Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

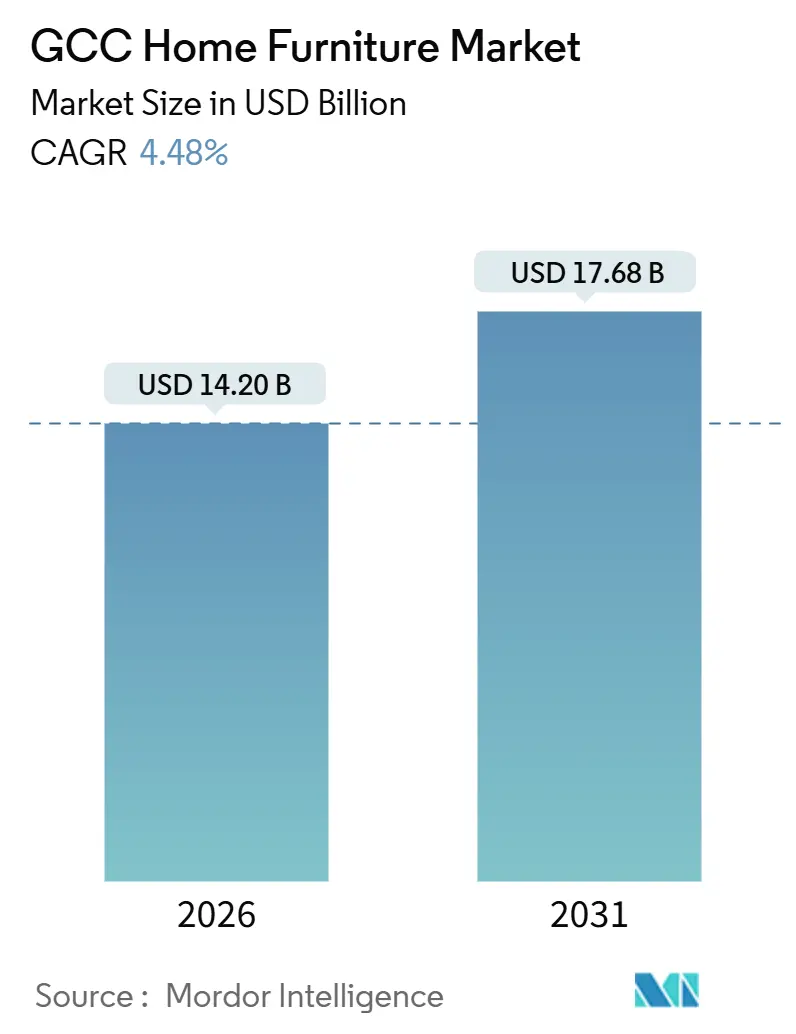

| Market Size (2026) | USD 14.20 Billion |

| Market Size (2031) | USD 17.68 Billion |

| Growth Rate (2026 - 2031) | 4.48% CAGR |

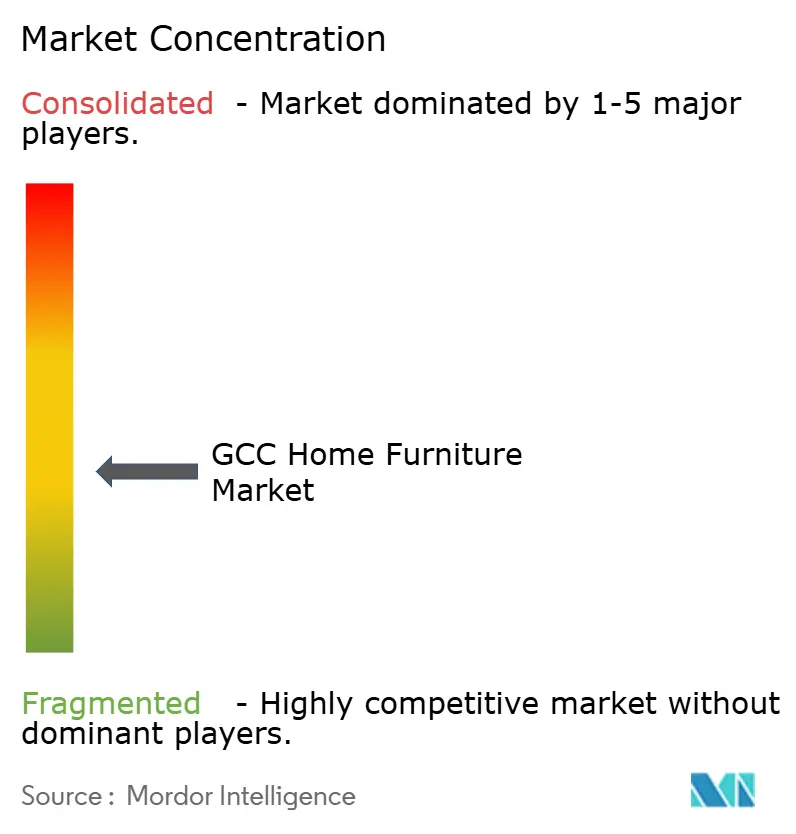

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Home Furniture Market Analysis by Mordor Intelligence

The GCC home furniture market size is USD 14.20 billion in 2026 and is projected to reach USD 17.68 billion by 2031, expanding at a 4.48% CAGR over 2025–2030. The expansion aligns with sustained residential delivery pipelines in the UAE and Saudi Arabia, ongoing non-oil sector investment programs, and visible channel shifts that favor omnichannel retail models integrating digital invoicing and last-mile fulfillment. The GCC home furniture market is also influenced by price dynamics, as the UAE recorded a 1.8% year-on-year decline in furniture and household goods