GCC Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

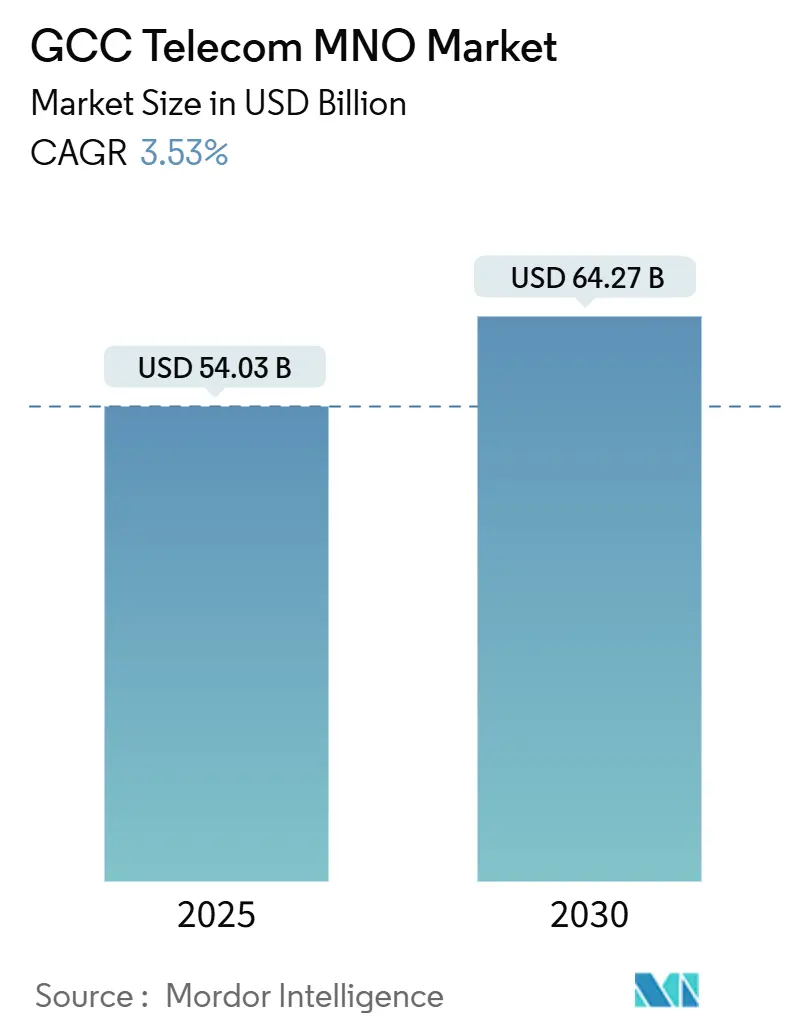

| Market Size (2025) | USD 54.03 Billion |

| Market Size (2030) | USD 64.27 Billion |

| Growth Rate (2025 - 2030) | 3.53% CAGR |

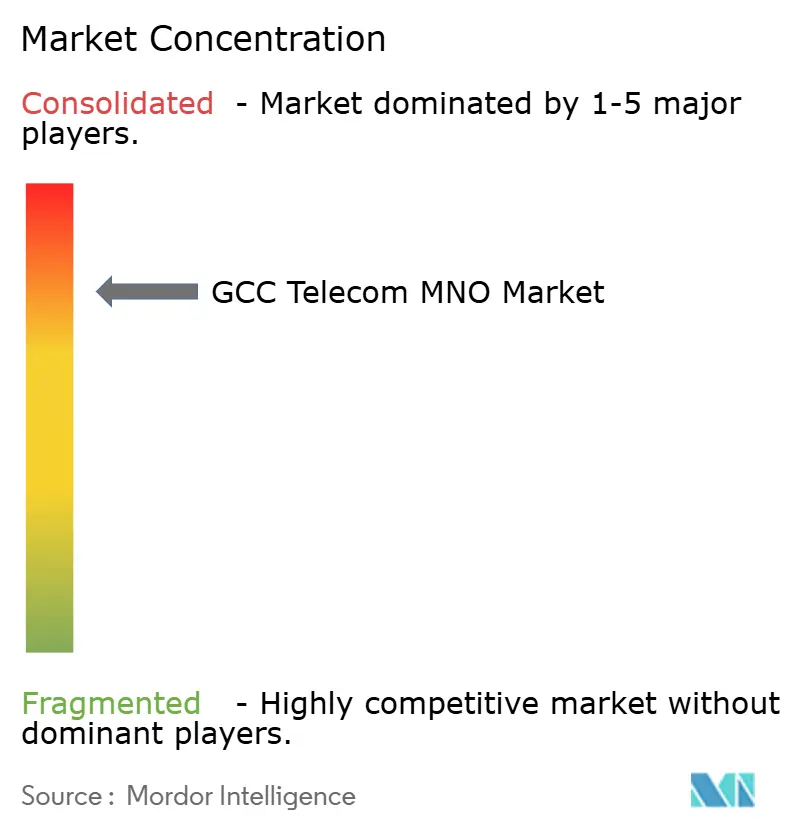

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

GCC Telecom MNO Market Analysis by Mordor Intelligence

The GCC Telecom MNO Market size is estimated at USD 54.03 billion in 2025, and is expected to reach USD 64.27 billion by 2030, at a CAGR of 3.53% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 103.15 million subscribers in 2025 to 120.67 million subscribers by 2030, at a CAGR of 3.19% during the forecast period (2025-2030).

The industry’s growth pattern underscores a shift from subscriber-led expansion to revenue optimization through enterprise services, advanced data products, and digital ecosystem enablement, an evolution closely aligned with national diversification agendas across the Gulf. Much of the incremental value flows from 5G-driven data monetization, a rising mix of managed services for industry verticals, and fresh wholesale income from new submarine-cable landings. Competition is intensifying as liberal MVNO policies unlock niche propositions, yet scale economics continue to favor incumbent MNOs that command extensive tower portfolios and international connectivity assets. Network modernization and energy-efficient RAN upgrades remain essential levers for cost control as spectrum fees and tower-power costs weigh on margins.

