| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 6.00 % |

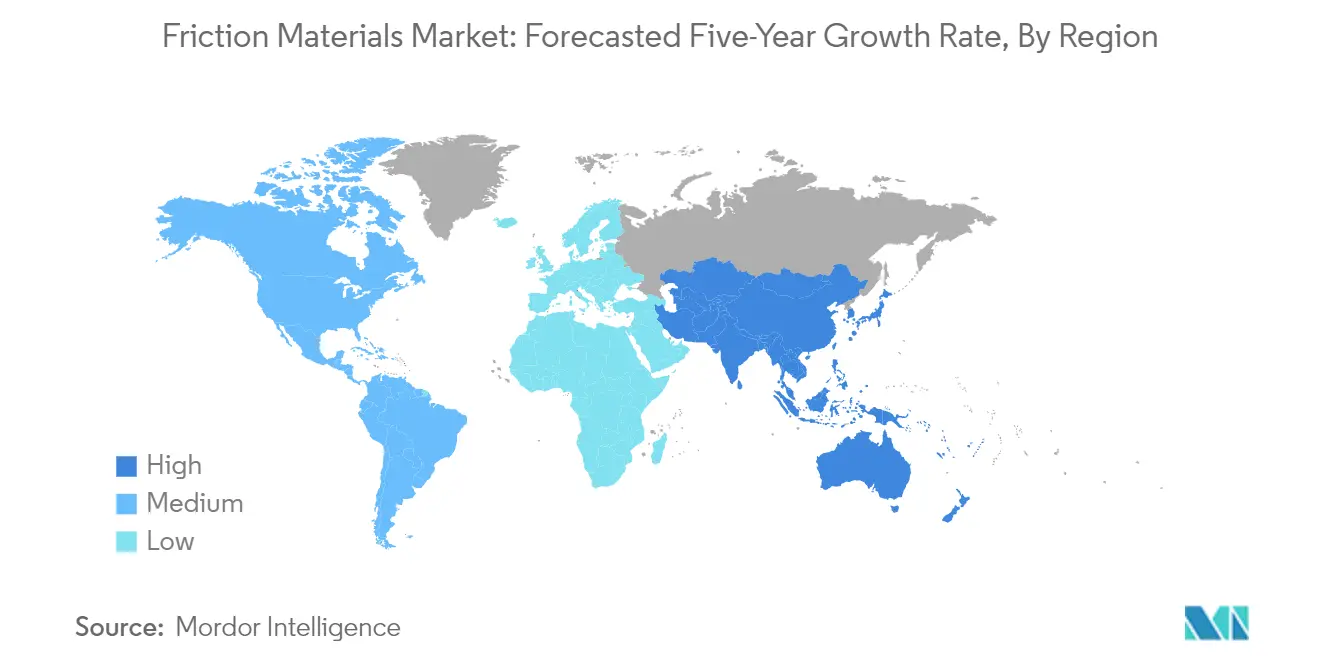

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Friction Materials Market Analysis

The Friction Material Market is expected to register a CAGR of greater than 6% during the forecast period.

The friction materials industry is undergoing significant transformation driven by technological advancements and changing market dynamics. Major manufacturers are investing heavily in expanding their production capabilities and developing innovative solutions. For instance, in 2023, Knorr-Bremse announced an investment of EUR 25 million in new production lines to strengthen its product portfolio, while ITT Inc. revealed a EUR 50 million expansion of its friction production facility in Termoli, Italy. These investments reflect the industry's commitment to meeting evolving market demands and maintaining competitive advantages through enhanced manufacturing capabilities.

The aerospace sector has emerged as a crucial growth driver for high-performance friction materials, with major manufacturers reporting significant delivery volumes. Boeing delivered 480 aircraft in 2022, marking a 41% increase from the previous year, while Airbus achieved 661 commercial aircraft deliveries in the same period. The trend continues to strengthen, as evidenced by Air India's landmark order of 470 aircraft worth approximately USD 80 billion in early 2023, indicating robust demand for aerospace-grade friction materials.

