| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 4.97 % |

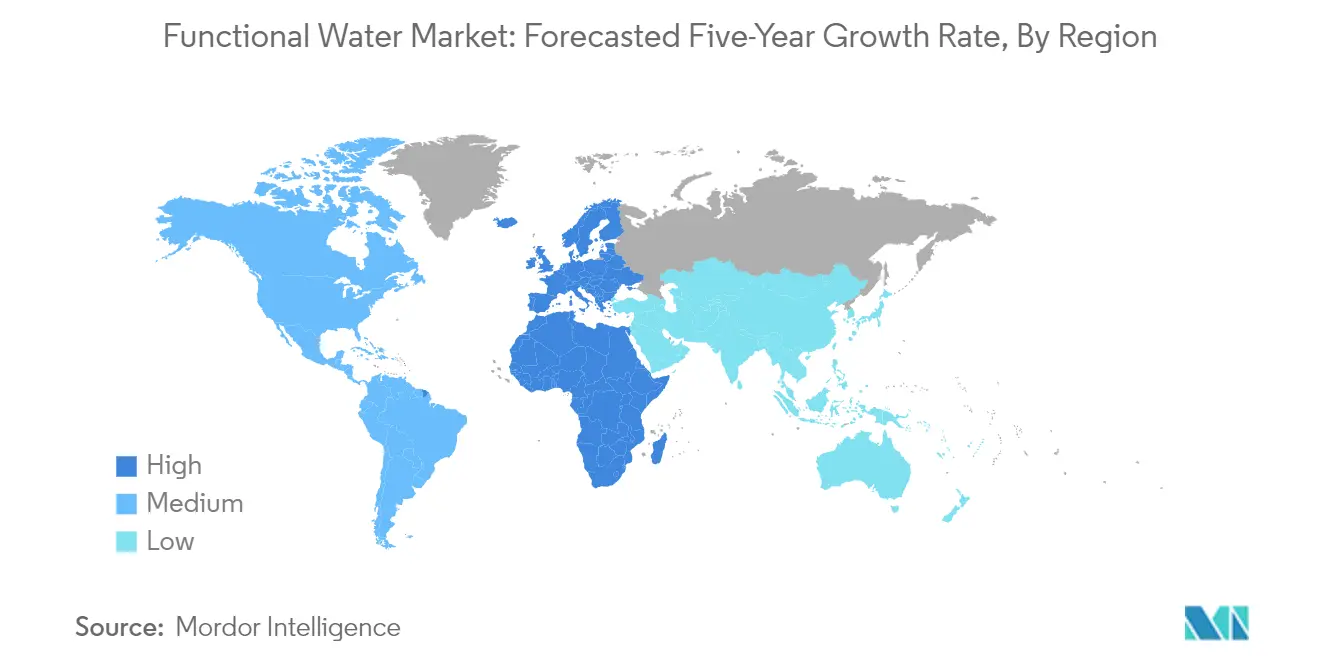

| Fastest Growing Market | Europe |

| Largest Market | North America |

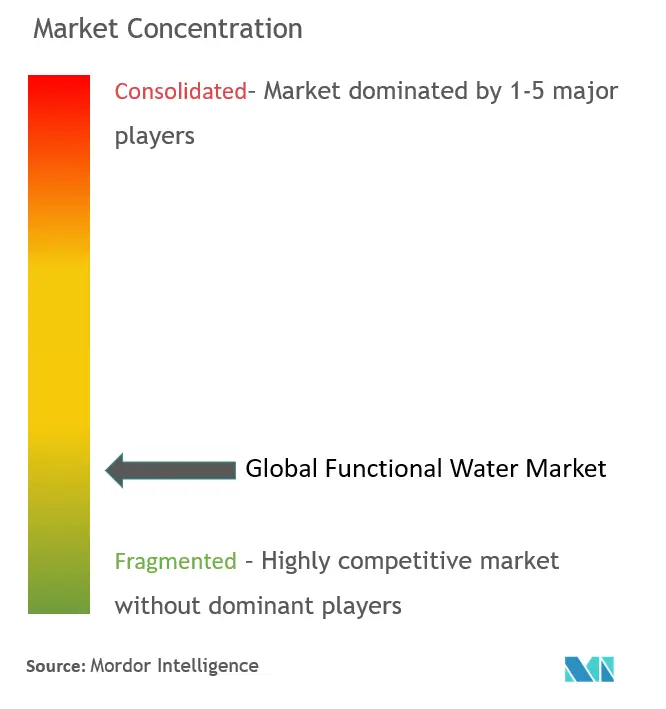

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Functional Water Market Analysis

The Functional Water Market is expected to register a CAGR of 4.97% during the forecast period.

