| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 15.66 Billion |

| Market Size (2030) | USD 18.42 Billion |

| CAGR (2025 - 2030) | 3.30 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Gas Turbine MRO Market Analysis

The Gas Turbine MRO Market In The Power is expected to grow from USD 15.66 billion in 2025 to USD 18.42 billion by 2030, at a CAGR of 3.3% during the forecast period (2025-2030).

The gas turbine maintenance industry is experiencing significant transformation driven by the aging infrastructure of existing power plants worldwide. As of 2020, approximately 77 GW of global gas-fired power plant capacity is over 50 years old, while more than 672 GW of operating gas turbine installed capacity is less than ten years old, creating a diverse maintenance landscape. This aging fleet requires increasingly sophisticated gas turbine services, repair, and overhaul services to maintain operational efficiency and meet stringent environmental standards. The industry is witnessing a shift toward predictive maintenance strategies and digital solutions, with major service providers incorporating advanced diagnostics and monitoring systems into their service offerings.

The global power generation landscape is undergoing a fundamental transition from coal to natural gas-based power generation, driven by environmental regulations and efficiency requirements. Natural gas power generation capacity is projected to expand from 1,839 GW in 2020 to approximately 2,414 GW by 2050, indicating substantial long-term growth potential for gas turbine maintenance services. This transition is particularly evident in developed markets where stringent emission regulations are accelerating the retirement of coal-fired plants and their replacement with modern gas turbine facilities. The industry is seeing increased adoption of advanced MRO technologies and service agreements that focus on optimizing performance while reducing environmental impact.

The integration of gas turbine operations with renewable energy sources is reshaping maintenance requirements and operational strategies. Power plants are increasingly required to operate flexibly to accommodate intermittent renewable energy sources, leading to new challenges in maintenance scheduling and component wear patterns. This trend is driving innovation in gas turbine services, with providers developing specialized maintenance programs for flexible operation scenarios. Service providers are expanding their capabilities to handle the complex maintenance requirements of hybrid power systems that combine gas turbines with renewable energy sources.

The market is witnessing substantial infrastructure development, particularly in emerging economies. As of 2021, significant gas-fired power plant capacity is under development across Asia, with China leading at 91 GW, followed by Vietnam with 56 GW, and South Korea with 20 GW of proposed capacity. This expansion is driving the evolution of MRO service networks, with providers establishing regional service centers and developing localized capabilities. The industry is seeing increased emphasis on long-term service agreements and comprehensive maintenance solutions that can support both new and existing infrastructure while ensuring optimal performance and reliability throughout the equipment lifecycle. This growth is further supported by advancements in industrial gas turbine maintenance and power plant asset management, which are critical for sustaining the operational efficiency of these new installations.

Gas Turbine MRO Market Trends

Aging Fleet of Gas Power Plants and Regular Maintenance Requirements

The substantial installed base of aging gas turbines across global power plants necessitates regular gas turbine maintenance and overhaul services to ensure optimal performance and reliability. As of 2023, a significant portion of the global gas-fired power plant fleet has been in operation for over two decades, with approximately 77 GW of capacity being more than 50 years old. These aging facilities require more frequent maintenance interventions, with industry standards recommending three quarterly inspections followed by comprehensive annual inspections during the first two years of operation. This maintenance schedule becomes even more critical as turbines age, requiring additional specialized gas turbine services, including component repairs, diagnostic assessments, and potential upgrades to maintain operational efficiency.

The complexity of modern gas turbines and their critical role in power generation demand stringent maintenance protocols to prevent unexpected outages and ensure stable operations. Power plant operators must adhere to manufacturer-recommended maintenance schedules that include periodic inspections, parts replacement, diagnostics, and renovations to improve operational performance and ensure long-term stability. These maintenance requirements are further intensified by the high-temperature and high-pressure operating conditions of gas turbines, which accelerate component wear and necessitate regular monitoring and servicing. The industry's focus on preventive maintenance has led to the development of sophisticated monitoring systems and predictive maintenance approaches, enabling operators to optimize their maintenance schedules and extend equipment life while maintaining performance standards.

Understand The Key Trends Shaping This Market

Download PDF

Growing Shift from Coal to Gas-based Power Generation

The global energy sector is experiencing a significant transition from coal-based to gas-based power generation, driven by environmental concerns and the need for cleaner energy sources. Natural gas power plants offer superior environmental performance compared to coal-fired facilities, with significantly lower emissions of greenhouse gases and other pollutants. This transition is particularly evident in major economies where governments are implementing stringent emission regulations and clean energy policies. For instance, the United States has witnessed substantial coal plant retirements, with approximately 59 GW of coal-fired capacity expected to be retired by 2035, creating opportunities for gas turbine installations and subsequent MRO services.

The clean fuel properties of natural gas have made it an attractive transition fuel for countries working towards their carbon reduction goals. This shift is particularly pronounced in regions with established gas infrastructure and supply chains, where power utilities are converting existing coal-fired plants to gas-fired facilities or building new gas-based power plants. The transition requires not only new turbine installations but also comprehensive maintenance and operational support services to ensure optimal performance and reliability. The increasing focus on operational flexibility and grid stability has further emphasized the importance of well-maintained gas turbine facilities, as they play a crucial role in supporting renewable energy integration and meeting variable power demand patterns.

Long-term Service Agreements (LTSAs) and Strategic Partnerships

The power generation industry has witnessed a growing trend toward comprehensive long-term service agreements (LTSAs) between power plant operators and service providers, reflecting the complex maintenance requirements of modern gas turbines. These agreements typically encompass a wide range of services, including fleet management, inventory management, maintenance, repair, overhaul, and day-to-day technical support. The adoption of LTSAs helps power utilities optimize their operational costs while ensuring consistent performance and reliability of their gas turbine assets. These agreements often span 15-20 years, providing stability for both service providers and power plant operators while enabling planned maintenance schedules and predictable cost structures.

The strategic importance of LTSAs is evidenced by recent industry developments and partnerships between major power producers and service providers. These agreements have evolved to include advanced digital solutions, remote monitoring capabilities, and performance optimization services, reflecting the industry's movement toward more sophisticated maintenance approaches. The comprehensive nature of modern LTSAs extends beyond basic maintenance to include technology upgrades, performance guarantees, and operational optimization services, helping power plants maintain competitive efficiency levels throughout their operational lifecycle. These partnerships also facilitate knowledge transfer and technical expertise sharing, enabling power plant operators to benefit from the latest technological advancements and best practices in gas turbine maintenance.

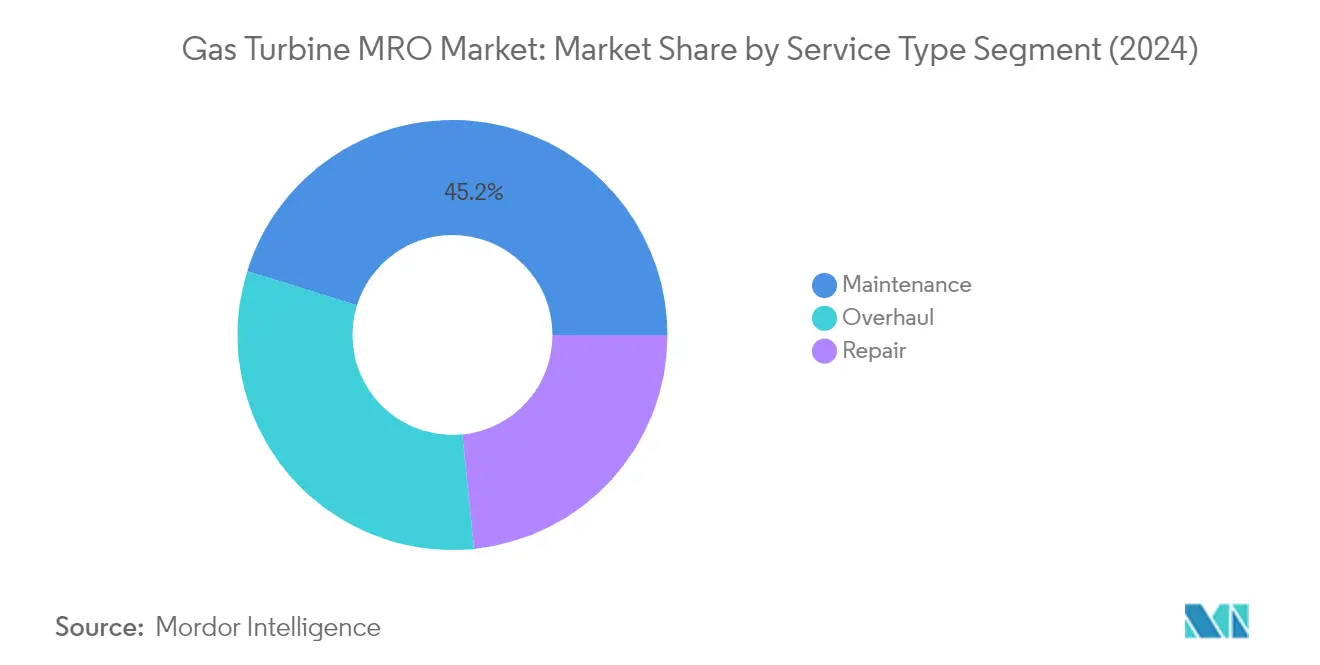

Segment Analysis: Service Type

Maintenance Segment in Gas Turbine MRO Market

The maintenance segment dominates the gas turbine MRO market, commanding approximately 45% of the total market share in 2024. This significant market position is driven by the critical need for regular gas turbine maintenance services to ensure optimal performance and reliability of gas turbines in power plants. Power utilities and independent power producers increasingly rely on long-term service agreements (LTSAs) to meet their comprehensive plant requirements, including fleet management, inventory management, and day-to-day technical support. The segment's dominance is further reinforced by industry recommendations for performing three quarterly inspections followed by annual inspections, particularly for new installations in their first two years of operation. These agreements help reduce overall costs while enhancing turbine capacity through higher performance parts, making gas turbine maintenance services an essential component of gas turbine operations.

Repair Segment in Gas Turbine MRO Market

The repair segment is projected to experience substantial growth from 2024 to 2029, driven by the increasing complexity of gas turbine components and the rising need for specialized gas turbine repair services. This growth is supported by the expanding base of gas-fired power plants globally and the aging infrastructure requiring more frequent repairs. Independent repair facilities continue to gain prominence as operators seek cost-effective alternatives to OEM services. The segment's growth is further bolstered by advancements in gas turbine component repair technologies and techniques, including component repair programs that minimize maintenance costs while maximizing equipment availability. The increasing focus on extending the operational life of existing gas turbines through timely repairs and the growing demand for specialized repair services for critical components like nozzles, rotor blades, compressors, and combustors contribute to the segment's rapid expansion.

Remaining Segments in Service Type

The overhaul segment plays a crucial role in the gas turbine MRO market by providing comprehensive maintenance solutions for aging power generation equipment. This segment focuses on complete system renovations, including gas turbine disassembly, rotor removal, clearance measurements, blade inspection and replacement, and inspection of main gearbox components. Overhaul services are particularly important for power plants reaching critical operational milestones, typically required after 48,000 firing hours. The segment's significance is enhanced by the increasing need for modernization and efficiency improvements in existing gas turbine installations, as well as the growing emphasis on extending equipment lifecycle through thorough gas turbine overhaul services.

Segment Analysis: Provider Type

OEM Segment in Gas Turbine MRO Market

Original Equipment Manufacturers (OEMs) dominate the gas turbine MRO market due to their unique competitive advantages and comprehensive service capabilities. These providers benefit from having direct access to original designs, engineering expertise, and proprietary technology that gives them significant leverage in the market. OEMs like General Electric, Siemens Energy, and Mitsubishi Power offer faster response times, seamless access to original replacement parts, and superior quality assurance backed by the engineers who originally designed the turbines. Their dominance is further strengthened by long-term service agreements (LTSAs) that are typically secured during initial gas turbine installations, providing them with a steady stream of MRO contracts. The complexity of gas turbines, particularly related to high temperatures, pressures, and intricate cooling schemes, makes it challenging for other players to replicate OEM-level services at scale.

Independent Service Provider Segment in Gas Turbine MRO Market

Independent Service Providers (ISPs) are experiencing rapid growth in the gas turbine MRO market by offering cost-effective alternatives to OEM services. These providers are gaining market share by delivering maintenance, service, and overhaul support across multiple brands and models, providing customers with greater flexibility in their maintenance strategies. ISPs have become increasingly attractive to power plant operators by offering potential cost savings of approximately 25% to 40% compared to OEM service agreements. Their growth is driven by their ability to provide customized solutions, work across various equipment brands, and offer more flexible service options compared to the one-size-fits-all approach typically employed by OEMs. The segment's expansion is further supported by their capability to service both onshore and offshore equipment, regardless of the original manufacturer.

Remaining Segments in Provider Type

The in-house service provider segment represents a significant component of the gas turbine MRO market, offering power plant operators direct control over their maintenance operations. This segment is characterized by power utilities and independent power producers maintaining their own service teams to handle fleet management, inventory control, and day-to-day technical support. In-house providers offer advantages such as 24/7 availability, immediate response capabilities, and reduced management costs since the plant operator utilizes existing employees for MRO services. While this segment handles many basic MRO services, it often relies on OEMs or ISPs for more complex repairs and overhaul services due to the specialized technical expertise and equipment required for such operations.

Gas Turbine MRO Market in the Power Sector Geography Segment Analysis

Gas Turbine MRO Market in North America

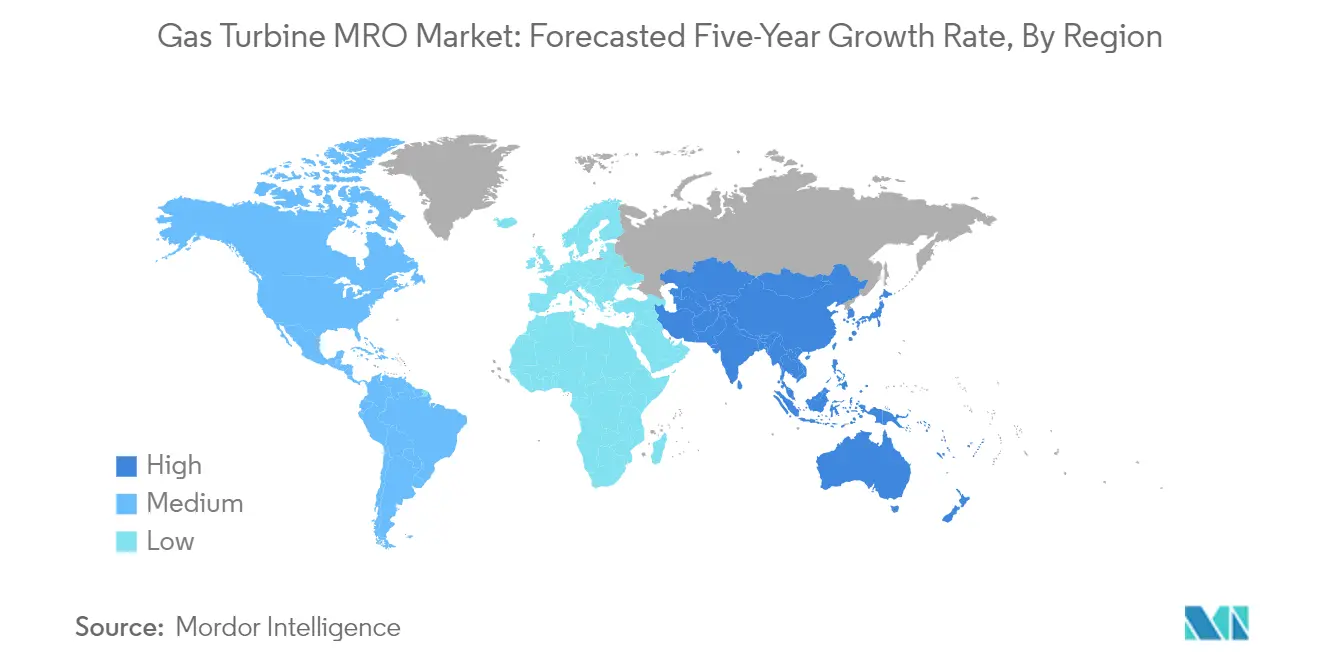

North America represents the largest market for gas turbine services in the power sector, commanding approximately 41% of the global market share in 2024. The region's dominance is primarily driven by its extensive fleet of aging gas turbines and the ongoing transition from coal to gas-based power generation. The United States leads the regional market, characterized by sophisticated maintenance infrastructure and stringent regulatory requirements for power plant operations. The region's strong focus on operational efficiency and reliability has fostered a robust ecosystem of both OEM and independent service providers. The presence of major industry players, advanced technological capabilities, and well-established service networks further strengthens North America's position. Additionally, the region's emphasis on reducing greenhouse gas emissions continues to drive investments in gas-based power generation, creating sustained demand for gas turbine maintenance services. The market is also characterized by increasing adoption of predictive maintenance technologies and long-term service agreements, reflecting the sophisticated nature of the regional market.

Gas Turbine MRO Market in Europe

Europe has demonstrated steady growth in the gas turbine maintenance market, registering approximately 4% annual growth from 2019 to 2024. The region's market is characterized by a strong shift from coal-fired to gas-based power generation, particularly in Western European countries. The market dynamics are shaped by stringent environmental regulations and the region's commitment to reducing carbon emissions. Germany, Italy, and the United Kingdom are the key markets, each with distinct characteristics and requirements for MRO services. The region's focus on energy security and grid stability has led to increased investment in gas turbine services and optimization. European operators are increasingly adopting advanced maintenance techniques and digital solutions to enhance operational efficiency. The presence of major OEMs and their extensive service networks has created a competitive market environment. The region's emphasis on technological innovation and sustainability continues to drive the evolution of MRO services, with a growing focus on efficiency improvements and emissions reduction.

Gas Turbine MRO Market in Asia-Pacific

The Asia-Pacific gas turbine MRO market is poised for robust growth, with an expected annual growth rate of approximately 3% during the 2024-2029 period. The region represents a dynamic market driven by rapid industrialization and increasing power demand across major economies. China, Japan, and India are the primary markets, each contributing significantly to regional growth. The market is characterized by a mix of new installations requiring regular maintenance and an aging fleet requiring comprehensive gas turbine repair services. The region's diverse energy landscape and varying regulatory requirements create unique opportunities for MRO service providers. Local service capabilities are expanding, with increasing investments in maintenance infrastructure and technical expertise. The market is witnessing a gradual shift towards more sophisticated maintenance approaches, including predictive maintenance and digital solutions. Growing emphasis on operational efficiency and reliability is driving the adoption of comprehensive maintenance programs and long-term service agreements.

Gas Turbine MRO Market in South America

The South American gas turbine MRO market represents a growing opportunity within the global landscape, driven by the region's increasing adoption of natural gas for power generation. Brazil and Argentina lead the regional market, with their substantial gas-fired power generation capacity requiring regular maintenance and overhaul services. The market is characterized by a mix of both OEM and independent service providers, offering various maintenance solutions to meet diverse customer needs. The region's focus on energy security and grid reliability has led to increased attention to maintenance practices and operational efficiency. Local service capabilities are developing, though the market still relies significantly on international expertise for complex maintenance operations. The region's economic dynamics and energy policies play crucial roles in shaping maintenance strategies and investment decisions. The market shows potential for growth as countries continue to expand their gas-based power generation capacity and modernize existing facilities.

Gas Turbine MRO Market in Middle East & Africa

The Middle East & Africa region presents a significant market for gas turbine services, driven by its substantial gas-fired power generation capacity and continued investments in power infrastructure. The Middle East, particularly the GCC countries, leads the regional market with its extensive fleet of gas turbines requiring regular maintenance and overhaul services. The region's harsh operating conditions necessitate specialized maintenance approaches and more frequent service intervals. Local service capabilities are expanding, with increasing investments in maintenance facilities and technical expertise. The market is characterized by a strong presence of both international OEMs and regional service providers. Africa represents an emerging opportunity, with growing investments in gas-based power generation creating new demand for MRO services. The region's focus on power sector reliability and efficiency continues to drive the adoption of comprehensive maintenance programs and advanced service solutions. The market benefits from the region's strategic focus on energy sector development and modernization initiatives.

Get Analysis on Important Geographic Markets

Download PDF

Gas Turbine MRO Industry Overview

Top Companies in Gas Turbine MRO Market

The gas turbine services market features prominent players like General Electric, Siemens Energy, Mitsubishi Heavy Industries, Solar Turbines, and Doosan Heavy Industries leading the industry through continuous innovation and strategic initiatives. These companies are focusing on developing comprehensive service portfolios that include preventative maintenance, predictive diagnostics, and digital solutions for remote monitoring. The market leaders are expanding their geographical footprint through strategic partnerships and service agreements with power generation companies across different regions. Companies are investing in advanced technologies and skilled workforce development to enhance their service capabilities and reduce turbine downtime. The competitive landscape is characterized by long-term service agreements, typically ranging from five to twenty-five years, demonstrating the emphasis on building lasting customer relationships and ensuring consistent revenue streams.

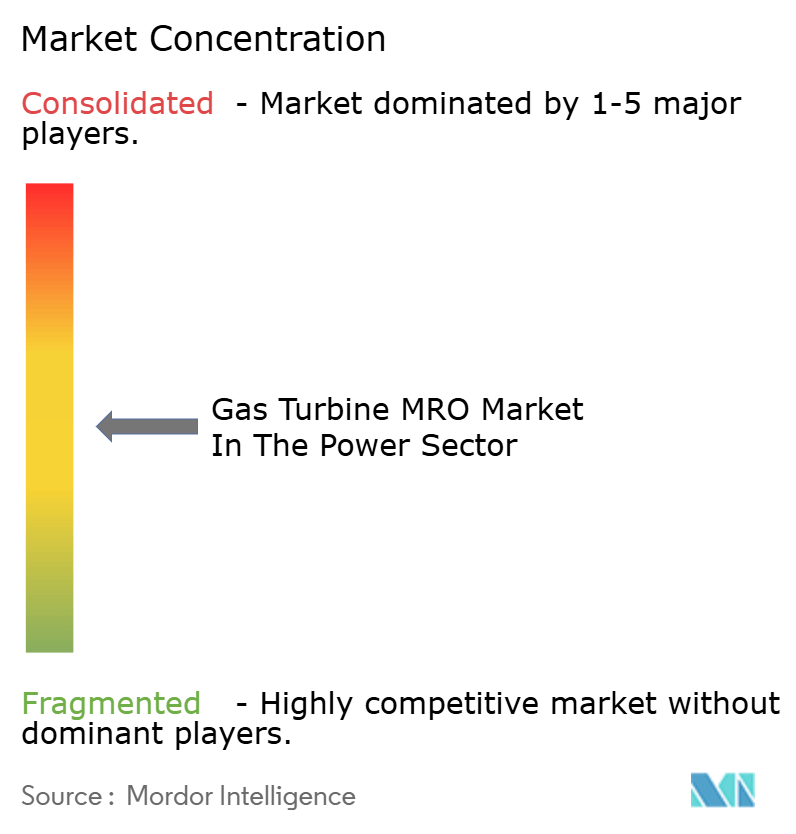

Consolidated Market with Strong Global Players

The gas turbine MRO market exhibits a moderately consolidated structure dominated by large multinational conglomerates with integrated operations across the power generation value chain. These major players leverage their original equipment manufacturing capabilities, extensive service networks, and technological expertise to maintain their market positions. The market features a mix of OEM service providers, independent service providers, and in-house maintenance teams, with OEMs holding a significant advantage due to their proprietary technology and authentic spare parts access. The industry witnesses regular strategic collaborations, particularly between regional service providers and global OEMs, to enhance service delivery capabilities and expand market reach.

The market demonstrates strong regional variations in competitive dynamics, with different players holding dominant positions in specific geographical areas based on their historical presence and established relationships with power generation companies. Merger and acquisition activities are primarily focused on acquiring specialized service capabilities, expanding geographical presence, and integrating digital technologies into service offerings. The competitive intensity is further shaped by the increasing presence of independent service providers who compete through competitive pricing and flexible service options, particularly in mature markets.

Innovation and Flexibility Drive Future Success

Success in the gas turbine MRO market increasingly depends on providers' ability to offer comprehensive digital solutions, flexible service agreements, and innovative maintenance approaches. Market players must invest in developing predictive maintenance capabilities, remote monitoring systems, and data analytics to meet evolving customer expectations for reduced downtime and improved operational efficiency. The ability to provide customized service packages, rapid response times, and cost-effective solutions while maintaining high-quality standards will be crucial for both established players and new entrants. Companies need to focus on building strong relationships with power generation companies while developing specialized expertise in handling different turbine technologies and configurations.

The competitive landscape is evolving with increasing emphasis on environmental regulations and the transition towards cleaner energy sources. Service providers must adapt their offerings to support the maintenance and optimization of gas turbines operating in flexible power generation scenarios. Success factors include developing specialized expertise in maintaining advanced turbine technologies, building strong supply chain networks for spare parts, and maintaining a skilled workforce. Market players need to balance between standardization of services for cost efficiency and customization to meet specific customer requirements, while also considering the increasing focus on sustainability and emissions reduction in the power generation sector. The integration of gas turbine maintenance and power plant asset management is becoming increasingly vital for optimizing operational efficiency and sustainability.

Gas Turbine MRO Market Leaders

-

General Electric Company

-

Siemens Energy AG

-

Mitsubishi Heavy Industries Ltd.

-

Sulzer Ltd

-

Solar Turbines Incorporated

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Gas Turbine MRO Market News

- March 2024: an agreement was signed between OEM GE Marine and TEI to provide depot-level maintenance and overhaul services for the LM2500 Gas turbine engines used by the U.S. Navy at TEI facilities during this 14-month period under an agreement that runs through October 2026.

- February 2024: MTU Power extended its contract with Norway’s Equinor ASA, Europe’s largest operator of offshore oil and gas platforms and second-largest supplier of gas. The contract covers the maintenance, repair, and overhaul (MRO) of its LM-series industrial gas turbines (IGTs) until 2028.

Gas Turbine MRO Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Study Assumptions

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

-

4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 The Aging Gas Turbine Fleet in the Long-Serving Power Plants

- 4.5.1.2 Reliability Requirements with Regard to Turbomachinery

- 4.5.2 Restraints

- 4.5.2.1 Growth in the Renewable Energy Sector

- 4.6 Supply Chain Analysis

-

4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5. MARKET SEGMENTATION

-

5.1 Service Type

- 5.1.1 Maintenane

- 5.1.2 Repair

- 5.1.3 Overhaul

-

5.2 Provider Type (Qualitative Analysis Only)

- 5.2.1 OEMs

- 5.2.2 Independent Service Providers

- 5.2.3 In-house

-

5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States of America

- 5.3.1.2 Canda

- 5.3.1.3 Rest of the North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Rest of the Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Rest of the Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of the South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of the Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

-

6.3 Company Profiles

- 6.3.1 General Electric Company

- 6.3.2 Mitsubishi Heavy Industries Ltd.

- 6.3.3 RWG (Repair & Overhauls) Limited

- 6.3.4 Metalock Engineering Group

- 6.3.5 Goltens Worldwide Management Corporation

- 6.3.6 Siemens Energy AG

- 6.3.7 Sulzer Ltd

- 6.3.8 Doosan Heavy Industries and Construction

- 6.3.9 Solar Turbines Incorporated

- 6.3.10 Ethos Energy LLC

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Shift From Coal to Gas-Based Power Generation

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Gas Turbine MRO Industry Segmentation

Gas Turbine MRO (Maintenance, Repair, and Overhaul) refers to the comprehensive services provided to ensure the optimal performance and longevity of gas turbines. These services include routine maintenance, troubleshooting, repairs, and complete overhauls. The goal is to maintain efficiency, prevent unexpected failures, and extend the operational life of the turbines. MRO activities are critical in industries such as power generation, aviation, and oil and gas, where gas turbines play a pivotal role.

The gas turbine MRO market is segmented by service type, provider type, and geography. By service type, the market is segmented into maintenance, repair, and overhaul. By provider type, the market is segmented by OEMs, independent service providers, and in-house. The report also covers the market size and forecasts for the gas turbine MRO market in the power sector across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Service Type | Maintenane | ||

| Repair | |||

| Overhaul | |||

| Provider Type (Qualitative Analysis Only) | OEMs | ||

| Independent Service Providers | |||

| In-house | |||

| Geography | North America | United States of America | |

| Canda | |||

| Rest of the North America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of the Europe | |||

| Asia-Pacific | India | ||

| China | |||

| Japan | |||

| Rest of the Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of the South America | |||

| Middle-East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| Rest of the Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Gas Turbine MRO Market Research FAQs

How big is the Gas Turbine MRO Market In The Power?

The Gas Turbine MRO Market In The Power size is expected to reach USD 15.66 billion in 2025 and grow at a CAGR of 3.30% to reach USD 18.42 billion by 2030.

What is the current Gas Turbine MRO Market In The Power size?

In 2025, the Gas Turbine MRO Market In The Power size is expected to reach USD 15.66 billion.

Who are the key players in Gas Turbine MRO Market In The Power?

General Electric Company, Siemens Energy AG, Mitsubishi Heavy Industries Ltd., Sulzer Ltd and Solar Turbines Incorporated are the major companies operating in the Gas Turbine MRO Market In The Power.

Which is the fastest growing region in Gas Turbine MRO Market In The Power?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Gas Turbine MRO Market In The Power?

In 2025, the North America accounts for the largest market share in Gas Turbine MRO Market In The Power.

What years does this Gas Turbine MRO Market In The Power cover, and what was the market size in 2024?

In 2024, the Gas Turbine MRO Market In The Power size was estimated at USD 15.14 billion. The report covers the Gas Turbine MRO Market In The Power historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Gas Turbine MRO Market In The Power size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Gas Turbine MRO Market In The Power Sector Research

Mordor Intelligence offers a comprehensive analysis of the gas turbine services industry. With decades of expertise in power sector research, our detailed report examines the full range of gas turbine maintenance activities. This includes the supply chains of gas turbine spare parts and strategies for thermal power plant maintenance. The analysis also covers power plant asset management solutions, focusing on industrial gas turbine maintenance practices and emerging technological innovations. Available as an easy-to-read report PDF for download, this research provides in-depth insights into gas turbine repair services and evolving industry dynamics.

Stakeholders gain valuable intelligence on gas turbine overhaul services trends and operational optimization strategies for combined cycle power plant maintenance. The report delivers actionable insights on gas turbine component repair methodologies and gas turbine retrofit opportunities. This enables informed decision-making for service providers and facility operators. Our analysis of power plant maintenance services includes detailed case studies, competitive landscape evaluation, and future market projections. It is an essential tool for industry professionals aiming to enhance their strategic planning and operational efficiency in the gas turbine services market.