Environmental sustainability and regulatory compliance have become central themes shaping product development in the friction materials industry. Manufacturers are increasingly focusing on developing copper-free and eco-friendly brake materials in response to stringent environmental regulations. This shift has led to accelerated research and development activities in alternative materials such as ceramic composites and organic compounds, fundamentally transforming the industry's approach to product innovation and environmental responsibility.

Strategic consolidation and technological innovation are reshaping the competitive landscape of the brake friction market. Companies are forming strategic partnerships and pursuing acquisitions to enhance their technological capabilities and market presence. The industry is witnessing a notable shift toward the development of smart friction materials with embedded sensors for real-time monitoring and predictive maintenance capabilities, particularly in high-performance applications. These advancements are driving the industry toward more sophisticated and efficient friction material solutions while opening new opportunities in emerging applications.

Friction Materials Market Trends

Growing Need for Industrial Machinery

The increasing industrialization across the globe has been driving the demand for industrial machinery, consequently boosting the friction materials market. According to recent data from the Ministry of Statistics and Program Implementation (MOSPI), the Index of Industrial Production (IIP) reached 144.7 in October 2023, with manufacturing, mining, and electricity sectors recording indices of 141.8, 127.4, and 203.8 respectively. The manufacturing sector's robust growth has particularly intensified the need for heavy machinery equipped with advanced braking and control systems that rely heavily on high-performance friction materials, including industrial friction components like brake lining. These materials are essential components in various industrial applications, including conveyor systems, winches, grinding mills, and power take-offs, where precise control over friction and wear is crucial for operational efficiency and safety.

The friction materials industry has witnessed substantial growth due to the rising automation and modernization of production processes across various industrial sectors. In December 2023, major equipment manufacturer Lingong Heavy Machinery (LGMG) inaugurated a new manufacturing facility with an investment exceeding USD 140 million, while Bobcat Company announced plans for a USD 300 million manufacturing facility in Monterrey, scheduled to begin production in early 2026. These industrial expansions demonstrate the growing demand for machinery that requires sophisticated friction materials for braking systems, clutches, and other mechanical components. The materials often consist of a combination of substances, including binder resins, reinforcements like aramid or carbon fibers, and various fillers, which are crucial for optimizing performance in demanding industrial applications.

Understand The Key Trends Shaping This Market

Download PDF

Growing Demand from the Automotive Industry

The automotive sector continues to be a primary driver for the friction materials market, with increasing vehicle production and the industry's transition toward electric mobility creating new opportunities. According to the National Automobile Dealers Association (NADA), new vehicle sales in the United States are projected to increase by 6.6% to 14.6 million units in 2023, indicating a robust demand for automotive friction materials in automotive applications. The materials are extensively used in automotive braking systems, clutches, and transmission components, with manufacturers developing specialized formulations to meet the specific requirements of different vehicle types. The industry has also witnessed significant investments in production capacity expansion, with major manufacturers like Knorr-Bremse AG announcing investments of EUR 25 million in July 2023 to strengthen its product portfolio and increase production to 9 million units annually.

The evolution of automotive technology and increasing focus on vehicle safety have led to enhanced demand for advanced friction materials. In 2023, several manufacturers have introduced innovative products to meet these requirements, such as Akebono Brake Corporation's launch of five new premium disc brake pad material lines expanding coverage for over 3 million operational vehicles. Additionally, NAPA Auto Parts' partnership with BREMBO in April 2023 to market comprehensive braking solutions through NAPA Auto Parts stores demonstrates the growing market opportunities. The industry is also witnessing a shift toward more environmentally friendly materials, with manufacturers developing copper-free and low-metal content friction materials to comply with environmental regulations while maintaining high performance standards. This trend is particularly evident in the electric vehicle segment, where specialized brake lining and clutch material are required to meet the unique braking and energy recovery requirements of these vehicles.

