| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 7.55 Billion |

| Market Size (2030) | USD 12.81 Billion |

| CAGR (2025 - 2030) | 11.16 % |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Bottled Water Market Major Players")

Bottled Water Market Size")

GCC Bottled Water Market Analysis

The Gulf Cooperation Council Bottled Water Market size is estimated at USD 7.55 billion in 2025, and is expected to reach USD 12.81 billion by 2030, at a CAGR of 11.16% during the forecast period (2025-2030).

The GCC bottled water market continues to benefit from robust growth in the tourism and hospitality sectors, which serve as key demand drivers across the region. The tourism industry's total economic contribution reached USD 155.4 billion in 2019, with the United Arab Emirates leading international tourist arrivals at 20.7 million visitors, followed by Saudi Arabia with 19 million visitors, and Bahrain with 12.7 million visitors. This substantial tourist influx has led to the rapid expansion of foodservice channels, including hotels, restaurants, and cafes, creating increased demand for bottled water products through these establishments.

A significant transformation in consumer preferences is reshaping the bottled water landscape, with health-conscious consumers increasingly shifting away from carbonated beverages toward healthier alternatives. The UAE market exemplifies this trend, with residents consuming an average of 250 liters of drinking water per year, representing one of the highest per capita consumption rates globally. This shift is particularly pronounced among the region's large expatriate population, which comprises between 32-39% of the working population across GCC countries, bringing diverse consumption patterns and preferences for premium water products.

The distribution landscape is evolving rapidly with the emergence of innovative delivery models and digital platforms. Major retailers and bottled water companies are investing heavily in e-commerce capabilities and home delivery services to meet changing consumer expectations. The market has witnessed the launch of several water delivery applications across GCC countries, enabling consumers to compare brands, prices, and schedule deliveries conveniently. This digital transformation has been particularly successful in reaching younger, tech-savvy consumers and urban professionals seeking convenience.

Industry collaboration and sustainability initiatives are becoming increasingly prominent, reflecting growing environmental awareness and regulatory pressures. A significant development was the formation of the Gulf Bottled Water Association (GBWA) in 2021, bringing together industry leaders to address sector challenges and promote sustainability. Companies are also implementing innovative packaging solutions and recycling programs, with several major brands introducing eco-friendly packaged water options and establishing recycling infrastructure across the region. These initiatives demonstrate the industry's commitment to environmental stewardship while maintaining product quality and meeting growing consumer demand for mineral water.

GCC Bottled Water Market Trends

Growth in Tourism Industry Leading to Favorable Demand

The robust tourism sector across GCC countries has emerged as a crucial driver for bottled water consumption, with both religious and non-religious tourism showing significant expansion potential. The total economic contribution toward tourism and travel in the GCC region has demonstrated steady growth, reaching $155.4 billion in 2019, highlighting the sector's substantial impact on bottled water demand. This growth in tourism has catalyzed the expansion of foodservice channels, including cafes, pubs, hotels, and restaurants across the region, creating multiple consumption points for bottled water products.

The distribution of international tourists across key GCC countries further emphasizes the market potential, with the United Arab Emirates receiving 20.7 million visitors, Saudi Arabia welcoming 19 million tourists, and Bahrain hosting 12.7 million visitors. In response to this growing tourist influx, bottled water manufacturers are developing various sizes of bottled water products that can be easily carried by tourists, catering to their specific needs and requirements. Additionally, companies are focusing on flavor innovation in the bottled water segment, particularly targeting tourists and expatriates, thereby diversifying their product offerings to meet varied consumer preferences.

Understand The Key Trends Shaping This Market

Download PDF

Foreign Brand Investments Along with Strategic Initiatives

The GCC bottled water market has witnessed significant foreign investment, particularly from global industry leaders who are helping accelerate the development of the bottled water industry across the region. A notable example is Nestlé Waters' investment of AED 100 million in constructing a water factory in Abu Dhabi's Higher Corporation for Specialized Economic Zones (ZonesCorp). This facility has been designed to meet the highest standards in environmental sustainability, positioning it as one of the most water and energy-efficient bottling facilities in the region, demonstrating the industry's commitment to sustainable practices while meeting increasing demand.