Key Report Takeaways

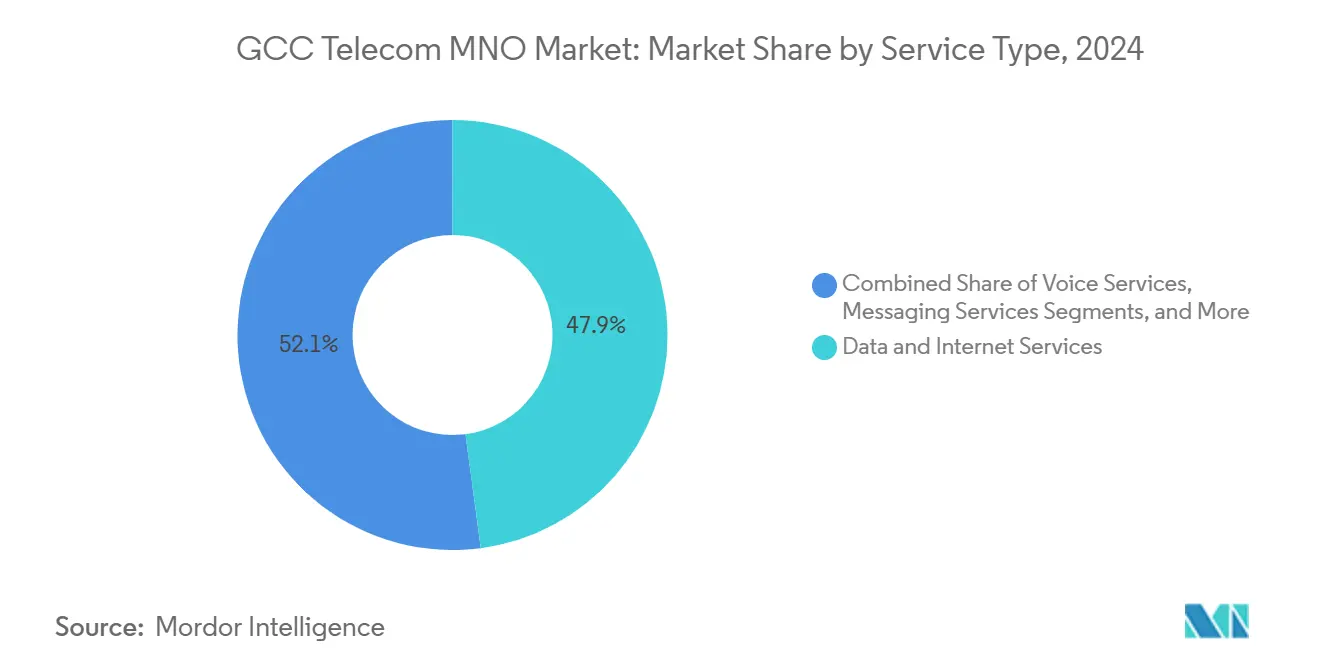

- By service type, data and internet Services captured 47.91% of the GCC telecom MNO market share in 2024, while IoT and M2M Services are advancing at a 3.61% CAGR through 2030.