The functional water industry is experiencing a significant transformation driven by evolving consumer preferences and retail modernization. Major retailers are expanding their footprint to improve product accessibility, with Walmart planning to operate 10,500 stores and clubs under 46 banners across 24 countries by the end of 2022. The rise of e-commerce platforms and omnichannel distribution strategies has revolutionized how functional water products reach consumers. This retail evolution has been accompanied by increasing consumer health consciousness, with Kerry Group reporting that over 65% of consumers have become more concerned about their health and wellness in recent years.

Product innovation has become a cornerstone of market development, with manufacturers focusing on clean-label formulations and natural ingredients. Companies are launching new products with unique flavor combinations and functional benefits to meet diverse consumer needs. For instance, Flow Beverages Corp. introduced vitamin water in three different flavors in 2022, featuring zero sugar, zero calories, and certified organic ingredients. This trend toward natural formulations is particularly significant as research by the International Food Information Council Foundation reveals that approximately 72% of consumers consider vitamin content when making food and beverage choices.

The industry is witnessing a notable shift toward sustainable packaging solutions and environmentally conscious production practices. Major players are implementing comprehensive sustainability initiatives, with companies like PepsiCo committing to using 100% recycled PET bottles for all Pepsi-branded products by 2030. This transformation extends beyond packaging to include responsible sourcing of ingredients and eco-friendly manufacturing processes, reflecting growing consumer awareness of environmental issues and their preference for brands that demonstrate environmental responsibility.

Health and wellness considerations continue to shape market dynamics, with a particular focus on sugar reduction and natural sweeteners. According to WHO data from 2023, 61.83% of the Russian population was overweight, exemplifying a global health concern that is driving demand for healthier beverage alternatives. Manufacturers are responding by developing innovative formulations that deliver functional benefits without added sugars or artificial ingredients. This has led to the emergence of new product categories featuring natural sweeteners, zero-calorie options, and enhanced nutritional profiles that align with contemporary health and wellness trends.

Functional Water Market Trends

Growing Demand for Healthy Hydration Products

Consumers are increasingly shifting toward maintaining a healthy lifestyle that aids in sustaining fitness while reducing the incidence of lifestyle diseases. This transformation, coupled with rising healthcare expenditures and increasing urbanization rates, is driving the demand for healthy hydration products like functional beverage water. Research by the International Food Information Council Foundation revealed that nearly 72% of consumers consider the presence of vitamins at least sometimes, and 22% consider it always when making decisions about what to eat and drink. This significant consumer awareness has led manufacturers to make water more nutritious by infusing it with vitamins and minerals that not only quench thirst but also improve immunity and metabolism, enhance the ability to concentrate, and reduce stress.

Athletes and fitness enthusiasts particularly prioritize proper hydration to enhance performance and recovery, driving the demand for electrolyte water and hydration solutions with specific mineral compositions. Market players are actively responding to this trend by diversifying their product range and appealing to health-conscious consumers. For instance, in 2021, PepsiCo launched the sparkling water drink Soulboost, featuring varieties like Blueberry Pomegranate and Black Cherry Citrus, with 200 milligrams of Panax ginseng to help support mental stamina. Additionally, manufacturers are exploring innovative ingredients, as exemplified by Verday's launch of chlorophyll-enriched water, which was positioned as a detoxification aid and skin and blood health product.

Understand The Key Trends Shaping This Market

Download PDF

Advertisement and Promotional Activities Gaining Prominence

Functional water is gaining immense popularity among millennial and Gen Z populations due to aggressive marketing campaigns run by prominent manufacturing companies. These campaigns specifically highlight features like added vitamins, minerals, antioxidants, electrolytes, and other functional ingredients that enhance hydration, support immune function, or boost energy. Major companies are making substantial investments in advertising, with Coca-Cola Company spending $4.32 billion in 2022 and PepsiCo allocating $3.5 billion in 2021 for advertising expenses. These investments demonstrate the industry's commitment to building brand awareness and influencing consumer purchasing decisions.