prices in the first quarter of 2025, signaling promotional intensity and margin compression in parts of the retail base. Digitalization is set to deepen, since the UAE will mandate e-invoicing for B2B and B2G transactions from July 2026, which will enable real-time, cross-border visibility of orders and inventories for furniture sellers and their logistics partners. Product mix continues to tilt toward functional categories like home office and outdoor living, while material innovation in polymers and composite wood systems supported by regional chemical suppliers is reshaping durability and maintenance profiles for humid coastal conditions.

Key Report Takeaways

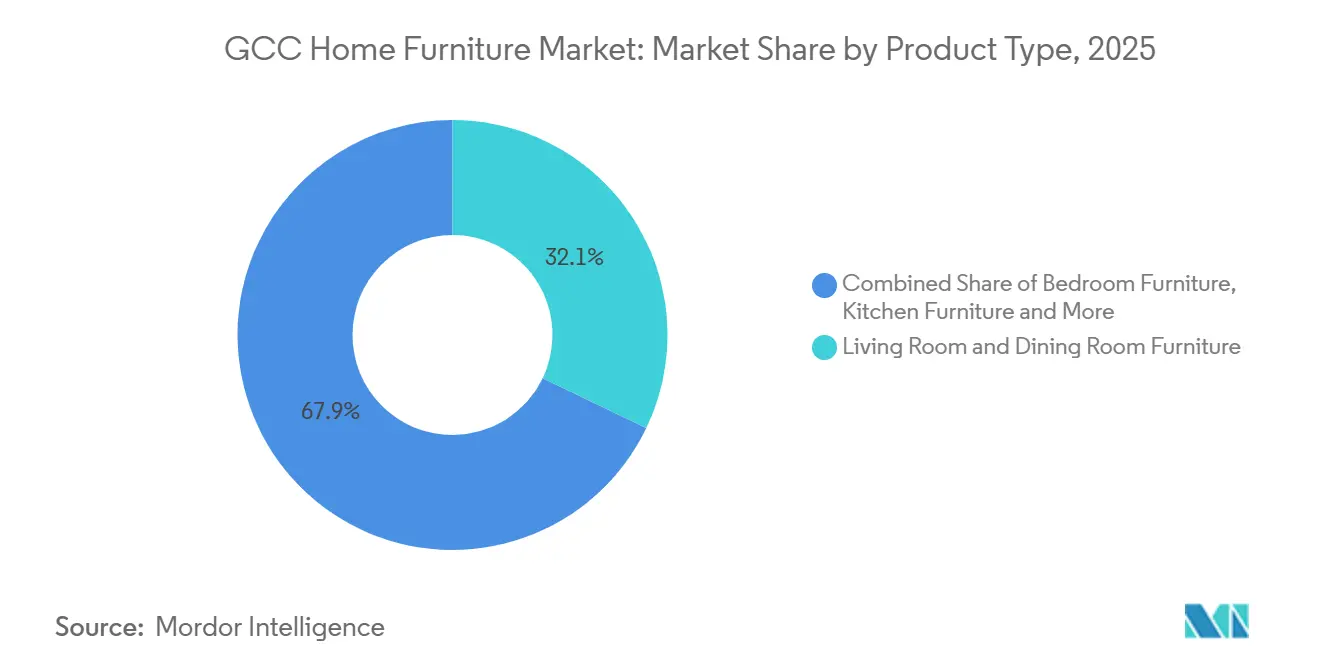

- By product type, living room and dining room furniture led with 32.12% of the GCC home furniture market share in 2025. GCC home furniture market size for home office furniture is projected to expand at a 5.97% CAGR through 2031.