Beyond production investments, companies are implementing strategic initiatives focused on consumer education and environmental responsibility. For instance, Nestlé Waters has collaborated with international NGO Project WET to raise awareness about water conservation, reaching approximately 22,000 active participants among students and instructors throughout schools in the United Arab Emirates. Furthermore, local initiatives such as the Sharjah school program, where the government-run Zulal bottled water company provides free bottled water to school pupils, demonstrate the industry's commitment to promoting healthy hydration habits among youth while expanding their consumer base through strategic community engagement.

Rising Water Scarcity in the Region

The Middle East & North Africa region, including GCC countries, faces severe water scarcity challenges, with more than 60% of the population having limited or no access to drinking water. This scarcity has created a fundamental dependency on bottled water, as over 70% of the region's gross domestic product (GDP) is exposed to high or very high-water stress, significantly exceeding the global average of 22%. The situation is particularly critical as the World Bank projects that climate-related water scarcity could lead to economic losses accounting for 6-14% of GDP by 2050, making it the region with the greatest expected economic impact from water-related challenges.

The deep scarcity of drinking water, coupled with the limited availability of treated water, has transformed bottled water from a convenience product to a necessity across the GCC region. This transformation is further intensified by the region's challenging climate conditions and rapid urbanization, which place additional strain on existing water resources. The situation has prompted both consumers and businesses to rely heavily on bottled water as a primary source of drinking water, particularly in areas where traditional water infrastructure struggles to meet the growing demand for clean, safe drinking water.

