Fruit Jellies Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

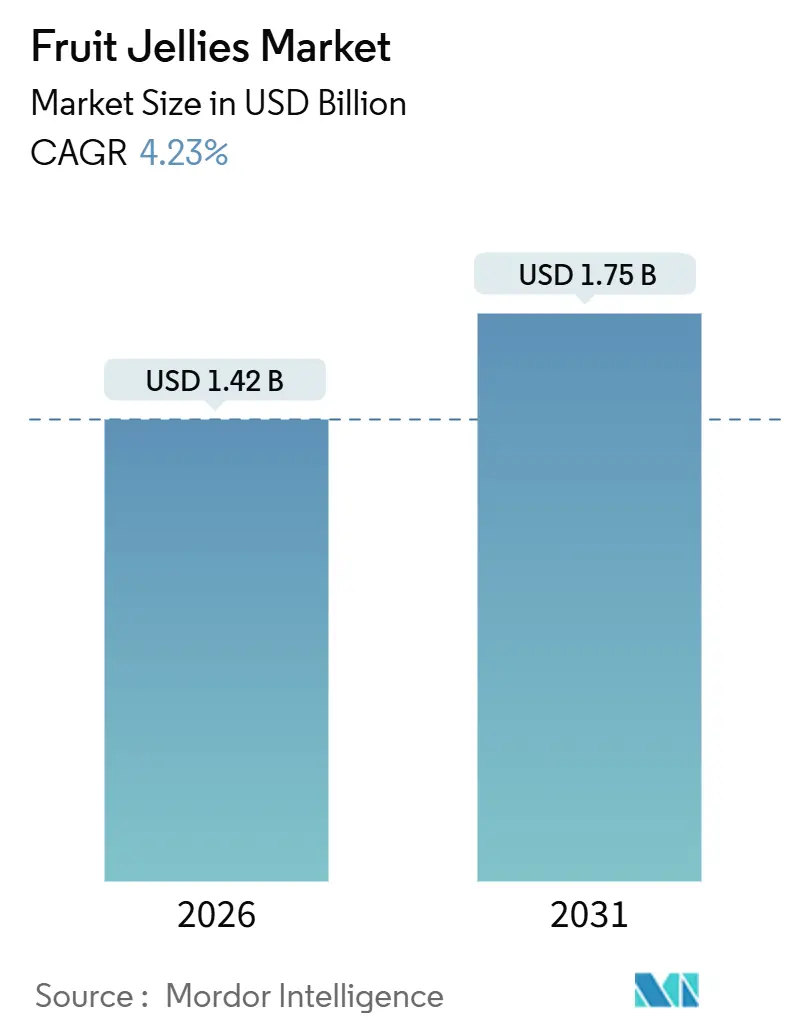

| Market Size (2026) | USD 1.42 Billion |

| Market Size (2031) | USD 1.75 Billion |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