- By material, wood held 57.23% of the GCC home furniture market share in 2025. GCC home furniture market size for plastic and polymer is forecast to grow at a 5.56% CAGR through 2031.

- By price range, the economy segment accounted for 47.13% of the GCC home furniture market share in 2025. GCC home furniture market size for the premium segment is set to expand at a 5.87% CAGR through 2031.

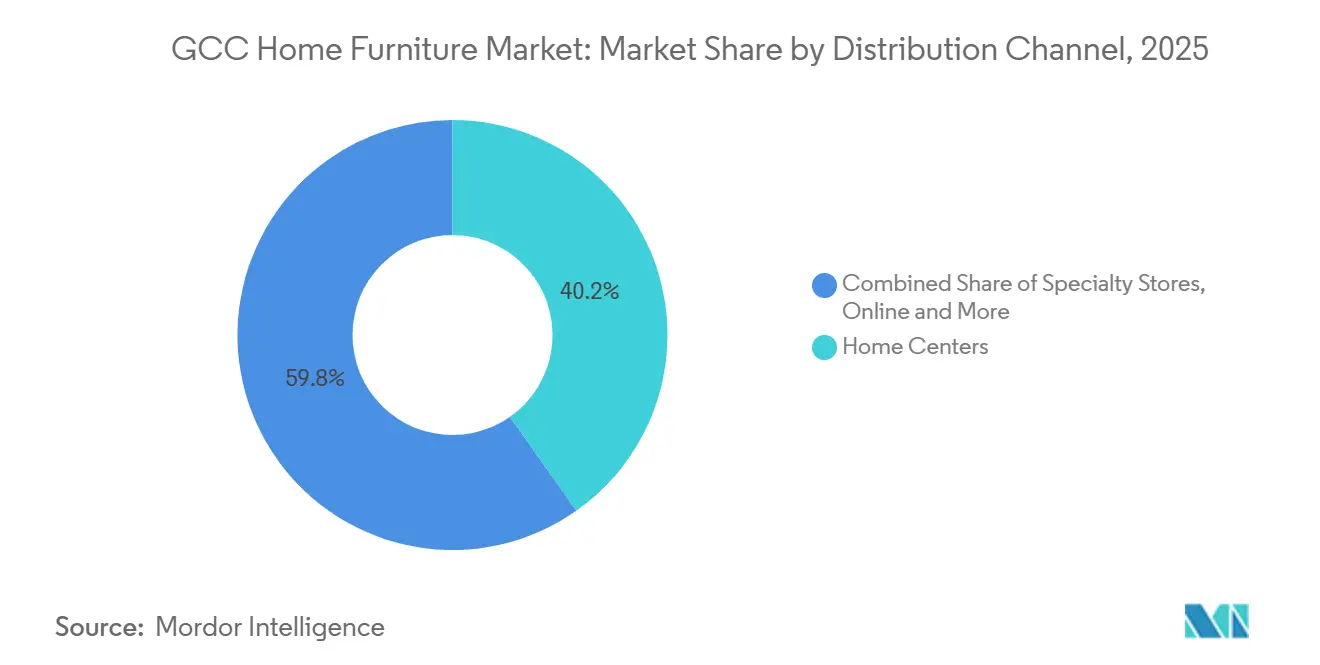

- By distribution channel, home centers captured 40.23% of the GCC home furniture market share in 2025. GCC home furniture market size for online channels is projected to grow at a 6.75% CAGR through 2031.

