Market Size of GCC Telecom Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

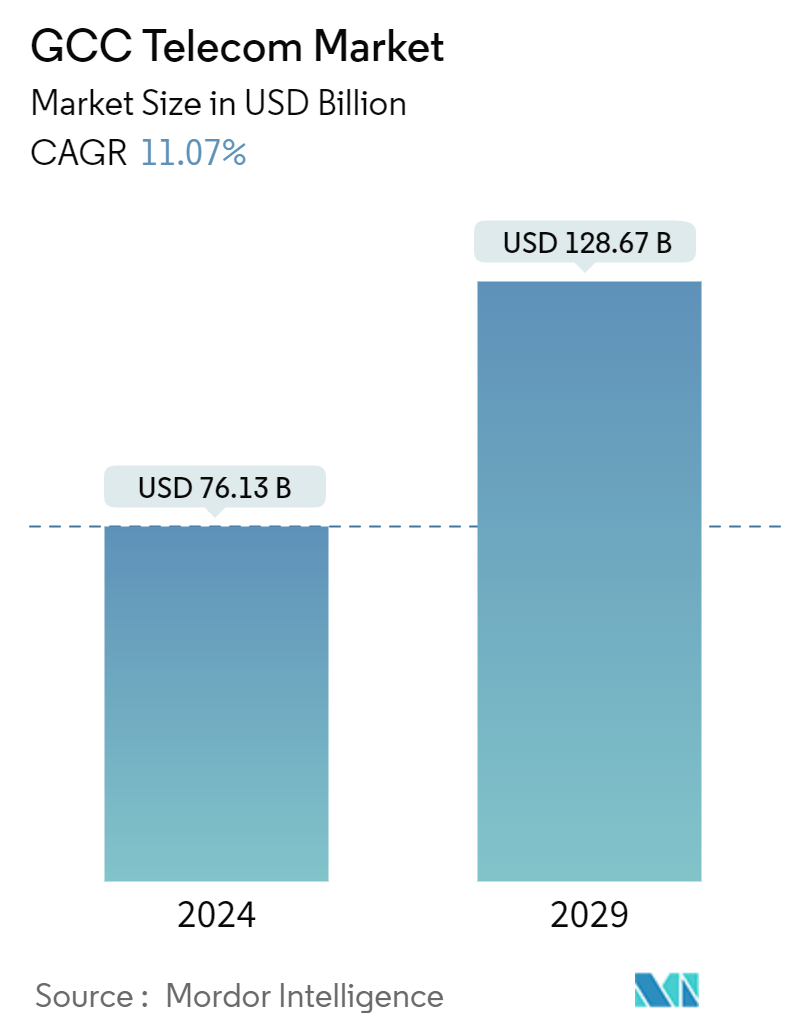

| Market Size (2024) | USD 76.13 Billion |

| Market Size (2029) | USD 128.67 Billion |

| CAGR (2024 - 2029) | 11.07 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

GCC Telecom Market Analysis

The GCC Telecom Market size is estimated at USD 76.13 billion in 2024, and is expected to reach USD 128.67 billion by 2029, growing at a CAGR of 11.07% during the forecast period (2024-2029).

- The telecom sector in the Gulf Cooperation Council (GCC) region is anticipated to expand primarily due to the growing urban population and the widespread use of cell phones that enable 3G, 4G, and 5G services. The Internet of Things (IoT), which connects with wired and wireless internet, is predicted to be used more in the telecom industry throughout the forecast period.

- According to the November 2023 Ericsson Mobility Report, mobile subscriptions in GCC are expected to increase from 76 million in 2023 to 81 million by 2029. By the end of 2023, 5G subscriptions were projected to constitute 34% of all mobile subscriptions, totaling 26 million subscriptions. Over the forecast period, 5G subscriptions are projected to grow annually at 19%, reaching 75 million by 2029 and accounting for approximately 90% of total subscriptions.

- The GCC telecommunications market has experienced substantial changes in recent years. These shifts are attributed to government efforts aimed at enhancing internet infrastructure and broadband connectivity, increased data consumption by both businesses and individuals, widespread adoption of 5G technology, and innovations introduced by major telecom vendors.

- In April 2024, Ericsson and Etihad Etisalat (Mobily) signed a memorandum of understanding (MoU) during LEAP 2024 in Riyadh, Saudi Arabia. The collaboration aims to enhance and evolve the network in Saudi Arabia using open radio access network (RAN) principles, with a focus on boosting network flexibility. As part of this initiative, they will explore different 5G deployment options within a flexible network architecture, including purpose-built RAN and Cloud RAN.

- For instance, a crucial platform for Saudi Arabia's Vision 2030 is the National Broadband Network of Saudi Arabia. The central government aims to finance significant resources and policies to create an all-encompassing fiber network. The region is witnessing many partnerships and developments in the fiber and broadband network area, strengthening the nation's overall telecom sector.