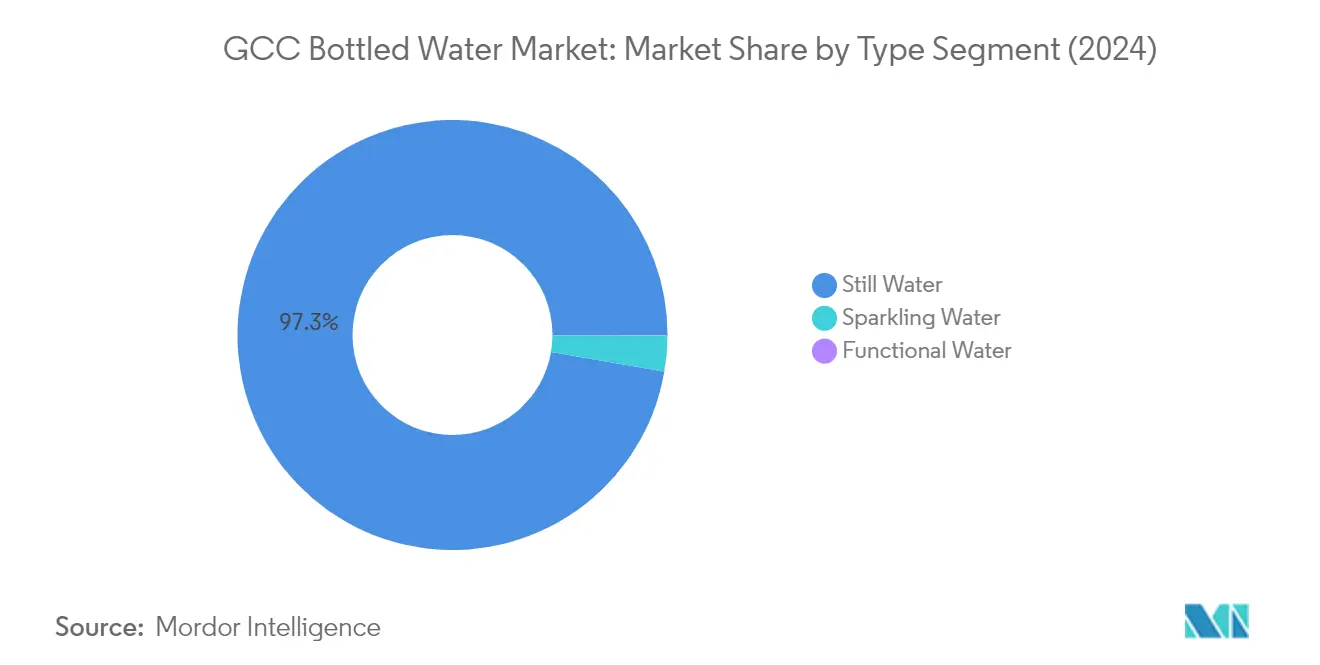

Segment Analysis: By Type

Still Water Segment in GCC Bottled Water Market

The still water segment continues to dominate the GCC bottled water market, commanding approximately 97% of the total market share in 2024. This overwhelming market dominance can be attributed to several factors, including the region's hot climate, growing health consciousness among consumers, and increasing settlement of expatriate populations and office spaces. The segment's growth is further supported by the rising tourism industry and the expansion of foodservice channels such as hotels and restaurants across the GCC region. Major companies are focusing on product innovation and packaging improvements to maintain their competitive edge, with particular emphasis on eco-friendly packaging solutions and various bottle sizes to cater to different consumer needs. The segment has also witnessed significant growth through modern retail channels and home delivery services, making still water more accessible to consumers across all GCC countries.

Functional Water Segment in GCC Bottled Water Market

The functional water segment is emerging as the most dynamic category in the GCC bottled water market, projected to grow at approximately 14% during 2024-2029. This remarkable growth is driven by increasing consumer awareness about health benefits and the rising demand for value-added water products. The segment is witnessing significant innovation with products offering various functional benefits such as enhanced vitamins, minerals, and other nutritional elements. Manufacturers are increasingly focusing on developing new functional water variants that cater to specific health needs, including vitamin-enriched water, protein-infused water, and alkaline water. The growth is further supported by the rising health consciousness among younger consumers and the increasing preference for functional beverages over traditional soft drinks. Premium positioning and innovative marketing strategies are also contributing to the segment's rapid expansion across the GCC region.

Remaining Segments in GCC Bottled Water Market

The sparkling water segment represents a niche but growing category in the GCC bottled water market. This segment is gaining traction as a healthier alternative to carbonated soft drinks, particularly among urban consumers and in the hospitality sector. The segment's growth is supported by increasing product innovations, including the introduction of flavored water variants and premium packaging options. International brands have been particularly active in this segment, introducing various premium sparkling water products that cater to the region's high-end consumer base. The segment has also benefited from the growing trend of using sparkling water as a mixer in mocktails and other beverages, particularly in hotels and restaurants across the GCC region.

Segment Analysis: By Distribution Channel

Supermarkets/Hypermarkets Segment in GCC Bottled Water Market

The supermarkets/hypermarkets segment maintains a dominant position in the GCC bottled water market, commanding approximately 43% market share in 2024. This channel's leadership is primarily attributed to its extensive retail visibility and the convenience it offers to consumers through a wide variety of product offerings. The proximity factor of these channels, especially in developed and large cities, provides them with a strategic advantage in influencing consumer purchasing decisions. These retail outlets also serve as crucial launch platforms for new products across the region, enabling manufacturers to showcase their innovations effectively. The segment's strong performance is further bolstered by consumers' preference for bulk purchasing, allowing them to maximize value for money while making fewer shopping trips. Additionally, these channels maintain strong relationships with both local and international bottled water brands, ensuring consistent product availability and competitive pricing strategies.

On-Trade Channel Segment in GCC Bottled Water Market

The on-trade channel segment, which includes pubs, bars, cafés, clubs, and various food service establishments, is experiencing the fastest growth trajectory in the GCC bottled water market. This remarkable growth is driven by several factors including rising disposable incomes, evolving consumer lifestyles, and the increasing trend of dining out across the region. The segment's expansion is further supported by numerous sporting and business events taking place across GCC countries, which significantly boost bottled water consumption through these channels. Consumers generally perceive on-trade channels as maintaining high quality standards and regulatory compliance, which enhances their trust in products served through these establishments. The segment also benefits from the growing preference for flavored waters among consumers who are more experimental with their beverage choices while dining out.