- By geography, the United Arab Emirates accounted for 48.23% of the GCC home furniture market share in 2025. GCC home furniture market size for Saudi Arabia is projected to advance at a 5.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

GCC Home Furniture Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust residential & hospitality construction pipeline | +1.8% | UAE core, Saudi Arabia, spill-over to Qatar, Oman, Kuwait, Bahrain | Medium term (2-4 years) |

| Rising disposable incomes & youthful demographics | +0.9% | GCC-wide, strongest in Saudi Arabia and UAE | Long term (≥ 4 years) |

| Acceleration of e-commerce & omnichannel retail | +1.1% | Saudi Arabia and UAE lead, others catching up | Short term (≤ 2 years) |

| Smart-city programmes driving smart-furniture adoption | +0.6% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Golden-Visa inflows boosting expatriate furnishing demand | +0.5% | UAE dominant, Saudi Arabia emerging RHQ incentives | Medium term (2-4 years) |

| SEZ-linked incentives for local furniture manufacturing | +0.4% | Saudi Arabia, UAE free zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acceleration Of E-commerce & Omnichannel Retail

E-invoicing in the UAE will become mandatory for B2B and B2G transactions from July 2026, which is expected to streamline order-to-cash processes for furniture retailers and enable tighter integration of online storefronts with warehouse and store inventories. GCC home furniture market operators are blending physical and digital journeys, as evidenced by IKEA’s deployment of small-format locations in Abu Dhabi and Fujairah that feed omnichannel fulfillment and click-and-collect behaviors. Retailers are adopting augmented reality to allow consumers to place sofas, dining sets, and storage units into room-scale visualizations on mobile devices, a step that helps reduce returns and improves consumer confidence for higher-ticket items[1]https://stylishadvanceddecor.ae/what-are-the-latest-innovations-in-furniture-manufacturing-technology-and-automation/. The upcoming Bharat Mart trade platform in Dubai’s Jebel Ali Free Zone will expand the assortment available to GCC shoppers by improving access for Indian MSMEs, including furniture exporters that target value and mid-range price points. As online penetration increases, the last mile for bulky deliveries remains cost-intensive relative to small parcels, which encourages retailers to optimize route planning and to use mixed models that combine showrooms for tactile assessment with digital ordering for fulfillment. The GCC home furniture market is positioned to capture sustained digital demand growth as payment rails and invoicing standards mature across the region and as retailers standardize delivery and installation services to raise customer satisfaction.

Smart-city Programmes Driving Smart-furniture Adoption

Telecom and platform investments are creating the digital backbone for connected environments in Saudi Arabia and the UAE, which in turn supports smart-ready furniture that integrates with building management and residential IoT ecosystems. Saudi Telecom Company (stc) Group’s IoT subsidiary reported revenue of USD 80.20 million (SAR 301 million) in 2024 and expanded its partner network to more than 120 entities, reflecting the rapid scale-up of deployments that include smart heritage and urban redevelopment programs[2]https://mordorintelligence1-my.sharepoint.com/personal/sarika_singh_mordorintelligence_com/Documents/Work 2025/RD's/GCC Home Furniture Market/STC.COM. Operators have rolled out hundreds of thousands of smart meters, safety devices, and connected vehicles, illustrating how city systems now generate real-time data streams that furniture in commercial and premium residential settings can tap for occupancy sensing and convenience features. The near-term addressable base is concentrated in high-spec buildings, hospitality, and public-sector projects where procurement standards include energy management and connected services rather than in mass retail segments. Because interoperability and data privacy frameworks are still evolving, early adoption focuses on showcase developments that can mandate standards across vendors, while mainstream uptake will follow once device communication protocols are codified. The GCC home furniture market should expect steady pilot activity and gradual premium-segment penetration first, followed by selective mass-market diffusion as cost points decline and integration kits become simpler to deploy.

Golden-Visa Inflows Boosting Expatriate Furnishing Demand

The UAE’s Golden Visa policy grants long-duration residency to qualifying property investors and has become a visible catalyst for large-ticket home furnishing purchases as households upgrade to villas and plan multi-room interior fit-outs. In the first quarter of 2025, villa transactions grew faster than apartment transactions, a pattern that typically lifts furniture spend per household because villas require more rooms to furnish and often include outdoor areas. Saudi Arabia’s regional headquarters policy brought a supportive corporate demand layer as senior expatriates relocate with families, adding premium and bespoke furniture demand tied to corporate housing and long-term leases. The purchase cycle for expatriate property buyers usually involves a period of renting while selecting and acquiring a home, and then a lag between contract signing and handover for off-plan purchases, which delays furniture demand realization. As these programs scale, retailers that segment their assortments for larger floor plans, customizable finishes, and outdoor furniture will be best positioned to capture a growing share of higher-value baskets. The GCC home furniture market will continue to benefit from policy frameworks that deepen resident tenure, which stabilizes furnishing cycles and lifts the average ticket among long-stay expatriate households.