The marketing landscape has evolved significantly with social media becoming a crucial factor in shaping consumer behavior. Companies are leveraging platforms like Facebook, Instagram, and YouTube to engage consumers through promotional campaigns, with both established players and start-ups benefiting from these digital channels. Recent notable campaigns include Propel Fitness Water's first campaign featuring Michael B. Jordan in May 2023, where the actor promoted the brand's product during a hike with WalkGoodLA members. Similarly, in June 2022, Coca-Cola's brand vitamin water collaborated with Lil Nas X for the "Nourish Every You" campaign, releasing six mini music videos featuring different vitamin water flavors. These campaigns demonstrate how brands are utilizing celebrity partnerships and multi-channel marketing approaches to create engaging content that resonates with their target audience while promoting the functional benefits of their products.

Segment Analysis: By Product Type

Vitamin Segment in Functional Water Market

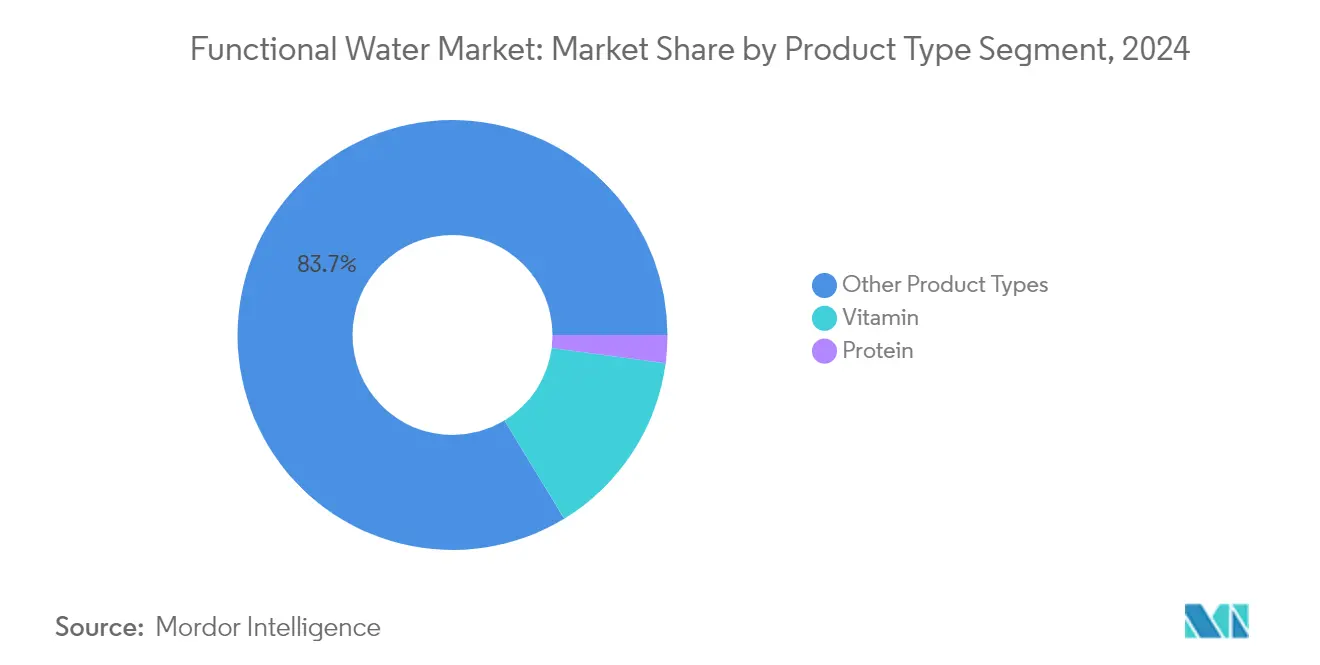

The vitamin water segment has emerged as a dominant force in the functional water market, holding approximately 14% market share in 2024. This segment's prominence is driven by increasing consumer awareness about proper nutritional intake and a shift toward healthier beverage options. The segment's growth is particularly strong among health-conscious consumers who seek convenient ways to supplement their daily vitamin intake through infused water beverages. Manufacturers are actively expanding their vitamin water portfolios with innovative formulations that include various combinations of vitamins like B-complex, C, and D. The segment's success is further bolstered by the rising demand for immunity-boosting beverages, with many brands incorporating vitamin C and other immune-supporting vitamins in their functional water products. Additionally, the segment is experiencing robust growth with a projected growth rate of nearly 7% from 2024 to 2029, making it the fastest-growing segment in the market, driven by continuous product innovations and increasing consumer preference for vitamin water over traditional sugary drinks.

Remaining Segments in Functional Water Market

The protein water segment and other product types, including electrolyte water, alkaline water, and herbal ingredients, play crucial roles in shaping the functional water market landscape. The protein water segment caters to fitness enthusiasts and athletes seeking convenient protein supplementation through beverages, with manufacturers introducing innovative protein water products targeting various consumer demographics. Other product types, encompassing electrolyte water, alkaline water, and waters infused with botanical ingredients, serve diverse consumer needs ranging from sports recovery to general wellness. These segments are characterized by continuous innovation in ingredients and formulations, with manufacturers introducing new functional benefits to meet evolving consumer preferences. The market has witnessed increased product development in areas such as collagen-infused waters, adaptogenic waters, and specialized functional waters targeting specific health benefits, demonstrating the dynamic nature of these segments.

Segment Analysis: By Distribution Channel

Supermarkets/Hypermarkets Segment in Functional Water Market

