| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Volume (2025) | 2.38 Million tonnes |

| Market Volume (2030) | 2.90 Million tonnes |

| CAGR | 4.01 % |

Major Players

*Disclaimer: Major Players sorted in no particular order |

GCC Rigid Plastic Packaging Market Analysis

The GCC Rigid Plastic Packaging Market size in terms of shipment volume is expected to grow from 2.38 million tonnes in 2025 to 2.90 million tonnes by 2030, at a CAGR of 4.01% during the forecast period (2025-2030).

The GCC rigid plastic packaging industry is experiencing significant transformation driven by rapid urbanization and changing consumer demographics. According to recent data, most GCC nations have achieved an urbanization rate exceeding 80%, fundamentally altering consumption patterns and packaging demands. This urbanization trend has led to a substantial increase in modern retail formats and organized supply chains, necessitating more sophisticated plastic packaging solutions. The shift in consumer preferences towards convenience and ready-to-use products has further accelerated the adoption of rigid packaging across various industries. The region's economic diversification initiatives and growing middle-class population have created new opportunities for packaging innovations, particularly in premium and sustainable packaging segments.

The industry landscape is witnessing substantial technological advancements and capacity expansions to meet evolving market demands. A notable example is Almarai's recent installation of two new Sidel PET complete lines at its Al Kharj central processing plant, each capable of handling 54,000 bottles per hour, demonstrating the scale of investment in modern packaging infrastructure. These technological upgrades are enabling manufacturers to improve production efficiency, reduce material waste, and enhance product quality. The integration of advanced manufacturing processes has also facilitated the development of lighter-weight plastic container solutions without compromising structural integrity, addressing both cost and sustainability concerns.

The food and beverage sector remains a primary growth driver for rigid plastic packaging in the GCC region. Recent market analysis indicates that Saudi Arabia's domestic food consumption has reached 3,130 calories per person per day, creating an annual consumption growth rate of 18.5% in the food sector. This surge in food consumption, coupled with changing dietary habits and increasing preference for packaged foods, has led to unprecedented demand for innovative packaging solutions. The industry is responding with new product developments focused on extended shelf life, improved barrier properties, and enhanced consumer convenience.

The market is experiencing a significant shift towards sustainable packaging solutions, driven by both regulatory requirements and changing consumer preferences. Major industry players are investing in research and development to create eco-friendly packaging alternatives while maintaining the functional benefits of rigid plastic packaging. The industry is witnessing increased adoption of recycled materials and the development of mono-material packaging solutions to improve recyclability. These sustainability initiatives are reshaping product development strategies and manufacturing processes across the value chain, while also opening new opportunities for innovation in material science and packaging design.

GCC Rigid Plastic Packaging Market Trends

Demand for Recyclable Rigid Plastic Packaging is Expected to Increase with New Regulations

Many countries' governments in the GCC region are actively supporting the adoption of plastic packaging through new regulations and initiatives to develop recyclable packaging manufacturing facilities. For instance, in January 2023, the UAE's Ministry of Industry and Advanced Technology (MoIAT) published a decree regulating the sale of recycled plastic bottle water bottles in accordance with food safety standards, which will help attract new investments by growing the plastic recycling sector. Additionally, the UAE government collaborated with food and beverage company Agthia to establish a recycling factory for PET packaging in Abu Dhabi, demonstrating the increasing demand for recyclable rigid plastic packaging in the region.