Remaining Segments in Distribution Channel

The convenience stores segment serves as a crucial distribution channel, particularly in developing areas, offering competitive pricing and extended operating hours to meet last-minute purchase needs. The home and office delivery segment has gained significant traction due to the increasing demand for convenience and the growth of residential and commercial spaces across the GCC region. This channel has been particularly strengthened by the emergence of various mobile applications and online ordering platforms. Other distribution channels, including online retail stores, warehouse clubs, and vending machines, though smaller in market share, play an important role in reaching specific consumer segments and providing alternative purchase options for consumers seeking convenience and accessibility.

Gulf Cooperation Council (GCC) Bottled Water Market Geography Segment Analysis

Bottled Water Market in Saudi Arabia

Saudi Arabia continues to dominate the GCC bottled water market, commanding approximately 39% of the total market share in 2024. The country's market leadership is driven by its large population base, increasing health consciousness among consumers, and a significant shift from carbonated beverages to bottled water. The hot climate and growing tourism industry, particularly religious tourism in cities like Makkah and Madinah, contribute substantially to the sustained demand. The market is characterized by strong domestic production capabilities, with numerous local manufacturers maintaining stringent quality standards in line with SFDA regulations. The retail landscape is well-developed, featuring diverse distribution channels including supermarkets, convenience stores, and growing home delivery services. Consumer preferences in Saudi Arabia are increasingly tilting towards premium water and functional water variants, with manufacturers responding through product innovations in areas like alkaline water and vitamin-enriched options.

Bottled Water Market in Bahrain

Bahrain's bottled water market is experiencing remarkable growth, projected to expand at approximately 14% annually from 2024 to 2029. The country's dynamic market is driven by its tech-savvy population's increasing adoption of water delivery applications and digital ordering platforms. The market structure is characterized by a mix of local and international players, creating a competitive environment that fosters innovation and service quality improvements. Bahrain's strategic focus on water resource management, coupled with the establishment of the Water Resources Council, has created a robust regulatory framework that ensures high-quality standards in the bottled water industry. The market has witnessed significant modernization in distribution networks, with companies implementing sophisticated delivery systems and innovative packaging solutions. Consumer preferences are evolving, with increasing demand for premium water products and functional variants that offer additional health benefits.

Bottled Water Market in United Arab Emirates

The United Arab Emirates represents a sophisticated bottled water market characterized by high per capita consumption rates and innovative product offerings. The country's position as a global business and tourism hub significantly influences market dynamics, with premium water and luxury water brands finding strong acceptance among consumers. The UAE's market is distinguished by its advanced distribution infrastructure, including modern retail channels and efficient home delivery services. Sustainability has become a key focus area, with manufacturers increasingly adopting eco-friendly packaging solutions and implementing water conservation practices. The market demonstrates strong segmentation across various product categories, from basic mineral water to premium functional water variants. Local manufacturers have shown remarkable capability in competing with international brands, often leading in product innovation and market responsiveness.

Bottled Water Market in Kuwait

Kuwait's bottled water market exhibits strong growth potential, supported by the country's high disposable income levels and increasing health consciousness among consumers. The market is characterized by sophisticated consumer preferences, with growing demand for premium and functional water products. Kuwait's retail landscape has evolved significantly, with modern trade channels and e-commerce platforms playing an increasingly important role in distribution. The country's extreme climatic conditions and limited natural water resources have made bottled water an essential commodity rather than a luxury item. Local manufacturers have invested significantly in advanced production technologies and quality control measures, ensuring high standards of product quality. The market shows strong segmentation across various price points and product categories, catering to diverse consumer preferences.

Bottled Water Market in Other Countries

The bottled water markets in other GCC countries, particularly Qatar and Oman, demonstrate unique characteristics and growth patterns. These markets are characterized by strong local production capabilities and growing consumer awareness about health and wellness. The competitive landscape in these countries features a mix of established local players and international brands, creating a dynamic market environment. Distribution networks have evolved significantly, with modern retail formats and digital platforms gaining prominence. Consumer preferences in these markets are increasingly sophisticated, with growing demand for premium and functional water products. Both countries have implemented robust regulatory frameworks to ensure product quality and safety standards, while also focusing on sustainable packaging solutions and environmental considerations.