Supermarkets and hypermarkets continue to dominate the functional water market, commanding approximately 65% of the total market share in 2024. These retail formats maintain their leadership position due to their extensive retail spaces and ability to accommodate a wide range of preferences from various brands. The segment's dominance is reinforced by their strategic product placement, attractive discounts, and promotional activities that effectively capture consumer attention. Supermarkets and hypermarkets are focusing on expanding their businesses and making their products accessible in every region to maintain their competitive edge. These stores feature strong competition among prominent manufacturers, inducing brands to differentiate products on their shelves, reposition their offerings, and target audiences effectively. The availability of multiple brands under one roof, coupled with the convenience of comparison shopping, makes supermarkets and hypermarkets the preferred choice for functional water purchases.

Online Retail Stores Segment in Functional Water Market

The online retail stores segment is projected to experience the highest growth rate of approximately 8% during the forecast period 2024-2029. This remarkable growth is driven by the increasing consumer preference for convenient shopping options and the rising penetration of internet services across global markets. Online channels offer the unique advantage of providing an extensive range of options compared to traditional brick-and-mortar stores, while eliminating intermediaries in the distribution chain. Key players are adopting various online retail strategies to attract a larger consumer base by improving their customer service and engagement through initiatives like same-day delivery, hassle-free payment options, and product authenticity guarantees. The segment's growth is further supported by the expansion of e-commerce platforms and the increasing adoption of digital payment solutions, making it easier for consumers to access and purchase functional water products from the comfort of their homes.

Remaining Segments in Distribution Channel

The convenience and grocery stores, along with other distribution channels, continue to play vital roles in the functional water market's distribution landscape. Convenience stores maintain their significance due to their proximity to residential areas and extended operating hours, making them essential for last-minute purchases and immediate consumption needs. The other distribution channels, including warehouse clubs, specialty/health stores, and forecourt retailers, cater to specific consumer segments with unique purchasing preferences. These channels often focus on premium products and specialized functional water varieties, contributing to the market's diversity and accessibility. Both segments complement the larger distribution channels by providing alternative purchase points and serving distinct consumer needs across different geographical locations and demographics.

Functional Water Market Geography Segment Analysis

Functional Water Market in North America

North America represents a mature functional water market, driven by increasing health consciousness and a preference for sugar-free beverages among consumers. The region benefits from strong distribution networks, established retail channels, and high consumer awareness about functional beverages. The United States dominates the regional landscape, followed by Mexico and Canada, with all three markets showing distinct consumption patterns and growth trajectories. The region's growth is primarily fueled by innovative product launches, expanding retail presence, and increasing consumer interest in the functional water industry that offers specific health benefits beyond basic hydration.

