| Study Period | 2020 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 68.25 Billion |

| Market Size (2030) | USD 97.44 Billion |

| CAGR (2025 - 2030) | 7.38 % |

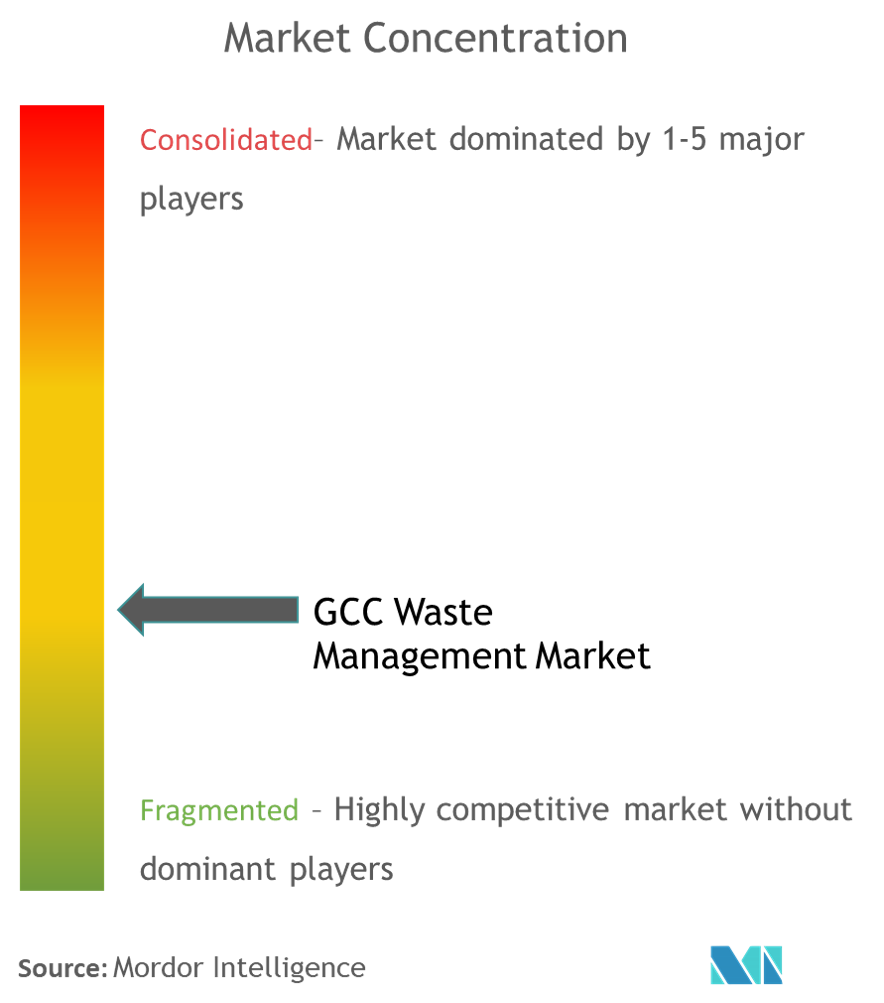

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

GCC Waste Management Market Analysis

The GCC Waste Management Market size is estimated at USD 68.25 billion in 2025, and is expected to reach USD 97.44 billion by 2030, at a CAGR of 7.38% during the forecast period (2025-2030).

The GCC waste management industry is experiencing significant transformation driven by rapid urbanization and population growth, coupled with evolving environmental consciousness. Currently, the GCC region generates between 105-130 million tonnes of waste annually, primarily comprising municipal solid waste, construction and demolition waste, and agricultural waste. The region's waste management challenges are particularly pronounced in Saudi Arabia and the UAE, which collectively account for approximately 75% of the total waste generated. This substantial volume has prompted governments across the GCC to implement comprehensive waste management strategies and sustainable disposal methods, focusing on reducing environmental impact while creating economic opportunities.