The Kingdom of Saudi Arabia and other GCC countries are focusing intensively on developing a circular plastics economy through various initiatives. Saudi Vision 2030 has prioritized waste management, particularly plastic waste management, with predictions indicating that recycling could generate USD 32 billion in yearly revenue by 2035. Many companies are expanding their product lines by introducing recyclable rigid plastic packaging products to fulfill environmental needs. For example, in December 2022, SABIC developed a unique HDPE packaging for blow molding motor oil and lubricant bottles, showcasing the company's commitment to advancing a circular economy for plastic packaging in Saudi Arabia.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Demand for Rigid Plastic Packaging to Increase Shelf Life of the Products

The demand for rigid plastic packaging solutions has been experiencing significant growth due to its superior capabilities in protecting and preserving products, particularly in the food and beverage sector. These packaging solutions are extensively used when transporting items that need extra safeguarding and shape preservation, offering superior toughness, affordability, and capacity to maintain fresh food products. The growing food delivery sector and changing consumer preferences toward packaged, processed, and pre-cooked foods have further accelerated this demand, with rigid plastic packaging emerging as the preferred choice for ensuring longer shelf life and maintaining product quality.

The pharmaceutical and healthcare sectors are increasingly adopting pharmaceutical plastic packaging solutions due to their ability to protect sensitive medical products and extend shelf life. The region's healthcare sector is witnessing substantial growth, with the pharmacy retail market in Saudi Arabia projected to reach USD 10.01 billion by 2026. Many types of rigid plastics are being employed more frequently due to their ability to maintain product integrity and extend shelf life. For instance, in November 2022, Abu Dhabi Medical Devices Company (ADMD) and Borouge signed an agreement for the supply of plastics and development of the medical device industry, with a strong focus on polyolefin, a thermoplastic polymer commonly used in packaging and medical equipment that offers superior product protection and shelf life extension capabilities.

