GCC Ceramic Tiles And Sanitary Ware Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

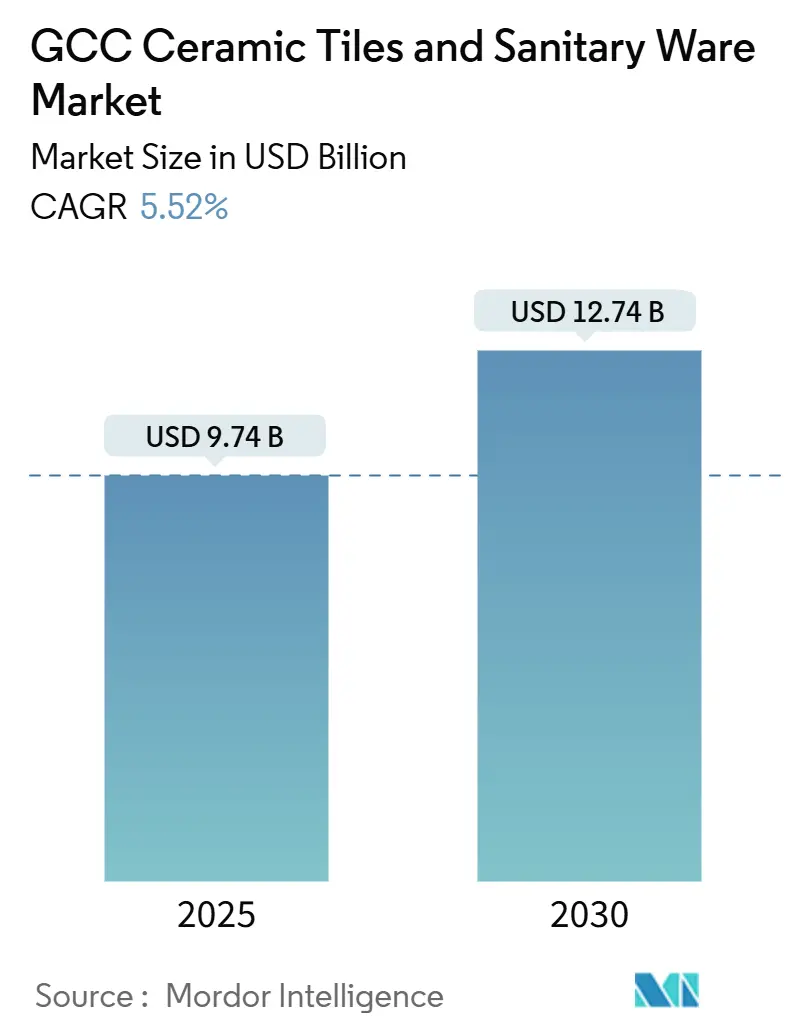

| Market Size (2025) | USD 9.74 Billion |

| Market Size (2030) | USD 12.74 Billion |

| Growth Rate (2025 - 2030) | 5.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