Technological advancement and innovation are reshaping the waste management landscape across the GCC region. Smart waste management solutions incorporating Internet of Things (IoT) platforms, cloud-based monitoring systems, and real-time tracking capabilities are being deployed to optimize collection routes and improve operational efficiency. In Saudi Arabia, where municipal solid waste generation averages 1.4 kg per person daily, authorities are implementing advanced sorting and waste processing technologies to better manage the diverse waste composition, which includes 40-51% food waste, 12-28% paper, and 5-17% plastics.

The transition toward a circular economy model is gaining momentum across the GCC, with governments and private sector entities increasingly focusing on waste-to-resource initiatives. According to a joint report by Boston Consulting Group and the World Business Council for Sustainable Development, the GCC region requires investments between USD 60-85 billion across four key value streams - plastic, concrete and cement, metal, and bio-waste - over the next two decades to achieve regional waste management targets. This substantial investment requirement underscores the region's commitment to developing sustainable waste management infrastructure and technologies.

The waste-to-energy (WTE) sector is emerging as a crucial component of the GCC's waste management strategy, with numerous projects under development across the region. Saudi Arabia's ambitious plan to generate approximately half of its energy requirements (72 GW) from renewable sources by 2032, including waste-to-energy systems, exemplifies this trend. The integration of WTE facilities is particularly significant given the region's current landfill challenges, with Saudi Arabia alone requiring approximately 28 million cubic meters of landfill space annually. This shift towards energy recovery from waste not only addresses waste management challenges but also contributes to the region's broader energy diversification objectives.

GCC Waste Management Market Trends

Growing Environmental Concerns and Government Initiatives

The GCC region's governments have demonstrated increasing commitment to environmental protection through comprehensive environmental services and waste management initiatives and regulations. In February 2023, the National Center for Waste Management (MWAN) in Saudi Arabia announced ambitious plans to eliminate 82% of all types of waste dumps by 2035, showcasing the government's dedication to sustainable waste management practices. This commitment is further reinforced by the UAE government's proactive approach in developing new regulations and facilities for effective electronic waste management, while also creating a framework for the Single-Use Plastic Policy and implementing a ban on non-biodegradable plastic products.

The environmental implications of current waste disposal practices have become a critical concern across the GCC region. For instance, in Kuwait, where the land area is 17,820 sq km, approximately 45 sq km is occupied by landfill sites and is expected to increase to 60 sq km by 2025. This situation has prompted governments to implement stricter environmental regulations and invest in modern waste management infrastructure. Qatar's government has particularly emphasized waste management and treatment due to its commitment to reducing environmental impacts and maintaining civic conditions, implementing integrated efforts for prevention, reduction, reuse, recycling, and energy recovery before considering landfill disposal as a last resort.

Understand The Key Trends Shaping This Market

Download PDF

Rising Industrial Activities and Waste Generation

The rapid industrialization and urban development across the GCC region have led to unprecedented levels of waste generation, particularly in the industrial and construction sectors. The World Bank has noted that Kuwait has a very high per capita waste generation of 1.55 kg per day, significantly higher than the global per capita average of 0.74 kg per day. Similarly, Bahrain, despite being the smallest nation in the region, produces the largest amount of waste per person among GCC countries, with an estimated 1.67–1.80 kg per person per day, highlighting the pressing need for effective industrial waste management solutions.

The petrochemical industry, one of the largest sectors in the GCC region, continues to be a major contributor to industrial waste generation. This is particularly evident in Saudi Arabia, where increasing investments in manufacturing facilities, supported by low-interest loans from SIDF for industrial plant construction, are driving the growth of industrial waste management output. The construction industry also remains a significant source of waste, especially in Qatar, where various steps are being taken by domestic municipalities and the government to address the massive waste production from construction activities. The surging quantity of liquid waste and the illegitimate disposal of hazardous waste management in water bodies has further complicated the situation, impacting aquatic life and augmenting the eutrophication of water bodies.