Segment Analysis: By Material

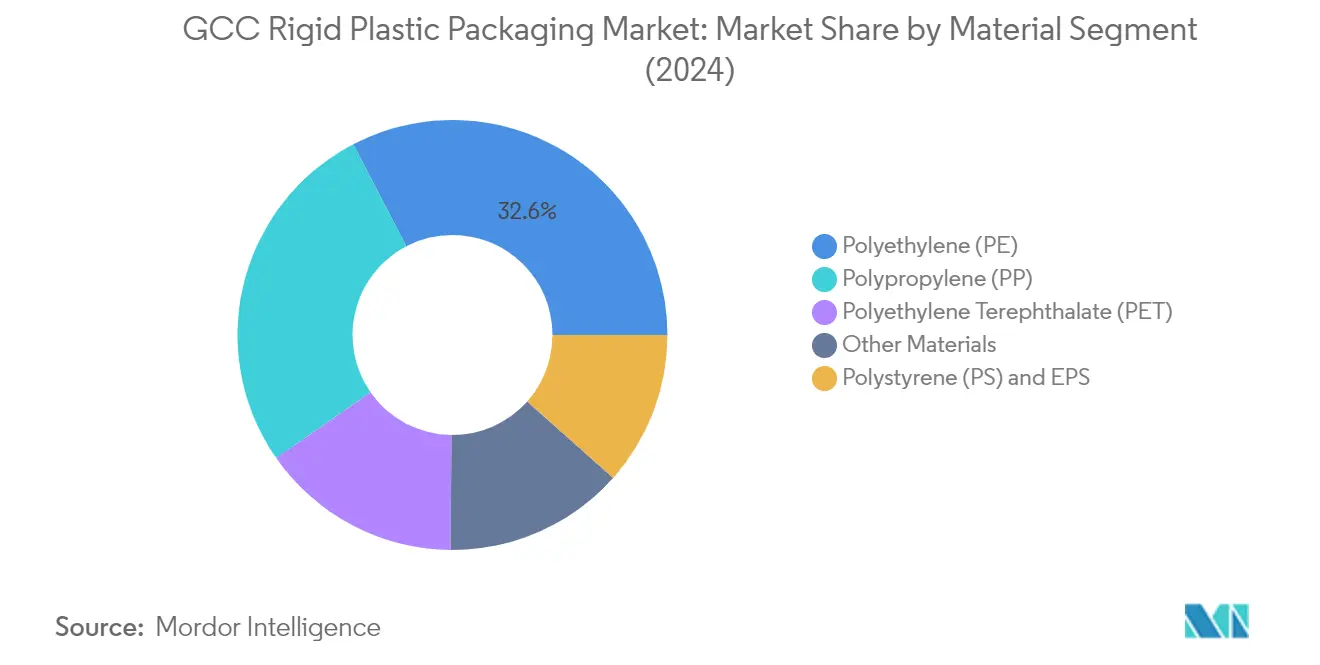

Polyethylene (PE) Segment in GCC Rigid Plastic Packaging Market

Polyethylene (PE) maintains its dominant position in the GCC rigid plastic packaging market, commanding approximately 33% market share in 2024. PE's market leadership is driven by its versatility, easy processability, and recyclability, making it the preferred choice across various plastic packaging applications. The material's high durability and chemical resistance properties have made it particularly valuable in food packaging, beverage containers, and pharmaceutical packaging applications. Companies like SABIC and Takween offer numerous products made from HDPE copolymers and homopolymers for rigid plastic packaging markets. The segment's growth is further supported by the region's rich availability of raw materials, with Saudi Arabia being one of the largest producers of polyolefins in the Middle Eastern region.

Polyethylene Terephthalate (PET) Segment in GCC Rigid Plastic Packaging Market

The PET segment is experiencing the most dynamic growth in the GCC rigid plastic packaging market, with an expected growth rate of approximately 6% during 2024-2029. This remarkable growth is primarily driven by increasing adoption in beverage packaging, particularly for water bottles and other drinks, due to its excellent clarity and natural CO2 barrier properties. The segment's growth is further accelerated by various sustainability initiatives across the GCC region, with companies increasingly focusing on recycled PET (rPET) solutions. For instance, the UAE's recent initiatives to establish PET recycling facilities and the growing trend of major beverage companies transitioning to recycled PET packaging demonstrate the segment's strong growth trajectory. The material's recyclability and lower environmental impact compared to alternative packaging materials continue to drive its adoption across various end-user industries.

Remaining Segments in GCC Rigid Plastic Packaging Market by Material

The other significant segments in the GCC rigid plastic packaging market include Polypropylene (PP), Polystyrene (PS) and Expanded Polystyrene (EPS), and other rigid plastic materials. PP maintains a strong presence due to its superior rigidity and resistance to heat, water, and chemicals, making it particularly suitable for food packaging and medical applications. The PS and EPS segment serves specific niches in food service packaging and protective packaging applications, while other materials like PVC and polycarbonate cater to specialized packaging needs across various industries. These segments collectively contribute to the market's diversity and provide solutions for specific packaging requirements across different end-user industries in the GCC region.

Segment Analysis: By Product

Bottles and Jars Segment in GCC Rigid Plastic Packaging Market

The plastic bottle and plastic jar segment dominates the GCC rigid plastic packaging market, commanding approximately 43% market share in 2024. This segment's prominence is driven by increasing consumption across food and beverage, cosmetics and personal care, and healthcare industries. The United Arab Emirates and Saudi Arabia are witnessing considerable growth in the food and beverage industry, particularly due to their status as major international travel and commercial destinations. The segment's growth is further supported by the development of recyclable PET plastic bottles, with many companies offering sustainable packaging solutions. For instance, Al Ain Water has launched new water bottles made of recycled polyethylene terephthalate (rPET) in the UAE market. The segment is also gaining significant traction from pharmaceuticals and personal care industries, with the longstanding presence of global companies like Unilever, Procter and Gamble, and L'Oréal fueling consumer interest in international beauty and personal care brands that utilize plastic jar packaging.

Remaining Segments in GCC Rigid Plastic Packaging Market by Product

The plastic tray and plastic container segment serves as a crucial component of the disposables market, primarily catering to the food and beverage and hospitality industries. These products offer cost-effective solutions while maintaining quality standards for food service applications. The caps and closures segment plays a vital role in providing secure sealing solutions across various industries, particularly in beverage packaging and pharmaceutical applications. The other products segment, which includes cups, tubs, crates, and pots, addresses diverse packaging needs across multiple industries. This segment particularly serves the dairy industry, juice sector, and various industrial applications, offering specialized solutions for specific packaging requirements. The market for these segments is evolving with an increasing focus on sustainable materials and innovative designs to meet changing consumer preferences and regulatory requirements.

