| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 41.94 Billion |

| Market Size (2030) | USD 51.87 Billion |

| CAGR (2025 - 2030) | 4.34 % |

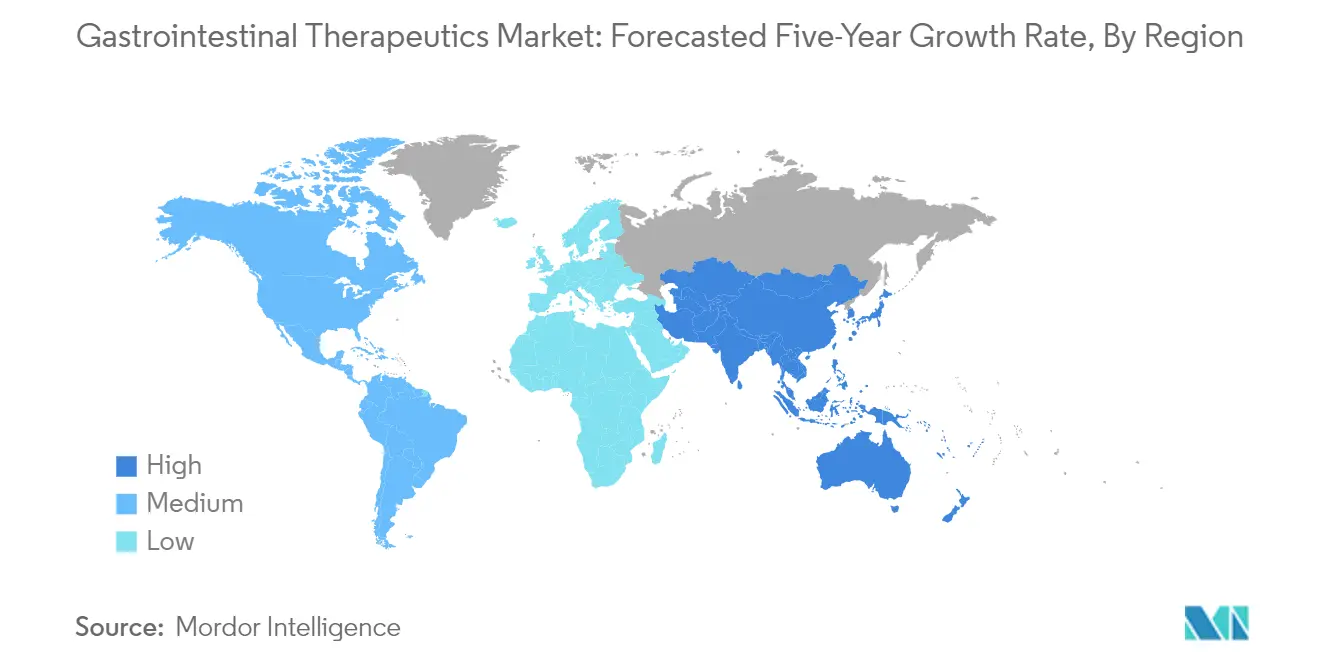

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

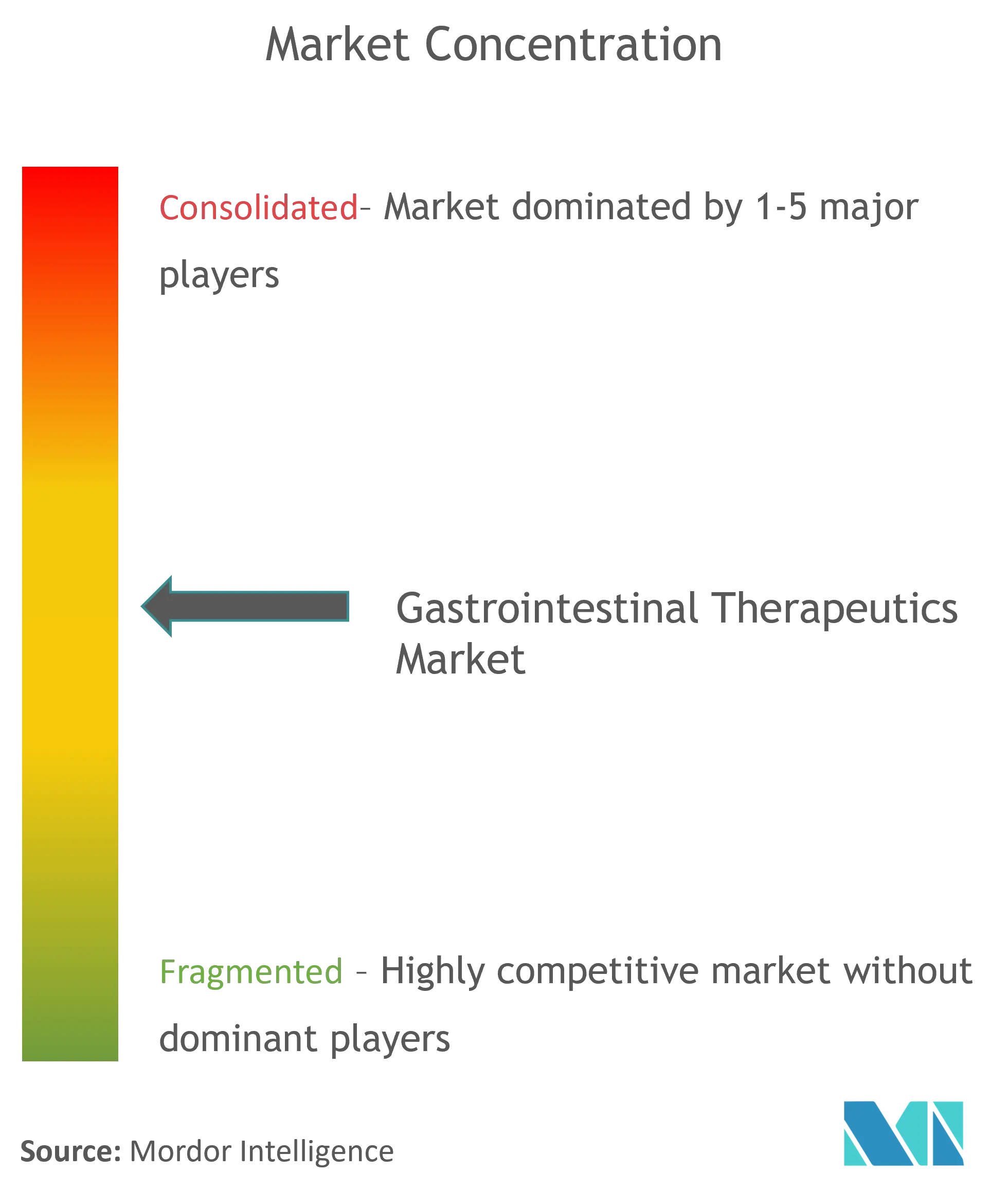

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Gastrointestinal Therapeutics Market Analysis

The Gastrointestinal Therapeutics Market size is estimated at USD 41.94 billion in 2025, and is expected to reach USD 51.87 billion by 2030, at a CAGR of 4.34% during the forecast period (2025-2030).

The gastrointestinal therapeutics market industry is experiencing a significant transformation driven by technological advancements and evolving treatment paradigms. Advanced drug delivery systems, including nanoparticles and sustained-release formulations, are revolutionizing how medications are administered and absorbed in the gastrointestinal tract. According to research published in the International Journal of Medicine in July 2023, nanoparticle-based therapies are showing promising results in treating conditions like colorectal cancer and inflammatory bowel disease, offering enhanced detection precision and improved imaging capabilities. This shift towards innovative delivery mechanisms is reshaping treatment approaches and improving patient outcomes through more targeted and effective therapeutic interventions.

The market is witnessing a notable trend towards personalized medicine and precision therapeutics, particularly in treating inflammatory bowel diseases. Recent epidemiological studies have revealed distinct geographical variations in disease patterns, with Japan showing a higher prevalence of ulcerative colitis among younger males, while the United States exhibits an opposite trend, as reported by the International Journal of Colorectal Disease in May 2023. This understanding of demographic and regional variations is driving the development of more tailored therapeutic approaches, leading to improved treatment outcomes and patient care strategies.

Strategic partnerships and investments are reshaping the competitive landscape, with significant capital flowing into innovative therapeutic solutions. In September 2023, Vivante Health secured USD 31 million in Series B funding to advance its personalized care plans and integrated care approach for gastrointestinal conditions. Similarly, the American Gastroenterological Association's investment in Oshi Health in June 2023 demonstrates the industry's commitment to supporting diagnostic and integrated care solutions. These investments are accelerating the development of novel treatments and improving access to specialized care services within the gastroenterology market.

The industry is witnessing a fundamental shift in treatment approaches, moving from symptomatic management to addressing underlying disease mechanisms. This evolution is supported by extensive research initiatives, with companies like Boehringer Ingelheim initiating more than 630 research, development, and clinical studies globally in 2022. The focus has expanded beyond traditional drug development to include innovative therapeutic modalities, such as targeted biologics and gene therapies. This comprehensive approach to treatment, combined with advances in diagnostic technologies, is enabling earlier intervention and more effective disease management strategies, ultimately improving patient outcomes across the spectrum of gastrointestinal disorders. The growing emphasis on gastrointestinal therapy is evident as the gastrointestinal drugs market continues to evolve, offering new solutions that enhance patient care.