Increasing Focus on Sustainable Waste Management Solutions

The GCC region is witnessing a significant shift towards sustainable waste management practices, driven by both environmental necessity and economic opportunity. E-waste management, in particular, has emerged as a promising sector, offering employment opportunities for both highly skilled and unskilled workers, supporting the GCC countries' goal of transferring employment from the public to the private sector. The UAE has taken the lead in this transition, establishing specialized facilities for e-waste classification and sorting, while also positioning itself to become a global recycling hub through systematic implementation of sustainable practices.

The economic benefits of sustainable waste management have become increasingly apparent across the GCC region. For instance, waste recycling initiatives have shown potential to minimize costs by reducing landfill space usage, a critical consideration in countries like Bahrain where the only existing landfill is approaching capacity. The region has also recognized the potential of waste-to-energy solutions, with facilities being developed to convert waste into valuable resources. This is exemplified by Qatar's focus on integrated waste management solutions, including waste recycling initiatives and the development of new technologies for waste treatment, demonstrating the region's commitment to finding sustainable solutions for its waste management challenges.

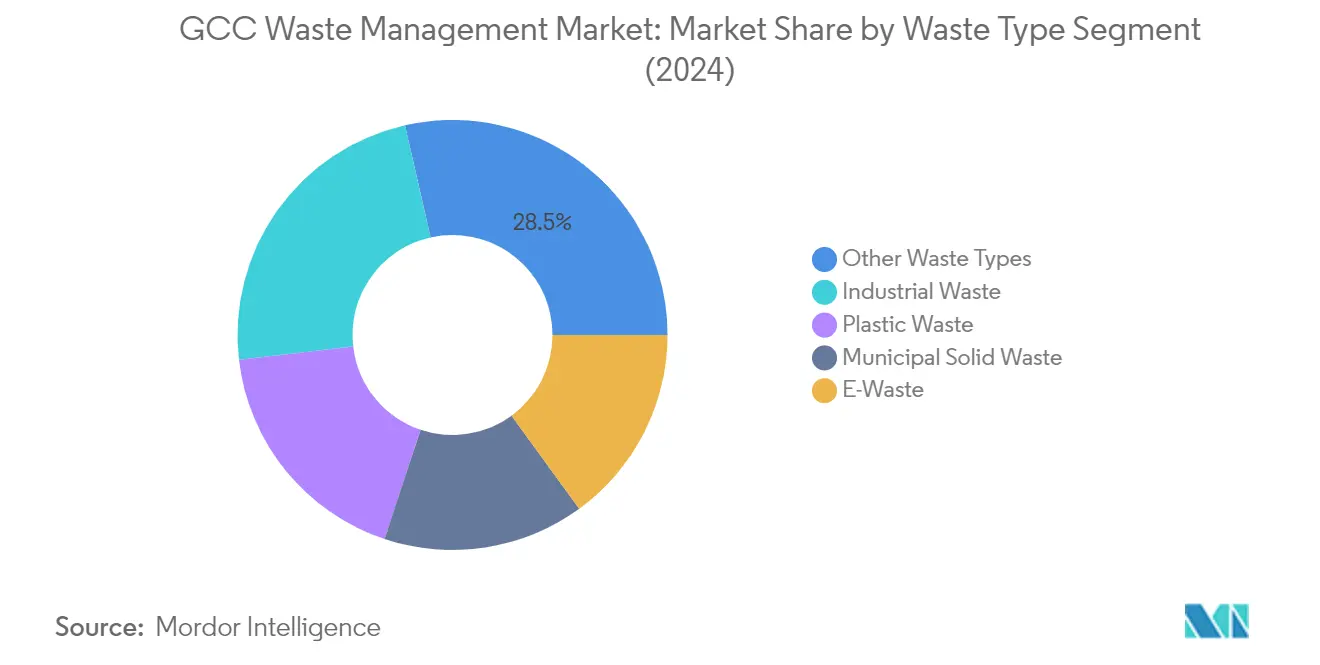

Segment Analysis: By Waste Type

Industrial Waste Segment in GCC Waste Management Market

Industrial waste represents the largest defined segment in the GCC waste management market, accounting for approximately 27% of the total market value in 2024. The segment's dominance is driven by the rapid industrialization across GCC countries, particularly in the petrochemical and manufacturing sectors. The region's industrial waste handling infrastructure has evolved significantly, with advanced technologies being deployed for waste processing and treatment. Several GCC countries have implemented stringent regulations for industrial waste disposal, promoting sustainable practices and encouraging investments in waste treatment facilities. The segment's growth is further supported by increasing investments in manufacturing facilities, backed by low-interest loans from development funds for establishing industrial plants.

Plastic Waste Segment in GCC Waste Management Market

The plastic waste segment is emerging as the most dynamic sector in the GCC waste management market, demonstrating robust growth potential for the period 2024-2029. This growth is primarily driven by increasing environmental awareness and stricter regulations on plastic waste disposal across GCC countries. The segment is witnessing significant technological advancements in recycling capabilities, with new facilities being established across the region. The UAE and Saudi Arabia are leading initiatives in plastic waste management, implementing comprehensive recycling programs and investing in advanced processing facilities. The segment's expansion is further supported by growing corporate commitments to reduce virgin plastic use and increase recycled content in packaging materials, along with government initiatives promoting circular economy principles in plastic waste management.