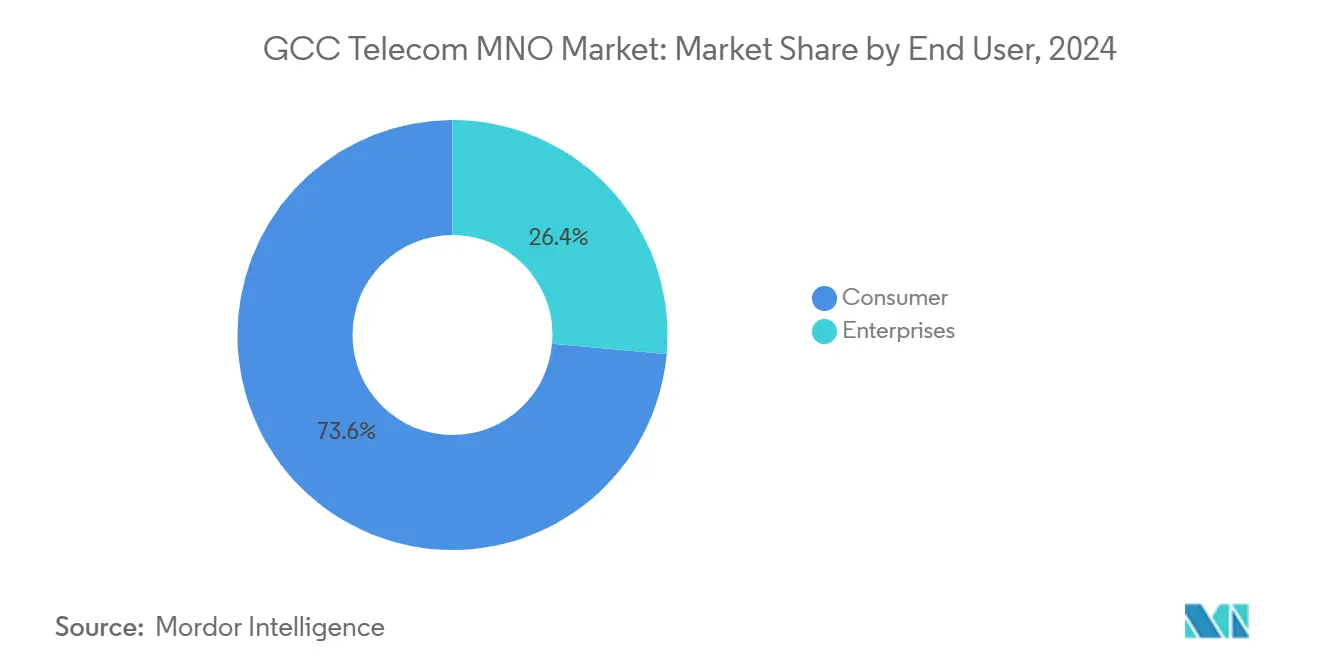

- By end user, consumer connections represented 73.59% of the GCC telecom MNO market size in 2024, yet enterprise subscriptions are projected to expand at a 3.92% CAGR to 2030.