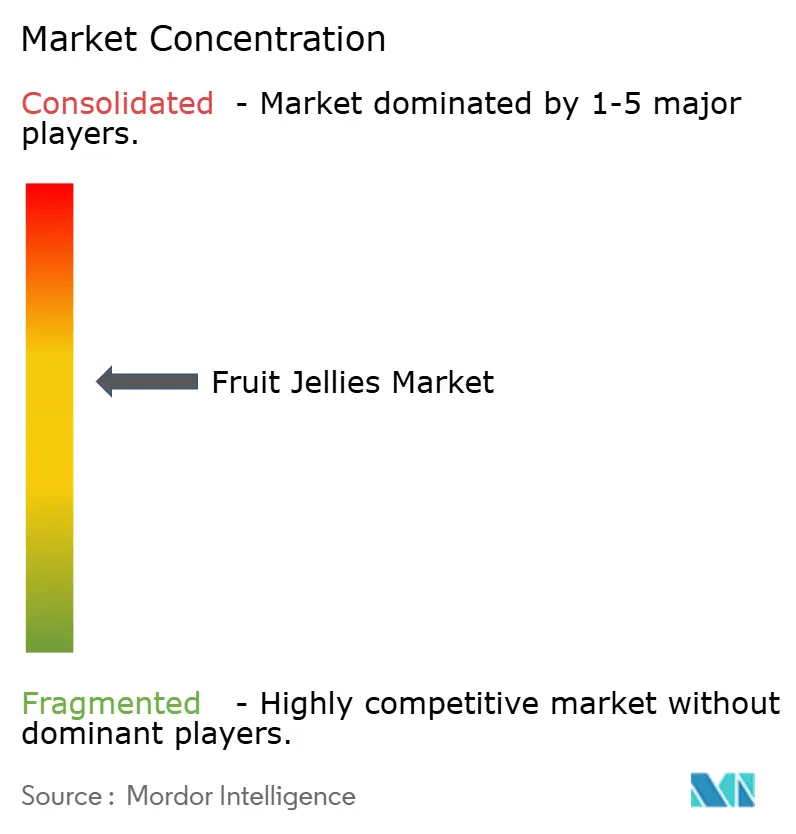

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fruit Jellies Market Analysis by Mordor Intelligence

The fruit jellies market size reached USD 1.42 billion in 2026 and is projected to rise to USD 1.75 billion by 2031, reflecting a 4.23% CAGR. Sustained demand for authentic fruit flavors, rising penetration of organized retail, and rapid packaging innovation underpin this growth trajectory. Premiumization is accelerating as pectin-based recipes allow “made with real fruit” claims that justify higher price points, while flexible mono-plastic pouches help brands meet retailer sustainability targets and trim logistics costs. Functional and vitamin-fortified variants continue to outpace the broader fruit jellies market, capturing shoppers who equate confectionery with wellness cues. At the same time, volatility in citrus, apple, and berry costs, coupled with tighter U.S. and EU labeling rules, is compressing margins and nudging the category toward scale-driven consolidation. Competitive rivalry remains moderate because regional specialists still defend local palates, yet format and on-pack messaging now influence impulse decisions more than brand legacy.