Remaining Segments in GCC Waste Management Market

The other significant segments in the GCC waste management market include municipal solid waste, e-waste, and various other waste types. Municipal solid waste management continues to evolve with cities implementing smart collection systems and advanced waste sorting facilities. The e-waste segment is gaining prominence due to the region's high technology adoption rate and increasing focus on the proper disposal of electronic devices. Other waste types, including medical waste and construction debris, play crucial roles in shaping the overall market landscape. These segments are witnessing continuous improvements in collection mechanisms, processing technologies, and disposal methods, supported by government initiatives and private sector investments.

Segment Analysis: By Service

Collection Segment in GCC Waste Management Market

The collection segment dominates the GCC waste management market, commanding approximately 74% of the total market share in 2024. This significant market position is attributed to the increasing focus on efficient waste collection systems across GCC countries, particularly in major urban centers. The segment's dominance is further strengthened by the implementation of advanced collection technologies and infrastructure development initiatives by various municipalities. Collection services have become increasingly sophisticated, incorporating smart waste collection systems, GPS-enabled fleet management, and automated collection schedules to optimize routes and improve operational efficiency. The segment's robust performance is also supported by growing public-private partnerships in waste collection services and the increasing adoption of specialized collection vehicles and equipment across residential, commercial waste management, and industrial sectors.

Processing Segment in GCC Waste Management Market

The processing segment is emerging as the fastest-growing segment in the GCC waste management market, projected to grow at approximately 9% during 2024-2029. This accelerated growth is driven by increasing investments in advanced waste processing technologies and facilities across the region. The segment is witnessing significant technological advancements, including the adoption of AI-powered waste sorting systems, automated processing facilities, and innovative waste-to-resource conversion technologies. The growth is further fueled by stringent environmental regulations promoting proper waste processing and the rising emphasis on circular economy principles. GCC countries are increasingly focusing on developing state-of-the-art waste processing facilities to handle various waste streams, including municipal solid waste, industrial waste, and hazardous materials, contributing to the segment's rapid expansion.