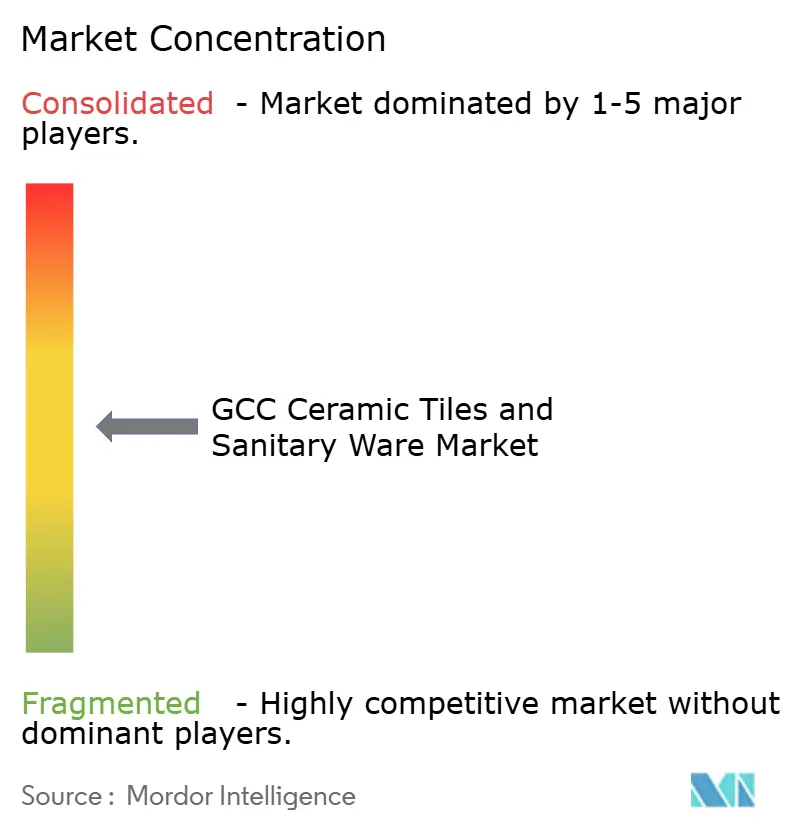

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Ceramic Tiles And Sanitary Ware Market Analysis by Mordor Intelligence

The GCC Ceramic Tiles and Sanitary Ware market size stands at USD 9.74 billion in 2025 and is projected to reach USD 12.74 billion by 2030, expanding at a 5.52% CAGR. The upward curve is anchored in mega-project construction pipelines, stricter water-efficiency codes, and premiumization trends that lift average selling prices. Government diversification programs in Saudi Arabia, the UAE, and Qatar sustain multi-year procurement cycles that insulate vendors from routine construction swings. Rapid hotel development, a growing base of owner-occupied homes, and e-commerce-enabled procurement are widening the addressable demand for tiles and fixtures. Local producers continue to add capacity, yet they face rising energy costs and potential competition if anti-dumping duties lapse. Global brands deepen regional footprints to secure large contracts and to meet green-building requirements that now influence every major project.

Key Report Takeaways

- By product category, tiles held 63% revenue share in 2024, while sanitary ware is forecast to grow at a 7.2% CAGR through 2030.

- By material, ceramic captured 68.5% of revenue in 2024; acrylic and perspex sanitary ware is projected to advance at a 7.4% CAGR to 2030.