Functional Water Market in the United States

The United States stands as the largest functional water market in North America, commanding approximately 93% of the regional functional water market share. The market's dominance is attributed to rising obesity levels and increasing cardiovascular disorders, which have led consumers to seek healthier beverage alternatives. The versatility of the functional water industry makes it suitable for consumption throughout the day in various settings, supported by diverse packaging options like containers and single-serve bottles. The country has witnessed a significant rise in demand for clean-label products, with consumers showing increased interest in understanding ingredient compositions. The presence of major manufacturers and their extensive distribution networks further strengthens the market position of functional water in the United States.

Functional Water Market Growth Trajectory in the United States

The United States is also experiencing the fastest growth in North America, with a projected CAGR of approximately 6% during 2024-2029. This growth is driven by the increasing popularity of the premium water market among working professionals and millennial populations. The market is witnessing a surge in product innovations, particularly in the premium segment, with manufacturers introducing new flavors and functional ingredients. The trend toward sugar-free and naturally flavored options continues to gain momentum, supported by growing health awareness and changing consumer preferences. The expansion of e-commerce channels and direct-to-consumer sales models is further accelerating market growth, making functional water more accessible to consumers across the country.

Functional Water Market in Europe

The European functional water market demonstrates a diverse landscape with varying consumer preferences across different regions. The market is characterized by a strong presence in countries like the United Kingdom, Russia, and Germany, with each country showing distinct consumption patterns and growth trajectories. The region's market is driven by increasing health consciousness, growing demand for sugar-free beverages, and rising interest in functional ingredients. Innovation in flavors and functional benefits, along with sustainable packaging initiatives, continues to shape the market dynamics across European countries.

Functional Water Market in the United Kingdom

The United Kingdom emerges as the largest functional water market in Europe, holding approximately 24% of the regional functional water market share. The market's strength is attributed to increasing health consciousness among customers and the growing demand for functional beverages among working professionals. The country's retail landscape, characterized by strong supermarket chains and convenience stores, plays a crucial role in product distribution and accessibility. The market also benefits from innovative product launches and growing consumer awareness about the benefits of functional beverages.

Functional Water Market Growth Trajectory in Russia

Russia demonstrates the highest growth potential in the European region, with a projected CAGR of approximately 11% during 2024-2029. The market's rapid growth is driven by increasing consumer interest in the alkaline water market made with traditional ingredients like van chai, linden, Siberian ginseng, and sage. The country's market is experiencing a transformation with local manufacturers expanding their product offerings, particularly following recent geopolitical changes. The growing interest in health and wellness products, especially among urban consumers, continues to drive market expansion.

Functional Water Market in Asia-Pacific

The Asia-Pacific functional water market presents a dynamic landscape with significant variations across different countries. The region encompasses major markets like China, Japan, India, and Australia, each with unique consumer preferences and market characteristics. The market is driven by increasing urbanization, rising disposable incomes, and growing health consciousness among consumers. The region shows particular strength in innovative product development and adaptation to local taste preferences.

Functional Water Market in China

China dominates the Asia-Pacific functional water market as the largest country in the region. The market's strength is attributed to increasing urbanization and rising health concerns regarding diabetes, obesity, and cardiovascular problems. The country's aging population and growing health consciousness among younger consumers drive the demand for nutrient-infused beverages. The market benefits from strong distribution networks and the presence of both international and local manufacturers offering innovative products.

Functional Water Market Growth Trajectory in India

India emerges as the fastest-growing market in the Asia-Pacific region. The market's growth is driven by rising consumer awareness about the vitamin water market and increasing sports and fitness participation rates. The younger population's willingness to try new and innovative products, especially among Gen Z and millennial consumers, contributes to market expansion. The trend toward vegan, keto, and gluten-free products is also influencing product development and market growth in the country.

Functional Water Market in South America

The South American functional water market shows promising development, with Brazil and Argentina as key markets in the region. The market is characterized by increasing urbanization, rising disposable incomes, and growing health consciousness among consumers. Brazil emerges as both the largest and fastest-growing market in the region, driven by changing consumer lifestyles and increasing demand for healthy hydration options. The region's market is influenced by local taste preferences and the growing trend toward sugar-free and naturally flavored beverages, with manufacturers focusing on product innovations to meet these evolving consumer demands.