Remaining Segments in Service Segmentation

The disposal/recovery segment plays a crucial role in completing the waste management cycle in the GCC region. This segment encompasses various disposal methods, including landfilling, incineration, and resource recovery operations. The segment is witnessing significant transformation with the increasing adoption of sustainable disposal practices and the implementation of waste-to-energy projects across the region. Modern disposal facilities are being equipped with environmental monitoring systems and advanced recovery technologies to minimize environmental impact. The segment is also seeing growing emphasis on material recovery and recycling initiatives, aligned with the broader sustainability goals of GCC nations.

Segment Analysis: By Disposal Method

Landfill Segment in GCC Waste Management Market

The landfill disposal segment continues to dominate the GCC waste management market, holding approximately 79% of the market share in 2024. This significant market position is driven by the widespread use of landfills across GCC countries, particularly in Saudi Arabia, where most municipal waste is disposed of in landfills. The segment's dominance is further reinforced by the relatively low cost of landfill disposal compared to other methods, with current costs averaging around USD 1.87 per ton in major markets like Saudi Arabia. However, the region is witnessing a gradual shift as governments implement stricter regulations and environmental standards for landfill operations, particularly in the UAE and Saudi Arabia, where new engineered landfills are being developed with enhanced environmental protection measures.

Recycling Segment in GCC Waste Management Market

The recycling segment is emerging as the fastest-growing disposal method in the GCC waste management market, projected to grow at approximately 9% during the forecast period 2024-2029. This growth is primarily driven by increasing government initiatives across the GCC region to promote recycling practices and reduce landfill dependency. The UAE is leading this transformation with ambitious recycling targets and investments in advanced recycling facilities, while Saudi Arabia is developing new recycling infrastructure through the Saudi Investment Recycling Company (SIRC). The segment's growth is further supported by rising environmental awareness, implementation of waste segregation practices, and increasing private sector participation in recycling initiatives across the region.

Remaining Segments in Disposal Method

The incineration segment represents a smaller but growing portion of the GCC waste management market, primarily focused on handling hazardous and medical waste. This method is gaining traction due to its ability to significantly reduce waste volume while potentially generating energy. Several waste-to-energy projects are being developed across the GCC, particularly in the UAE and Saudi Arabia, where governments are exploring incineration as part of their sustainable waste management strategies. The segment is seeing increased adoption in urban areas where land availability for landfills is limited, and there is a growing need for more efficient waste disposal methods.

GCC Waste Management Market Geography Segment Analysis

GCC Waste Management Market in Saudi Arabia

Saudi Arabia continues to dominate the GCC waste management landscape, commanding approximately 57% of the total market share in 2024. The kingdom's waste management sector is undergoing a significant transformation, driven by ambitious sustainability goals outlined in Vision 2030. The country has implemented comprehensive strategies to address various waste streams, including municipal solid waste, industrial waste, and construction debris. The government's commitment is evident through the establishment of the National Center for Waste Management (MWAN), which oversees the implementation of advanced waste management practices. The country has also made substantial progress in developing waste-to-energy facilities, with plans to build 3GW of waste-to-energy plants. Furthermore, the Saudi Investment Recycling Company (SIRC) is spearheading efforts to modernize the sector through technological innovation and infrastructure development. The kingdom's approach to waste management has evolved from traditional landfilling to more sustainable practices, including recycling services, composting, and energy recovery.

GCC Waste Management Market in United Arab Emirates

The United Arab Emirates has established itself as a pioneer in sustainable waste management practices across the GCC region. The country has implemented several innovative initiatives, particularly in Dubai and Abu Dhabi, focusing on smart waste management solutions and circular economy principles. The UAE's approach combines advanced technology with environmental consciousness, evident in its deployment of AI-powered waste sorting systems and smart bins. The country has made significant strides in recycling services infrastructure development, with facilities capable of processing various waste streams, including electronic waste, construction debris, and organic waste. The emirates have also introduced strict regulations and guidelines for waste segregation at the source, particularly in commercial and residential areas. Dubai's integrated waste management master plan and Abu Dhabi's Tadweer initiatives demonstrate the country's commitment to achieving zero-waste goals. The UAE's focus on public-private partnerships has attracted significant investments in waste management infrastructure, leading to the development of state-of-the-art recycling services and treatment facilities.