SEZ-linked Incentives For Local Furniture Manufacturing

Saudi Arabia’s investment and industrial policies are reducing barriers to local manufacturing and assembly, supported by updated investment law frameworks and incentive programs designed to attract capital and advanced production capabilities. The Standard Incentives Program allocated USD 2.66 billion (SAR 10 billion) in January 2025 to bolster local manufacturing and target sectors that include furniture, which encourages import substitution and value addition inside the Kingdom[3]https://investmentpolicy.unctad.org/investment-policy-monitor/190/saudi-arabia. Supply chains are adapting as Chinese exporters increase shipments of semi-processed wood panels to the Gulf, enabling regional factories to cut, edge-band, and assemble products while capturing available incentives tied to local value creation. Projects located in free zones and special economic areas may benefit from customs and tax advantages, although goods sold into the mainland market are subject to VAT and other domestic rules that manufacturers must incorporate into pricing. Over time, a hybrid model is likely to deepen, with semi-finished inputs flowing into GCC assembly lines that tailor designs to local tastes and climatic conditions while shortening lead times. The GCC home furniture market should see more domestically produced SKUs in flat-pack and modular categories as factories standardize processes and scale supplier qualification programs around regional hubs.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile imported raw-material prices (wood, metal) | -0.7% | GCC-wide, acute in UAE and Saudi Arabia | Short term (≤ 2 years) |

| Import-dependency exposed to global supply-chain shocks | -0.5% | All GCC markets | Medium term (2-4 years) |

| VAT & new corporate-tax regimes squeezing retailer margins | -0.4% | UAE, Saudi Arabia, Bahrain, Oman | Short term (≤ 2 years) |

| Shortage of skilled craftsmen for high-end customization | -0.2% | UAE and Saudi Arabia premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Imported Raw-material Prices

Saudi Arabia’s building-material cost indices rose during 2024, which raised transport and processing costs for furniture manufacturers that depend on diesel-fueled logistics and machinery, adding pressure on margins at a time of intense retail competition[4]https://publications.aecom.com/MEH/update/mena-economic-review-2025. In the UAE, copper and aluminum posted year-on-year increases by January 2025, which directly affects hardware, frames, and fittings used across furniture categories. Despite higher input costs, UAE consumer prices for furniture and household goods fell 1.8% year-on-year in the first quarter of 2025, signaling discount-led volume strategies and a willingness by retailers to absorb cost shocks to sustain throughput. Scale players provided further price relief, since IKEA’s fiscal-year 2024 actions lowered wholesale prices to protect affordability and stimulate demand in price-sensitive segments. Timber import patterns into Saudi Arabia underscore working-capital stress and inventory rebalancing across distributors, which influences availability and lead times for wood-based SKUs across the Kingdom. The GCC home furniture market must keep hedging and sourcing diversification central to procurement to protect price points and maintain unit economics when commodity cycles tighten.

Import-dependency Exposed To Global Supply-chain Shocks

Chinese plywood shipments into the UAE and Saudi Arabia increased during 2024, and particleboard imports also grew, reinforcing the region’s reliance on a single dominant supply origin for key semi-processed inputs. Any production or port disruption in major supplier countries would cascade into GCC inventories, given the time required to qualify alternative vendors and rework logistics contracts. GCC tariff regimes are generally low, but selected categories and national policies impose higher rates on goods that compete with domestic industries, and those variations can complicate rapid re-sourcing strategies in response to shocks. For goods routed from free zones to domestic markets such as the UAE mainland, VAT and related documentation requirements add administrative steps that must be built into fulfillment timelines. Over-dependence on a narrow set of upstream suppliers elevates inventory risk and forces conservative stocking, which raises working capital and can reduce assortment breadth in peak seasons. The GCC home furniture market’s resilience will depend on supplier diversification, buffer stock strategies for critical inputs, and closer collaboration with logistics partners on routing and transit-time risk.

Segment Analysis

By Product Type: Home Office Furniture Outpaces Traditional Living Room Demand

Living room and dining room furniture held 32.12% in 2025, confirming the category as the largest by share in the GCC home furniture market. GCC home furniture market operators see demand anchored by social gathering spaces and frequent refresh cycles in rental-heavy districts that prize presentable common areas. Product renewal in sofas and dining sets is supported by promotional calendars and seasonal retail events, which help sustain unit volumes in the largest category. The home office category is the fastest-growing, and its ascent is tied to hybrid work adoption and the availability of ergonomic and modular designs that fit spare rooms or mezzanine spaces. The GCC home furniture market continues to benefit from new format stores and online browsing tools that reduce friction in selecting desks, adjustable seating, and cable management kits that integrate cleanly into villa-based layouts.