Gastrointestinal Therapeutics Market Trends

Increasing Prevalence of Gastrointestinal Diseases

The therapeutics market for gastrointestinal diseases has witnessed notable expansion, now spanning from inflammatory bowel disease (IBD) to gastroesophageal reflux disease (GERD) and peptic ulcers. According to recent statistics published in January 2023, Crohn's disease shows particularly high prevalence in Western Europe and North America, affecting 100 to 300 per 100,000 people. The disease demonstrates a higher occurrence among people of northern European ancestry and those of eastern and central European (Ashkenazi) Jewish descent, with over half a million Americans currently affected by this disorder. This increasing prevalence pattern is not limited to Crohn's disease but extends to other gastrointestinal conditions, creating a significant healthcare burden that demands effective therapeutic solutions.

The burden of gastrointestinal diseases is further exemplified by the rising incidence of various conditions across different population groups. For instance, according to data released by NBC Universal in February 2023, Norovirus alone accounted for 19 to 21 million incidents of vomiting and diarrhea in the United States during 2023, leading to 465,000 emergency room admissions and 109,000 hospitalizations. The winter season of 2023 saw a particularly notable increase in cases and outbreaks, with peak activity in March 2023 extending well into late spring. Additionally, inflammatory bowel disease (IBD) has emerged as a significant concern, with approximately 1.6 million individuals in the United States affected by conditions including Crohn's disease and ulcerative colitis, as reported by US Pharm in December 2023. These conditions, characterized by gastrointestinal tract inflammation, manifest through symptoms such as persistent diarrhea, abdominal discomfort, and hematochezia.

Understand The Key Trends Shaping This Market

Download PDF

Rising Investments in Research and Development by Pharmaceutical Companies

Pharmaceutical companies are demonstrating increased commitment to research and development in gastrointestinal therapies, as evidenced by significant investments and breakthrough developments throughout 2023. For instance, in October 2023, Eli Lilly and Company revealed promising results from its Phase 3 study evaluating mirikizumab, an investigational interleukin-23p19 antagonist, for treating adults with moderately to severely active Crohn's disease. The VIVID-1 study demonstrated successful achievement of both co-primary and major secondary endpoints compared to placebo, highlighting the pharmaceutical industry's progress in developing targeted therapies for complex gastrointestinal conditions. This advancement is particularly significant given the serious complications associated with Crohn's disease, including severe abdominal pain, diarrhea, and weight loss.

The investment landscape in the gastrointestinal therapeutics market continues to expand, with both private and public sectors contributing to advancements in therapeutic solutions. Government funding has played a crucial role in supporting research initiatives, as evidenced by the National Institutes of Health's allocation of approximately USD 352 million for colorectal cancer research and development in 2022, marking an increase from USD 335 million in 2021. Similarly, Crohn's disease research received USD 92 million in government funding in 2022, up from USD 88 million in 2021. These investments have yielded tangible results, as demonstrated by the FDA approval of mirikizumab in October 2023 for ulcerative colitis treatment, and the successful Phase 3 clinical trial results of zolbetuximab in August 2023, which showed improved survival rates in patients with advanced gastric or gastroesophageal junction cancer when combined with conventional chemotherapy.