Get Analysis on Important Geographic Markets

Download PDF

GCC Bottled Water Industry Overview

Top Companies in GCC Bottled Water Market

The GCC bottled water market features a mix of multinational corporations and regional players actively competing through various strategic initiatives. Companies are increasingly focusing on product innovation through the introduction of specialized variants like alkaline water, zero-sodium options, and flavored alternatives to cater to evolving consumer preferences. Operational excellence is being pursued through investments in advanced bottling technologies and expanded production capacities across key markets. Strategic partnerships and distribution network optimization remain crucial focus areas, with companies leveraging both traditional retail channels and emerging digital platforms. Market leaders are also emphasizing sustainability initiatives, including eco-friendly packaging solutions and responsible water sourcing practices, while simultaneously expanding their geographical presence through new manufacturing facilities and market entries.

Dynamic Market with Strong Regional Players

The competitive landscape is characterized by a balanced presence of both global beverage conglomerates and well-established regional specialists with deep market understanding. Global players like Nestlé, PepsiCo, and Danone leverage their international expertise and brand recognition, while regional leaders such as Agthia Group, Masafi Co., and Binzomah Group capitalize on their local market knowledge and established distribution networks. The market structure exhibits moderate consolidation, with the top players collectively holding significant market share while numerous smaller players operate in specific geographic or product niches.

The market has witnessed notable merger and acquisition activities as companies seek to strengthen their market positions and expand their operational footprint. Regional players are increasingly pursuing strategic partnerships and acquisitions to enhance their production capabilities and distribution reach, while international companies are establishing local manufacturing facilities through joint ventures or direct investments. This dynamic has created a competitive environment where success depends on balancing scale advantages with local market responsiveness.

Innovation and Distribution Drive Market Success

Success in the GCC bottled water market increasingly depends on companies' ability to differentiate their offerings through innovation while maintaining efficient distribution networks. Market leaders are investing in research and development to create unique product propositions, including premium water variants and health-focused offerings. Distribution excellence has become paramount, with companies needing to maintain strong relationships with both traditional retail channels and emerging e-commerce platforms. Additionally, sustainability initiatives and compliance with regional quality standards have become crucial factors in maintaining market position.

For new entrants and challenger brands, the path to market share growth requires a combination of targeted market positioning and operational excellence. Companies must navigate the high consumer brand loyalty while addressing the growing demand for premium water and specialized packaged water products. The regulatory environment, particularly regarding water sourcing and quality standards, continues to shape market dynamics and entry barriers. Future success will increasingly depend on companies' ability to balance premium positioning with competitive pricing, while simultaneously addressing sustainability concerns and maintaining operational efficiency in a market characterized by intense competition and evolving consumer preferences.

GCC Bottled Water Market Leaders

-

NestlE SA

-

Agthia Group PJSC

-

Masafi Inc.

-

PepsiCo Inc.

-

DANONE SA

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

GCC Bottled Water Market News

In 2021, Masafi Co LLC introduced a sustainable bottled drinking water brand in the United Arab Emirates called SOURCE.

In 2021, Red Sea Development Co. inaugurated the first 100% renewable bottled water plant in Saudi Arabia. It is the country's first mineral water extraction plant that uses solar and wind energy in line with efforts to preserve the environment by limiting carbon emissions.

In March 2020, Agthia Group launched the Al Ain Plant bottle, the region's first plant-based water bottle. The packaging of the new Al Ain Plant Bottle is environmentally-friendly and made of 100% plant-based sources, including the cap.

GCC Bottled Water Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

-

4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 By Type

- 5.1.1 Still Water

- 5.1.2 Sparkling Water

- 5.1.3 Functional Water

-

5.2 By Distribution Channel

- 5.2.1 Supermarkets/Hypermarkets

- 5.2.2 Convenience/Grocery Stores

- 5.2.3 On-trade Channels

- 5.2.4 Home and Office Delivery

- 5.2.5 Other Distribution Channels

-

5.3 Geography

- 5.3.1 Saudi Arabia

- 5.3.2 United Arab Emirates

- 5.3.3 Kuwait

- 5.3.4 Qatar

- 5.3.5 Bahrain

- 5.3.6 Oman

6. COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

-

6.3 Company Profiles

- 6.3.1 Nestle SA

- 6.3.2 Agthia Group PJSC

- 6.3.3 Masafi Inc.