GCC Waste Management Market in Kuwait

Kuwait has demonstrated significant progress in modernizing its waste management infrastructure and practices. The country has moved beyond traditional waste disposal methods to embrace more sustainable approaches, focusing particularly on reducing its environmental footprint. Kuwait's waste management strategy encompasses comprehensive waste collection systems, advanced waste treatment facilities, and innovative recycling services programs. The government has implemented several initiatives to address the challenges of high per capita waste generation, including public awareness campaigns and improved waste segregation practices. The country has also invested in developing specialized facilities for handling various waste streams, including industrial and hazardous waste. Kuwait's emphasis on environmental protection has led to the introduction of stricter regulations for waste disposal and treatment. The nation has also focused on developing partnerships with international waste management companies to bring advanced technologies and best practices to its operations. The modernization of Kuwait's waste management sector continues to attract investments in infrastructure development and technological advancement.

GCC Waste Management Market in Other Countries

The waste management landscape in other GCC countries, including Qatar and Bahrain, exhibits unique characteristics and development patterns. These nations have implemented various initiatives to improve their waste management infrastructure and practices, aligned with their respective national development strategies. Qatar has focused on developing integrated waste management facilities and implementing advanced recycling services technologies, particularly in preparation for and as a legacy of major international events. Bahrain, despite its smaller size, has made significant strides in modernizing its waste management practices, with a particular focus on recycling services and waste-to-energy initiatives. These countries share common challenges, including high per capita waste generation and limited landfill space, driving them to adopt more sustainable waste management solutions. Their approaches to waste management are increasingly focusing on circular economy principles and environmental sustainability, supported by public awareness campaigns and regulatory frameworks.

Get Analysis on Important Geographic Markets

Download PDF

GCC Waste Management Industry Overview

Top Companies in GCC Waste Management Market

The GCC waste management market features prominent players like Averda, EnviroServe, Green Mountains, Veolia, Blue LLC, Envac, SEPCO Environment, and Saudi Investment Recycling Company, among others. Companies are increasingly focusing on technological innovation through the implementation of AI-driven solutions, automated sorting systems, and smart waste collection platforms to improve operational efficiency. Strategic partnerships and collaborations with government entities and private sector players have become crucial for market expansion and service diversification. Companies are investing heavily in developing advanced recycling services facilities and waste-to-energy plants while expanding their geographical presence across different GCC countries. The industry is witnessing a strong push towards circular economy principles, with companies adopting innovative technologies for waste collection, waste processing, and disposal while simultaneously working on reducing environmental impact through sustainable practices.

Market Structure Shows Growing Regional Integration

The GCC waste management market exhibits a moderately diversified structure with a mix of global environmental services conglomerates and local specialized operators. While international players like Veolia bring advanced technological capabilities and global expertise, local companies such as SEPCO Environment and Al Haya Enviro leverage their strong regional networks and understanding of local regulations. The market demonstrates a balanced competitive landscape where both established multinational corporations and emerging regional players maintain significant market presence through different service offerings and geographical focus areas. The industry is experiencing increased consolidation through strategic acquisitions and partnerships, particularly as government initiatives drive the need for integrated waste management solutions.

The market is characterized by strong public-private partnerships, with government bodies playing a crucial role in shaping the competitive dynamics through regulations and infrastructure development initiatives. Major players are increasingly focusing on vertical integration, expanding their service portfolio from collection to advanced recycling and waste-to-energy solutions. The competitive landscape is evolving with the entry of new technology-focused players and the transformation of traditional waste management companies into integrated environmental solution providers. Strategic alliances between local and international players are becoming more common, combining global expertise with local market knowledge.

Innovation and Sustainability Drive Future Success

Success in the GCC waste management market increasingly depends on companies' ability to align with national sustainability goals and circular economy initiatives. Market leaders are strengthening their position by investing in advanced technologies, developing specialized waste treatment facilities, and expanding their service offerings across the value chain. Companies that can demonstrate strong environmental compliance, operational efficiency, and technological innovation while maintaining cost competitiveness are better positioned for long-term success. The ability to secure long-term contracts with government entities and major industrial clients while maintaining operational flexibility to adapt to changing regulatory requirements has become crucial.

Future market success will be determined by companies' capacity to develop comprehensive waste management solutions that address specific regional challenges while meeting international environmental standards. Players must focus on building strong relationships with key stakeholders, including government bodies, industrial clients, and technology providers. The increasing emphasis on environmental sustainability and circular economy principles is reshaping competitive dynamics, with companies needing to demonstrate a clear commitment to reducing environmental impact while maintaining operational efficiency. Success factors include the ability to manage complex logistics networks, implement advanced processing technologies, and develop innovative solutions for waste reduction and recycling.

GCC Waste Management Market Leaders

-

Averda

-

EnviroServe

-

Blue LLC

-

Saudi Investment Recycling Company

-

Envac

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

GCC Waste Management Market News

- December 2023: Electric mobility firm Wardwizard Innovations and Mobility entered into an agreement with the Sharjah Government co-owned sustainable waste management company BEEAH Group (BG) for the manufacturing of electric vehicles. Under this collaboration, Wardwizard Innovations and Mobility, along with BEEAH Group, will jointly promote electric vehicles in GCC nations and the African region.

- October 2022: Marafiq, an integrated utility service provider, commenced the construction of a new state-of-the-art sewage treatment plant at Jeddah Airport II. The project has a capacity of 300,000 m3/d for sewage treatment, with the potential for expansion up to 500,000 m3/d.

- September 2022: Qatar's Public Works Authority, Ashghal, awarded a USD 1.48 billion public-private partnership contract. This contract encompasses the development, design, build, finance, and procurement of a 150,000 cubic meter per day sewage treatment facility. Additionally, the project was granted to a consortium comprising Metito, Al Attiyah Motors and Trading Co., and Gulf Investment Corp.

GCC Waste Management Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

-

4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Increasing demand for mining waste co-disposable

- 4.2.2 Restraints

- 4.2.2.1 The treatment of medical waste and industrial waste requires a lot of cost

- 4.2.3 Opportunities

- 4.2.3.1 Increasing focus towards smart technologies to bolster growth

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Brief on Government Regulations and Initiatives

- 4.6 Insights on the Logistics Support and Development in the GCC Waste Management Industry

- 4.7 Spotlight on Waste Management Contracts

- 4.8 Insights on Waste Recycling in the GCC (Regional Trends, Recycled Materials)

- 4.9 Insights on Technological Advancements and Innovation in Effective Waste Management

- 4.10 Brief on Waste Management Equipment Providers

- 4.11 Insights on Waste Generated by Category (Hospitals, Buildings, Construction, Hotels etc.)

- 4.12 Impact of COVID 19 on the Market

5. MARKET SEGMENTATION

-

5.1 By Waste Type

- 5.1.1 Industrial Waste

- 5.1.2 Municipal Solid Waste

- 5.1.3 Hazardous Waste

- 5.1.4 E-Waste

- 5.1.5 Plastic Waste

- 5.1.6 Bio-Medical Waste

-

5.2 By Disposal Method

- 5.2.1 Collection

- 5.2.2 Landfills

- 5.2.3 Incineration

- 5.2.4 Recycling

-

5.3 By Country

- 5.3.1 United Arab Emirates

- 5.3.2 Saudi Arabia

- 5.3.3 Kuwait

- 5.3.4 Qatar

- 5.3.5 Rest of GCC

6. COMPETITIVE LANDSCAPE

- 6.1 Overview (Market Concentration and Major Players)

