Furniture And Home Furnishing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2025) | USD 1 Trillion |

| Market Size (2030) | USD 1.43 Trillion |

| Growth Rate (2026 - 2031) | 7.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Furniture And Home Furnishing Market Analysis by Mordor Intelligence

The furniture and home furnishing market size stands at USD 1.00 trillion in 2026 and is projected to reach USD 1.43 trillion by 2031 at a 7.39% CAGR, reflecting a clear acceleration from the 2019 to 2024 trajectory. This shift follows normalization of post-pandemic demand patterns, a durable pivot to hybrid work, and sustained investment in omnichannel capabilities that lift reach and conversion across formats. Leading manufacturers and retailers are scaling smaller format stores, deepening in-store planning services, and expanding last-mile capacity to reduce returns and delivery costs in categories with bulky logistics. Procurement strategies are adapting to tariff exposure and supply volatility across wood, steel, aluminum, and critical components, with some companies nearshoring or dual sourcing to maintain service levels. Select operators are balancing these pressures with pricing actions and disciplined capital allocation to fund expansion where digital and physical channels reinforce one another.

Key Report Takeaways

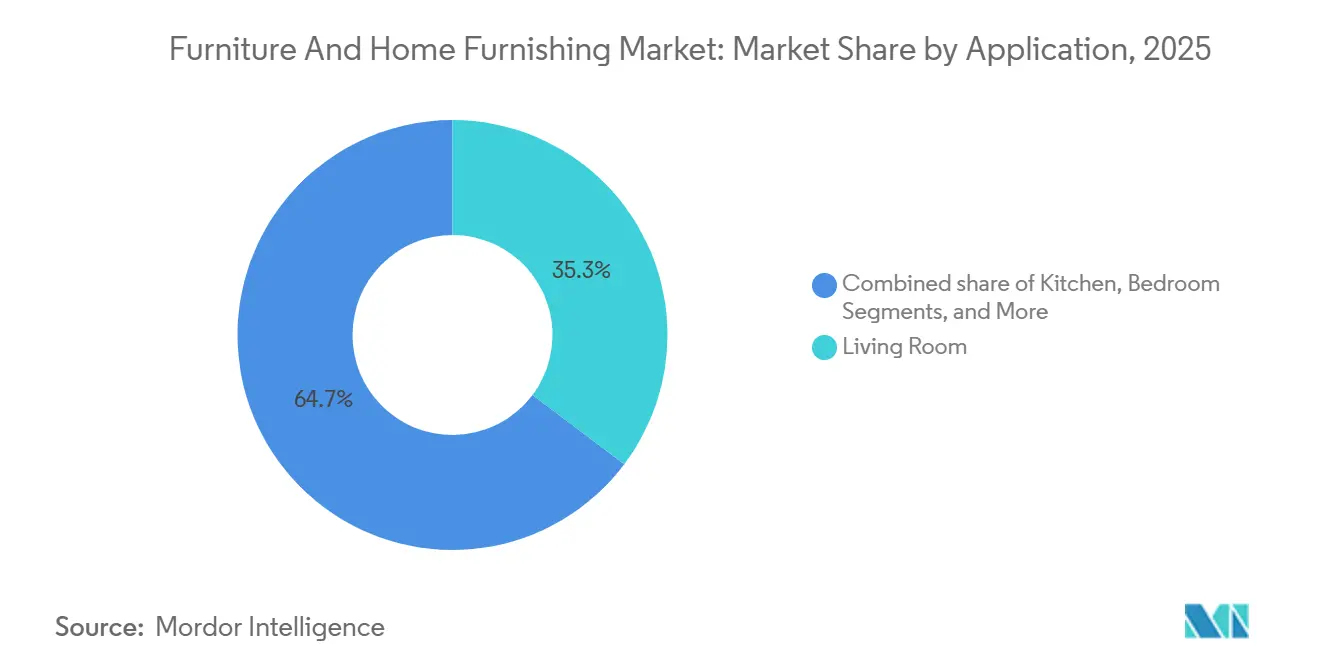

- By application, Living Room led with 35.26% of the furniture and home furnishing market share in 2025, while Outdoor is projected to expand at an 8.12% CAGR through 2031, emphasizing the resilience of indoor anchors and the durability of post-pandemic outdoor living upgrades.