- 6.3.4 ALGhadeer Drinking Water LLC

- 6.3.5 PepsiCo Inc.

- 6.3.6 Crystal Mineral Water & Refreshments LLC Co.

- 6.3.7 Al-Qassim Water

- 6.3.8 Al Furat Drinking Water LLC

- 6.3.9 New Technology Bottling Company (NTBC) KSCC

- 6.3.10 Al-Rawdatain Water Bottling Co.

- 6.3.11 Danone SA

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

8. IMPACT OF COVD-19 ON THE MARKET

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

GCC Bottled Water Industry Segmentation

Bottled drinking water types are sometimes carbonated, sealed in bottles, and usually certified as pure. The market studied is segmented by type, distribution channel, and geography. By type, the market has been segmented into still water, sparkling water, and functional water. By distribution channel, the market has been segmented into supermarkets/hypermarkets, convenience/grocery stores, on-trade channels, home and office delivery, and other distribution channels. The report outlines the insights from countries in the region, including Saudi Arabia, the United Arab Emirates, Kuwait, Qatar, Bahrain, and Oman. The report offers market size and forecasts in value (USD million) for the above segments.

| By Type | Still Water |

| Sparkling Water | |

| Functional Water | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| On-trade Channels | |

| Home and Office Delivery | |

| Other Distribution Channels | |

| Geography | Saudi Arabia |

| United Arab Emirates | |

| Kuwait | |

| Qatar | |

| Bahrain | |

| Oman |

Need A Different Region or Segment?

Customize Now

GCC Bottled Water Market Research FAQs

How big is the Gulf Cooperation Council (GCC) Bottled Water Market?

The Gulf Cooperation Council (GCC) Bottled Water Market size is expected to reach USD 7.55 billion in 2025 and grow at a CAGR of 11.16% to reach USD 12.81 billion by 2030.

What is the current Gulf Cooperation Council (GCC) Bottled Water Market size?

In 2025, the Gulf Cooperation Council (GCC) Bottled Water Market size is expected to reach USD 7.55 billion.

Who are the key players in Gulf Cooperation Council (GCC) Bottled Water Market?

NestlE SA, Agthia Group PJSC, Masafi Inc., PepsiCo Inc. and DANONE SA are the major companies operating in the Gulf Cooperation Council (GCC) Bottled Water Market.

What years does this Gulf Cooperation Council (GCC) Bottled Water Market cover, and what was the market size in 2024?

In 2024, the Gulf Cooperation Council (GCC) Bottled Water Market size was estimated at USD 6.71 billion. The report covers the Gulf Cooperation Council (GCC) Bottled Water Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Gulf Cooperation Council (GCC) Bottled Water Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Gulf Cooperation Council (GCC) Bottled Water Market Research

Mordor Intelligence provides a comprehensive analysis of the bottled water industry across the GCC region. This analysis covers everything from mineral water and spring water to enhanced water and functional water segments. Our extensive research includes various categories such as premium bottled water, alkaline water, sparkling water, and artesian water. These insights offer a detailed understanding of market dynamics. The report, available as an easy-to-download PDF, thoroughly examines drinking water trends, packaged water distribution channels, and the growing demand for glass bottled water products.

Stakeholders gain valuable insights into diverse segments, including purified water, distilled water, and natural mineral water markets. The report also explores emerging trends in flavored water and carbonated water categories. Our analysis covers bulk water supply chains, portable water solutions, and premium water positioning strategies. Additionally, our research addresses pet bottled water packaging innovations and the evolution of enhanced water products. This delivers actionable intelligence for business decision-makers. The comprehensive report PDF download includes detailed analysis of market dynamics, competitive landscapes, and future growth opportunities in the GCC region.