Segment Analysis: By End-User Industry

Food Segment in GCC Rigid Plastic Packaging Market

The food segment dominates the GCC rigid plastic packaging market, commanding approximately 36% market share in 2024, driven by the increasing demand for packaged and processed foods across the region. This significant market position is supported by rapid urbanization, changing dietary habits, and the expanding food manufacturing sector in key GCC countries. The segment's growth is further bolstered by the rising number of supermarkets and hypermarkets, increasing consumer preference for convenience foods, and the need for extended shelf life of food products. Additionally, the food sector benefits from substantial investments in food processing facilities and the expansion of international food brands in the region, particularly in Saudi Arabia and UAE, which has created robust demand for various rigid plastic packaging solutions including plastic containers, plastic trays, and plastic bottles.

Pharmaceutical and Healthcare Segment in GCC Rigid Plastic Packaging Market

The pharmaceutical and healthcare segment is emerging as the fastest-growing sector in the GCC rigid plastic packaging market, with a projected growth rate of approximately 7% during 2024-2029. This remarkable growth is primarily attributed to increasing healthcare investments across GCC countries, particularly in Saudi Arabia and the UAE, along with the expansion of domestic pharmaceutical manufacturing capabilities. The segment's growth is further accelerated by stringent regulations requiring high-quality packaging solutions for medical products, rising demand for tamper-evident packaging, and the growing need for specialized pharmaceutical containers. The expansion of healthcare facilities, increasing focus on domestic drug production, and rising health awareness among consumers are also contributing to the segment's rapid growth, creating substantial opportunities for rigid plastic packaging manufacturers specializing in medical-grade materials and sterile packaging solutions.

Remaining Segments in End-User Industry

The beverage, cosmetics and personal care, household care, and other industrial segments collectively form a significant portion of the GCC rigid plastic packaging market, each serving distinct market needs. The beverage segment maintains strong demand through bottled water, dairy products, and soft drinks packaging requirements. The cosmetics and personal care segment is driven by the region's high per capita spending on beauty products, particularly in Saudi Arabia and UAE. The household care segment, while smaller, continues to provide steady demand for rigid plastic packaging solutions. Other industrial applications, including chemical packaging and automotive fluids, contribute to market diversity through specialized packaging requirements and innovative solutions.

GCC Rigid Plastic Packaging Market Geography Segment Analysis

GCC Rigid Plastic Packaging Market in Saudi Arabia

Saudi Arabia dominates the GCC rigid plastic packaging landscape, commanding approximately 63% of the total market share in 2024. The country's market leadership is driven by its extensive consumer base and diverse industrial activities beyond the oil and gas sector. The nation's food and beverage sector has emerged as one of the largest adopters of plastic packaging products, particularly for plastic containers and plastic bottles. The country's strategic position is further strengthened by its rich raw material resources, particularly in polyolefins production, making it one of the largest producers in the Middle Eastern region. Saudi Arabia's commitment to Vision 2030 and the National Industrial Development and Logistics Program (NIDLP) has been instrumental in driving regional industrial production, creating substantial demand for packaging products. The country's high consumption of plastic packaging products has led to the establishment of new production plants and lines, boosting production capacity. Additionally, the nation's focus on developing manufacturing facilities for plastic and polymer-based packaging products, coupled with its strategic priority to increase export quantities, is fueling the packaging market growth in the region.