- By material, Wood held a dominant 46.61% of the furniture and home furnishing market share in 2025, while Plastic is forecast to post the fastest 8.36% CAGR to 2031 as recycled-content mandates and weather-resistant outdoor use cases gather momentum.

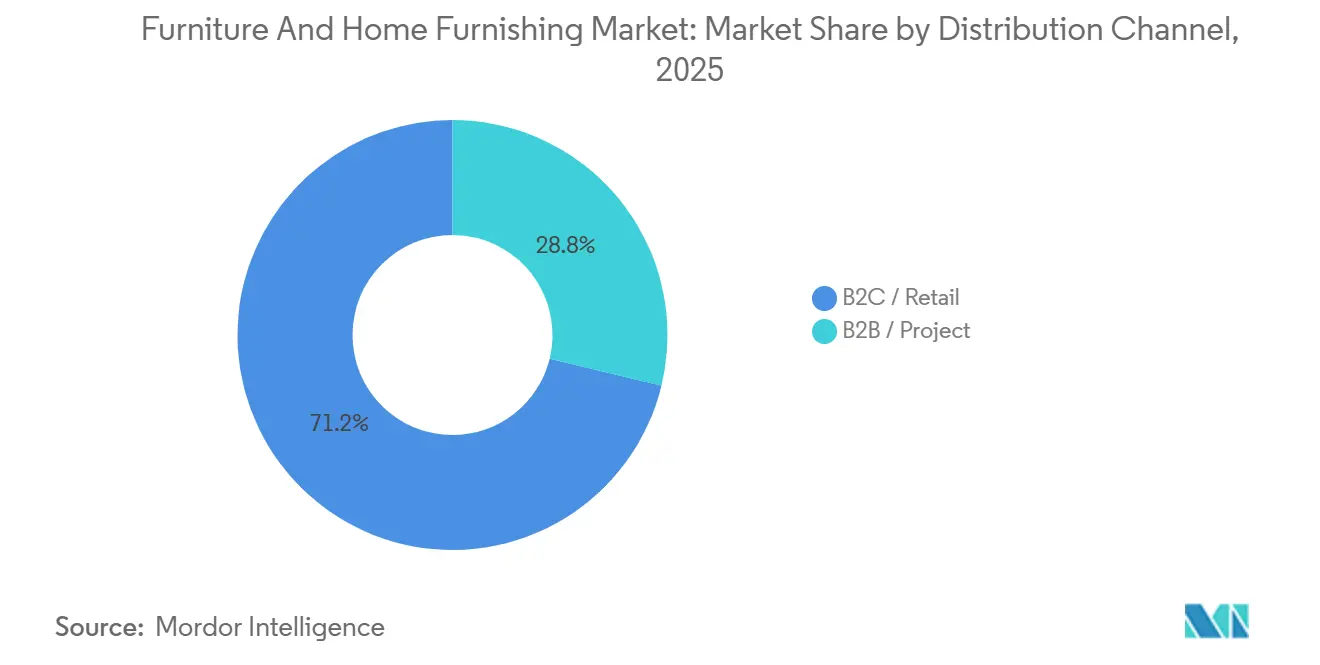

- By distribution channel, B2C/Retail captured 71.15% of the furniture and home furnishing market share in 2025 sales, while B2B/Project is the fastest-growing at a 7.25% CAGR, aligned to hybrid office retrofits and institutional purchasing cycles.