Functional Water Market in the Middle East & Africa

The Middle East & Africa functional water market demonstrates steady growth potential, with the United Arab Emirates and South Africa as significant markets. The region's market is characterized by increasing health consciousness and a growing preference for premium beverage options. South Africa represents the largest market in the region, while the United Arab Emirates shows the fastest growth potential. The market benefits from the region's young population and increasing awareness about health and wellness products, with manufacturers focusing on innovative product launches and expanding distribution networks to capture market opportunities.

Get Analysis on Important Geographic Markets

Download PDF

Functional Water Industry Overview

Top Companies in Functional Water Market

The functional water market features established beverage giants like PepsiCo, Coca-Cola, and Nestlé alongside specialized players such as Flow Beverage Corp, CENTR Brands, and Vitamin Well. Companies are heavily focused on product innovation through the introduction of new flavors, functional ingredients, and sustainable packaging solutions to meet evolving consumer preferences. Operational agility is demonstrated through strategic partnerships with sports teams, athletes, and retail chains to enhance brand visibility and market penetration. Market leaders are expanding their distribution networks through omnichannel strategies, combining traditional retail presence with growing e-commerce capabilities. Companies are also investing significantly in marketing and promotional activities, particularly through social media platforms and influencer partnerships, to build brand awareness and capture the attention of health-conscious millennials and Gen Z consumers.

Dynamic Market with Strong Growth Potential

The functional beverage industry exhibits a moderate level of consolidation, with global beverage conglomerates holding substantial market share through their established brands and extensive distribution networks. These major players leverage their financial strength and research capabilities to continuously introduce innovative products and capture emerging market opportunities. Regional and specialized players maintain their competitive edge by focusing on specific market segments, unique ingredient combinations, and local consumer preferences, creating a diverse competitive landscape that spans from global to hyperlocal offerings.

The market is characterized by frequent merger and acquisition activities as larger companies seek to expand their enhanced water portfolios and gain access to innovative products and technologies. Strategic partnerships and collaborations between manufacturers, distributors, and retailers are common, enabling companies to enhance their market presence and operational efficiency. The competitive dynamics are further shaped by the increasing presence of private label brands and the emergence of direct-to-consumer brands that leverage digital platforms to reach health-conscious consumers.

Innovation and Adaptability Drive Market Success

Success in the smart water industry increasingly depends on companies' ability to differentiate their products through unique functional benefits, sustainable packaging solutions, and authentic brand storytelling. Incumbent players must focus on continuous product innovation, investment in research and development, and strengthening their distribution networks while maintaining strong relationships with retailers and distributors. Companies need to develop comprehensive digital strategies, including e-commerce capabilities and social media engagement, to effectively reach and engage with their target consumers.

Market contenders can gain ground by identifying and serving underserved market segments, developing unique value propositions, and building strong brand identities that resonate with health-conscious consumers. The relatively low switching costs for consumers and the growing acceptance of new brands present opportunities for emerging players to establish themselves. However, companies must navigate potential regulatory challenges related to ingredient claims, packaging requirements, and environmental regulations while maintaining product quality and safety standards. Success also requires careful attention to supply chain optimization, cost management, and the ability to scale operations efficiently while maintaining product consistency and quality.

Functional Water Market Leaders

-

The Coca-Cola Co.

-

PepsiCo Inc.

-

Vitamin Well

-

Nirvana Water Sciences Corp.

-

Flow Beverage Corp.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Functional Water Market News

- September 2023: UC Berkeley and PepsiCo renewed their partnership, confirming PepsiCo as the official beverage partner of the campus for the next decade. This extended collaboration with PepsiCo is anticipated to enhance the company's support for Berkeley's sustainability, equity, and health and wellness initiatives. Under the agreement and in alignment with PepsiCo's pep+ (PepsiCo Positive) business model, the company will provide energy-efficient beverage distribution and cooling equipment to Berkeley, along with financial support for campus sustainability priorities.

- October 2022: CENTR Brands Corporation expanded its portfolio of health and wellness products with the introduction of CENTR Enhanced, a non-CBD functional sparkling water.

