. Hence, with the rising occurrence of genetic disorders, pharmaceutical and biotechnology companies are increasing their research in developing gene therapy drugs, leading to heightened requirements for gene vectors globally. As of January 2024, according to the FDA, more than 900 clinical trials were ongoing in North America's cell and gene therapy sector, while 1,500 trials were ongoing globally, per data from ClinicalTrials.gov, a registry of clinical trials run by the United States National Library of Medicine (NLM). Such a large number of ongoing trials showcase the potential for gene therapy; it is also anticipated to promote the application of gene vectors.

Therefore, owing to the high burden of chronic diseases among the population and growing company activities to increase the development of gene therapy drugs, the market is expected to grow over the forecast period. However, most gene therapy drugs are required to pass through intense regulatory scrutiny, driving the cost of developing and utilizing gene therapy drugs. Such factors hinder gene therapy drug development, leading to lower utilization of gene vectors and thus restraining market growth.

Gene Vector Market Trends

The Segment for Cancer is Expected to Witness Substantial Growth Over the Forecast Period

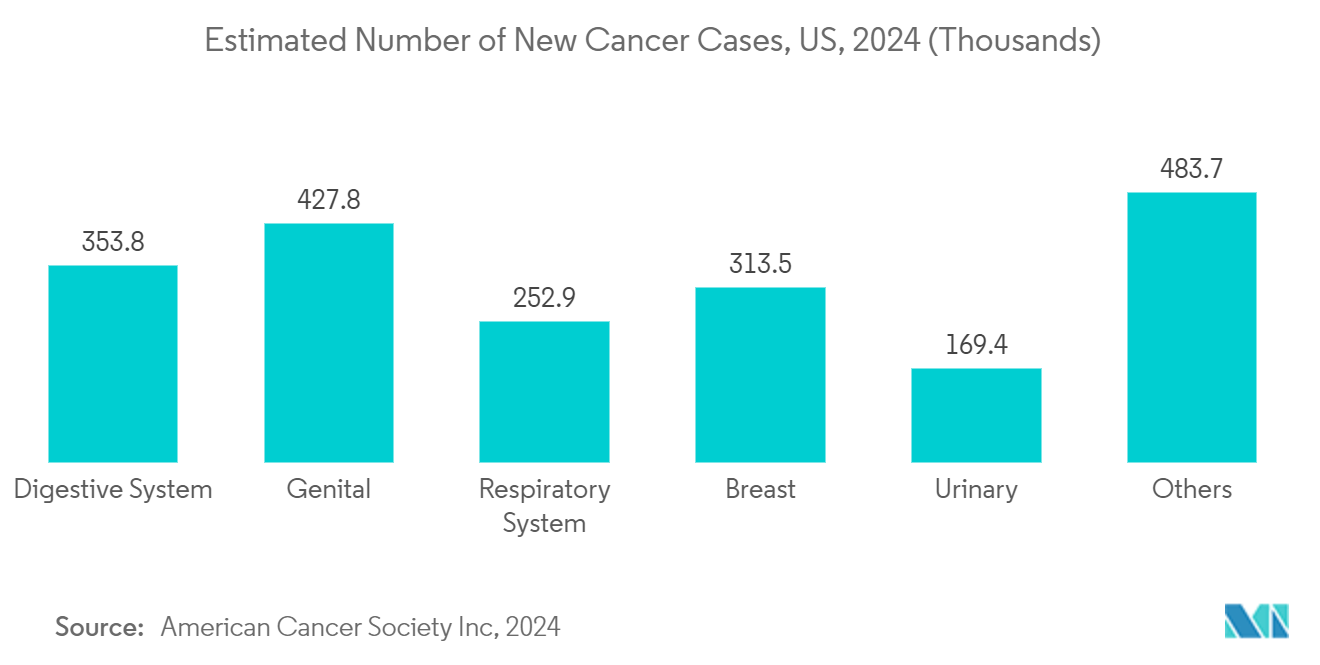

The mounting burden of cancer incidences is a significant health concern witnessed by most countries. The expansion in cancer incidences strongly drives the demand for gene vector-based oncological gene therapy. According to data from June 2022 from the World Health Organization (WHO), every year, approximately 400,000 children develop cancer globally. Similarly, the Indian Journal of Medical Research published a study in March 2023 that estimated the prevalence of cancer in India to rise from 1.46 million in 2022 to 1.57 million by 2025. Owing to such growth in the prevalence of cancer cases, several research programs are ongoing to identify, eliminate, and cure the disease through gene therapy. As of November 2022, the National Clinical Trial (NCT) Registry listed more than 600 ongoing interventional clinical trials related to gene therapy of cancer across different phases of development. Such a growing number of research programs on developing gene therapy drugs promote the growth of this segment.