Key Report Takeaways

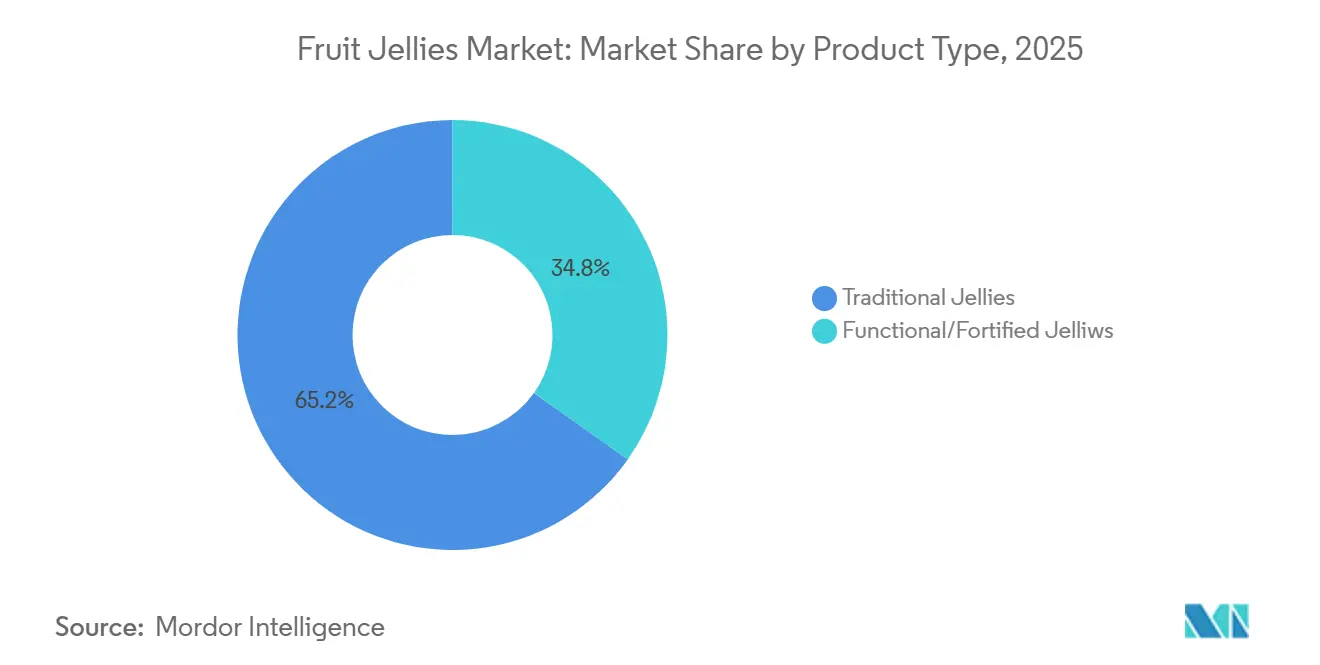

- By product type, traditional fruit jellies retained 65.17% of the fruit jellies market share in 2025, while functional and fortified jellies recorded the fastest projected CAGR at 5.12% through 2031.

- By packaging type, cups and jars held 48.23% of the fruit jellies market share in 2025; pouches and sachets are forecast to expand at a 4.88% CAGR to 2031.

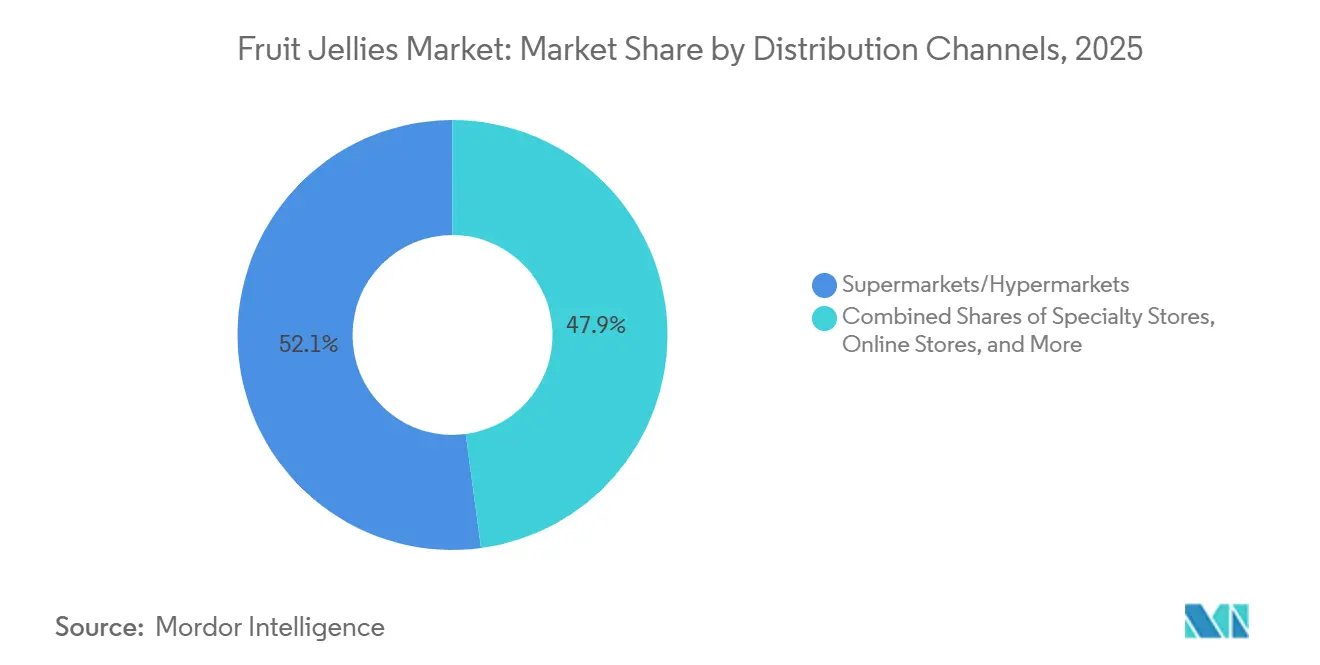

- By distribution channel, supermarkets and hypermarkets accounted for 52.12% of 2025 sales, yet online retail is advancing at a 4.56% CAGR.