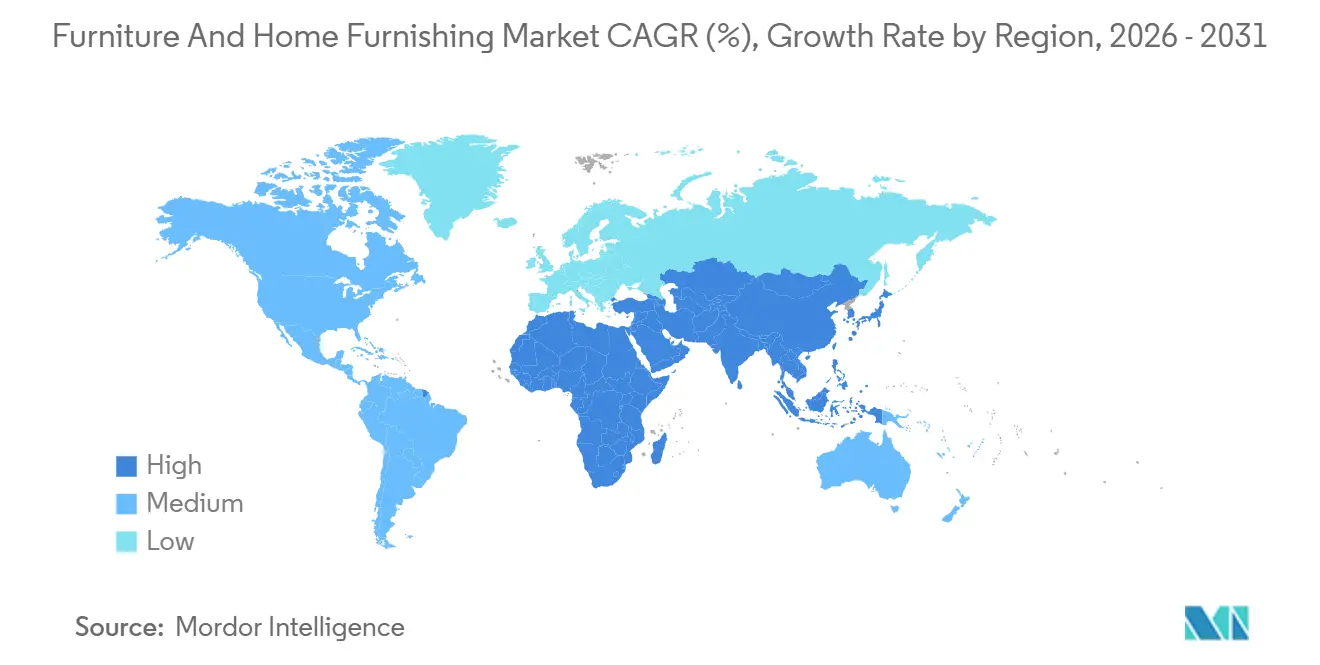

- By geography, North America accounted for 28.41% of the furniture and home furnishing market share in 2025, while Asia-Pacific is the fastest-expanding region at an 8.01% CAGR through 2031, underscoring long-run urbanization and demographic tailwinds in core Amarkets.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Furniture And Home Furnishing Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Urbanization & Shrinking Living Spaces | +1.8% | Global, peak in India, China, Asia-Pacific | Long term (≥ 4 years) |

| Rising Disposable Income in Emerging Economies | +1.5% | Asia-Pacific core, spill-over to Middle East & Africa, South America | Long term (≥ 4 years) |

| Growth of E-Commerce & Omnichannel Furniture Retailing | +1.2% | Global, early gains in North America, Europe | Medium term (2-4 years) |

| Post-Pandemic Work-From-Home Furniture Demand Spike | +2.1% | North America, Western Europe, select Asia-Pacific metros | Medium term (2-4 years) |

| Surge in Demand for Modular, Space-Saving Designs | +1.3% | Global, concentrated in urban centers | Medium term (2-4 years) |

| Circular-Economy Mandates Driving Recycled Material Adoption | +0.8% | Europe leadership, regulatory influence spreading globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization and Shrinking Living Spaces Propel Space-Efficient Furniture Demand

Rising urban density is compressing residential footprints in major metro areas, which heightens the appeal of modular and multifunctional designs that can reconfigure across daily routines. Government statistics show that in the Netherlands, the average living space per person in major cities like Amsterdam is about 49 square metres, compared with a national average of 65 square metres, reflecting smaller residential footprints in urban areas [1]CBS, “Construction and Housing Figures,” Statistics Netherlands, longreads.cbs.nl/trends19-eng/economy/figures/construction-and-housing/. This trend is most visible in compact floor plans where convertible sofas, folding desks, and vertical storage systems deliver real space utility. Product development cycles increasingly focus on knock-down designs that cut packaging volume and streamline last-mile handling while supporting lower-emission logistics. Global brands are adapting assortments and packaging to small-space living and urban delivery constraints, with compact series and room-by-room planning tools embedded into store formats. As more households prioritize adaptability and ease of assembly, the furniture and home furnishing market benefits from design innovations that meet the constraints of modern city housing while reducing waste in shipping and storage.