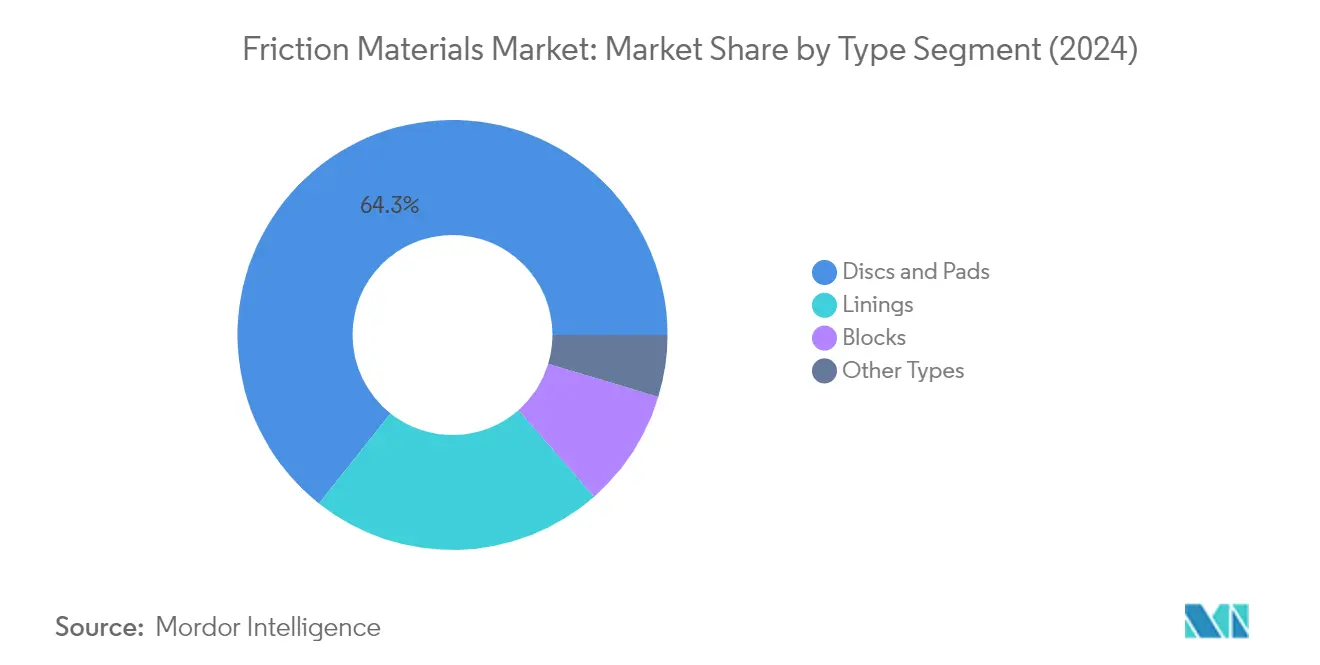

Segment Analysis: Type

Discs and Pads Segment in Friction Materials Market

The Discs and Pads segment dominates the global friction materials market, commanding approximately 64% of the total market share in 2024. This segment's prominence is primarily attributed to its extensive application in automotive and transportation sectors, where disc brakes and brake pad material play a crucial role in vehicle safety systems. The segment is also experiencing the highest growth rate with a projected growth of nearly 5% from 2024 to 2029, driven by increasing automotive production, stringent safety regulations, and the growing emphasis on high-performance braking systems. The segment's growth is further supported by technological advancements in material composition, including the development of ceramic and semi-metallic variants that offer superior performance characteristics such as better heat dissipation, reduced noise, and longer service life.

Remaining Segments in Friction Materials Market by Type

The remaining segments in the friction materials market include Linings, Blocks, and Other Types, each serving specific applications across various industries. The Linings segment represents a significant portion of the market, primarily used in drum brake systems for commercial vehicles, railways, and industrial machinery. The Blocks segment plays a vital role in heavy-duty applications, particularly in railway systems and industrial equipment where high braking force is required. The Other Types segment encompasses specialized friction materials used in specific applications such as industrial machinery, mining equipment, and aerospace systems. These segments collectively contribute to the market's diversity and cater to specialized requirements across different end-user industries, offering various friction characteristics and performance specifications based on specific application needs.