- By country, Saudi Arabia led with 42.54% revenue share in 2024; Bahrain is forecast to grow fastest at a 3.70% CAGR through 2030.

GCC Telecom MNO Market Trends and Insights

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G roll-out and soaring data traffic | +1.2% | GCC-wide, strongest in UAE and Saudi Arabia | Medium term (2-4 years) |

| National digital-economy agendas (e.g., Vision 2030) | +0.8% | Saudi Arabia primary, spillover to Kuwait and UAE | Long term (≥ 4 years) |

| Oil and gas IoT/M2M connectivity demand | +0.6% | Saudi Arabia, UAE, Qatar core markets | Medium term (2-4 years) |

| Private-5G networks in industrial zones and ports | +0.4% | UAE and Saudi Arabia leading, Oman emerging | Medium term (2-4 years) |

| New submarine-cable landings lowering transit costs | +0.3% | Regional connectivity hubs: UAE, Bahrain | Long term (≥ 4 years) |

| Liberal MVNO licensing unlocking niche segments | +0.2% | Kuwait and Bahrain early adopters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

5G Roll-out and Soaring Data Traffic

Regional 5G penetration already exceeds 40%, reversing earlier ARPU pressure observed in the 4G era and opening premium revenue streams tied to ultra-low-latency applications [1]Huawei, “Middle East: Leading the 5.5G Era and Striding Towards an Intelligent World,” huawei.com. Zain KSA alone invested SAR 1.6 billion (USD 427 million) in 2024 to densify sustainable 5G sites that deliver both coverage and energy savings [2]Telecom Talk, “Zain KSA Invests SAR 1.6 Billion in Sustainable 5G Infrastructure,” telecomtalk.info. Operators monetize the technology through network slicing for enterprise SLAs and fixed-wireless access propositions that offset fiber gaps. Increasing mobile-data usage, averaging 21.6 GB per SIM monthly by late 2024, supports differentiated tariff tiers built around speed and content bundling. The network foundation also underpins cognitive-city pilots such as NEOM, where immersive services serve as a proof point for future regional deployments.

National Digital-Economy Agendas

Saudi Vision 2030, the UAE’s digital-economy policy, and Kuwait Vision 2035 each embed robust connectivity goals that de-risk operator capex by offering long-term policy clarity. A notable example is Aramco Digital’s 450 MHz spectrum award specifically reserved for industrial 5G, signaling a regulatory intent to align spectrum policy with enterprise transformation. Sovereign cloud and data-center programs further drive wholesale backhaul demand, while smart-city funding pipelines link telecom infrastructure directly to national competitiveness metrics. Such alignment cushions operators against cyclical consumer revenues and sustains multi-year network-upgrade roadmaps.

Oil and Gas IoT/M2M Connectivity Demand

Energy producers view real-time data as mission-critical, leading ADNOC and e& to commit to a private 5G deployment spanning 11,000 km², covering 12,000 wells and pipelines with USD 1.5 billion in contract value over five years [3]Indian Chemical News, “ADNOC and e& to Build Energy Industry's Largest Private 5G Wireless Network,” indianchemicalnews.com . These industrial networks transmit telemetry for predictive maintenance and safety monitoring and carry latency-sensitive control traffic that commands premium SLAs. The sector’s high barrier to entry and long asset lifecycles translate into multi-year connectivity contracts that enhance revenue visibility for mobile operators. Similar initiatives in Qatar’s LNG complexes and Kuwait’s upstream fields replicate the model, underscoring how oil-and-gas IoT uptake contributes a steady uplift to the GCC telecom MNO market.