Rising Disposable Income in Emerging Economies Unlocks Premium Segment Growth

A larger middle class in high-growth Asian markets is supporting steady trading-up behaviour from basic to premium finishes, especially in living room and bedroom categories. In India, category expansion aligns with broad-based home formation and residential upgrades, where organized retail and online channels have widened access to branded offerings for urban households. Pradhan Mantri Awas Yojana – Urban (PMAY-U) 2.0 covers 5,206 towns, with 995 thousand houses sanctioned and 5.616 million households registered, across implementation verticals such as Beneficiary-Led Construction (BLC), Affordable Housing in Partnership (AHP), and In-Situ Slum Redevelopment (ISS). The scheme targets Economically Weaker Sections (EWS), Low-Income Groups (LIG), and Middle-Income Groups (MIG), with total central government assistance of USD 29.3 billion. Pradhan Mantri Awas Yojana – Urban (PMAY-U) 2.0 covers 5,206 towns, with 995 thousand houses sanctioned and 5.616 million households registered, across implementation verticals such as Beneficiary-Led Construction (BLC), Affordable Housing in Partnership (AHP), and In-Situ Slum Redevelopment (ISS). The scheme targets Economically Weaker Sections (EWS), Low-Income Groups (LIG), and Middle-Income Groups (MIG), with total central government assistance of USD 29.3 billion[2]Ministry of Housing and Urban Affairs, “PMAY-U 2.0 Dashboard,” pmaymis.gov.in/pmaymis2_2024/pmaydefault.aspx. This large-scale urban housing expansion is a key driver of increased demand for furniture and home furnishings. Certifications such as FSC and GREENGUARD have become buying criteria for upwardly mobile consumers, which directs demand toward cleaner materials and low-emission finishes that meet recognized ecolabel benchmarks. This preference is visible in both residential and project-driven purchases, as procurement teams standardize on third-party standards in corporate, hospitality, and education settings. As premiumization advances, the furniture and home furnishing market captures higher ticket sizes through better materials, curated collections, and services that reinforce perceived value.

Growth of E-Commerce and Omnichannel Retailing Revolutionizes Furniture Purchasing Journeys

Omnichannel expansion continues to remove friction from a historically tactile and high-involvement category as retailers merge visualization tools with physical planning support. New store concepts emphasize smaller footprints for design consultations alongside Click and Collect services that lower delivery costs and shorten lead times for priority ranges. Flagship digital tools now allow room scanning and 3D placement to improve the fit of scale-sensitive items, which reduces return rates in bulky categories and improves confidence at checkout. Investment programs focus on additional small-format locations, distribution nodes, and end-to-end planning services that are critical to conversion in urban corridors. This combination lifts the reach of the furniture and home furnishing market by aligning digital discovery with reliable fulfillment and in-store support that simplifies complex decisions. According to the United States Census Bureau, quarterly retail e-commerce sales in the United States reached USD 310.3 billion in the third quarter of 2025, representing a 1.9 % increase from the previous quarter and a 5.1 % increase year-over-year. During the same period, total United States retail sales amounted to USD 1,893.6 billion, with e-commerce accounting for 16.4 % of the total. On a non-adjusted basis, e-commerce sales were USD 299.6 billion, making up 15.8 % of all retail sales and continuing a consistent growth trend over recent years, underscoring the increasing comfort of consumers with digital discovery and online purchasing, even for high-involvement items like furniture [3]U.S. Census Bureau, “Quarterly Retail E‑Commerce Sales,” census.gov/retail/ecommerce.html.