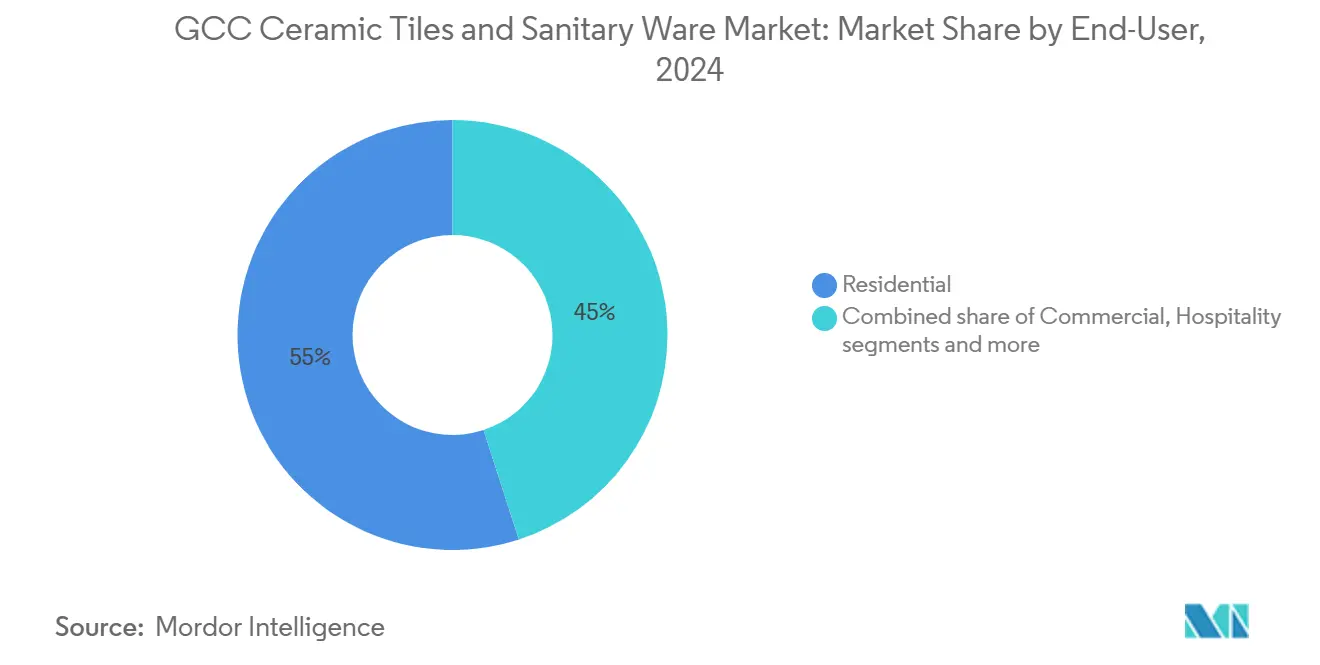

- By end-user, residential applications commanded 55% of demand in 2024, whereas commercial installations are expected to expand at a 6.8% CAGR through 2030.

- By construction type, replacement and renovation accounted for 39% share of the GCC sanitary ware market size in 2024 and is set to grow at a 7.1% CAGR to 2030.

- By country, Saudi Arabia led with 37% of the GCC sanitary ware market share in 2024, while the UAE registers the fastest country-level CAGR at 7.0% through 2030.

GCC Ceramic Tiles And Sanitary Ware Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed mega-projects under GCC Visions | +1.8% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Rising consumer spend on home renovations and luxury bathrooms | +1.2% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Tourism-fueled hotel pipeline enlarging premium demand | +1.0% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Mandatory water-efficiency labeling accelerating low-flow sanitary ware | +0.8% | GCC-wide | Short term (≤ 2 years) |

| Off-site modular bathroom pods multiplying factory-finished tile demand | +0.5% | UAE, Saudi Arabia | Medium term (2-4 years) |

| Green-building credits spurring recycled-content ceramics | +0.4% | UAE, Qatar, Saudi Arabia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-Backed Mega-Projects Under GCC Visions

Saudi giga-projects such as NEOM, the Red Sea Project, and Qiddiya each specify millions of square meters of tiles and large volumes of advanced sanitary fixtures. The sheer scale stabilizes the GCC sanitary ware market by locking in multi-year purchase agreements and compelling manufacturers to localize capacity[1]RAK Ceramics, “ESG Report 2023,” rakceramics.com. Comparable diversification programs in the UAE and Qatar follow similar pathways, continually refreshing tender pipelines that support both commodity and premium product segments of the GCC sanitary ware market.

Rising Consumer Spend on Home Renovations & Luxury Bathrooms

The AED 90 billion First-Time Home Buyer Programme in the UAE triggered a surge in owner-occupied villas and apartments, where buyers prioritize smart toilets, freestanding tubs, and designer faucets[2]Arabian Business, “UAE launches new expanded ‘Digital Procurement Platform’ catalogue,” arabianbusiness.com. Shorter renovation cycles translate into recurring revenue opportunities, advancing the GCC sanitary ware market as homeowners seek status-oriented upgrades and water-efficient fixtures that satisfy new green codes.

Tourism-Fueled Hotel Pipeline Enlarging Premium Demand

More than 400,000 hotel rooms are under construction or planning across the region through 2030, with roughly 48,000 rooms in the UAE alone. Each room needs multiple fixtures, creating outsized demand for large-format slabs and smart sanitary ware. Hospitality standards require faster replacement, giving suppliers a dependable refresh cycle and bolstering value growth in the GCC sanitary ware market.