Private-5G Networks in Industrial Zones and Ports

Free-zone operators, logistics parks, and container ports increasingly demand sliceable campus networks that guarantee deterministic performance for automated guided vehicles and robotics. UAE’s Jebel Ali Port and Saudi industrial estates have issued multi-year RFPs that bundle design, deployment, and managed-service fees, creating an annuity-style revenue layer for participating MNOs. The engagements broaden operator skill sets into systems integration, edge computing, and cybersecurity, differentiating them from pure-play ISPs. Successful pilots are now scaling to broader footprints, demonstrating a replicable enterprise-go-to-market that further enlarges the GCC telecom MNO market.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High spectrum‐license and renewal fees | -0.7% | Saudi Arabia and UAE primary impact | Medium term (2-4 years) |

| Market saturation (≥135% SIM penetration) | -0.5% | GCC-wide, acute in UAE and Qatar | Short term (≤ 2 years) |

| Slow progress on cross-border 5G roaming | -0.3% | Regional connectivity challenges | Long term (≥ 4 years) |

| Single-vendor RAN supply-chain risk | -0.2% | Technology dependency concerns | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Spectrum-License and Renewal Fees

Auctions structured to maximize fiscal receipts push upfront costs higher just as operators must fund 5G roll-outs, squeezing free cash flow and raising payback thresholds. The January 2025 auction in Costa Rica, where more than 1 GHz of 5G spectrum drew steep reserve prices, illustrates how aggressive pricing can ripple across global policy debates. In the Gulf, regulators are increasingly weighing long-term digital-economy targets against one-off auction income, yet fee levels remain material drains on operator balance sheets. Elevated license renewals compel tighter opex controls and may delay mid-band expansion, tempering the overall GCC telecom MNO market growth contribution from next-gen services.

Market Saturation (≥ 135% SIM Penetration)

SIM penetration above 135% in markets such as the UAE constrains incremental subscriber additions and intensifies price competition in the consumer segment. As a result, operators rely on ARPU-accretive service bundling and upselling of higher data tiers to sustain revenue, but discounting pressure persists. High churn, driven by multi-SIM behavior and prepaid migration patterns, inflates acquisition costs and dilutes marketing ROI. Consequently, incremental growth must originate from enterprise, fixed-mobile convergence, and value-added solutions rather than from pure subscriber gains, making strategic diversification essential to preserve the GCC telecom MNO market trajectory.

Segment Analysis

By Service Type: Data Dominance Drives IoT Upside

Data and Internet Services represented 47.91% of the GCC telecom MNO market size in 2024, cementing their role as the primary revenue engine for regional operators. High-definition video streaming, which accounted for nearly 60% of traffic, underpinned robust 21.6 GB monthly usage per smartphone that year. Enhanced 5G coverage and device subsidies accelerated migration toward unlimited or speed-tiered plans, pushing blended data ARPU higher despite saturated subscriber bases. Voice and messaging volumes continue to erode as OTT applications proliferate; however, carrier voice retains relevance for enterprise mission-critical and emergency services, preserving a stabilizing albeit declining cash flow line.

IoT and M2M Services are forecast to deliver a 3.61% CAGR, outpacing all other categories, as industrial automation and smart-city mandates scale across the region. The ADNOC-e& private 5G blueprint and Aramco Digital’s spectrum-backed Industry 4.0 push exemplify how asset-intensive sectors translate operational imperatives into long-term connectivity partnerships. These specialized services demand bespoke SLAs, cybersecurity overlays, and edge analytics integration, enabling operators to command price premiums that mitigate commodity data tariff compression. OTT/Pay-TV and value-added services further diversify revenue, particularly where exclusive sports rights bolster subscriber stickiness.