Post-Pandemic Work-From-Home Demand Spike Sustains Ergonomic and Home-Office Furniture Growth

Remote and hybrid work patterns have become part of normal workforce design, which sustains demand for ergonomic desks, task seating, and storage that fit in smaller home offices. According to the United States Census Bureau’s American Community Survey, 13.8 % of United States workers usually worked from home in 2023, more than double the share in 2019, reflecting a structurally higher base of home-based work even as some employees return to traditional offices [4]U.S. Census Bureau, “Work-From-Home Inequalities,” census.gov/library/stories/2025/01/work-from-home-inequalities.html. Category leaders are refining home-focused lines that bring commercial ergonomics into residential settings with lighter footprints, quiet motors, and simplified controls. Product launches advanced sustainable material options and comfort features, complementing adjustable seating that aligns with recognized office performance standards. Corporate buyers and dealer networks are also standardizing residential-grade packages for distributed teams and project-based deployments across regions. This shift keeps home-office demand relevant in the furniture and home furnishing market, with new seating and desk lines anchored in ergonomics and materials innovation.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility In Raw-Material Prices (Wood, Metals, Fabrics) | -1.3% | Global, acute in import-dependent markets | Short to Medium term (≤ 4 years) |

| Trade-Policy Uncertainties & Tariff Fluctuations | -1.1% | United States-China trade axis, Canada softwood lumber | Short to Medium term (≤ 4 years) |

| Supply-Chain Bottlenecks For Specialty Hardware | -0.6% | Global, regional variations by component type | Short term (≤ 2 years) |

| Rising Reverse-Logistics Costs From E-Commerce Returns | -0.9% | North America, Europe, high-penetration markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Raw-Material Prices Pressures Margins and Supply-Chain Stability

Lumber price volatility, duty changes, and supply curtailments have kept input costs unpredictable for wood-based categories and upstream suppliers. Framing lumber market movements since 2024 have challenged purchasing plans in sequential quarters, which complicates pricing and promotions for wood-heavy lines. In parallel, governments have tightened import protections on steel and derivative products, which elevates costs for metal frames, fittings, and components in seating and storage. These forces raise material-to-revenue ratios and require more focused cost control in freight, packaging, and returns to hold margins. As a result, brands are working earlier with suppliers on substitutions and design-to-value choices that stabilize lead times and costs in the furniture and home furnishing market.

Trade-Policy Uncertainties and Tariff Fluctuations Disrupt Sourcing Strategies

Shifts in tariff schedules and scope force companies to rebalance sourcing across China, Southeast Asia, North America, and Europe to manage delivered costs and duty exposure. Changes to softwood lumber regimes and steel import protections alter the relative economics of domestic versus imported inputs, which affects category-level pricing decisions and promotional calendars. Currency movements compound planning risk in tariff-sensitive lanes, which can affect the timing of purchase orders and inventory positioning near quarter-ends. To counter these pressures, companies are resizing supplier portfolios, mixing nearshore capacity with longstanding vendor relationships, and adjusting value engineering to meet target prices. As these policies evolve, the furniture and home furnishing market faces periodic cost pass-through and mix shifts that test consumer price tolerance and retailer agility.

Segment Analysis

By Application: Outdoor Furniture Captures Post-Pandemic Lifestyle Shift While Living Room Dominates

Living Room furniture commanded 35.26% of applications in 2025 within the furniture and home furnishing market, supported by staples such as sectionals, entertainment units, and coordinated tables that anchor daily use in homes. The Outdoor category is the fastest-moving application with an 8.12% CAGR through 2031, which reflects the lasting adoption of backyard and balcony settings as extensions of indoor living. This mix underscores how households now balance core indoor replacements with exterior upgrades that emphasize weather-proof materials and easy care. The furniture and home furnishing market benefits from brands that align indoor aesthetics with outdoor durability, improving cross-category basket sizes and coordinated looks for patios and decks. Stronger materials performance and modular sets also aid retail execution by simplifying selection and reducing service calls after installation.