-

6.2 Company Profiles

- 6.2.1 Averda

- 6.2.2 EnviroServe

- 6.2.3 Suez Middle East Recycling LLC

- 6.2.4 Green Mountains

- 6.2.5 Veolia

- 6.2.6 Blue LLC

- 6.2.7 Envac

- 6.2.8 SEPCO Environment

- 6.2.9 Wasco

- 6.2.10 Saudi Investment Recycling Company

- 6.2.11 Dulsco Waste Management Services

- 6.2.12 Bee'ah

- 6.2.13 Power Waste Management and Transport LLC

- 6.2.14 Al Haya Enviro

- 6.2.15 Bin-Ovation

- 6.2.16 United Waste Management Company

- 6.2.17 Kuwait Waste Collection and Recycling Company*

- *List Not Exhaustive

7. FUTURE OF THE MARKET

8. INSIGHTS ON INVESTMENT ACTIVITIES (PE AND OTHERS)

9. APPENDIX

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

GCC Waste Management Industry Segmentation

Waste management involves the processes of waste collection, transportation, processing, as well as waste recycling or disposal. The prime objective of waste management is to reduce the number of unusable materials and to avert potential health and environmental hazards.

The Gulf Cooperation Council waste management market is segmented by waste type (industrial waste, municipal solid waste, hazardous waste, e-waste, plastic waste, and bio-medical waste), by disposal methods (collection, landfills, incineration, and recycling), and by country (United Arab Emirates, Saudi Arabia, Qatar, Kuwait, and the rest of GCC).

The report provides market size and forecasts for the Gulf Cooperation Council waste management market in value (USD) for all the above segments.

| By Waste Type | Industrial Waste |

| Municipal Solid Waste | |

| Hazardous Waste | |

| E-Waste | |

| Plastic Waste | |

| Bio-Medical Waste | |

| By Disposal Method | Collection |

| Landfills | |

| Incineration | |

| Recycling | |

| By Country | United Arab Emirates |

| Saudi Arabia | |

| Kuwait | |

| Qatar | |

| Rest of GCC |

Need A Different Region or Segment?

Customize Now

GCC Waste Management Market Research FAQs

How big is the GCC Waste Management Market?

The GCC Waste Management Market size is expected to reach USD 68.25 billion in 2025 and grow at a CAGR of 7.38% to reach USD 97.44 billion by 2030.

What is the current GCC Waste Management Market size?

In 2025, the GCC Waste Management Market size is expected to reach USD 68.25 billion.

Who are the key players in GCC Waste Management Market?

Averda, EnviroServe, Blue LLC, Saudi Investment Recycling Company and Envac are the major companies operating in the GCC Waste Management Market.

What years does this GCC Waste Management Market cover, and what was the market size in 2024?

In 2024, the GCC Waste Management Market size was estimated at USD 63.21 billion. The report covers the GCC Waste Management Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the GCC Waste Management Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

GCC Waste Management Market Research

Mordor Intelligence provides a comprehensive analysis of the waste management industry across the GCC region. With decades of expertise in environmental services research, our detailed report covers the full range of waste collection and garbage disposal operations. This includes practices in solid waste management, medical waste management, and hazardous waste management. The analysis addresses crucial aspects such as waste recycling, waste sorting, and waste to energy technologies. These insights offer stakeholders actionable information on both industrial waste handling and municipal solid waste management strategies.

The report, available as an easy-to-download PDF, provides valuable insights for organizations involved in waste processing, waste treatment, and waste recovery operations. Our analysis covers the entire value chain, from residential waste collection to commercial waste management, including waste transportation and industrial waste management solutions. Stakeholders benefit from detailed assessments of recycling services, electronic waste management, and municipal waste management practices. This is supported by comprehensive data on waste disposal trends and refuse management systems. The report offers strategic recommendations for optimizing trash management operations and enhancing waste handling efficiency across the GCC region.