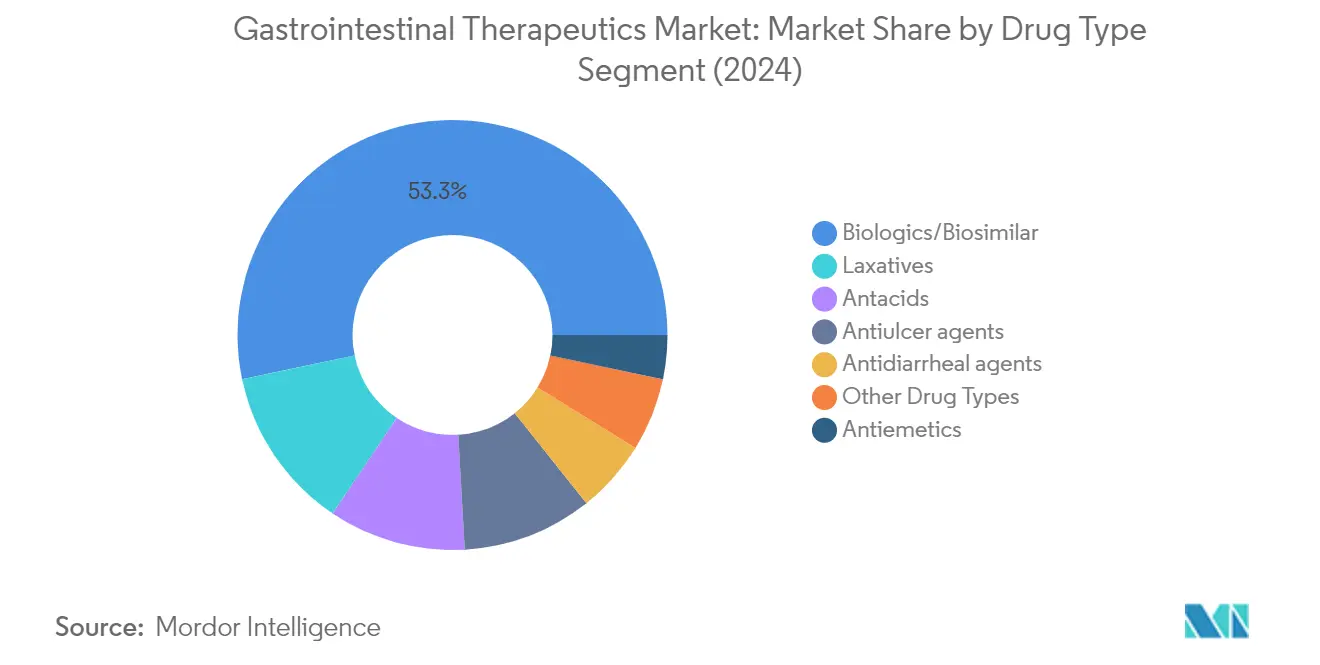

Segment Analysis: By Drug Type

Biologics/Biosimilar Segment in Gastrointestinal Therapeutics Market

The biologics/biosimilar segment dominates the gastrointestinal therapeutics market, commanding approximately 53% of the total market share in 2024, with a value of USD 21.44 billion. This segment's leadership position is primarily driven by the increasing adoption of biologics and biosimilars for treating gastrointestinal diseases, particularly in managing conditions like Crohn's disease and ulcerative colitis. The segment is also experiencing the fastest growth rate in the market, projected to grow at nearly 5% from 2024 to 2029. This growth is supported by recent developments such as the FDA's approval of ABRILADA (adalimumab-afzb) as an interchangeable biosimilar to Humira in October 2023, and Wezlana's approval as one of the first biosimilars to Ustekinumab in November 2023. The exceptional outcomes in therapy and limited recurrence of diseases associated with biologics/biosimilars continue to drive their adoption among healthcare providers and patients.

Remaining Segments in Gastrointestinal Therapeutics Market by Drug Type

The gastrointestinal therapeutics market encompasses several other significant drug segments, each serving specific therapeutic needs. Laxatives represent a substantial portion of the market, primarily used for treating constipation and bowel preparation. Antacids play a crucial role in managing acid-related disorders, while antiulcer agents are essential for treating gastric and duodenal ulcers. Antidiarrheal agents continue to be vital in managing acute and chronic diarrheal conditions, particularly in regions with a high prevalence of gastrointestinal infections. Antiemetics serve a critical function in controlling nausea and vomiting associated with various gastrointestinal conditions. Each of these segments contributes uniquely to the overall market landscape, with their growth driven by factors such as increasing disease prevalence, a rising geriatric population, and continuous product innovations.

Segment Analysis: By Dosage Form

Parenteral Segment in Gastrointestinal Therapeutics Market

The parenteral segment dominates the gastrointestinal therapeutics market, commanding approximately 60% of the total market share in 2024. This significant market position is primarily attributed to the quick onset of action and superior efficacy of parenteral gastrointestinal therapy medications compared to other dosage forms. Many biologics and biosimilars, which are increasingly being used for treating gastrointestinal diseases, are available in injectable formulations. For instance, key medications like Infliximab (Remicade), adalimumab (Humira), golimumab (Simponi), Vedolizumab (Entyvio), and Ustekinumab (Stelara) are administered parenterally for conditions such as ulcerative colitis. The segment is also projected to maintain its growth momentum, driven by factors such as the increasing adoption of parenteral GI medications, continued product launches, and the advantages offered by parenteral products in terms of rapid therapeutic response. Additionally, parenteral doses of GI therapies have proven more effective than oral drugs in certain scenarios, particularly for patients with bleeding peptic ulcers who are treated with parenteral omeprazole.

Oral Segment in Gastrointestinal Therapeutics Market

The oral segment represents a significant portion of the gastrointestinal therapeutics market, with its popularity driven by factors such as convenience, accessibility, and patient compliance. Oral medications are the most commonly prescribed route for GI diseases due to their non-invasive nature and ease of self-administration. The segment benefits from continuous research and development activities focused on improving drug delivery systems and enhancing bioavailability. For example, formulations can be specifically designed to target particular regions in the upper or lower gastrointestinal tract, offering more precise treatment options. Recent developments in oral GI therapeutics include innovative drug delivery technologies that help overcome traditional absorption barriers and improve therapeutic outcomes. The segment's growth is further supported by the increasing prevalence of chronic gastrointestinal conditions requiring long-term medication management and the expanding portfolio of oral medications available for various GI disorders.