GCC Rigid Plastic Packaging Market in United Arab Emirates

The United Arab Emirates is positioned as the most dynamic market in the GCC region, with a projected growth rate of approximately 5% from 2024 to 2029. The country's rigid plastic packaging sector is experiencing significant transformation driven by sustainability initiatives and technological advancements. The UAE has been particularly proactive in implementing recycling initiatives, with notable developments such as the establishment of food-grade recycling facilities and the introduction of recycled PET (rPET) plastic bottles. The nation's pharmaceutical sector has witnessed remarkable growth, creating substantial opportunities for rigid plastic packaging vendors, particularly in high-density polyethylene (HDPE) applications. The expansion of the food and beverage industry, coupled with the growing tourism sector, has significantly increased the demand for plastic packaging products such as food containers, bottles, and plastic jars. The UAE's commitment to reducing plastic waste and emphasis on recycling has led to innovative solutions in the packaging industry, with many companies focusing on sustainable and recyclable packaging options.

GCC Rigid Plastic Packaging Market in Rest of GCC

The Rest of GCC region, encompassing Bahrain, Kuwait, and Oman, represents a significant market for plastic packaging solutions. These countries are witnessing a transformation in consumption patterns, driven by urbanization and demographic changes. The region has attracted several acquisitions and partnerships, with emerging regional players aiming to capture market share. Oman's economic growth prospects and advancements in packaging materials have contributed significantly to the market's development. The region has seen notable progress in sustainable packaging initiatives, with companies introducing innovative solutions for various end-user industries. The presence of multiple manufacturing facilities and the growing focus on customized packaging solutions have strengthened the market position of these countries. Additionally, the increasing penetration of organized retail outlets and changing dietary habits have created new opportunities for rigid plastic packaging applications.

GCC Rigid Plastic Packaging Market in Qatar

Qatar's rigid plastic packaging market has been shaped by its high GDP per capita and strategic vision for economic diversification. The country has made significant strides in implementing recyclability initiatives, particularly in the beverage packaging sector. Qatar's hosting of major international events has accelerated the adoption of sustainable packaging solutions, leading to partnerships between global and local players. The nation's agricultural sector expansion has created new demands for vegetable crates and packaging solutions. Qatar's commitment to food security has driven investments in local food production, consequently increasing the demand for plastic packaging. The country's focus on developing petrochemical capabilities has strengthened the supply side of the packaging industry. Furthermore, Qatar's emphasis on sustainable development has encouraged packaging manufacturers to adopt eco-friendly practices and innovative solutions.

GCC Rigid Plastic Packaging Market in Other Countries

The rigid plastic packaging market in other GCC countries demonstrates varying levels of development and potential. These markets are characterized by their unique regulatory environments and industrial development stages. The focus on sustainability and circular economy initiatives is becoming increasingly prominent across these regions. Local manufacturers are expanding their capabilities to meet the growing demand for specialized packaging solutions. The markets are witnessing increased collaboration between international and local players to enhance technological capabilities and market reach. The development of new industrial zones and economic diversification efforts are creating opportunities for plastic packaging applications. These regions are also seeing growing demand from various end-user industries, particularly in the food and beverage sector, driving innovation in packaging solutions.

Get Analysis on Important Geographic Markets

Download PDF

GCC Rigid Plastic Packaging Industry Overview

Top Companies in GCC Rigid Plastic Packaging Market

The GCC rigid plastic packaging market features established players like Zamil Plastic Industries, Takween Advanced Industries, Packaging Products Company (PPC), and Saudi Arabian Packaging Industry (SAPIN) leading the competitive landscape. Companies are focusing on product innovation through advanced technologies like injection-molded packaging, in-mold labeling, and thermoformed plastic packaging to develop specialized packaging solutions across food & beverage, pharmaceutical, and personal care segments. Operational agility is being enhanced through investments in automated manufacturing processes and quality control systems. Strategic partnerships with global technology providers and raw material suppliers are helping companies strengthen their market position. Geographic expansion within GCC countries and the development of new manufacturing facilities demonstrate the industry's growth focus, while sustainability initiatives and recycling capabilities are becoming key differentiators.