Note: Segment shares of all individual segments available upon report purchase

By End User: Enterprise Momentum Rebalancing Revenue Mix

Consumer subscriptions generated 73.59% of the GCC telecom MNO market size in 2024, yet flat population growth and multi-SIM ownership limit upside. Operators respond by packaging mobile, fixed broadband, and content to elevate household spending, while loyalty programs and digital-wallet tie-ins aim to curb churn. 5G fixed wireless access additionally targets underserved suburban households, providing incremental ARPU with minimal incremental fiber capex.

Enterprise lines are projected to grow at a 3.92% CAGR through 2030, outpacing consumer and gradually tilting the revenue balance in favor of B2B. National digital agendas require robust connectivity for government, energy, and logistics projects, motivating long-term contracts that bundle connectivity with cloud adjacency, edge services, and cybersecurity. STC Group’s managed-service wins in smart-industrial parks and du’s launch of GPU-as-a-Service for advanced analytics illustrate how operators now function as full-stack ICT partners rather than commodity bandwidth providers. This shift not only diversifies income but raises switching costs, reinforcing enterprise customer loyalty and supporting the sustained expansion of the GCC telecom MNO market.

Geography Analysis

Saudi Arabia commanded 42.54% of 2024 revenue, reflecting economic scale, Vision 2030’s digital ambitions, and extensive 5G infrastructure. The new Telecommunications and Information Technology Act, which took effect in December 2022, broadened regulated services to cover IoT and VoIP, formalizing pathways for innovative offerings. STC Group posted SAR 75.89 billion (USD 20.24 billion) revenue in 2024, maintaining a 43.2% share against Mobily and Zain, while fresh spectrum allocations such as Aramco Digital’s 450 MHz license highlight an enterprise-centric regulatory approach. Substantial tower carve-outs and shared-infrastructure initiatives also free capital for data-center and edge-compute investments that will underpin future demand within the GCC telecom MNO market.

The UAE retains hub status through aggressive hyperscaler attraction and submarine-cable projects that expand wholesale capacity. e& recorded AED 59.2 billion (USD 16.12 billion) revenue in 2024, complemented by du’s double-digit profit growth as both firms harvested gains from converged offerings and inbound data traffic. The formation of Khazna Data Centers via the G42-e& partnership enlarges colocation supply while cementing the federation’s role in trans-continental data flows [G42]. Continuous 5G densification supports rapidly growing cloud-gaming and AR-trade applications, reinforcing domestic consumption and transit revenue streams.

Bahrain, though modest in scale, is the fastest-growing geography with a 3.70% CAGR to 2030. A progressive regulatory stance fast-tracked nationwide 5G coverage, and strategic positioning as a financial services center amplifies enterprise bandwidth requirements. Beyon’s Q1 2025 revenue rose 6% year-over-year to USD 312 million on higher data and wholesale earnings, while the planned 1,400 km Al Khaleej cable promises lower latency inter-GCC routes [4]e&, “e& and Batelco to Land Al Khaleej Subsea Cable in the UAE,” eand.com. Kuwait and Oman contribute incremental upside, leveraging Vision 2035 reforms and new entrant competition. Vodafone’s capture of a 12% share in Oman by late 2024 attests to latent demand tapped through novel pricing and enterprise packages. Collectively, these developments reinforce a diversified country footprint that underpins the GCC telecom MNO market expansion.

Competitive Landscape

Regional telecoms exhibit moderate concentration: incumbents retain economies of scale in spectrum holdings and towers, yet regulatory liberalization fosters fresh rivalry. In Saudi Arabia, STC, Mobily, and Zain combine for a balanced triopoly that tempers pricing aggression while encouraging service differentiation. February 2025’s fusion partnership between STC Group and Ericsson underscores a strategy of leveraging vendor collaboration for faster 5G feature rollouts and streamlined capex efficiency, a template other MNOs may emulate as network complexity rises.