Remaining Segments in Dosage Form

Other dosage forms in the gastrointestinal therapeutics market include enteral (NG or PEG) administration via tubes directly into the GI tract, rectal (PR) administration through suppositories, and transdermal patches. These alternative routes of administration play a crucial role in situations where oral or parenteral delivery may not be optimal or feasible. The rectal route, in particular, offers advantages such as partial bypass of hepatic first-pass metabolism and a relatively stable environment with low enzymatic activity. These dosage forms are particularly important for specific patient populations, such as those unable to take oral medications or requiring localized treatment. The development of innovative delivery systems within these segments continues to expand treatment options and improve patient outcomes across various gastrointestinal conditions.

Segment Analysis: By Application

Crohn's Disease Segment in Gastrointestinal Therapeutics Market

The Crohn's Disease segment dominates the global gastrointestinal therapeutics market, holding approximately 36% market share in 2024. This significant market position is driven by strategic initiatives from leading pharmaceutical companies to advance treatment options and address unmet patient needs worldwide. Major developments include Roche's acquisition of Telavant for over USD 7 billion in October 2023, securing rights to develop RVT-3101 for Crohn's disease treatment. Additionally, Eli Lilly and Company's positive Phase 3 study results for mirikizumab, and Agemal Therapeutics' advancement of AGM-129 through clinical trials demonstrate the robust pipeline activity in this segment. The segment's leadership is further strengthened by increasing research collaborations, expanding treatment options, and growing investment in innovative therapies targeting Crohn's disease.

Celiac Disease Segment in Gastrointestinal Therapeutics Market

The Celiac Disease segment is projected to experience the fastest growth rate of approximately 5% during the forecast period 2024-2029. This accelerated growth is supported by significant advancements in research and development of novel therapeutic solutions. Recent developments include Topas Therapeutics' launch of a Phase IIA clinical trial of TPM502 in May 2023, and Anelekion's promising early-stage data for KAN-101 in August 2023. The segment's growth is further propelled by innovative drug developments such as DONQ52, a multispecific antibody by Chugai Pharmaceuticals, targeting the HLA-DQ2.5 serotype complex. Additionally, strategic partnerships, like the Celiac Disease Foundation's collaboration with Mark Cuban Cost Plus Drug Company in December 2023, are enhancing treatment accessibility and awareness, contributing to the segment's rapid expansion.

Remaining Segments in Gastrointestinal Therapeutics Market by Application

The other significant segments in the gastrointestinal therapeutics market include Ulcerative Colitis, Irritable Bowel Syndrome, and Gastroenteritis. The Ulcerative Colitis segment is characterized by continuous innovation in drug development and expanding treatment options, including recent FDA approvals of novel therapies. The Irritable Bowel Syndrome segment benefits from advancing digital therapeutics and increasing focus on personalized treatment approaches. The Gastroenteritis segment is driven by rising disease prevalence and the development of targeted therapeutic solutions. These segments collectively contribute to the market's diversity and demonstrate the industry's commitment to addressing various gastrointestinal conditions through innovative therapeutic approaches and enhanced treatment options.

Gastrointestinal Therapeutics Market Geography Segment Analysis

Gastrointestinal Therapeutics Market in North America

North America represents a dominant force in the global gastrointestinal therapeutics market, driven by advanced healthcare infrastructure, an increasing prevalence of gastrointestinal disorders, and substantial investments in research and development. The region's market landscape is characterized by the presence of major pharmaceutical companies, innovative drug development initiatives, and a robust pipeline of therapeutic solutions. The United States leads the regional market, followed by Canada and Mexico, with all three countries showing distinct patterns in disease prevalence and treatment approaches. The region's growth is further supported by favorable reimbursement policies, increasing awareness about gastrointestinal diseases, and the rising adoption of novel therapeutic solutions.

Gastrointestinal Therapeutics Market in the United States

The United States dominates the North American gastrointestinal therapeutics market, holding approximately 85% market share in 2024. The country's market leadership is attributed to advancements in drug development, an increasing prevalence of gastrointestinal disorders such as ulcerative colitis and irritable bowel syndrome, and rising investments in research and development. The presence of major pharmaceutical companies, extensive clinical research activities, and a favorable regulatory environment further strengthen the market position. The country has witnessed significant developments in therapeutic solutions, particularly in biologics and targeted therapies for inflammatory bowel diseases. The robust healthcare infrastructure and increasing focus on personalized medicine continue to drive innovation in the gastroenterology market.

Gastrointestinal Therapeutics Market in Canada

Canada emerges as a significant market in North America, demonstrating strong growth potential with a projected CAGR of approximately 4% from 2024-2029. The country's market is characterized by increasing research grants, growing accessibility of treatment for digestive diseases, and rising support from government and non-profit organizations. The Canadian market benefits from a universal healthcare system that ensures widespread access to the gastrointestinal drugs market. The country's focus on research and development, particularly in inflammatory bowel disease treatments, coupled with strategic initiatives by pharmaceutical companies to expand their presence, positions it for sustained growth in the gastrointestinal therapeutics market.