Local Players Dominate Fragmented Regional Market

The GCC plastic packaging market exhibits a fragmented structure with a mix of large regional conglomerates and specialized packaging manufacturers. Local players hold significant market share due to their established distribution networks, understanding of regional requirements, and proximity to raw material sources in the petrochemical-rich region. While global packaging giants maintain a limited direct presence, they operate through technology licensing agreements and joint ventures with regional players, contributing to knowledge transfer and industry advancement.

Market consolidation remains relatively low, with most major players focusing on organic growth rather than acquisitions. However, there is an emerging trend of strategic partnerships and collaborations, particularly in areas of sustainable packaging development and advanced manufacturing technologies. The presence of multiple family-owned businesses and government-linked companies adds a unique dynamic to the competitive landscape, influencing investment decisions and market strategies.

Innovation and Sustainability Drive Future Success

Success in the GCC rigid plastic packaging market increasingly depends on companies' ability to balance innovation with sustainability requirements. Market leaders are investing in research and development to create lighter, more recyclable packaging solutions while maintaining product functionality. The concentration of end-users in food and beverage, personal care, and pharmaceutical sectors necessitates close collaboration with customers to develop tailored solutions. Companies that can demonstrate environmental responsibility while meeting stringent quality standards will likely gain a competitive advantage.

For new entrants and smaller players, specialization in niche segments and focus on specific end-user industries offers a path to market growth. The risk of substitution from alternative packaging materials is being addressed through continuous product innovation and cost optimization. Regulatory changes regarding plastic usage and recycling are reshaping competitive dynamics, making investment in sustainable technologies and circular economy solutions crucial for long-term success. Companies that can adapt to evolving environmental regulations while maintaining cost competitiveness will be better positioned to capture market opportunities.

GCC Rigid Plastic Packaging Market Leaders

-

Zamil Plastic Industries Co.

-

Takween Advanced Industries (Plastico SPS)

-

Packaging Products Company (PPC)

-

Al Rashid Boxes and Plastic Co., Ltd.

-

Saudi Arabian Packaging Industry WLL (SAPIN)

- *Disclaimer: Major Players sorted in no particular order

.webp)

Need More Details on Market Players and Competiters?

Download PDF

GCC Rigid Plastic Packaging Market News

- April 2024: SABIC, a prominent player in the global chemical industry and a member of GPCA, announced Saudi Arabia's inaugural circular packaging initiative. This initiative is a pivotal part of SABIC's TRUCIRCLE program, designed to propel the adoption of a circular plastic economy.

- November 2023: PepsiCo started using 100% recycled plastic bottles for its Pepsi, Diet Pepsi, and Pepsi Zero brands in the United Arab Emirates. This move marked a significant milestone, making PepsiCo the first in the country to introduce locally produced, fully recycled packaging in the carbonated soft drinks (CSDs) segment.

GCC Rigid Plastic Packaging Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

-

4.4 Trade Scenario

- 4.4.1 Trade Analysis (Top Five Import-export Countries)

- 4.5 Industry Regulation, Policy and Standards

- 4.6 Technology Landscape

-

4.7 Pricing Trend Analysis

- 4.7.1 Plastic Resins (Current Pricing and Historic Trends)

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Demand for Recyclable Rigid Plastic Packaging is Expected to Increase with New Regulations

- 5.1.2 Increasing Demand for Rigid Plastic Packaging to Increase Shelf Life of the Products

-

5.2 Market Restraints

- 5.2.1 Environmental Concerns Over Safe Disposal and Price Volatility of the Raw Materials

6. MARKET SEGMENTATION

-

6.1 By Resin Type

- 6.1.1 Polyethylene (PE)

- 6.1.1.1 Low-density Polyethylene (LDPE) and Linear Low-density Polyethylene (LLDPE)

- 6.1.1.2 High Density Polyethylene (HDPE)

- 6.1.2 Polyethylene terephthalate (PET)

- 6.1.3 Polypropylene (PP)

- 6.1.4 Polystyrene (PS) and Expanded polystyrene (EPS)