Segment Analysis: Material

Semi-Metallic Segment in Friction Materials Market

The semi-metallic segment dominates the global friction materials market, accounting for approximately 44% market share in 2024. Semi-metallic friction materials offer excellent friction and heat resistance capabilities, leading to effective braking even at high speeds and temperatures. These materials maintain consistent performance under sustained braking conditions, unlike organic materials that can fade under high heat. The segment's dominance is largely driven by its widespread adoption in everyday driving applications due to their balanced performance and comfort characteristics. Semi-metallic friction materials are particularly popular in trucks and buses due to their high stopping power and durability, while some high-performance vehicles utilize them for their excellent braking capabilities.

Ceramic Segment in Friction Materials Market

The ceramic friction segment is experiencing rapid growth in the friction materials market from 2024-2029, driven by increasing demand for high-performance braking solutions. Ceramic friction materials possess exceptional properties including high strength, abrasion resistance, and superior thermal stability, making them ideal for demanding applications. These materials exhibit minimal fade even at high temperatures and their low thermal expansion coefficient ensures consistent performance under varying operating conditions. The segment's growth is further propelled by the materials' resistance to corrosion and chemical degradation, making them suitable for harsh environments like marine and industrial settings. Additionally, ceramic materials typically generate less noise and vibration compared to other materials, enhancing comfort and reducing noise pollution, which is particularly valuable in high-end automotive applications.

Remaining Segments in Material Segmentation

The friction materials market encompasses several other significant segments including sintered metal, aramid fiber, asbestos, and other specialized materials. Sintered metal materials are particularly valued in heavy-duty applications due to their exceptional durability and heat dissipation properties. Aramid fibers have gained prominence as an eco-friendly alternative, offering high strength and temperature resistance while being lightweight. Despite historical usage, asbestos-based materials are seeing declining adoption due to environmental and health concerns, with many regions implementing strict regulations against their use. Other specialized materials continue to emerge as manufacturers invest in research and development to meet specific application requirements and environmental standards.

Segment Analysis: Application

Clutch and Brake Systems Segment in Friction Materials Market

The clutch facing and brake systems segment dominates the global friction materials market, accounting for approximately 75% of the total market volume in 2024. This segment's prominence is primarily attributed to the extensive use of friction materials in automotive and transportation industry applications, where these components play a crucial role in vehicle safety and performance. The segment's growth is driven by the rising demand for brake material in brake systems to slow down wheels or bring them to a halt, as well as in clutch systems for effective torque transfer and transmission control. The segment is expected to maintain its market leadership while growing at around 5% CAGR from 2024 to 2029, supported by increasing vehicle production, stringent safety regulations, and the growing need for high-performance braking systems across various industries. The development of advanced friction materials with improved durability and performance characteristics, particularly for electric vehicles and heavy-duty applications, further strengthens this segment's market position.

Gear Tooth Systems Segment in Friction Materials Market

The gear tooth systems segment represents a vital application area in the friction materials market, focusing on precision and efficiency in power transmission systems. This segment plays a crucial role in minimizing wear and tear while maintaining optimal performance in various industrial applications. The application of friction materials in gear tooth systems helps in controlling friction between sliding surfaces, which is essential for efficient power transmission and reducing energy losses. The segment's importance is particularly evident in heavy machinery, manufacturing equipment, and industrial applications where precise control over gear movement and wear resistance is critical. The development of advanced friction materials specifically designed for gear tooth applications, incorporating features like improved thermal stability and reduced noise generation, continues to drive innovation in this segment. The growing focus on industrial automation and the need for more efficient power transmission systems across various sectors maintains the segment's significance in the overall friction materials market.

Segment Analysis: End-User Industry

Automotive Segment in Friction Materials Market

The automotive segment continues to dominate the global friction materials market, commanding approximately 63% of the total market volume in 2024, while also maintaining the highest growth trajectory with a projected growth rate of around 5% during 2024-2029. This segment's prominence is primarily driven by the increasing global automotive production and sales volumes, with major automotive manufacturers expanding their production capacities worldwide. The segment's growth is further bolstered by the rising demand for electric vehicles, particularly in regions like North America and Europe, where government initiatives are actively promoting EV adoption. Additionally, the aftermarket sector for automotive friction materials remains robust due to regular maintenance requirements and the growing vehicle parc globally. The segment's dominance is particularly evident in countries like China, India, and the United States, where automotive production continues to show strong growth momentum.