Mandatory Water-Efficiency Labeling Accelerating Low-Flow Sanitary Ware

Systems such as Abu Dhabi’s ESTIDAMA Pearl, Dubai’s Al Sa’fat, Qatar’s GSAS, and Saudi Building Code 701 require dual-flush toilets and low-flow taps. These rules push legacy fixtures out and elevate certified products, a transition that channels procurement toward established brands able to document compliance and therefore expands the GCC sanitary ware market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material and energy price volatility | -0.6% | Saudi Arabia, UAE | Short term (≤ 2 years) |

| Import-driven price wars from low-cost Asian tiles | -0.5% | GCC-wide | Medium term (2-4 years) |

| High breakage risk for large-format slabs | -0.3% | Saudi Arabia, UAE, Qatar | Short term (≤ 2 years) |

| Slow contractor adoption of e-commerce procurement | -0.2% | GCC-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material and Energy Price Volatility

Natural gas feeds represent around half of the kiln operating costs. Saudi industrial gas rose from USD 0.75 to USD 1.25 per MMBtu, and further hikes remain plausible. Margin compression already reduced Saudi Ceramics’ net profit in H1 2024 by 90% despite steady top-line sales. Similar exposure exists across local producers, placing a drag on near-term earnings and on reinvestment capacity within the GCC sanitary ware market.

Import-Driven Price Wars from Low-Cost Asian Tiles

Anti-dumping duties on Chinese and Indian tile imports are scheduled for sunset review in June 2025. A rollback could reintroduce inventory priced 20% lower than regional output, pressuring selling prices and profitability. Such competition would echo through distributor networks, tempering value expansion in the GCC sanitary ware market.

Segment Analysis

By Product: Sanitary Ware Outpaces Tiles on Technology Adoption

The segment generated 63% of overall revenue from tiles in 2024, yet sanitary ware is set to climb faster at 7.2% CAGR through 2030. Premium fixtures, including smart toilets with app-based hygiene analytics, lift margins and shorten replacement intervals. Continued hotel construction and owner-occupied home renovations bring steady volume. Large-format slabs still dominate lobby and façade finishes, but design-led bathrooms drive the most value for the GCC sanitary ware market. The product mix shift supports manufacturer moves up the price curve, thereby enhancing the resilience of the GCC sanitary ware market.

Rising investment in IoT-enabled faucets and touchless cisterns underscores a technology-first mindset among developers and homeowners. Economies of scale from new local lines reduce lead times for commodity tiles, allowing plant capacity to pivot toward value-added fixtures. This balance lets producers defend share even if anti-dumping duties expire. The sanitary ware uptrend therefore underpins sustainable long-term growth in the GCC sanitary ware market.

Note: Segment shares of all individual segments available upon report purchase

By Material: Acrylic Gains Momentum in Wellness-Centric Projects

Ceramic retained 68.5% revenue in 2024 thanks to affordability and strength, yet lightweight acrylic bathtubs gained rapid adoption in spa-style bathrooms across luxury hotels. The 7.4% CAGR forecast for acrylic and perspex through 2030 stems from moldability that enables freestanding units, chromotherapy features, and lower transport costs. These attributes align with consumer preferences for wellness, pushing more orders toward higher-margin materials that elevate the GCC sanitary ware market size at the premium end.

Porcelain slabs, prized for low porosity and seamless visuals, maintain relevance in high-traffic zones. Manufacturers add recycled content to porcelain lines to meet green credits, mitigating raw-material volatility. This evolutionary portfolio preserves ceramic’s mass-market presence while letting acrylic and porcelain chase upscale niches, jointly diversifying revenue streams inside the GCC sanitary ware market.

By End-User: Commercial Installations Accelerate on Hospitality Demand

Residential buyers drove 55% of 2024 value, mostly through first-time homeowners seeking mid-range ceramic solutions. Yet commercial spaces, led by hotels and malls, will grow 6.8% CAGR amid a 400,000-room regional pipeline. Hospitality specifications of large-format slabs and sensor-activated fixtures lift average selling prices and reduce replacement intervals to five-to-seven years. This cadence intensifies demand for rapid turnaround services, helping suppliers lock in repeat business and stabilize forecasting for the GCC sanitary ware market.

Institutional builds such as hospitals and schools also benefit from water-saving mandates, elevating procurement standards. Suppliers providing compliance documentation and service contracts gain an advantage, further cementing commercial share growth within the GCC sanitary ware market.