- July 2022: Flow Beverage Corp. launched its Flow Vitamin-Infused Water line in three new organic flavors: Cherry, Citrus, and Elderberry, offering consumers a variety of healthy beverage options.

Functional Water Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Deliverables and Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Market Drivers

- 4.1.1 Consumer Preferences Toward Value-added Beverages

- 4.1.2 Expenditure on Advertisement and Promotional Activities

-

4.2 Market Restraints

- 4.2.1 Inclination Toward Other Functional Beverages

- 4.2.2 High Cost Associated With Functional Water Hampering Growth in Developing Countries

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Buyers/Consumers

- 4.3.2 Bargaining Power of Suppliers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products and Services

- 4.3.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Product Type

- 5.1.1 Vitamin

- 5.1.2 Protein

- 5.1.3 Other Product Types

-

5.2 Distribution Channel

- 5.2.1 Hypermarkets/Supermarkets

- 5.2.2 Convenience/Grocery Stores

- 5.2.3 Online Retail Stores

- 5.2.4 Other Distribution Channels

-

5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 Spain

- 5.3.2.4 France

- 5.3.2.5 Italy

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Most Active Companies

-

6.3 Company Profiles

- 6.3.1 The Coca-Cola Co. (Glaceau Smartwater)

- 6.3.2 PepsiCo Inc. (Soulboost)

- 6.3.3 Balance Water Company (Balance Water)

- 6.3.4 Danone SA (Salus, Żywiec Zdrój, Volvic, Aqua, Font Vella, Mizone)

- 6.3.5 Dr. Pepper Snapple Group Inc. (Canada Dry, Schweppes, Core Hydration, bai)

- 6.3.6 Function Drinks (function)

- 6.3.7 CENTR Brands Corporation (Centr)

- 6.3.8 Flow Beverage Corp. (Flow)

- 6.3.9 Disruptive Beverages Inc. (Ayala's Herbal Water)

- 6.3.10 Hint Inc.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Functional Water Industry Segmentation

Functional water, which belongs to the non-alcoholic beverage category, is fortified with additional ingredients that offer various health benefits.

The market studied is segmented by product type, distribution channel, and geography. By product type, the market analyzed is segmented into protein water, vitamin water, and other product types. The distribution channel segments the market into hypermarkets/supermarkets, convenience/grocery stores, online retail stores, and other distribution channels. By geography, the study provides critical insights into the major regions, including North America, Europe, Asia-Pacific, South America, and Middle-East & Africa.

The market sizing and forecasts have been done for each segment based on value (in USD).

| Product Type | Vitamin | ||

| Protein | |||

| Other Product Types | |||

| Distribution Channel | Hypermarkets/Supermarkets | ||

| Convenience/Grocery Stores | |||

| Online Retail Stores | |||

| Other Distribution Channels | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | United Kingdom | ||

| Germany | |||

| Spain | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | United Arab Emirates | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Functional Water Market Research FAQs

What is the current Functional Water Market size?

The Functional Water Market is projected to register a CAGR of 4.97% during the forecast period (2025-2030)

Who are the key players in Functional Water Market?

The Coca-Cola Co., PepsiCo Inc., Vitamin Well, Nirvana Water Sciences Corp. and Flow Beverage Corp. are the major companies operating in the Functional Water Market.

Which is the fastest growing region in Functional Water Market?

Europe is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Functional Water Market?

In 2025, the North America accounts for the largest market share in Functional Water Market.

What years does this Functional Water Market cover?

The report covers the Functional Water Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Functional Water Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Functional Water Market Research

Mordor Intelligence provides a comprehensive analysis of the functional water industry. We leverage our extensive expertise in functional beverage research. Our latest report examines the expanding market for enhanced water products. This includes segments such as alkaline water, vitamin water, and smart water. The analysis covers emerging trends in fortified water and enriched water categories. We offer detailed insights into premium water and protein water developments across global markets.

Stakeholders gain valuable insights through our detailed examination of electrolyte water, infused water, and botanical water segments. The report explores growth opportunities in wellness water, sports water, and performance water categories. It also analyzes healthy hydration trends and energy water innovations. Available as an easy-to-download report PDF, our analysis includes deep dives into fitness water and nutraceutical water segments. This provides actionable intelligence for industry participants in the functional beverage industry.