Remaining Segments in End-User Industry

The railway, aerospace, machinery, and other end-user industries collectively represent significant opportunities in the friction materials market. The railway segment maintains a strong presence due to the ongoing expansion of rail networks and high-speed train projects across various regions, particularly in developing economies. The aerospace segment, while smaller in volume, is characterized by high-value applications in commercial and military aircraft, where advanced friction materials are essential for critical braking systems. The machinery segment continues to grow steadily, driven by increasing industrial automation and the need for reliable friction materials in various manufacturing applications. Other end-user industries, including mining, wind energy, and construction equipment, contribute to the market's diversity by requiring specialized friction materials for their unique operational requirements. Each of these segments plays a vital role in driving innovation and technological advancement in friction material development.

Friction Material Market Geography Segment Analysis

Friction Materials Market in Asia-Pacific

The Asia-Pacific region represents the largest market for friction materials globally, driven by substantial manufacturing activities across the automotive, aerospace, railway, and industrial sectors. The region's dominance is supported by the presence of major automotive manufacturing hubs in China, Japan, and South Korea, along with rapidly growing industrial bases in India. The market is characterized by increasing investments in research and development, particularly in developing advanced friction materials for electric vehicles and high-speed railways. Countries like China and India are witnessing significant growth in their automotive and industrial sectors, while Japan and South Korea continue to be technological leaders in friction material innovation.

Friction Materials Market in China

China dominates the Asia-Pacific friction materials market, holding approximately 52% share of the regional market in 2024. The country's leadership position is reinforced by its massive automotive production capacity and extensive railway network. China's friction materials industry benefits from strong government support for industrial development and technological advancement. The country has established itself as a major hub for friction materials manufacturing, with numerous domestic and international companies operating production facilities. The market is further strengthened by China's growing aerospace sector and increasing focus on electric vehicle production.

Friction Materials Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 9% during 2024-2029. The country's rapid growth is driven by increasing automotive production, expanding railway infrastructure, and growing industrial activities. India's friction materials market is witnessing significant investments in manufacturing capabilities and technological advancements. The government's push for domestic manufacturing through initiatives like 'Make in India' has attracted several international friction materials manufacturers to establish production facilities in the country. The market is also benefiting from the growing demand for electric vehicles and the modernization of railway systems.

Friction Materials Market in North America

The North American friction materials market is characterized by advanced manufacturing capabilities and high technological adoption rates across the United States, Canada, and Mexico. The region's market is driven by strict safety regulations, a growing automotive aftermarket sector, and increasing aerospace activities. The presence of major automotive and aerospace manufacturers, coupled with significant research and development investments, continues to shape the market landscape. The region also benefits from the growing trend toward electric vehicles and the increasing focus on sustainable friction materials.

Friction Materials Market in United States

The United States maintains its position as the largest market in North America, commanding approximately 64% of the regional market in 2024. The country's dominant position is supported by its robust automotive industry, extensive aerospace sector, and strong presence of major friction materials manufacturers. The market benefits from advanced research and development facilities, stringent quality standards, and continuous technological innovations. The United States leads in the development of eco-friendly friction materials and advanced braking systems for electric vehicles.

Friction Materials Market in Mexico

Mexico demonstrates the highest growth potential in North America, with an expected growth rate of approximately 5% during 2024-2029. The country's growth is primarily driven by increasing automotive production, expanding manufacturing capabilities, and rising foreign investments in the automotive sector. Mexico's strategic location and trade agreements with major economies have attracted significant investments from international friction materials manufacturers. The country is increasingly becoming a preferred manufacturing hub for automotive components, including brake linings and brake materials, supported by competitive labor costs and improving infrastructure.

Friction Materials Market in Europe

The European friction materials market is characterized by its strong focus on technological innovation and environmental sustainability. The region's market landscape is shaped by stringent environmental regulations, particularly regarding the use of copper and other materials in brake linings products. Countries across the region are witnessing significant developments in eco-friendly friction materials, especially for electric vehicles and high-speed rail applications.

Friction Materials Market in Germany

Germany maintains its position as the largest friction materials market in Europe, driven by its robust automotive manufacturing sector and strong presence in the railway industry. The country's market is characterized by high-quality standards and significant investments in research and development. German manufacturers are at the forefront of developing innovative friction materials for electric vehicles and high-performance applications.

Friction Materials Market Growth in Germany

Germany also leads the European region in terms of market growth, supported by its continuous technological advancements and strong industrial base. The country's growth is driven by increasing demand for premium vehicles, an expanding electric vehicle market, and ongoing developments in the railway sector. German manufacturers are actively investing in developing new brake materials compositions that meet increasingly stringent environmental regulations.

Friction Materials Market in South America

The South American friction materials market is primarily driven by developments in Brazil and Argentina, with Brazil emerging as both the largest and fastest-growing market in the region. The market is characterized by growing automotive production, increasing industrialization, and rising demand for commercial vehicles. The region's friction materials industry is witnessing gradual technological advancement, particularly in Brazil, where both domestic and international manufacturers are expanding their presence.

Friction Materials Market in Middle East and Africa

The Middle East and Africa region represents an emerging market for friction materials, with Saudi Arabia and South Africa leading the regional development. South Africa maintains its position as the largest market in the region, while Saudi Arabia demonstrates the highest growth potential. The market is driven by increasing automotive sales, growing industrial activities, and rising investments in transportation infrastructure across both regions. The development of new manufacturing facilities and increasing focus on localization of production are key trends shaping the market landscape.

Get Analysis on Important Geographic Markets

Download PDF

Friction Materials Industry Overview

Top Companies in Friction Materials Market

The global friction materials market is characterized by continuous product innovation and technological advancement, with leading companies focusing on developing sustainable and environmentally friendly materials. Companies are investing heavily in research and development to create copper-free brake pads and other eco-friendly solutions, particularly targeting the growing electric vehicle segment. Operational agility is demonstrated through strategic manufacturing facility expansions and upgrades, particularly in key automotive manufacturing regions. Market leaders are strengthening their positions through strategic collaborations and long-term supply agreements with major automotive manufacturers. Geographic expansion remains a key focus, with companies establishing production facilities and distribution networks across emerging markets while simultaneously strengthening their presence in established markets through acquisitions and joint ventures.