Varied gene vectors have been engineered in oncology for therapeutic and preventive applications. Several gene therapy strategies are also being developed to treat various cancers, including anti-angiogenesis, oncolytic virotherapy, and therapeutic gene vaccines. For instance, in November 2023, researchers from the University of Texas announced the successful development of a potential gene therapy containing programmed plasmid DNA to "pre-treat" neuroblastoma tumors in order to increase the effectiveness of chemotherapy. Again, in November 2023, new research from the University of Pennsylvania's Gene Therapy Program (GTP) suggested that gene therapy AAVs were unlikely to cause cancer-triggering insertions in humans or monkeys and may contribute to long-term efficacy. Such research findings further promote the application of gene vectors for developing gene therapies to treat cancer. They are also expected to promote the growth of the cancer segment.

North America is Expected to Dominate the Gene Vector Market

North America is expected to dominate the market owing to factors such as broad regulatory support, competent research institutes, developing healthcare infrastructure, and established players in the region. The United States is renowned for developing medical breakthroughs, owing to government support and funding. The incentives offered through the Orphan Drugs Act have boosted biotechnology and pharmaceutical companies to deliberate advancing research on rare disease medicines as a potentially lucrative venture. According to the Orphan Drug Act, drugs receiving Orphan Drug Designation (ODD) in the country can avail of various regulatory support, including exemption of new drug application fees, tax credits for clinical trial expenses, and 7-year market exclusivity after product approval. Such support for ODD drives the research in various gene therapy drugs, boosting the demand for gene vectors in the United States.

Additionally, there is a constant rise in the number of congenital diseases in the nation. The Institute for Clinical and Economic Review’s (ICER) 2022 report estimated the presence of 7,000 rare diseases in the US, and more than 90% lacked Food and Drug Administration (FDA)-approved disease-specific treatments. It also found that the proportion of new FDA approvals gaining orphan drug designation reached nearly 50% in a bid to curb such a gap. For instance, in December 2023, the FDA granted ODD to NeuExcell Therapeutics Inc.’s NXL-004, an investigational AAV gene therapy product for treating malignant glioma. Also, by 2025, the FDA anticipates approving 10 to 20 cell and gene therapy products yearly. Such factors promote the demand for gene vectors to develop such drugs.

Similar to the US, Canada aims to support healthcare innovation by establishing a pathway for Advanced Therapeutic Products (ATPs). In January 2024, Health Canada approved Pfizer’s BEQVEZ, an AAV vector-based gene therapy for treating adults with moderately severe to severe hemophilia B who are negative for neutralizing antibodies to variant AAV serotype Rh74. In October 2023, Health Canada authorized CSL's HEMGENIX (etranacogene dezaparvovec) as a one-time, single-dose treatment for adults with hemophilia B who require routine prophylaxis. Such approvals indicate the government’s positive outlook toward approving ATPs, which is anticipated to boost the demand for gene vectors in the country.

Therefore, owing to the increasing government support, higher research activities, and rising rate of chronic diseases, the market is expected to witness growth in North America.

Gene Vector Industry Overview

The gene vector market is moderately fragmented in nature due to the presence of several companies operating globally as well as regionally. The competitive landscape includes an analysis of a few international as well as local companies that hold significant market share and are well known, including Cell Therapy Catapult Ltd, Charles River Laboratories International Inc., Fujifilm Diosynth Biotechnologies, Genezen Laboratories Inc., Kaneka Eurogentec SA, Lonza Group Ltd, Merck KGaA, Oxford Biomedica PLC, Spark Therapeutics Inc., and uniQure biopharma BV.

Gene Vector Market Leaders

-

Charles River Laboratories International Inc

-

Fujifilm Diosynth Biotechnologies

-

Kaneka Eurogentec SA

-

Merck KGaA

-

uniQure biopharma BV

*Disclaimer: Major Players sorted in no particular order

Gene Vector Market News

- April 2024: Ring Therapeutics successfully delivered a viral gene to the retinas of mice. The viral gene vector was developed using the company's Anellogy platform and was based on the human anellovirus.

- November 2023: Genezen, a cell and gene therapy (CGT) CDMO, received funding worth USD 18.5 million, led by Ampersand Capital Partners. The funding aimed to accelerate and support the company's retroviral, lentiviral, and adeno-associated viral (AAV) vector manufacturing.