Gastrointestinal Therapeutics Market in Europe

Europe represents a significant market for gastrointestinal therapeutics, characterized by advanced healthcare systems, strong research initiatives, and an increasing prevalence of digestive disorders. The region's market is driven by substantial investments in healthcare infrastructure, rising adoption of innovative therapeutic solutions, and growing awareness about gastrointestinal diseases. Key countries, including Germany, the United Kingdom, France, Italy, and Spain, demonstrate varying patterns in disease prevalence and treatment approaches. The region's market dynamics are further influenced by robust regulatory frameworks, increasing healthcare expenditure, and a growing focus on personalized medicine approaches.

Gastrointestinal Therapeutics Market in Germany

Germany leads the European gastrointestinal therapeutics market, commanding approximately 23% market share in 2024. The country's dominant position is supported by significant research advancements in gastrointestinal treatments, increasing surveillance, and the rising prevalence of digestive diseases such as inflammatory bowel disease and gut infections. The German market benefits from a strong healthcare infrastructure, substantial investment in research and development, and the presence of major pharmaceutical companies. The country's commitment to innovation in gastrointestinal therapeutics is evident through its numerous research initiatives and clinical trials.

Gastrointestinal Therapeutics Market in France

France demonstrates the highest growth potential in the European region, with a projected CAGR of approximately 5% from 2024-2029. The country's market growth is driven by increasing investments in healthcare infrastructure, a rising prevalence of gastrointestinal disorders, and a growing adoption of innovative therapeutic solutions. France's strong focus on research and development, coupled with favorable healthcare policies and reimbursement frameworks, creates an environment conducive to market expansion. The country's commitment to advancing the gastrointestinal therapeutics market is reflected in its robust clinical research programs and increasing adoption of novel treatment approaches.

Gastrointestinal Therapeutics Market in Asia-Pacific

The Asia-Pacific gastrointestinal drugs market represents a dynamic market for gastrointestinal therapeutics, characterized by rapid healthcare infrastructure development, increasing healthcare expenditure, and growing awareness about digestive disorders. The region encompasses diverse healthcare systems and market dynamics across countries including China, Japan, India, Australia, and South Korea. The market is driven by the large patient population, improving access to healthcare services, and increasing investments in research and development. The region's growth is further supported by rising disposable incomes, expanding healthcare coverage, and a growing adoption of advanced therapeutic solutions.

Gastrointestinal Therapeutics Market in Japan

Japan emerges as the largest market in the Asia-Pacific region, demonstrating a strong market presence through its advanced healthcare infrastructure and significant investments in gastrointestinal research. The country's market is characterized by rising demand for gastrointestinal drugs and an increasing prevalence of gastrointestinal disorders such as irritable bowel syndrome and gastroesophageal reflux disease. Japan's commitment to advancing therapeutic solutions is evident through its robust research programs and innovative drug development initiatives. The country's healthcare system supports widespread access to the gastrointestinal therapeutics market, contributing to market growth.

Gastrointestinal Therapeutics Market in China

China demonstrates remarkable growth potential in the Asia-Pacific region, driven by its large patient population, improving healthcare infrastructure, and increasing investments in pharmaceutical research and development. The country's market is characterized by rising awareness about gastrointestinal diseases, growing healthcare expenditure, and expanding access to innovative therapeutic solutions. China's commitment to advancing healthcare services and an increasing focus on research and development in gastrointestinal therapeutics position it for sustained growth. The country's evolving regulatory landscape and growing domestic pharmaceutical industry further support market expansion.

Gastrointestinal Therapeutics Market in the Middle East and Africa

The Middle East and Africa region presents unique opportunities in the gastrointestinal therapeutics market, characterized by improving healthcare infrastructure and increasing awareness about digestive disorders. The region encompasses diverse healthcare systems across the GCC countries and South Africa, with varying levels of market development and healthcare access. The GCC emerges as the largest market in the region, benefiting from substantial healthcare investments and advanced medical facilities. South Africa demonstrates the fastest growth potential, driven by increasing healthcare accessibility and rising awareness about gastrointestinal diseases. The region's market is supported by government initiatives to improve healthcare services and growing investments in medical infrastructure.

Gastrointestinal Therapeutics Market in South America

South America represents an emerging market for gastrointestinal therapeutics, characterized by increasing healthcare expenditure and growing awareness about digestive disorders. The region's market landscape spans across countries including Brazil and Argentina, with varying levels of healthcare infrastructure and market maturity. Brazil emerges as the largest market in the region, supported by its extensive healthcare system and significant investments in pharmaceutical research. Argentina demonstrates the fastest growth potential, driven by increasing research and development activities and a growing focus on gastrointestinal disease management. The region's market growth is further supported by improving healthcare access and the rising adoption of innovative therapeutic solutions.