GCC home furniture market size for home office furniture is projected to expand at 5.97% CAGR through 2031, supported by higher-value purchases in villas that require multi-room setups with coordinated finishes. Retailers are standardizing flat-pack solutions with quick assembly that lower last-mile times and improve throughput for logistics partners. Adoption of augmented-reality visualization supports confident purchasing and helps reduce returns, which preserves margins in bulky items. The largest category remains competitive, yet growth pockets exist in modular, storage-rich sets and space-saving designs that address apartment constraints without sacrificing seating capacity. GCC home furniture market participation is likely to widen as more brands align designs with contemporary interiors favored by younger households and long-stay expatriates.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Material: Plastic and Polymer Alternatives Gain Ground Against Wood Dominance

Wood maintained 57.23% of the 2025 material mix, underscoring enduring consumer preferences for natural finishes in bedrooms, dining sets, and majlis seating that communicate quality and warmth in premium interiors. GCC home furniture market sellers also rely on metal for structural strength across storage, office seating, and outdoor frames that balance durability and weight. Polymer alternatives are taking share in coastal cities where humidity challenges natural materials and where renters value maintenance simplicity and lightweight designs. Huntsman’s polyurethane systems footprint in Dammam and Dubai supplies binders and cushioning systems that advance low-VOC and process-efficiency goals for panel production and seating comfort. Composite wood flows from Asia complement these shifts, as suppliers provide semi-processed boards that regional factories can format for local tastes while capturing incentives tied to domestic value creation.

GCC home furniture market size for plastic and polymer is projected to expand at a 5.56% CAGR to 2031, reflecting advances in surface fidelity and resistance to warping or corrosion in high-humidity environments. Demand for Scandinavian-inspired aesthetics encourages lighter-toned woods and engineered surfaces, which is visible in importer and distributor notes on species preferences and inventory cycles in Saudi Arabia. Polymer innovation also reduces weight, which can lower last-mile delivery and handling costs in tall buildings and gated communities. As free zones and SEZs deepen assembly capability, Gulf factories will increase the share of cut-to-size, edge-banded components that capture local value while meeting regional durability requirements. The GCC home furniture market is expected to retain wood leadership while polymer and composite adoption rise in outdoor, kitchen, and youth-bedroom lines.

By Price Range: Premium Segment Growth Outpaces Economy Despite Larger Base

The economy segment accounted for 47.13% in 2025, driven by mid-income households and renters who value affordability, portability, and ready-to-assemble convenience. GCC home furniture market participants in economy lines have leaned on price promotions and bundle offers, which helped maintain volumes even as input prices increased in metals and petrochemical derivatives. UAE furniture and household goods prices fell 1.8% year-on-year in the first quarter of 2025, indicating discount intensity and retailer absorption of cost to defend traffic and share. Large-scale players also lowered wholesale pricing in 2024, reinforcing affordability as a core pillar while optimizing logistics and throughput. The economy base will remain sizable, though richer margins and brand differentiation accumulate in mid-range and premium tiers.

GCC home furniture market size for the premium segment is forecast to grow at a 5.87% CAGR through 2031, helped by villa buyers with Golden Visas in the UAE and corporate relocations in Saudi Arabia linked to regional headquarters incentives. Premium assortments combine catalog customization in fabrics and finishes with elevated service layers across design consultation and installation scheduling. Retailers in this tier are insulated from the deepest discounting seen in economy channels, which stabilizes price realization and supports curated expansions into outdoor and home office suites. Corporate and policy tailwinds that increase household tenure across the Gulf continue to favor higher-ticket conversions and repeat upgrades over multi-year horizons. The GCC home furniture market is therefore split between scale-driven affordability plays and premium formats that leverage design and service differentiation.

By Distribution Channel: Online Growth Accelerates as Home Centers Hold Dominant Share

Home centers held 40.23% of distribution in 2025, reflecting the reach and assortment advantages of region-wide chains with integrated furniture, décor, and soft furnishings. GCC home furniture market leaders have invested in omnichannel tech such as QR-enabled product tags, click-and-collect points, and cross-store inventory visibility to make store networks central to hybrid shopping. The online channel is forecast to grow at a 6.75% CAGR through 2031, fueled by regulatory digitalization and platform investments that raise consumer confidence and reduce back-office friction. In July 2026, e-invoicing will be mandatory for B2B and B2G transactions in the UAE, which will harmonize the order-to-cash cycle and simplify reconciliation for cross-border operations. The combined effect is a model where stores serve as experience and pickup hubs while online platforms extend assortment and scheduling flexibility for large-item delivery.