Gene Vector Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Rising Number of Infectious Diseases

4.2.2 Increasing Adoption by Food & Beverage Industry

4.2.3 Growing Government Initiatives

4.3 Market Restraints

4.3.1 High Initial Investment in Instruments

4.4 Porter's Five Force Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD)

5.1 By Product Type

5.1.1 Consumables

5.1.2 Instruments

5.1.2.1 Automated Identification & Testing Systems

5.1.2.2 Bioluminescence & Fluorescence-based Detection Systems

5.1.2.3 Mass Spectrometers

5.1.2.4 Others

5.1.3 Reagents & Kits

5.2 By Method

5.2.1 Cellular Component-based Testing

5.2.2 Nucleic Acid-based Testing

5.2.3 Others

5.3 By End User

5.3.1 Clinical Laboratories

5.3.2 Food & Beverage Industry

5.3.3 Healthcare Facilities

5.3.4 Life Science Research & Development Facilities

5.3.5 Other End Users

5.4 Geography

5.4.1 North America

5.4.1.1 United States

5.4.1.2 Canada

5.4.1.3 Mexico

5.4.2 Europe

5.4.2.1 Germany

5.4.2.2 United Kingdom

5.4.2.3 France

5.4.2.4 Italy

5.4.2.5 Spain

5.4.2.6 Rest of Europe

5.4.3 Asia-Pacific

5.4.3.1 China

5.4.3.2 Japan

5.4.3.3 India

5.4.3.4 Australia

5.4.3.5 South Korea

5.4.3.6 Rest of Asia-Pacific

5.4.4 Middle East and Africa

5.4.4.1 GCC

5.4.4.2 South Africa

5.4.4.3 Rest of Middle East and Africa

5.4.5 South America

5.4.5.1 Brazil

5.4.5.2 Argentina

5.4.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 Abbott Laboratories

6.1.2 Becton, Dickinson & Company

6.1.3 bioMerieux SA

6.1.4 Bruker Corporation

6.1.5 Charles River

6.1.6 Danaher Corporation

6.1.7 Merck KGaA

6.1.8 Sartorius Group

6.1.9 Shimadzu Corporation

6.1.10 Thermo Fisher Scientific

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Gene Vector Industry Segmentation

Gene therapy uses genetic material to treat or prevent a specific disease. The objective is to reinstate the normal function of essential proteins in the body by pursuing and counteracting genetic alterations. It aims to improve overall health and proper functioning of the host body of organisms.

The gene vector market is segmented into vector type, disease, application, end-user, and geography. By vector type, the market is segmented into lentivirus, adenovirus, adeno-associated virus (AAV), plasmid DNA, and others. Based on disease, the market is segmented into cancer, genetic disorders, infectious diseases, and others. The gene vector market is segmented by application into gene therapy, vaccinology, and others. Based on end user, the market is segmented into CDMO, CRO, scientific research, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report also offers the market sizes and forecasts for 17 countries across the region. For each segment, the market sizing and forecasts were made on the basis of value (USD).

| By Product Type | ||||||

| Consumables | ||||||

| ||||||

| Reagents & Kits |

| By Method | |

| Cellular Component-based Testing | |

| Nucleic Acid-based Testing | |

| Others |

| By End User | |

| Clinical Laboratories | |

| Food & Beverage Industry | |

| Healthcare Facilities | |

| Life Science Research & Development Facilities | |

| Other End Users |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Gene Vector Market Research FAQs

How big is the Gene Vector Market?

The Gene Vector Market size is expected to reach USD 1.68 billion in 2024 and grow at a CAGR of 12.45% to reach USD 3.02 billion by 2029.

What is the current Gene Vector Market size?

In 2024, the Gene Vector Market size is expected to reach USD 1.68 billion.

Who are the key players in Gene Vector Market?

Charles River Laboratories International Inc, Fujifilm Diosynth Biotechnologies, Kaneka Eurogentec SA, Merck KGaA and uniQure biopharma BV are the major companies operating in the Gene Vector Market.

Which is the fastest growing region in Gene Vector Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Gene Vector Market?

In 2024, the North America accounts for the largest market share in Gene Vector Market.

What years does this Gene Vector Market cover, and what was the market size in 2023?

In 2023, the Gene Vector Market size was estimated at USD 1.47 billion. The report covers the Gene Vector Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Gene Vector Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Gene Vector Industry Report

Statistics for the 2024 Gene Vector market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Gene Vector analysis includes a market forecast outlook for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.

Gene Vector Market Report Snapshots