Note: Segment shares of all individual segments available upon report purchase

By Construction Type: Renovation Overtakes New Build in Growth Rate

New construction still accounts for 61% of revenue, yet renovation is slated to rise at 7.1% CAGR, outpacing new projects by 100 basis points. Aging hotels in Dubai and mid-2000s residential towers face tenant pressure for modern finishes and water-saving fixtures. As owners bring interiors up to code, renovation spend becomes a stable contributor to the GCC sanitary ware market size.

Faster renovation cycles favor modular solutions and adhesive systems that cut downtime. Manufacturers that supply both product and training on quick-set materials win bids and secure after-sales maintenance. These services lock in loyalty and cushion the GCC sanitary ware market from macro construction slowdowns.

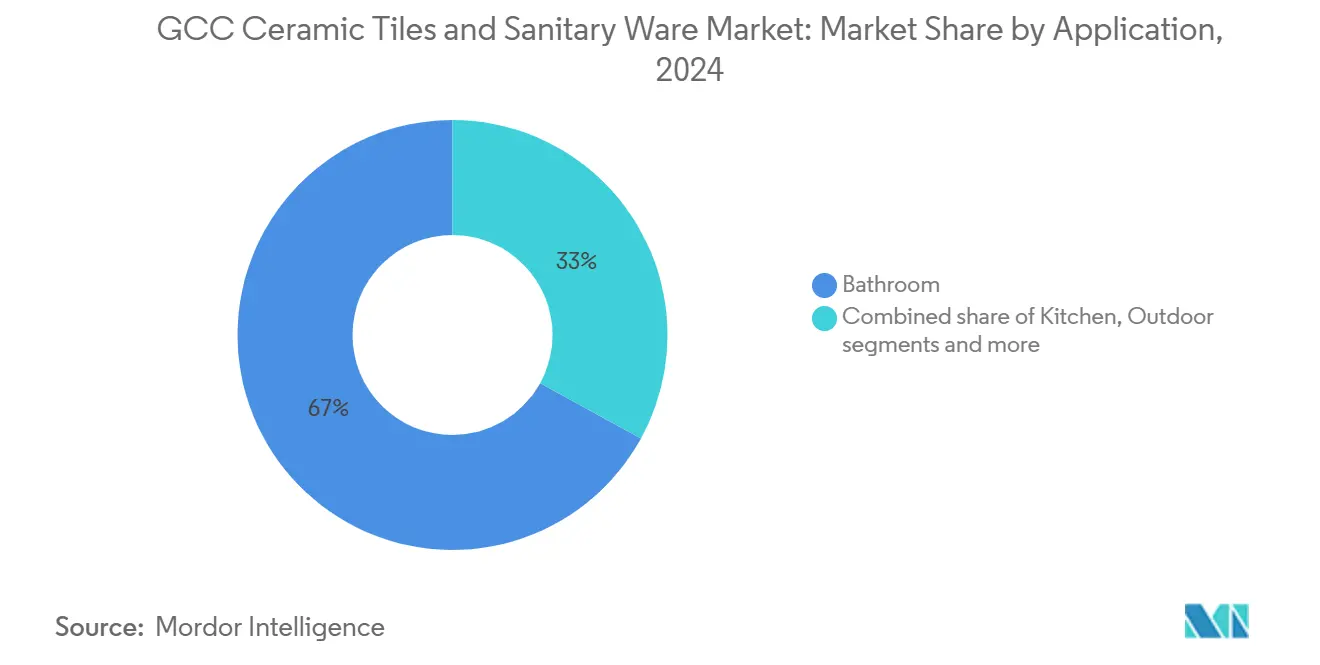

By Application: Kitchens Close the Gap Behind Bathroom Dominance

Bathrooms absorbed 67% of value in 2024 because every unit requires multiple fixtures and extensive tile coverage. However, open-plan living is transforming kitchens into social hubs that command design attention. Kitchen applications are forecast to grow 6.6% CAGR as homeowners install porcelain slab backsplashes and integrated worktops. Modular kitchen pods imported for residential towers bring direct factory orders, squeezing supply chains yet creating scale for the GCC sanitary ware market.