- By geography, North America contributed 38.28% of global revenue in 2025; Asia-Pacific is poised to deliver the highest regional CAGR of 4.58% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fruit Jellies Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer preference for natural and fruit-flavored confections | +0.8% | Global, with strongest uptake in North America and Western Europe | Medium term (2-4 years) |

| Innovation in flavors, textures, and premiumization | +0.7% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Rising health consciousness favors low-sugar, vitamin-enriched variants | +0.6% | Global, led by North America and Northern Europe | Long term (≥ 4 years) |

| Demand for clean-label, vegan, and allergen-free products | +0.5% | North America, Western Europe, Australia | Medium term (2-4 years) |

| Seasonal and festive gifting in regions like Europe and Asia | +0.4% | Europe (Christmas, Easter), Asia-Pacific (Lunar New Year, Diwali) | Short term (≤ 2 years) |

| Expansion of organized retail and e-commerce | +0.9% | Asia-Pacific core, spill-over to Middle East and Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Consumer Preference for Natural and Fruit-Flavored Confections

Consumers are increasingly examining ingredient lists, preferring recognizable fruit names over synthetic flavors. According to Mondelez's 2023 State of Snacking survey, 43% of global consumers review ingredient labels before purchasing, and 42% prioritize nutritional benefits in their snacks over indulgence. This trend is driving formulators to adopt pectin-based gels, which offer clean-label credentials and support "made with real fruit" claims. In 2024, U.S. blueberry production increased by 23%, with 46% of the harvest designated for processing, ensuring a steady supply for natural colorants and flavor concentrates, as reported by the USDA[1]Source: United States Department of Agriculture, “Fruit and Tree Nuts Outlook 2024-2025,” usda.gov. Additionally, USDA data showed that strawberry frozen-pack volumes reached 343.3 million pounds in 2024, enhancing their availability for jelly applications. Regulatory support is reinforcing this shift; the FDA's 21 CFR Part 101 requires percent-juice declarations when fruit terms appear on labels, encouraging brands to use authentic fruit content instead of artificial essences. As a result, traditional jellies are being reformulated with higher fruit solids, reducing the sensory gap with premium preserves and driving up price points.

Innovation in Flavors, Textures, and Premiumization

Texture layering and exotic flavor pairings are reshaping the premium tier of the candy market. In April 2025, HARIBO enhanced its Starmix line with foam-egg and foam-heart inclusions, merging chewy fruit jelly bases with aerated toppings for a unique mouthfeel. Mars, in 2025-2026, unveiled Skittles Gummies Fuego, fusing spicy-sour profiles with tropical fruit notes, aiming to attract younger consumers in search of novelty. Perfetti Van Melle, in May 2025, launched Mentos Discovery Roll, which combines botanical extracts with fruit jellies, appealing to those who see confections as mood enhancers. These brands are tapping into sugar-reduction platforms like Incredo Sugar, which boosts sweetness perception by 30-50% without altering flavor systems. Premiumization efforts are bolstered by sustainable packaging; a survey by Mondelez found 82% of consumers are willing to pay a premium for products in recyclable or bio-based materials. This blend of sensory innovation and eco-consciousness is broadening market reach, moving beyond conventional candy aisles into specialty retail and gifting sectors.

Rising Health Consciousness Favors Low-Sugar, Vitamin-Enriched Variants

Fruit jellies are transitioning from indulgent treats to wellness-oriented snacks through functional fortification. The better-for-you snacks segment, valued at USD 40.9 billion in 2025, is projected to grow to USD 54.4 billion by 2035, with fruit-pectin jellies identified as a significant growth driver. Brands are incorporating vitamins C, D, and B-complex, along with probiotics and adaptogens, into jelly formulations, effectively masking medicinal flavors with fruit acids. High-fructose corn syrup is being substituted with Stevia Reb M and monk fruit mogrosides, which provide zero-calorie sweetness without the metallic aftertaste associated with earlier stevia extracts. D-allulose, a rare sugar offering 70% of sucrose's sweetness with minimal glycemic impact, is gaining popularity in North American and European markets. Regulatory support is aiding this shift; the FDA's nutrient content claim guidelines allow jellies to be labeled as a "good source of vitamin C" if they deliver 10% of the daily value per serving, encouraging fortification. However, a challenge persists: vitamin-enriched jellies are priced 20-30% higher than traditional options, limiting their reach in price-sensitive markets. As ingredient costs decrease and consumer awareness improves, functional jellies are expected to gain market share from both traditional confections and dietary supplements.