- 6.1.5 Polyvinyl chloride (PVC)

- 6.1.6 Other Resin Types

-

6.2 By Product Type

- 6.2.1 Bottles and Jars

- 6.2.2 Trays and Containers

- 6.2.3 Caps and Closures

- 6.2.4 Intermediate Bulk Containers (IBCs)

- 6.2.5 Drums

- 6.2.6 Pallets

- 6.2.7 Other Product Types

-

6.3 By End-user Industry

- 6.3.1 Food**

- 6.3.1.1 Candy and Confectionery

- 6.3.1.2 Frozen Foods

- 6.3.1.3 Fresh Produce

- 6.3.1.4 Dairy Products

- 6.3.1.5 Dry Foods

- 6.3.1.6 Meat, Poultry, And Seafood

- 6.3.1.7 Pet Food

- 6.3.1.8 Other Food Products

- 6.3.2 Foodservice**

- 6.3.2.1 Quick Service Restaurants (QSRs)

- 6.3.2.2 Full-Service Restaurants (FSRs)

- 6.3.2.3 Coffee and Snack Outlets

- 6.3.2.4 Retail Establishments

- 6.3.2.5 Institutional

- 6.3.2.6 Hospitality

- 6.3.2.7 Others Food Service Sectors

- 6.3.3 Beverage

- 6.3.4 Healthcare

- 6.3.5 Cosmetics and Personal Care

- 6.3.6 Industrial

- 6.3.7 Building and Construction

- 6.3.8 Automotive

- 6.3.9 Other End-user Industries

-

6.4 By Country***

- 6.4.1 Middle East and Africa

- 6.4.1.1 United Arab Emirates

- 6.4.1.2 Saudi Arabia

- 6.4.1.3 Qatar

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 Zamil Plastic Industries Co.

- 7.1.2 Takween Advanced Industries (Plastico SPS)

- 7.1.3 Packaging Products Company (PPC)

- 7.1.4 Al Rashid Boxes and Plastic Co. Ltd

- 7.1.5 Saudi Arabian Packaging Industry WLL (SAPIN)

- 7.1.6 AL-Ghandoura Plastic Co. (GhanPlast)

- 7.1.7 Al Bayader International

- 7.1.8 KANR For Plastic Industries

- 7.1.9 Saudi Plastic Factory Company

- 7.1.10 Precision Plastic Products Co. (LLC)

- 7.1.11 Al Jabri Plastics

- 7.1.12 Premier Plastic Company (PPC).

- 7.2 Heat Map Analysis

- 7.3 Competitor Analysis - Emerging vs. Established Players

8. RECYCLING & SUSTAINABILITY LANDSCAPE

9. FUTURE OUTLOOK

**Subject to Availability

***In the Report, Rest of GCC will be considered as a separate GCC.

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

GCC Rigid Plastic Packaging Industry Segmentation

The GCC rigid plastic packaging market tracks the demand for rigid plastic packaging products catering to the food, beverage, healthcare, personal care, cosmetic, and other industries. Plastics can be of different grades and different material combinations based on the type of product being packed, such as polyethylene, polypropylene, and polyvinyl chloride.

The GCC rigid plastic packaging market report is segmented by resin type (polyethylene [PE] (low-density polyethylene [LDPE] and linear low-density polyethylene [LLDPE], high-density polyethylene [HDPE], polyethylene terephthalate [PET], polypropylene [PP], polystyrene [PS] and expanded polystyrene [EPS], polyvinyl chloride [PVC], and other resin types), product type (bottles and jars, trays and containers, caps and closures, intermediate bulk containers [IBCs], drums, pallets, and other product types), end-user industry (food [candy and confectionery, frozen foods, fresh produce, dairy products, dry foods, meat, poultry, and seafood, pet food, and other food products], food service [quick service restaurants {QSRs}, full-service restaurants {FSRs}, coffee and snack outlets, retail establishments, institutional, hospitality, and other food service sectors], beverage, healthcare, cosmetics and personal care, industrial, building and construction, automotive, and other end-user industries), and country (United Arab Emirates, Saudi Arabia, Qatar, and Rest of GCC). The report offers market sizes and forecasts in volume (tonnes) for all the above segments.