The acceleration in outdoor specifications continues in hospitality and multifamily settings as project buyers add terraces, rooftop lounges, and shared courtyards to amenity programs. These installations favor products with recycled content and certifications alongside UV-resistant finishes that retain color and structural strength over multiple seasons. As outdoor assortments mature, retailers integrate visualization and space-planning tools to support set selection by size, seating count, and storage for covers and cushions. Living room still anchors the furniture and home furnishing market with consistent replacement cycles and style-driven updates that lift upholstery, case goods, and soft furnishings together. This balance between durable indoor staples and growing outdoor use supports steady revenue across applications in both residential and commercial channels.

Note: Segment shares of all individual segments available upon report purchase

By Material: Plastic Surges on Recycled-Content Mandates While Wood Maintains Dominance

Wood held 46.61% material share in 2025 within the furniture and home furnishing market size, reflecting its durability, repairability, and strong consumer preference in visible case goods and premium seating. Engineered-wood variants help optimize resource use and cost while meeting emissions and performance thresholds required by institutional buyers. Compliance frameworks influence adhesive choices, finishes, and recycled-content claims, reinforcing supply-chain transparency and design-for-disassembly practices. As policy and buyer standards evolve, wood-based products with clear chain-of-custody and low-emission finishes continue to command strong demand. This positioning helps sustain the long-term role of wood in the furniture and home furnishing market across both residential and contract buyers.

Plastic is the fastest-growing material at an 8.36% CAGR through 2031, with the strongest momentum in outdoor lines where recycled HDPE and UV-stable polymers deliver multi-season performance. Mandates and procurement preferences for recycled content support innovations in blends and recyclability features that reduce waste and extend life. Metal remains critical to office and hospitality applications, with frames and hardware selected for strength, longevity, and ease of refurbishment. New standards and labeling programs guide buyers toward verified performance and sustainability tiers that align with rebates or green-building targets. Together, these developments align the furniture and home furnishing market with circularity goals and customer expectations on durability and end-of-life pathways.

By Distribution Channel: B2C/Retail Leads with Omnichannel Pivot, While B2B/Project Accelerates on Hybrid Work

B2C/Retail captured 71.15% of the 2025 furniture and home furnishing market share, reflecting the category’s high involvement purchases, where in-store planning and tactile evaluation remain influential. The channel is integrating smaller design-led stores with pick-up points and service desks that improve the end-to-end path to purchase and reduce delivery friction. Retailers are using store remodeling and new formats to offer room-planning services and curated vignettes that speed decision-making on bigger-ticket sets. Parallel investments in microfulfillment and flexible delivery windows improve throughput on bulky shipments that require careful scheduling and site readiness. As these changes take hold, the furniture and home furnishing market sees more consistent conversion across online and store environments that complement each other.

B2B/Project accounted for the remaining share in 2025 and is the fastest-growing at a 7.25% CAGR as employers and institutions fit out activity-based spaces and refresh hybrid collaboration zones. Dealer networks and contract specialists are pairing ergonomic seating, height-adjustable work points, and mobile storage into standard packages for speed and scalability. Category leaders continue to release lines tailored for distributed teams and flexible spaces, supported by service programs for installation and reconfiguration. Corporate demand also drives adherence to labeling standards and indoor air quality criteria that qualify for procurement preferences or sustainability reporting. This broadening of project demand helps the furniture and home furnishing market capture recurring programs across workplace, education, healthcare, and hospitality.

Geography Analysis

North America held 28.41 % of the global furniture and home furnishing market in 2025, with price sensitivity rising due to input cost fluctuations and tariff-related adjustments. Retailers are responding by refining assortments and investing in value-engineered solutions to maintain competitiveness. Volatility in lumber and import protections for steel and wood components has increased production costs for metal-framed and wood-based items. To counter logistics complexity, many operators are relying on smaller-format planning stores and micro-fulfillment centers to reduce delivery times for priority lines. These strategies help improve service levels and protect market share despite ongoing price pressures.

Asia-Pacific is the fastest-growing region, projected to expand at an 8.01 % CAGR through 2031, driven by urbanization, home formation, and a growing middle class. Rising incomes are fueling demand for premium and durable furniture, with buyers showing stronger preferences for certified materials and long-lasting finishes. The expansion of organized retail and e-commerce is improving access to branded collections and planned spaces with reliable after-sales support. Companies with strong local supplier networks and design localization are scaling faster across diverse housing types and climatic zones. These dynamics support steady growth for both residential and contract furniture markets throughout the region.