- Telecom operators face intensifying market competition. Thus, they are looking to optimize costs and pricing, giving rise to tower sharing amongst the operators. This has led to a significant shift in the focus area of telecom operators from network coverage, branding, and service design to tower sharing. Tower sharing provides potential reductions in operating and capital costs, which helps the telecom operator focus more effectively on marketing and customer satisfaction, thereby increasing the network reach.

- After the COVID-19 pandemic, the GCC telecom market experienced notable growth driven by increased demand for digital services and remote connectivity solutions. Countries like the United Arab Emirates and Saudi Arabia saw a surge in e-commerce and digital payments, boosting telecom revenues. Qatar and Bahrain also witnessed expansion, with investments in 5G infrastructure driving innovation and market competitiveness. Overall, the pandemic accelerated digital transformation, propelling the GCC telecom sector to new heights.

GCC Telecom Industry Segmentation

The telecommunication industry is largely concerned with the operations and provision of infrastructure for transmitting data, voice, image, sound, text, and video. The GCC telecom market study tracks the overall revenue accrued through the sale of network, voice, and data services by telecom providers in the Gulf Cooperation Council.

The GCC telecom market is segmented by telecom services (voice services (wired and wireless), data and messaging services, and payTV services), telecom connectivity (fixed network and mobile network), and country (Saudi Arabia, Kuwait, Qatar, Oman, United Arab Emirates, and Bahrain). The market sizes and forecasts are provided in USD for all the above segments.

| Overall telecom revenue | |

| Telecom Subscriptions | |

| Average revenue per user |

| Telecom services | ||||

| ||||

| Data and Messaging Services | ||||

| PayTV Services |

| Telecom connectivity | |

| Fixed Network | |

| Mobile Network |

| Country | |

| Saudi Arabia | |

| Kuwait | |

| Qatar | |

| Oman | |

| United Arab Emirates | |

| Bahrain |

GCC Telecom Market Size Summary

The GCC telecom market is poised for significant growth, driven by the increasing urban population and the widespread adoption of advanced mobile technologies such as 3G, 4G, and 5G. The sector is experiencing a transformation due to enhanced internet infrastructure, government initiatives, and the proliferation of IoT applications. Key players like Saudi Telecom Company (STC), e& Etisalat, and Oman Telecommunications Company (Omantel) are at the forefront, focusing on expanding 5G networks and improving digital services. The market is also witnessing strategic partnerships and investments aimed at enhancing network capacity and flexibility, such as the collaboration between Ericsson and Etihad Etisalat (Mobily) in Saudi Arabia. These developments are supported by government policies promoting fiber-optic networks and digital transformation, particularly in Saudi Arabia's Vision 2030.

The competitive landscape in the GCC telecom market is characterized by a moderate consolidation, with major operators and several internet service providers (ISPs) and mobile virtual network operators (MVNOs) vying for market share. The demand for high-speed internet and digital services has surged, particularly post-COVID-19, as countries like the UAE and Saudi Arabia see increased e-commerce and digital payment activities. Investments in infrastructure, such as Zain KSA's expansion of its 5G network, and strategic alliances, like those between Ericsson and Du, are pivotal in driving innovation and enhancing customer experience. The market's growth is further fueled by aggressive IT modernization projects and the liberalization of the telecom industry, which are enhancing service levels and fostering competition across the region.

GCC Telecom Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Suppliers

-

1.2.2 Bargaining Power of Consumers

-

1.2.3 Threat of New Entrants

-

1.2.4 Threat of Substitutes

-

1.2.5 Intensity of Competitive Rivalry

-

-

1.3 An Assessment of the impact of COVID-19 on the Industry

-

-

2. MARKET SEGMENTATION

-

2.1 Overall telecom revenue

-

2.1.1 Telecom Subscriptions

-

2.1.2 Average revenue per user

-

-

2.2 Telecom services

-

2.2.1 Voice Services

-

2.2.1.1 Wired

-

2.2.1.2 Wireless

-

-

2.2.2 Data and Messaging Services

-

2.2.3 PayTV Services

-

-

2.3 Telecom connectivity

-

2.3.1 Fixed Network

-

2.3.2 Mobile Network

-

-

2.4 Country

-

2.4.1 Saudi Arabia

-

2.4.2 Kuwait

-

2.4.3 Qatar

-

2.4.4 Oman

-

2.4.5 United Arab Emirates

-

2.4.6 Bahrain

-

-

GCC Telecom Market Size FAQs

How big is the GCC Telecom Market?

The GCC Telecom Market size is expected to reach USD 76.13 billion in 2024 and grow at a CAGR of 11.07% to reach USD 128.67 billion by 2029.

What is the current GCC Telecom Market size?

In 2024, the GCC Telecom Market size is expected to reach USD 76.13 billion.