Get Analysis on Important Geographic Markets

Download PDF

Gastrointestinal Therapeutics Industry Overview

Top Companies in Gastrointestinal Therapeutics Market

The gastrointestinal therapeutics market is characterized by the strong presence of established pharmaceutical giants, including Abbott Laboratories, AbbVie, AstraZeneca, Bayer AG, GSK, Johnson & Johnson, Pfizer, and Takeda Pharmaceutical. These gastroenterology pharmaceutical companies are actively pursuing product innovation through extensive research and development initiatives, particularly in biologics and targeted therapies for conditions like inflammatory bowel disease and Crohn's disease. Strategic collaborations and licensing agreements have become increasingly prevalent as companies seek to expand their therapeutic portfolios and geographical reach. Companies are also focusing on developing novel drug delivery systems and investing in advanced technologies like nanoparticles and sustained-release formulations to enhance treatment efficacy. The market has witnessed significant investment in digital therapeutics and patient support platforms, demonstrating the industry's commitment to comprehensive care solutions.

Dynamic Market Structure Drives Industry Evolution

The gastrointestinal therapeutics market exhibits a relatively consolidated structure dominated by multinational pharmaceutical conglomerates with diverse product portfolios. These major players leverage their extensive research capabilities, global distribution networks, and strong financial positions to maintain market leadership. The market has witnessed significant merger and acquisition activity, particularly involving innovative biotech companies developing novel therapeutic approaches. Companies like Roche's acquisition of Telavant and strategic partnerships between established players and emerging biotechnology firms highlight the industry's focus on expanding therapeutic capabilities and addressing unmet medical needs.

Regional players and specialized pharmaceutical companies maintain a significant presence in specific therapeutic areas or geographical markets, contributing to the market's competitive dynamics. The emergence of biosimilars has introduced new competitive dimensions, with companies like Boehringer Ingelheim and Cipla expanding their presence in this segment. Private equity investment in gastroenterology practices has increased substantially, leading to consolidation in healthcare delivery and influencing market dynamics. The industry has also seen increased collaboration between pharmaceutical companies and healthcare technology firms to develop integrated treatment solutions.

Innovation and Adaptability Drive Market Success

Success in the gastrointestinal diseases therapeutics market increasingly depends on companies' ability to develop innovative, targeted treatments while maintaining operational efficiency. Market leaders are investing heavily in research and development, focusing on personalized medicine approaches and novel drug delivery systems. Companies are also expanding their digital capabilities, incorporating artificial intelligence and data analytics to enhance drug development and patient care. Building strong relationships with healthcare providers, maintaining robust supply chains, and developing comprehensive patient support programs have become crucial for maintaining market position.

For emerging players and contenders, success lies in identifying and addressing specific unmet needs within the gastrointestinal therapeutics space. This includes developing specialized treatments for rare conditions, improving existing therapeutic approaches, or focusing on specific geographical markets. Regulatory compliance and safety standards continue to play a crucial role in market success, with companies needing to maintain robust quality control systems and pharmacovigilance programs. The increasing focus on value-based healthcare and cost-effectiveness has made it essential for companies to demonstrate both the clinical efficacy and economic benefits of their treatments, while also navigating the complex landscape of healthcare reimbursement and access.

Gastrointestinal Therapeutics Market Leaders

-

Abbvie Inc.

-

AstraZeneca

-

Takeda Pharmaceutical Company Limited

-

Bausch Health Companies Inc. (Salix Pharmaceuticals Inc.)

-

Johnson & Johnson(Janssen Global Services LLC)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Gastrointestinal Therapeutics Market News

• In February 2024, gastrointestinal care startup Salvo Health closed a USD 5 million Seed Prime round led by City Light Capital and Human Ventures. The company offers a virtual care clinic for people with chronic gut issues and will use the funds to expand its reach with providers.

• In March 2024, Johnson & Johnson submitted a supplemental Biologics License Application (sBLA) to the US Food and Drug Administration (FDA) seeking approval of TREMFYA (guselkumab) for the management of adults with moderately to severely active ulcerative colitis (UC).

Gastrointestinal Therapeutics Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Gastrointestinal Diseases

- 4.2.2 Rising Investments in Research and Development by Pharmaceutical Companies

-

4.3 Market Restraints

- 4.3.1 Stringent Regulatory Norms Regarding Drug Approvals

- 4.3.2 Increasing Number of Patent Expiries

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD)

-

5.1 By Drug Type

- 5.1.1 Biologics/ Biosimilars

- 5.1.2 Antacids

- 5.1.3 Laxatives

- 5.1.4 Antidiarrheal agents

- 5.1.5 Antiemetics

- 5.1.6 Antiulcer agents

- 5.1.7 Other Drug Types

-

5.2 By Dosage Form

- 5.2.1 Oral

- 5.2.2 Parenteral

- 5.2.3 Other Dosage Forms

-

5.3 By Application

- 5.3.1 Ulcerative Colitis

- 5.3.2 Irritable Bowel Syndrome

- 5.3.3 Crohn's Disease

- 5.3.4 Celiac Disease

- 5.3.5 Gastroenteritis

- 5.3.6 Other Applications

-

5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

6. COMPANY PROFILES AND COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Abbott

- 6.1.2 Abbvie Inc.