Europe and the Middle East & Africa are also shaping the global market through regulatory and project-driven dynamics. In Europe, sustainability and circular economy regulations are influencing product design, sourcing, and material choices, while Digital Product Passports will simplify verification of compliance and end-of-life tracking. The UK shows steady replacement cycles for home-office and contract furniture, aided by hybrid work patterns and aligned procurement standards. In the Middle East and Africa, particularly the GCC, hospitality, residential, and mixed-use developments are driving demand for durable, high-performance contract furniture. Regional e-commerce growth and modular, specialty assortments are expanding consumer access, while aligning with project timelines and standards remains critical for scaling operations.

Competitive Landscape

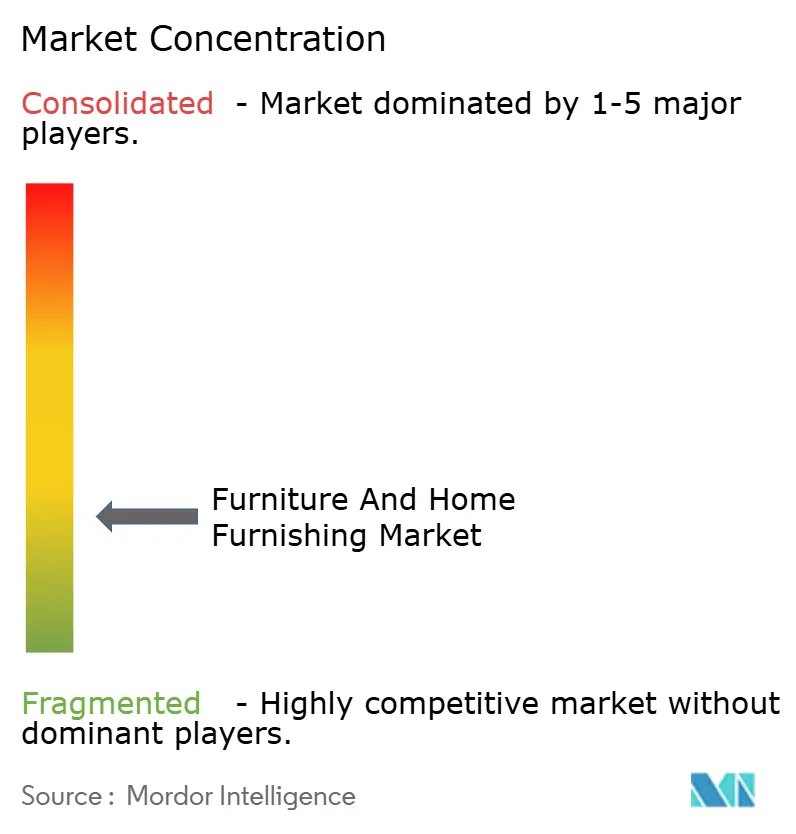

The furniture and home furnishing market remains highly fragmented, with the largest players holding a relatively small share of overall revenue. Leading companies include Inter IKEA Group, Ashley Furniture Industries, MillerKnoll, Steelcase, and Williams-Sonoma, while regional specialists, nimble pure-play retailers, and contract-focused suppliers continue to capture significant portions of the market. Retailers are investing in store format innovation, omnichannel integration, and planning services that blend digital discovery with in-store experiences. Premium-focused brands are emphasizing ergonomic design, verified sustainability, and workplace solutions that support hybrid and flexible office layouts. Together, these strategies maintain a diverse and competitive market landscape.

Major companies are focusing on vertical integration, logistics improvements, and expanding store networks to speed up delivery and reduce damage for bulky products. Inter IKEA Group is adding smaller-format planning points and enhancing fulfillment capacity to support omnichannel growth, while Ashley Furniture Industries is expanding United States manufacturing with new facilities aimed at boosting operational efficiency. Contract-focused brands are launching product lines that combine home-office ergonomics with residential aesthetics for hybrid work environments. These initiatives strengthen visibility and availability across regions and support a consistent market presence.