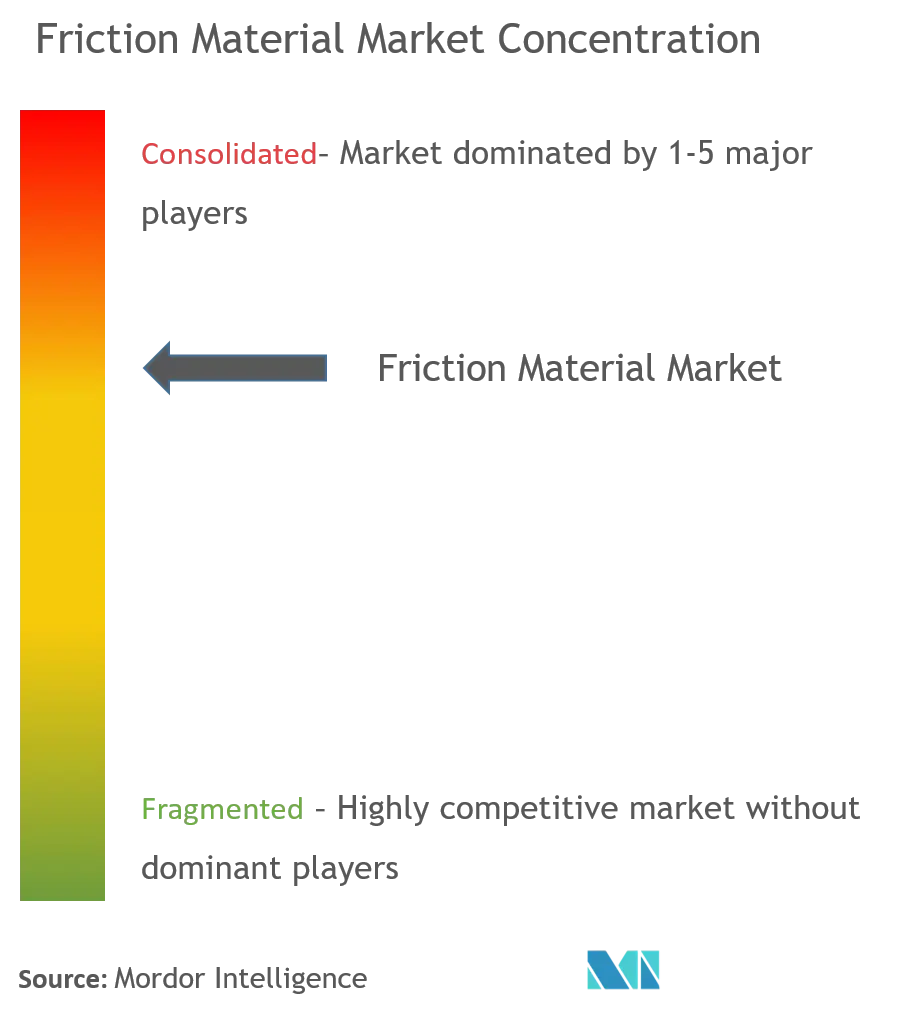

Fragmented Market with Strong Regional Players

The friction materials market exhibits a fragmented structure with a mix of global conglomerates and specialized manufacturers competing across different regions and application segments. Major players like Japan Brake Industrial Co. Ltd, Robert Bosch LLC, and Brembo SpA maintain significant market presence through their established brand reputation, extensive distribution networks, and technological capabilities. The market is characterized by the presence of both vertically integrated companies that control their entire value chain and specialized manufacturers focusing on specific product segments or regional markets.

The industry has witnessed notable merger and acquisition activities, particularly aimed at strengthening market positions and expanding product portfolios. Companies are increasingly pursuing strategic acquisitions to gain access to new technologies, expand their geographic footprint, or enhance their manufacturing capabilities. The acquisition of TMD Friction by AEQUITA demonstrates the ongoing consolidation trends in the market, as companies seek to achieve economies of scale and strengthen their competitive positions through strategic partnerships and collaborations.

Innovation and Sustainability Drive Future Success

Success in the friction materials market increasingly depends on companies' ability to develop innovative, sustainable products while maintaining cost competitiveness. Market leaders are investing in advanced manufacturing technologies and automation to improve operational efficiency and product quality. Companies are also focusing on developing specialized products for emerging applications, particularly in the electric vehicle segment, while maintaining strong relationships with key automotive manufacturers through long-term supply agreements and collaborative development projects.

The market presents significant barriers to entry due to high initial investment requirements, stringent quality standards, and established relationships between major players and end-users. Future success will depend on companies' ability to navigate increasing environmental regulations, particularly regarding the use of certain materials in friction products. Companies must also address the growing bargaining power of large automotive manufacturers while managing the threat of substitute products and materials. Building strong distribution networks, maintaining product quality, and investing in research and development will remain crucial for both established players and new entrants seeking to gain market share.

Friction Materials Market Leaders

-

Nisshinbo Holdings Inc.

-

AKEBONO BRAKE INDUSTRY CO., LTD.

-

ITT INC.

-

Miba AG

-

ANAND Group

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Friction Materials Market News

In November 2020, Brembo SpA signed an agreement to acquire a 100% stake in SBS Friction AS, a manufacturer of sintered and organic material brake pads for motorbikes. The agreement was expected to be completed by the first quarter of 2021, which will enhance the company's product portfolio.

In October 2018, Tenneco Inc. completed the acquisition of Federal-Mogul LLC, a manufacturer of friction material, thereby enhancing the company's product portfolio.