- 6.1.3 AstraZeneca

- 6.1.4 Bayer AG

- 6.1.5 GSK plc

- 6.1.6 Johnson & Johnson(Janssen Global Services LLC)

- 6.1.7 Pfizer Inc.

- 6.1.8 Takeda Pharmaceutical Company Limited

- 6.1.9 Bausch Health Companies Inc. (Salix Pharmaceuticals Inc.)

- 6.1.10 Boehringer Ingelheim International GmbH

- 6.1.11 Cipla Inc.

- 6.1.12 Sebela Pharmaceuticals

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape Covers - Business Overview, Financials, Products and Strategies, and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Gastrointestinal Therapeutics Industry Segmentation

As per the scope of the report, gastrointestinal disorders are medical conditions related to the digestive system that affect the colon, small and large intestine, and rectum. The disorders mainly include constipation, peptic ulcer diseases, and irritable bowel syndrome, characterized by various symptoms such as pain, bloating, diarrhea, nausea, and vomiting.

The gastrointestinal therapeutics market is segmented by drug type, dosage form, application, and geography. The drug type segment is further divided into biologics/ biosimilars, antacids, laxatives, antidiarrheal agents, antiemetics, antiulcer agents, and other drug types. The dosage form is further segmented into oral, parenteral, and other dosage forms. The application is further bifurcated into ulcerative colitis, irritable bowel syndrome, Crohn's disease, celiac disease, gastroenteritis, and other applications. The geography region is further divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for countries across major regions globally. The report offers the value (in USD) for the above segments.

| By Drug Type | Biologics/ Biosimilars | ||

| Antacids | |||

| Laxatives | |||

| Antidiarrheal agents | |||

| Antiemetics | |||

| Antiulcer agents | |||

| Other Drug Types | |||

| By Dosage Form | Oral | ||

| Parenteral | |||

| Other Dosage Forms | |||

| By Application | Ulcerative Colitis | ||

| Irritable Bowel Syndrome | |||

| Crohn's Disease | |||

| Celiac Disease | |||

| Gastroenteritis | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Gastrointestinal Therapeutics Market Research FAQs

How big is the Gastrointestinal Therapeutics Market?

The Gastrointestinal Therapeutics Market size is expected to reach USD 41.94 billion in 2025 and grow at a CAGR of 4.34% to reach USD 51.87 billion by 2030.

What is the current Gastrointestinal Therapeutics Market size?

In 2025, the Gastrointestinal Therapeutics Market size is expected to reach USD 41.94 billion.

Who are the key players in Gastrointestinal Therapeutics Market?

Abbvie Inc., AstraZeneca, Takeda Pharmaceutical Company Limited, Bausch Health Companies Inc. (Salix Pharmaceuticals Inc.) and Johnson & Johnson(Janssen Global Services LLC) are the major companies operating in the Gastrointestinal Therapeutics Market.

Which is the fastest growing region in Gastrointestinal Therapeutics Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Gastrointestinal Therapeutics Market?

In 2025, the North America accounts for the largest market share in Gastrointestinal Therapeutics Market.

What years does this Gastrointestinal Therapeutics Market cover, and what was the market size in 2024?

In 2024, the Gastrointestinal Therapeutics Market size was estimated at USD 40.12 billion. The report covers the Gastrointestinal Therapeutics Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Gastrointestinal Therapeutics Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Gastrointestinal Therapeutics Market Research

Mordor Intelligence provides a comprehensive analysis of the gastrointestinal therapeutics market. We leverage our extensive expertise in gastroenterology market research and consulting. Our detailed report examines the evolving landscape of GI therapy solutions. It covers developments across the Americas gastrointestinal drug market, Asia-Pacific gastrointestinal drugs market, and Europe, Middle East and Africa gastrointestinal drugs market. The analysis includes various therapeutic areas, such as chronic gastritis drugs and the digestive medication market segments. Stakeholders can access crucial insights in an easy-to-read report PDF format available for download.

The report offers invaluable insights for gastroenterology pharmaceutical companies and industry stakeholders. It examines key trends in gastrointestinal diseases drug development and therapeutic innovations. Our comprehensive coverage includes a detailed analysis of gastrointestinal therapeutics diagnostics solutions. We also explore visceral pain associated with GI disorders and emerging treatment paradigms. Stakeholders benefit from our thorough examination of digestive distress treatment options, lower GI series market developments, and gastrointestinal diseases therapeutics advancements. This is supported by robust data analysis and future market projections.