GCC home furniture market size for online distribution will expand as retailers adopt AR for product visualization and streamline returns to protect margins in bulky categories. Pure-play e-commerce operators are testing hybrid concepts with temporary showrooms in high-traffic locations to provide tactile validation before checkout. The launch of Bharat Mart in Dubai’s JAFZA will offer Indian MSMEs a subsidized regional gateway, which can further widen online and wholesale assortments at entry and mid-range price points. Home centers continue to defend share by pairing store-led inspiration with competitive delivery, assembly, and warranty bundles that reduce the perceived risk of large-ticket purchases. The GCC home furniture market will likely retain its home center core while online steadily accounts for a larger share of total transactions as logistics and digital experiences improve.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The United Arab Emirates accounted for 48.23% of the GCC home furniture market in 2025, supported by strong residential activity and sustained inflows of long-stay expatriates under residency and investor programs. Furniture and household goods prices in the UAE fell 1.8% year-on-year in the first quarter of 2025, indicating discount-led strategies and inventory turns that keep assortments fresh through seasonal cycles. The non-hydrocarbon economy is projected to grow by 4.5% annually in 2025 and 2026, which supports employment and household formation tied to residential leasing and purchases. E-invoicing mandates coming into force in July 2026 will digitize the inter-company flow of furniture orders and returns, enabling faster reconciliation and better forecasting across borders. Trade and customs transparency through the UAE’s International Trade Map also supports granular tracking of HS Chapter 94 flows, which helps furniture importers calibrate sourcing and pricing.

Saudi Arabia is forecast to grow at a 5.74% CAGR from 2026 through 2031, making it the fastest-growing GCC home furniture market over the outlook window. The policy environment continues to catalyze industrial and commercial expansion, with updated investment frameworks and licensing processes that aim to reduce administrative friction for new entrants and manufacturers. Special Economic Zones and related programs encourage local assembly and component production, which can shorten lead times and support product customization for the domestic market. Telecom and digital-infrastructure investment, including IoT platforms and smart deployments, are expanding the potential for connected interiors and high-spec commercial furnishings. The combination of delivery pipelines, investment incentives, and rising digital readiness underpins the growth trajectory in the Kingdom’s furniture demand across residential, hospitality, and corporate settings.

Qatar, Kuwait, Oman, and Bahrain collectively represent the balance of the GCC home furniture market and share common traits that tie demand closely to public-sector cycles and infrastructure spillovers into residential finishing. Retail footprints in these markets are smaller than in the UAE and Saudi Arabia, which encourages many consumers to cross-shop via UAE-based online platforms that offer wider assortments and frequent promotions. When re-sourcing becomes necessary, tariff and import frameworks can differ by product and country, requiring careful planning when switching away from dominant supply origins for wood panels and fittings. Over the medium term, digital invoicing, logistics improvements, and trade facilitation are expected to lift cross-border fulfillment, especially for standardized items that ship efficiently and assemble quickly. The Gulf’s smaller markets will continue to benefit from pan-GCC retail brands and trade platforms that raise assortment depth without necessitating extensive local inventory, which keeps the consumer value proposition competitive.

Competitive Landscape

The GCC home furniture market is moderately fragmented, with leading chains and international brands operating through regional franchisees and home centers, while a long tail of specialty stores and independents serves design-led and bespoke demand. Scale players have pursued omnichannel infrastructure that blends store-based inspiration with digital selection and scheduling, supported by QR-linked catalogs and integrated inventory views. Retailers with the widest footprints have used price investments and curated assortments to defend share, including global groups that cut wholesale prices in 2024 to reinforce affordability. Format innovation has included opening smaller stores in secondary cities to improve accessibility and to function as pickup nodes for online orders, which also reduces last-mile costs. The GCC home furniture market increasingly rewards retailers that can operate integrated stores and digital ecosystems and offer consistent delivery, assembly, and after-sales service.

Digital infrastructure is becoming a competitive differentiator as invoice digitization, electronic payments, and IoT adoption reshape operational baselines for fulfillment and customer experience. E-invoicing mandates in the UAE will standardize documentation flows and encourage process automation, reducing errors and cycle times across wholesale and retail transactions. Group’s IoT programs and partner network expansion point to more connected spaces in commercial and high-end residential settings, which in turn create niches for smart-ready furniture lines. The roll-out of smart devices and meters by entities supports energy and safety use cases that designers can integrate into interiors for high-spec projects. Trade facilitation initiatives such as Bharat Mart will add competitive pressure in entry and mid-range categories by widening supplier access to the Gulf and compressing time-to-shelf for new lines.