Friction Materials Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Growing Need for Industrial Machinery

- 4.1.2 Other Drivers

-

4.2 Restraints

- 4.2.1 High Maintenance and Cost of Friction Materials

- 4.2.2 Impact of COVID-19 Outbreak

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION

-

5.1 Type

- 5.1.1 Discs

- 5.1.2 Pads

- 5.1.3 Blocks

- 5.1.4 Linings

- 5.1.5 Other Types

-

5.2 Material

- 5.2.1 Ceramic

- 5.2.2 Asbestos

- 5.2.3 Semi-metallic

- 5.2.4 Sintered Metals

- 5.2.5 Aramid Fibers

- 5.2.6 Other Materials

-

5.3 Application

- 5.3.1 Clutch and Brake Systems

- 5.3.2 Gear Tooth Systems

- 5.3.3 Other Applications

-

5.4 End-user Industry

- 5.4.1 Automotive

- 5.4.2 Railway

- 5.4.3 Aerospace

- 5.4.4 Mining

- 5.4.5 Other End-user Industries

-

5.5 Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 ABS Friction

- 6.4.2 ANAND Group

- 6.4.3 Akebono Brake Industry Co. Ltd

- 6.4.4 Brembo SpA

- 6.4.5 ITT Inc.

- 6.4.6 Japan Brake Industrial Co. Ltd

- 6.4.7 Miba AG

- 6.4.8 Nisshinbo Holdings Inc.

- 6.4.9 Tenneco Inc.

- 6.4.10 Yantai Haina Brake Technology Co. Ltd

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Demand for High Thermal-resistant Friction Materials

- 7.2 Other Opportunities

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Friction Materials Industry Segmentation

Friction materials are used to provide or enhance friction to decelerate or stop the system. Friction materials majorly find applications in braking systems, where they are used in brake pads and brake linings. The friction material market is segmented by type, material, application, end-user industry, and geography. By type, the market is segmented into discs, pads, blocks, linings, and other types. By material, the market is segmented into ceramic, asbestos, semi-metallic, sintered metals, aramid fibers, and other materials. By application, the market is segmented into clutch and brake systems, gear tooth systems, and other applications. By end-user industry, the market is segmented into automotive, railway, aerospace, mining, and other end-user industries. The report also covers the market sizes and forecasts for the friction material market in 15 countries across the major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD million).

| Type | Discs | ||

| Pads | |||

| Blocks | |||

| Linings | |||

| Other Types | |||

| Material | Ceramic | ||

| Asbestos | |||

| Semi-metallic | |||

| Sintered Metals | |||

| Aramid Fibers | |||

| Other Materials | |||

| Application | Clutch and Brake Systems | ||

| Gear Tooth Systems | |||

| Other Applications | |||

| End-user Industry | Automotive | ||

| Railway | |||

| Aerospace | |||

| Mining | |||

| Other End-user Industries | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Friction Materials Market Research FAQs

What is the current Friction Material Market size?

The Friction Material Market is projected to register a CAGR of greater than 6% during the forecast period (2025-2030)

Who are the key players in Friction Material Market?

Nisshinbo Holdings Inc., AKEBONO BRAKE INDUSTRY CO., LTD., ITT INC., Miba AG and ANAND Group are the major companies operating in the Friction Material Market.

Which is the fastest growing region in Friction Material Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Friction Material Market?

In 2025, the Asia Pacific accounts for the largest market share in Friction Material Market.

What years does this Friction Material Market cover?

The report covers the Friction Material Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Friction Material Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Friction Material Market Research

Mordor Intelligence provides a comprehensive analysis of the friction material market. We leverage extensive expertise in automotive friction and related sectors. Our detailed research covers the full spectrum of brake material applications. This includes brake lining technologies, brake pad material innovations, and developments in clutch material. The report offers an in-depth analysis of friction product evolution across industrial friction applications, railway friction systems, and specialized ceramic friction solutions.

Stakeholders in the brake lining industry benefit from our actionable insights. These insights are available in an easy-to-read report PDF format for immediate download. The analysis addresses crucial developments in clutch facing technologies and emerging trends in the brake friction market. Our research methodology ensures thorough coverage of all market segments. This provides valuable intelligence for manufacturers, suppliers, and end-users involved in friction applications. The report delivers strategic insights essential for understanding market dynamics and future growth opportunities in this vital industrial sector.