Product standards, sustainability goals, and evolving procurement rules are shaping innovation and compliance among market leaders. MillerKnoll continues to scale core product lines and expand retail operations to meet enterprise buyer expectations, while Steelcase integrates workplace solutions with brand collaborations designed for hybrid and modern office environments. Ecolabels and material reporting standards are increasingly influencing design, emissions, and end-of-life management, favoring companies with strong compliance infrastructure. Williams-Sonoma balances pricing actions, shareholder returns, and selective growth to manage cost pressures from tariffs. Retailers are also optimizing sourcing strategies, including nearshoring and dual sourcing, to stabilize costs while maintaining product quality, ensuring steady execution in a complex market.

Furniture And Home Furnishing Industry Leaders

Inter IKEA Group

Ashley Furniture Industries

Herman Miller (MillerKnoll)

Steelcase

Williams-Sonoma

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Shoptelligence launched its new VendorSense IQ Suite, introducing ShopLab AI and ShopLaunch AI to help furniture manufacturers and vendors make faster, more confident product and go‑to‑market decisions using real consumer demand data and advanced analytics.

- September 2025: Singapore-based D2C brand Castlery entered the United Kingdom market in September 2025, marking its European debut. The brand launched an e-commerce store and showcased its furniture collections during London Design Week and the London Design Festival through dedicated pop-up events.

- February 2025: IKEA Canada grew its Plan and order point network in Quebec and continued to invest in delivery and fulfillment infrastructure in Greater Vancouver, Greater Toronto, and other key areas.

- January 2025: Niso Furniture and Kornit Digital collaborated to launch a sustainable home decor collection, unveiled at Heimtextil 2025, combining advanced furniture design with innovative digital textile solutions for environmental consciousness.

Global Furniture And Home Furnishing Market Report Scope

Furniture comprises essential, movable items such as tables, chairs, beds, and sofas, serving primary utility. Furnishings, a broader category, include these items alongside decorative and functional accessories like carpets, curtains, cushions, lighting, and artwork. These elements collectively enhance a room's decor, ensuring comfort and aesthetic appeal, while furniture provides the foundational functionality of a space.

The furniture and home furnishing market report is segmented by application (kitchen, living room, bedroom, bathroom, outdoor, other furniture), material (wood, metal, plastic, fabric, others), distribution channel (b2c/retail and b2b/project), and geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The market forecasts are provided in terms of value (USD).

| Kitchen |

| Living Room |

| Bedroom |

| Bathroom |

| Outdoor |

| Other Furniture |

| Wood |

| Metal |

| Plastic |

| Fabric |

| Others |

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Project |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Application | Kitchen | |

| Living Room | ||

| Bedroom | ||

| Bathroom | ||

| Outdoor | ||

| Other Furniture | ||

| By Material | Wood | |

| Metal | ||

| Plastic | ||

| Fabric | ||

| Others | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Project | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the furniture and home furnishing market?

The furniture and home furnishing market size is USD 1.00 trillion in 2026 and is projected to reach USD 1.43 trillion by 2031 at a 7.39% CAGR, reflecting sustained demand across residential and project channels.

Which product applications are leading and which are growing the fastest in this space?

Living Room leads with 35.26% of 2025 revenue, while Outdoor is projected to grow the fastest at an 8.12% CAGR through 2031 as exterior spaces become extensions of indoor living.

How do materials trends shape the competitive outlook?

Wood retains a 46.61% share in 2025 due to consumer preference and durability, while Plastic is the fastest-growing material at an 8.36% CAGR, supported by recycled-content mandates and outdoor use cases.

Which regions are most important for near-term growth?

North America holds 28.41% of 2025 revenue, while Asia-Pacific is the fastest-growing region at an 8.01% CAGR based on urbanization and rising household incomes across key markets.

How are regulations influencing product and sourcing decisions?

EU circularity rules and procurement standards prioritize durability, repairability, recycled content, and verified ecolabels, which shape materials choices and supply-chain documentation for products sold in Europe.

What strategic moves are leaders making to strengthen positioning?

Leading companies are investing in smaller format planning stores, fulfillment capacity, and standards alignment while executing pricing and capital actions to offset input volatility and tariff exposure.