| By Resin Type | Polyethylene (PE) | Low-density Polyethylene (LDPE) and Linear Low-density Polyethylene (LLDPE) | |

| High Density Polyethylene (HDPE) | |||

| Polyethylene terephthalate (PET) | |||

| Polypropylene (PP) | |||

| Polystyrene (PS) and Expanded polystyrene (EPS) | |||

| Polyvinyl chloride (PVC) | |||

| Other Resin Types | |||

| By Product Type | Bottles and Jars | ||

| Trays and Containers | |||

| Caps and Closures | |||

| Intermediate Bulk Containers (IBCs) | |||

| Drums | |||

| Pallets | |||

| Other Product Types | |||

| By End-user Industry | Food** | Candy and Confectionery | |

| Frozen Foods | |||

| Fresh Produce | |||

| Dairy Products | |||

| Dry Foods | |||

| Meat, Poultry, And Seafood | |||

| Pet Food | |||

| Other Food Products | |||

| Foodservice** | Quick Service Restaurants (QSRs) | ||

| Full-Service Restaurants (FSRs) | |||

| Coffee and Snack Outlets | |||

| Retail Establishments | |||

| Institutional | |||

| Hospitality | |||

| Others Food Service Sectors | |||

| Beverage | |||

| Healthcare | |||

| Cosmetics and Personal Care | |||

| Industrial | |||

| Building and Construction | |||

| Automotive | |||

| Other End-user Industries | |||

| By Country*** | Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | |||

| Qatar | |||

Need A Different Region or Segment?

Customize Now

GCC Rigid Plastic Packaging Market Research FAQs

How big is the GCC Rigid Plastic Packaging Market?

The GCC Rigid Plastic Packaging Market size is expected to reach 2.38 million tonnes in 2025 and grow at a CAGR of 4.01% to reach 2.90 million tonnes by 2030.

What is the current GCC Rigid Plastic Packaging Market size?

In 2025, the GCC Rigid Plastic Packaging Market size is expected to reach 2.38 million tonnes.

Who are the key players in GCC Rigid Plastic Packaging Market?

Zamil Plastic Industries Co., Takween Advanced Industries (Plastico SPS), Packaging Products Company (PPC), Al Rashid Boxes and Plastic Co., Ltd. and Saudi Arabian Packaging Industry WLL (SAPIN) are the major companies operating in the GCC Rigid Plastic Packaging Market.

What years does this GCC Rigid Plastic Packaging Market cover, and what was the market size in 2024?

In 2024, the GCC Rigid Plastic Packaging Market size was estimated at 2.28 million tonnes. The report covers the GCC Rigid Plastic Packaging Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the GCC Rigid Plastic Packaging Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

GCC Rigid Plastic Packaging Market Research

Mordor Intelligence provides a comprehensive analysis of the rigid plastic packaging industry, utilizing decades of expertise in industrial plastic packaging research. Our extensive report covers the full range of plastic packaging solutions. This includes plastic containers, plastic bottles, plastic trays, plastic jars, and plastic clamshells. The analysis addresses both PET packaging and HDPE packaging segments, offering detailed insights into material preferences and applications throughout the GCC region.

Stakeholders gain valuable insights from our detailed examination of pharmaceutical plastic packaging trends and manufacturing processes. This includes technologies such as injection molded packaging, thermoformed plastic packaging, and blow molded packaging. The comprehensive report, available as an easy-to-download PDF, delivers in-depth analysis of rigid packaging developments and rigid plastic container innovations. Our research is particularly beneficial for manufacturers, suppliers, and end-users in the hard plastic packaging sector. It offers actionable intelligence for strategic decision-making across the value chain.