Demand for Clean-Label, Vegan, and Allergen-Free Products

Allergen-free certifications and plant-based gelling agents are expanding the reach of fruit jellies to consumer segments previously excluded. In vegan formulations, pectin—extracted from citrus peel or apple pomace—replaces gelatin. Additionally, xanthan gum and locust bean gum provide texture without relying on animal-derived inputs. The FDA, under the Food Allergen Labeling and Consumer Protection Act, requires disclosure of the top 8 allergens. Brands avoiding these allergens can label their products as "free from," appealing to parents of children with dietary restrictions. In November 2025, HARIBO collaborated with K-pop star JENNIE to launch vegan jelly hearts, targeting Gen Z consumers who prioritize ethical sourcing and transparency. The clean-label trend is further driven by retail gatekeepers, particularly major European supermarket chains, which now demand full disclosure of ingredient origins from suppliers. This has pushed formulators to eliminate synthetic colors and preservatives. These regulatory and commercial pressures are transforming the supply chain. Smaller co-packers, often unable to meet audit requirements due to inadequate traceability systems, are losing ground. Consequently, brands are consolidating production with vertically integrated manufacturers that manage fruit sourcing and ensure traceability from farm to package.

Restraint Impact Analysis

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High sugar content and artificial additives raise health concerns | -0.5% | Global, most acute in North America and Western Europe | Medium term (2-4 years) |

| Intense competition from gummies, chocolates, and healthier snacks | -0.4% | Global, with pressure intensifying in North America | Short term (≤ 2 years) |

| Stringent food safety and labeling regulations | -0.2% | North America, European Union, Australia | Long term (≥ 4 years) |

| Volatility in fruit prices and supply chain disruptions | -0.3% | Global, with acute impact in North America (citrus) and Europe (berries) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Sugar Content and Artificial Additives Raise Health Concerns

Sugar content in traditional fruit jellies—often 50-60% by weight—positions the category in direct conflict with public-health campaigns targeting added sugars. The FDA's updated Nutrition Facts label requires separate disclosure of added sugars, making high-sugar confections more transparent to consumers and vulnerable to taxation[2]Source: U.S. Food and Drug Administration, “Food Labeling & Nutrition—21 CFR Part 101,” fda.gov. Several European municipalities have proposed sugar levies on confectionery exceeding 10 grams per 100 grams, which would encompass most fruit jellies. Artificial colors, particularly azo dyes like Allura Red and Tartrazine, face consumer backlash despite regulatory approval; brands are reformulating with anthocyanins from berries and carotenoids from carrots, but these natural alternatives cost 2-3 times more and exhibit lower color stability under light and heat. The shift to natural colors and reduced sugar is compressing margins, as reformulation requires pilot-plant trials and sensory validation that can span 12-18 months. Smaller brands lacking R&D budgets are exiting the category or accepting private-label contracts, accelerating market concentration.

Intense Competition from Gummies, Chocolates, and Healthier Snacks

Fruit jellies are caught between the appeal of indulgent chocolates and the functionality of gummies. Gummy vitamins and CBD-infused gummies have adopted the fruit-jelly format, promoting wellness benefits that traditional jellies lack. Meanwhile, chocolate confections, priced 3-4 times higher per kilogram, capitalize on cocoa's indulgent image, often pushing fruit jellies into lower value tiers across many markets. The 'better-for-you' snacks segment, growing at an annual rate of 2.9%, is drawing health-conscious consumers who might otherwise choose low-sugar jellies. Products like dried fruit snacks, nut-and-fruit bars, and freeze-dried fruit crisps offer authentic fruit content without the gelling agents and preservatives that some consumers view with skepticism. Brands are increasingly merging category boundaries: Mars' Skittles Gummies Fuego bridges the gap between candy and snack, while HARIBO's foam-layered Starmix imitates the textural complexity of premium chocolates. However, this format innovation requires substantial investment in co-extrusion and aeration equipment, a cost feasible only for the largest manufacturers, thereby strengthening the competitive edge of established global players.