MVNO frameworks have widened addressable niches, allowing lifestyle-, expatriate- and IoT-focused brands to enter at lower capital intensity. Kuwait and Bahrain lead on licence issuance, nudging incumbents toward wholesale deals that unlock incremental capacity utilization without eroding retail brands. Parallelly, infrastructure arms races pivot to international connectivity: e& and Batelco’s agreement to land the Al Khaleej cable exemplifies how carriers seek ownership stakes in subsea assets to secure transit economics and differentiate latency-sensitive enterprise offerings.

Enterprise digitalization shapes a new battleground where operators combine private 5G, edge, cloud, and cybersecurity into bundled propositions. ADNOC and e&’s USD 1.5 billion private 5G contract covering 11,000 km² highlights the revenue potential of vertical solutions in oil and gas. Players now market themselves as end-to-end ICT integrators, partnering with Hyperscalers for cloud adjacency and with industrial OEMs for turnkey automation. The strategy hedges consumer ARPU erosion and firmly aligns operator roadmaps with national diversification goals, anchoring the long-term resilience of the GCC telecom MNO market.

GCC Telecom MNO Industry Leaders

-

stc (Saudi Telecom Company)

-

e&UAE (Etisalat)

-

Omani Qatari Telecommunications Company (Ooredoo)

-

Zain Group

-

du (Emirates Integrated Telecommunications Co.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: du launched GPU-as-a-Service while Ooredoo Kuwait demonstrated 5G Advanced readiness, showcasing ongoing service diversification.

- January 2025: Power International Holding acquired Mobile Telecom-Service LLP, including the Altel and Tele2 brands, expanding its 5G footprint in Kazakhstan.

- January 2025: STC Group and Ericsson unveiled a fusion partnership to enhance network innovation and accelerate 5G services across the Gulf.

- July 2024: ADNOC and e& announced a project to build a private 5G network covering 11,000 km² and 12,000 assets, valued at USD 1.5 billion.

- June 2024: Aramco Digital obtained a 450 MHz license to create dedicated Industry 4.0 networks across Saudi Arabia.

- February 2024: e& and Batelco signed an MoU to land the 1,400 km Al Khaleej subsea cable in the UAE, boosting regional interconnectivity.

GCC Telecom MNO Market Report Scope

The telecommunication industry is largely concerned with the operations and provision of infrastructure for transmitting data, voice, image, sound, text, and video. The GCC telecom market study tracks the overall revenue accrued through the sale of network, voice, and data services by telecom providers in the Gulf Cooperation Council.

The GCC telecom market is segmented by telecom services (voice services (wired and wireless), data and messaging services, and payTV services), telecom connectivity (fixed network and mobile network), and country (Saudi Arabia, Kuwait, Qatar, Oman, United Arab Emirates, and Bahrain). The market sizes and forecasts are provided in USD for all the above segments.

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International, Enterprise and Wholesale, etc.) |

| Enterprises |

| Consumer |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Bahrain |

| Oman |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International, Enterprise and Wholesale, etc.) | |

| End-user | Enterprises |

| Consumer | |

| Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Bahrain | |

| Oman |

Key Questions Answered in the Report

What is the current value and 2030 outlook for GCC telecom MNO revenue?

It stands at USD 54.03 billion in 2025 and is projected to reach USD 64.27 billion by 2030, reflecting a 3.53% CAGR.

Which GCC country contributes the largest share of operator revenue?

Saudi Arabia leads with 42.54% of 2024 revenue, supported by Vision 2030 digital priorities and extensive 5G roll-outs.

How quickly are enterprise services expanding for Gulf mobile operators?

Enterprise subscriptions are growing at a 3.92% CAGR to 2030, outpacing consumer lines as firms digitize operations.

What portion of operator income comes from data and internet services?

Data and internet services accounted for 47.91% of 2024 revenue, driven by rising 5G traffic and video streaming.

Why are private 5G networks becoming popular in the region?

Energy, port and industrial zones demand low-latency, sliceable connectivity, prompting long-term private-network deals.

Which factors most constrain revenue growth for Gulf operators?

High spectrum fees and SIM penetration above 135% squeeze margins and limit fresh subscriber gains.

Page last updated on: