Market Trends of Gabon Oil and Gas Industry

This section covers the major market trends shaping the Gabon Oil & Gas Market according to our research experts:

Upstream Sector to Drive the Oil and Gas Market

According to OPEC's World-proven oil reserves, there are more than 2 billion barrels of offshore and onshore reserves in Gabon, primarily located in South West of Gabon. This predicts a potential market for development, particularly for upstream oil and gas companies.

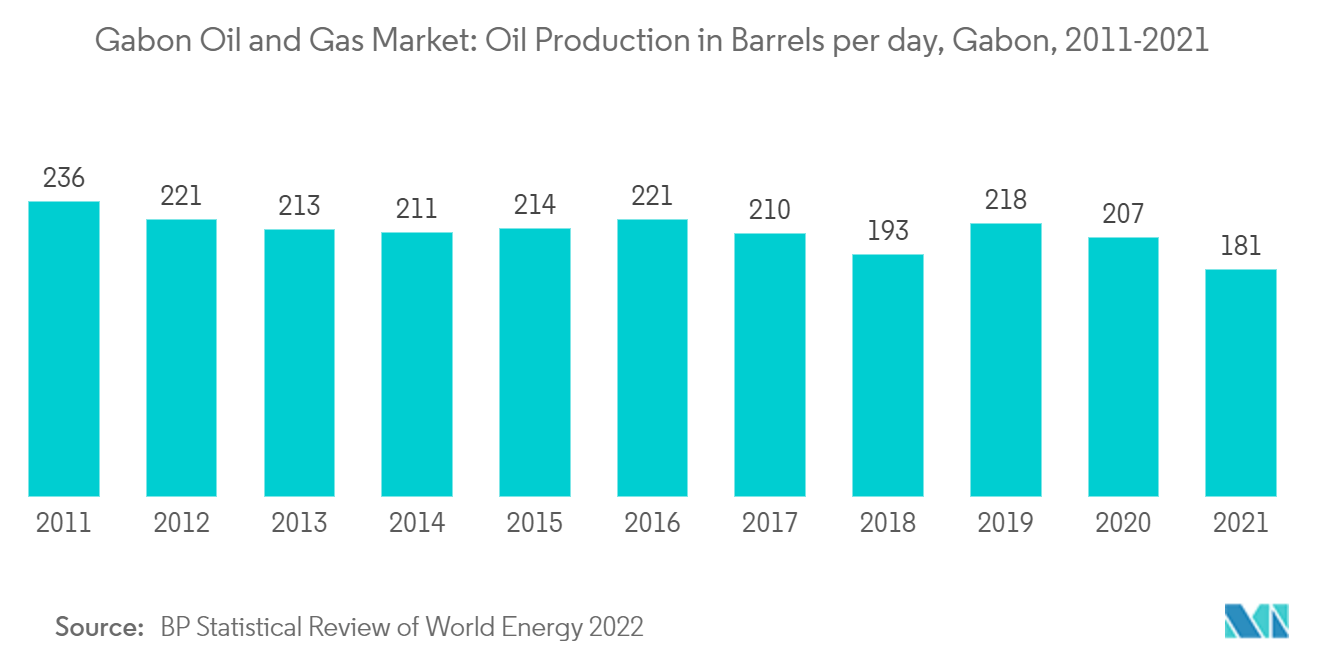

In 2021, with 30 oilfields in production, Gabon was the eighth-largest oil-producing country in Africa. However, most of the fields have been declining, which has led to a drop in oil production from 236 thousand barrels in 2011 to 181 thousand barrels in 2021. With the 12th offshore license distribution for deepwater projects backed up by the new hydrocarbon code, the interest of major oil and gas companies has been observed in recent years. These companies are expected to make large-scale investments during the forecast period. In November 2022, BW Energy started preparing to kick off a drilling campaign in the country's offshore Hibiscus and Ruche fields. The project is on track for the first oil in the late first quarter of 2023.

Therefore, huge reserves of proved oil reserves and updated policies are anticipated to boost the growth of the upstream sector, assisting in achieving the aim to increase oil production by 50% in the near future.

Updated Hydrocarbon Code and Upcoming Projects to Drive the Market

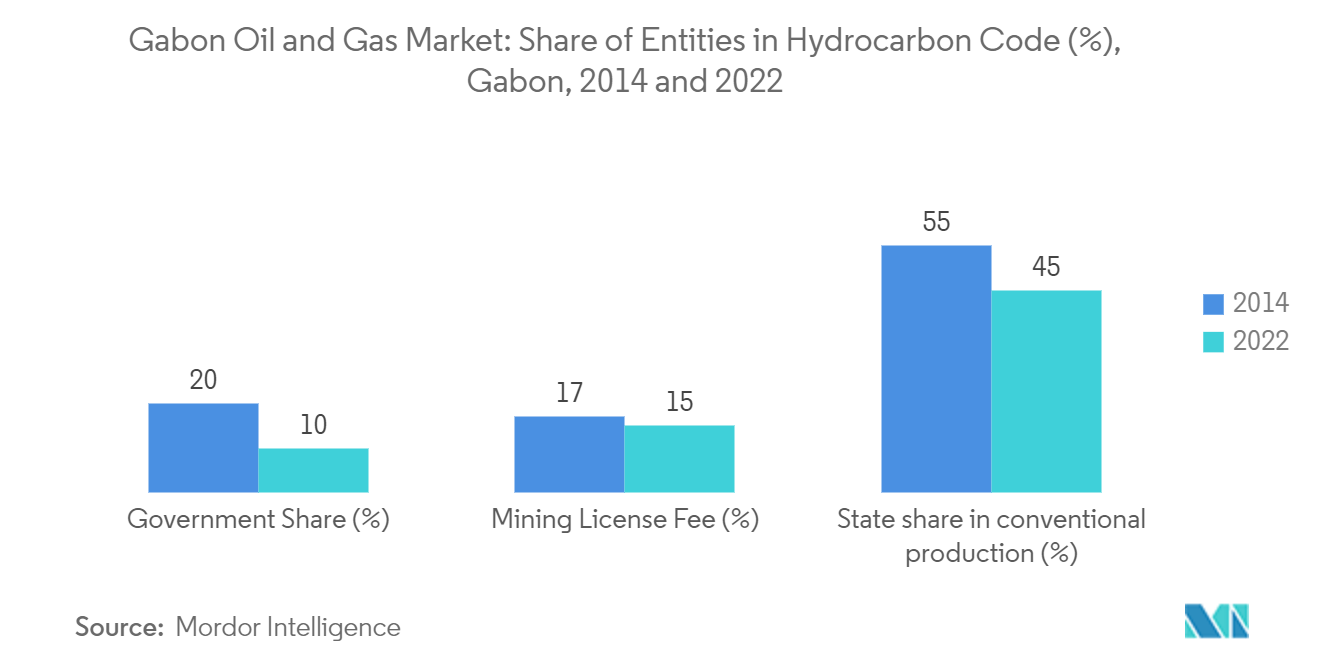

The oil and gas market accounted for a significant share of Gabon's GDP and export earnings. Diminishing production and the oil price resulted in lower investment in the oil and gas sector, resulting in the implementation of the new hydrocarbon code.

In July 2018, Gabon implemented a new Hydrocarbon code with significant updates to lure investments from the international market. Even with decreasing oil and gas prices and changes in contract share and contract tenure, the government continued with the same policy in 2022.

The state's participation has been reduced to 10% during the development and exploitation phase, in addition to a possible 10% acquisition at the market price of shares in any oil and gas producer's share capital.

However, there has been no new licensing round since the 12th Licensing Round in November 2018, slightly restraining the market's growth.

Therefore, due to favorable market conditions and the presence of huge reserves, the oil and gas sector is anticipated to witness investment and growth during the forecast period.