Segment Analysis

By Product Type: Functional Variants Gain Traction

Functional jellies are expanding at a 5.12% CAGR, materially faster than the wider fruit jellies market. They capture shoppers looking for vitamin boosts, collagen, or probiotic claims without swallowing pills. Traditional lines still delivered 65.17% of 2025 revenue because they dominate gifting and impulse displays. However, the segment’s volume edge masks a profit gap: fortified SKUs retail at 20-30% premiums and enjoy pharmacy placement that insulates them from confectionery discounting. Two of the top five global launches in 2025 combined vitamin C enrichment with reduced-sugar matrices, signaling convergence rather than cannibalization. FDA guidance allowing “good source” claims once a serving hits 10% DV of vitamin C enables brands to upgrade incumbent recipes without full repositioning.

Traditional sub-segments remain strategically important for cash flow and regional nostalgia. HARIBO’s foam-egg refresh reinforced how micro-texture tweaks can reignite heritage lines. Percent-juice disclosure rules incentivize higher fruit solids, letting classic SKUs borrow halo effects from functional peers. Over the forecast horizon, functional products are expected to account for 42% of absolute dollar growth in the fruit jellies market, cementing their status as the primary innovation frontier.

Note: Segment shares of all individual segments available upon report purchase

By Packaging Type: Sustainability Drives Format Shift

Cups and jars captured 48.23% of 2025 sales, buoyed by gifting aesthetics and sturdy shelf displays. Despite this, pouches and sachets are on track for a 4.88% CAGR, propelled by mono-material advances that slash lifecycle emissions by up to 60% compared with glass. The fruit jelly market is therefore transitioning from rigid to flexible, mirroring beverage pouch adoption in juice. Retail mandates for “Made for Recycling” icons accelerate the shift; Germany already requires proof of recyclability for shelf entry in several chains. Brands adopting Packiro laminates absorbed a 10-15% cost lift but gained secondary placements in eco aisles, offsetting margin dilution.

Bottles and cans cater to on-the-go snacking but face cannibalization from resealable pouches that weigh less and enable portion control. Some premium producers now deploy a triple-format strategy: rigid glass for seasonal gifts, lightweight cups for mass retail, and stand-up pouches for e-commerce kits. Mars Wrigley reports that format rather than flavor now drives 54% of incremental purchases in U.S. convenience stores. As carbon-accounting disclosures move from voluntary to mandatory in Europe, pouch adoption is poised to accelerate, making packaging a core competitive lever within the fruit jellies market.

By Distribution Channel: E-Commerce Reshapes Discovery

Supermarkets and hypermarkets still deliver 52.12% of the fruit jellies market revenue, offering visibility, multisensory sampling, and holiday end-caps. Yet online retail, growing 4.56% a year, is outpacing all offline formats. Social platforms have redefined discovery; 74% of confection buyers admit purchasing after first seeing a product online, often through influencer unboxings. HARIBO’s vegan hearts sold direct-to-consumer in Asia within 24 hours of launch, generating 15 million hashtag views. Brands capture 15-20 percentage-point higher gross margins when shipping directly, offsetting cold-chain costs in warm climates by using heat-tolerant recipes.