Outdoor and pool applications gain relevance in luxury villas and resorts, using slip-resistant pavers and decorative mosaics that withstand desert climates. These niches marginally lift volume but deliver strong margins, supporting the higher end of the GCC sanitary ware industry.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Digital Ordering Gains Scale

Offline showrooms still hold 72% share because touch-and-feel remains crucial for high-value decisions. Yet the UAE Digital Procurement Platform showed that digital tendering can cut buying cycles from 60 days to six minutes ARABIANBUSINESS.COM. Online channels are therefore expected to rise 12.0% CAGR, the quickest of any route, allowing contractors to compare real-time prices and specifications. Direct B2B developer contracts already account for 18% of volume and climb as mega-projects lock in multi-year supply at fixed prices. These channel shifts dilute traditional retailer power but broaden reach, fueling broader penetration of the GCC sanitary ware market.

Vendors that integrate virtual showrooms, AR visualizers, and sample delivery retain design influence while capturing digital efficiencies. Omnichannel competence becomes a decisive factor in sustaining growth and defending margins across the GCC sanitary ware market.

Geography Analysis

Saudi Arabia generated 37% of 2024 revenue, anchored by Vision 2030 giga-projects that collectively demand millions of fixtures each year. The kingdom’s higher VAT and potential gas price hikes strain margins, yet sovereign funding buffers project timelines, giving suppliers volume certainty and reinforcing Saudi Arabia’s anchor role in the GCC sanitary ware market. Anti-dumping protection remains pivotal; an unfavorable 2025 review could invite lower-cost Asian imports and squeeze domestic producers.

The UAE held a 31% share in 2024 and is set to grow fastest at a 7.0% CAGR. A 48,000-room hotel pipeline and AED 90 billion in first-time home purchases underpin robust construction. Water-efficiency codes and e-procurement mandates accelerate the adoption of compliant smart fixtures, thereby lifting value capture in the GCC sanitary ware market. Showroom investment remains intense in Dubai and Abu Dhabi, yet online ordering is scaling quickly, especially for repeat commodity items.

Qatar’s post-World Cup infrastructure push raised monthly building permits by 36% in July 2024[3]Commercial Interior Design, “Surface design: How Middle East designers are rethinking materiality,” commercialinteriordesign.com. GSAS green-building rules favor certified products, offering a premium share for brands with documented performance. Kuwait, Bahrain, and Oman contribute smaller slices yet carve niches in luxury residential and boutique resorts where design differentiation commands high margins. Collectively, these sub-markets enrich supplier portfolios and reinforce demand diversity inside the GCC sanitary ware market.

Competitive Landscape

Local majors RAK Ceramics and Saudi Ceramics retain scale advantages, yet energy-cost escalation and potential duty expiry test pricing power. RAK Ceramics invested USD 49.9 million in kiln upgrades and smart factory automation during 2024, yet its sanitary ware revenue fell 8.6% in the same year. Saudi Ceramics commissioned an 8.25 million m² tile plant in Q1 2024 to meet forecast demand, but saw net profit plunge as gas costs climbed.

International players amplify competitive heat. Grohe opened a 26,000 m² Dammam plant in 2024 and launched installer training tours nationwide. Kohler established Riyadh headquarters in December 2024 to anchor Middle East operations, while Villeroy & Boch completed a EUR 600 million takeover of Ideal Standard, consolidating premium distribution. These moves shorten lead times and strengthen after-sales networks, positioning global brands to win hotel and government contracts that define high-value slices of the GCC sanitary ware market.

Strategic white space centers on modular pods, e-commerce, and verified sustainability. Few suppliers yet bundle tiles, fixtures, adhesive, and rapid-install training in a single offer. Digital procurement remains in early growth, creating room for first movers with user-friendly pricing engines and AR visualization. Environmental Product Declarations are still absent across many regional lines, handing compliant firms a strong bid advantage as green codes tighten. The competitive field, therefore, favors firms that unite localized production, digital service, and sustainability credentials to capture emerging premiums within the GCC sanitary ware market.

GCC Ceramic Tiles And Sanitary Ware Industry Leaders

RAK Ceramics

Saudi Ceramic Company

Al Anwar Ceramic Tiles Co.