Compliance and sustainability are rising on executive agendas as taxation, labor, and supply-chain expectations evolve. The UAE’s corporate tax regime and Saudi tax frameworks require updated governance, which can add operating costs but also encourage formalization and process control across large retail networks. Responsible recruitment and worker welfare initiatives are gaining traction, with programs involving the International Organization for Migration and regional partners designed to improve conditions across the Gulf supply chain. Tariff structures and local-content preferences continue to shape sourcing choices and factory siting, especially on government-linked projects where economic participation commitments apply. Investment frameworks and incentive schemes are expected to support more localized assembly and panel processing near major consumer markets to reduce lead times and enable customization. The GCC home furniture market is moving toward a model that balances affordability, design differentiation, ethical sourcing, and operational discipline under increasingly digital rules of engagement.

GCC Home Furniture Industry Leaders

Al Huzaifa

IKEA

Home Center

Danube Home

Midas Furniture

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: Saudi Arabia’s Ministry of Investment allocated SAR 10 billion (USD 2.66 billion) under the Standard Incentives Program to strengthen local manufacturing, explicitly targeting sectors including furniture.

- November 2024: LTIMindtree established NextEra, a next-generation technology joint venture with Aramco Digital to support the localization of advanced IT services under Vision 2030.

- August 2024: IKEA opened small-format stores in Abu Dhabi and Fujairah, enhancing access and improving click-and-collect network density in the UAE.

- April 2024: IKEA’s sustainability organization partnered with the International Organization for Migration and Gulf Sustain to promote responsible recruitment and worker welfare across GCC supply chains.

GCC Home Furniture Market Report Scope

Across the Gulf Cooperation Council (GCC) countries, the home furniture market encompasses the entire spectrum from manufacturing and import to distribution and retail. Catering to spaces like living rooms, bedrooms, kitchens, and home offices, the market spans both mass-market and premium segments. Demand is buoyed by factors such as population growth, urbanization, real estate development, renovation activities, and rising disposable incomes. Additionally, there's a marked preference for modern, luxury, and customized furnishings.

The GCC Home Furniture Market Report is Segmented by Product Type (Living & Dining Room, Bedroom, Kitchen, Home Office, Bathroom, Outdoor, Other), Material (Wood, Metal, Plastic & Polymer, Others), Price Range (Economy, Mid-Range, Premium), Distribution Channel (Home Centers, Specialty Stores, Online, Others), and Geography (Saudi Arabia, UAE, Qatar, Kuwait, Oman, Bahrain).

By Product

| Living Room & Dining Room Furniture |

| Bedroom Furniture |

| Kitchen Furniture |

| Home Office Furniture |

| Bathroom Furniture |

| Outdoor Furniture |

| Other Furniture |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Others |

By Price Range

| Economy |

| Mid-Range |

| Premium |

By Distribution Channel

| Home Centers |

| Specialty Furniture Stores |

| Online |

| Other Distribution Channels |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Product | Living Room & Dining Room Furniture |

| Bedroom Furniture | |

| Kitchen Furniture | |

| Home Office Furniture | |

| Bathroom Furniture | |

| Outdoor Furniture | |

| Other Furniture | |

| By Material | Wood |

| Metal | |

| Plastic & Polymer | |

| Others | |

| By Price Range | Economy |

| Mid-Range | |

| Premium | |

| By Distribution Channel | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size and growth outlook for the GCC home furniture market?

The GCC home furniture market size is USD 14.20 billion in 2026 and is projected to reach USD 17.68 billion by 2031 at a 4.48% CAGR over 2026–2031.

Which product categories lead demand in the GCC home furniture market?

Living room and dining room furniture is the largest category at 32.12% in 2025, while home office furniture is the fastest-growing with a 5.97% CAGR through 2031.

How is the GCC home furniture market adapting to digital retail?

E-invoicing mandates in the UAE starting July 2026 and omnichannel investments by leading retailers are standardizing digital order-to-cash and enabling store-linked delivery and click-and-collect.

Which materials are gaining share in the GCC home furniture market?

Wood remains dominant at 57.23%, while plastic and polymer alternatives are growing at 5.56% CAGR due to humidity resistance and easy maintenance.