Convenience stores thrive on immediacy and single-serve packs; Mars notes that 40% of U.S. jelly sales through c-stores occur within two feet of the checkout. Specialty and health-food shops, though niche, serve as proving grounds for collagen- or adaptogen-laden concepts before national rollouts. Collectively, the fragmentation of channels compels manufacturers to adopt omnichannel pricing and inventory-replenishment systems to avoid stockouts that tarnish launch momentum.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

In 2025, North America contributed 38.28% of the global fruit jellies revenue, driven by established gifting traditions, premium market positioning, and high per-capita confectionery consumption. Cultural factors, such as increased demand during Halloween, Christmas, and Easter, along with structural advantages like organized retail and cold-chain logistics, reinforce the region's leadership. However, supply chain disruptions are impacting cost stability. USDA data revealed a 74% year-over-year increase in processing orange prices in 2024, alongside a 35% decline in Florida's orange production. This forced formulators to shift to apple, blueberry, or synthetic flavor carriers. In January 2025, apple grower prices rose by 20%. Although peach harvests increased by 22%, heat-related quality issues limited the availability of clingstone peaches for processing. These rising input costs are compressing margins and driving consolidation, as smaller brands struggle to manage procurement challenges. Regulatory oversight is also intensifying; the FDA's Compliance Program 7321.005 now includes fruit jellies, requiring percent-juice declarations and allergen labeling, which increases compliance costs. Despite these obstacles, North America's mature market structure and consumers' willingness to pay premiums for functional and clean-label products maintain its revenue leadership.

Asia-Pacific is projected to grow at an annual rate of 4.58% through 2031, supported by the expansion of organized retail in tier-2 cities, rising disposable incomes, and cultural gifting practices. Japan's omiyage tradition drives consistent demand for regionally branded fruit jellies, often featuring local fruits like yuzu or ume. Similarly, China's Lunar New Year and India's Diwali generate seasonal demand spikes comparable to Western holiday trends. Meiji Holdings and Morinaga capitalize on these occasions by launching limited-edition flavors tied to seasonal harvests, creating urgency among consumers. E-commerce is experiencing significant growth in Southeast Asia, enabling niche brands to bypass traditional distribution channels and connect with consumers through targeted social media campaigns. However, challenges such as high last-mile logistics costs and the need for temperature-controlled shipping in tropical climates persist. To address these issues, brands are developing ambient-stable formulations that can withstand transit temperatures of 30-35°C without compromising texture. In China, domestic players like Guanshengyuan and Hsu Fu Chi (a Nestlé subsidiary) benefit from vertical integration in fruit sourcing and expertise in local flavors, creating significant barriers for Western competitors.

Europe combines mature Western markets with emerging opportunities in the East, achieving steady growth through premiumization and sustainability initiatives. Christmas and Easter drive 30-40% volume increases, with fruit jellies marketed as premium boxed assortments alongside chocolates. Germany, the UK, and France lead consumption, supported by HARIBO's strong market presence and extensive retail penetration. However, regulatory pressures on sugar content and artificial colors are intensifying. Some municipalities are proposing sugar levies on confectioneries with more than 10 grams of sugar per 100 grams. In response, brands are reformulating with natural colorants like anthocyanins from berries and carotenoids from carrots. These alternatives, however, are 2-3 times more expensive and less color-stable than artificial options, as noted in the Journal of Food Science[3]Source: Institute of Food Technologists (IFT). "Natural Colors and Gelling Agents in Confectionery Applications." ift.onlinelibrary.wiley.com. Eastern Europe and Russia offer growth potential with the expansion of organized retail, but geopolitical tensions and currency fluctuations pose challenges for long-term planning. Meanwhile, South America and the Middle East-Africa, though smaller markets, are growing steadily. Local companies like Arcor in Argentina and others in Brazil are increasing investments in production capacity and distribution, targeting both domestic markets and exports to neighboring regions.

Competitive Landscape

The fruit jellies market exhibits moderate concentration, scoring 6 out of 10, reflecting a landscape where global incumbents coexist with regional specialists and private-label challengers. HARIBO, Mars, Perfetti Van Melle, and Ferrara (post-Jelly Belly acquisition in November 2023) command significant shelf space through vertical integration, multi-format SKU portfolios, and long-standing retailer relationships. However, their dominance is not absolute; regional players like Arcor in South America, Meiji and Morinaga in Japan, and Yupi Indo in Southeast Asia leverage local flavor expertise, cultural gifting traditions, and lower distribution costs to defend home markets.