Jaquar Middle East

Riyadh Ceramics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Kohler opened its regional headquarters in Riyadh to deepen project engagement across Saudi giga-projects.

- October 2024: Grohe launched a multi-city Pro Tour in Saudi Arabia to train plumbers on touchless water-efficient fixtures.

- September 2024: RAK Ceramics unveiled recycled-resin acrylic bathtubs aimed at wellness-focused hospitality projects.

- February 2024: RAK Ceramics signed a two-year supply pact with Azizi Developments for residential and mixed-use projects

GCC Ceramic Tiles And Sanitary Ware Market Report Scope

The GCC Ceramic Tiles and Sanitary Ware Market is segmented by product, material, end user, construction type, application, distribution channel, and country. By product, the market is segmented into tiles and sanitary ware. By material, the market is segmented into ceramic, porcelain, glazed ceramic, unglazed or vitrified, and others, including stoneware, acrylic, and metal. By end user, the market is segmented into residential, commercial, hospitality, and industrial or institutional. By construction type, the market is segmented into new construction and replacement, and renovation. By application, the market is segmented into bathroom, kitchen, outdoor or landscaping, and pools and water features. By distribution channel, the market is segmented into offline retail, including specialty stores, direct to project or business to business, and online or e-commerce. By country, the market is segmented into the United Arab Emirates, Saudi Arabia, Qatar, Kuwait, Bahrain, and Oman. The report provides the market size in value terms in USD for all the above-mentioned segments.

| Tiles | Floor Tiles |

| Wall Tiles | |

| Decorative / Mosaic Tiles | |

| Outdoor / Anti-Slip Tiles | |

| Sanitary Ware | Water Closets |

| Wash Basins | |

| Cisterns | |

| Bidets | |

| Pedestals | |

| Urinals |

| Ceramic |

| Porcelain |

| Glazed Ceramic |

| Unglazed / Vitrified |

| Others (Stoneware, Acrylic, Metal) |

| Residential |

| Commercial |

| Hospitality |

| Industrial / Institutional |

| New Construction |

| Replacement & Renovation |

| Bathroom |

| Kitchen |

| Outdoor / Landscaping |

| Pools & Water Features |

| Offline Retail (Specialty Stores) |

| Direct-to-Project / B2B |

| Online / E-commerce |

| United Arab Emirates |

| Saudi Arabia |

| Qatar |

| Kuwait |

| Bahrain |

| Oman |

| By Product | Tiles | Floor Tiles |

| Wall Tiles | ||

| Decorative / Mosaic Tiles | ||

| Outdoor / Anti-Slip Tiles | ||

| Sanitary Ware | Water Closets | |

| Wash Basins | ||

| Cisterns | ||

| Bidets | ||

| Pedestals | ||

| Urinals | ||

| By Material | Ceramic | |

| Porcelain | ||

| Glazed Ceramic | ||

| Unglazed / Vitrified | ||

| Others (Stoneware, Acrylic, Metal) | ||

| By End-User | Residential | |

| Commercial | ||

| Hospitality | ||

| Industrial / Institutional | ||

| By Construction Type | New Construction | |

| Replacement & Renovation | ||

| By Application | Bathroom | |

| Kitchen | ||

| Outdoor / Landscaping | ||

| Pools & Water Features | ||

| By Distribution Channel | Offline Retail (Specialty Stores) | |

| Direct-to-Project / B2B | ||

| Online / E-commerce | ||

| By Country | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Kuwait | ||

| Bahrain | ||

| Oman | ||

Key Questions Answered in the Report

What is the current value of the GCC sanitary ware market?

The market is valued at USD 9.74 billion in 2025.

How fast is demand expected to grow through 2030?

Sales are projected to rise at a 5.52% CAGR to reach USD 12.74 billion by 2030.

Which country records the highest market share?

Saudi Arabia held 37% of regional revenue in 2024.

Why are renovation projects gaining ground?

Aging residential and hotel stock in Dubai and Riyadh face code updates and consumer expectations, lifting renovation demand at a 7.1% CAGR.

How important is e-commerce procurement?

Online channels are expected to expand 12% annually as digital platforms cut buying cycles and increase price transparency.