Mars Wrigley's convenience-store data reveals a strategic vulnerability for incumbents: fruity confections are increasingly purchased based on package format—pouches, resealable bags, single-serve cups—rather than brand loyalty, suggesting that format innovation and point-of-sale visibility now outweigh legacy brand equity. This shift is opening white-space opportunities for agile entrants that can deliver sustainable packaging, functional fortification, or allergen-free certifications faster than global players burdened by legacy production lines. Technology adoption is fragmenting the competitive landscape, as brands deploy sugar-reduction platforms, natural-color extraction, and flexible packaging to differentiate. Incredo Sugar's crystal-restructuring technology, which amplifies sweetness perception by 30-50%, allows brands to cut sugar content without reformulating flavor systems, addressing health concerns while maintaining sensory appeal Incredo.

Packiro's recyclable mono-plastic pouches and FSC-certified paper laminates enable "Made for Recycling" certifications that resonate with sustainability-conscious consumers, though these formats add 10-15% to packaging costs Packiro. Patent filings in pectin-based gelling systems and natural-flavor encapsulation are accelerating, indicating R&D investment by both incumbents and emerging players. Smaller brands targeting functional niches—vitamin-enriched, probiotic-infused, or adaptogen-loaded jellies—are capturing share in pharmacy and health-food channels previously closed to confections, forcing incumbents to either acquire disruptors or launch competing SKUs. The net effect is a market in transition, where scale sustains volume leadership but innovation velocity determines margin expansion and long-term relevance.

Fruit Jellies Industry Leaders

-

Perfetti van Melle

-

HARIBO GmbH & Co. KG

-

Ferrera Candy Company

-

Jelly Belly Candy Company

-

Cloetta AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Premier Foods has introduced McDougalls No Added Sugar Vegan Jelly, a gelatin-free dessert targeted at UK school caterers to meet HFSS, School Food Standards, vegan, gluten-free, and allergen-free requirements.

- April 2025: Oddball, a New York-based startup, introduced a ready-to-eat, animal-free jelly snack made with fruit and plant-based ingredients, including agar and carob, targeting the Jell-O and fruit snack categories. Available in mango, grape, double berry, and pink grapefruit flavors inspired by Asian agar-agar desserts, each 2.75-oz cup contains under 60 calories.

- April 2025: Japanese food company St Cousair, via its US subsidiary Stair Inc. (SCI), acquired Kelly's Jelly, an Oregon-based producer of pepper jelly and fruit spreads in the northwestern United States. Pepper jelly is available in different fruit flavors.

Global Fruit Jellies Market Report Scope

The scope of this report is limited to fruit jellies used as a confectionery product and does not include fruit spreads. The global fruit jellies market is segmented by ingredient type into High Methoxyl Pectin (HMP) and Low Methoxyl Pectin (LMP) and by distribution channel into Supermarkets/Hypermarkets, Convenience Stores, Online CHannel and other channels. The market is also segmented by geography to understand the market opportunity and emerging trends in the top countries across regions such as North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

| Traditional Fruit Jellies |

| Functional/Fortified Jellies |

| Pouches & Sachets |

| Cups & Jars |

| Bottles |

| Cans & Others |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Specialty Stores |

| Online retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Belgium | |

| Poland | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Saouth America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| By Product Type | Traditional Fruit Jellies | |

| Functional/Fortified Jellies | ||

| By Packaging Type | Pouches & Sachets | |

| Cups & Jars | ||

| Bottles | ||

| Cans & Others | ||

| By Distribution Channels | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Specialty Stores | ||

| Online retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Belgium | ||

| Poland | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Saouth America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the fruit jellies market in 2026?

The fruit jellies market size reached USD 1.42 billion in 2026 and is forecast to climb to USD 1.75 billion by 2031 at a 4.23% CAGR.

Which product type is growing fastest within fruit jellies?

Functional and fortified jellies are advancing at a 5.12% CAGR through 2031, outpacing traditional formats.

Which region offers the highest growth outlook?

Asia-Pacific is set to deliver the fastest regional CAGR of 4.58% as organized retail and e-commerce expand.

How strict are labeling rules for fruit jellies in the United States?

FDA Compliance Program 7321.005 targets fruit jellies, requiring percent-juice declarations and stringent allergen labeling, which raises compliance costs.