Market Overview

| Study Period | 2019 - 2030 |

|---|---|

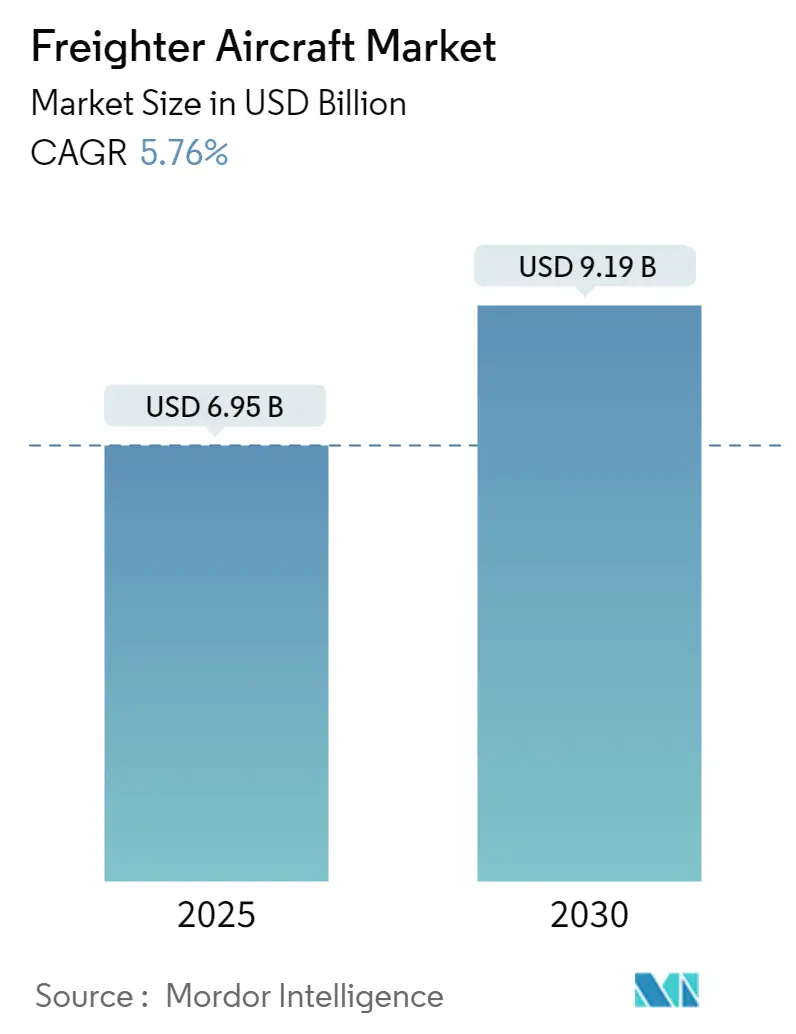

| Market Size (2025) | USD 6.95 Billion |

| Market Size (2030) | USD 9.19 Billion |

| Growth Rate (2025 - 2030) | 5.76% CAGR |

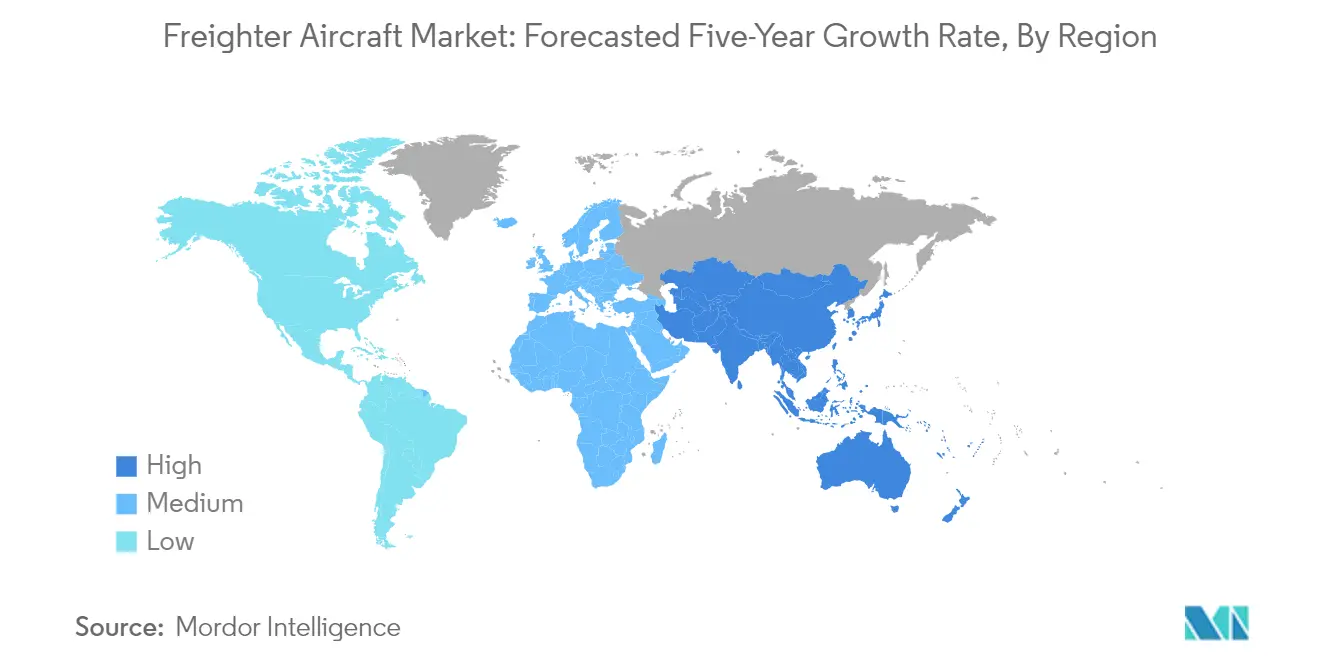

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

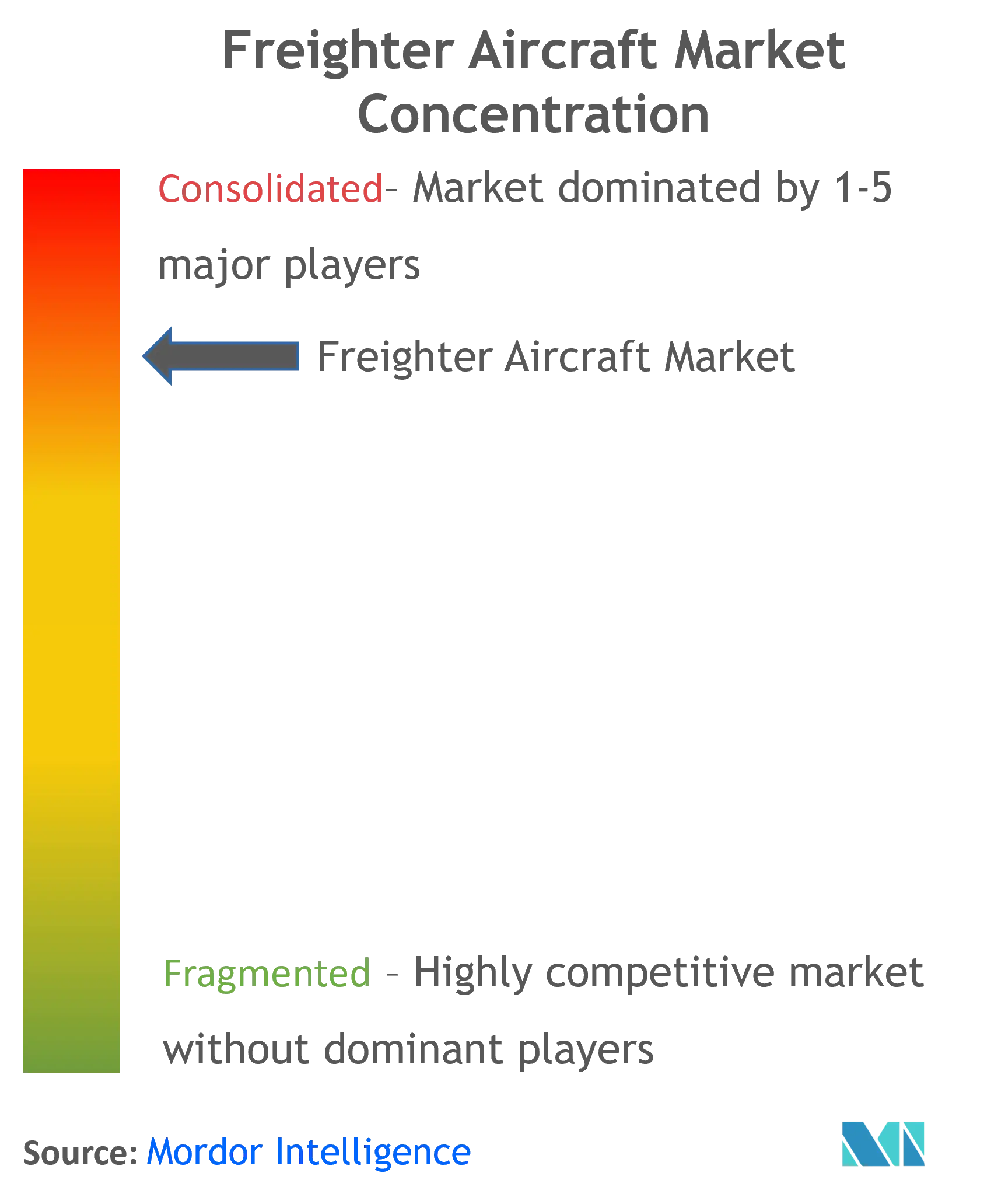

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Freighter Aircraft Market Analysis by Mordor Intelligence

The Freighter Aircraft Market size is estimated at USD 6.95 billion in 2025, and is expected to reach USD 9.19 billion by 2030, at a CAGR of 5.76% during the forecast period (2025-2030).

The freighter aircraft industry is experiencing significant transformation driven by evolving global trade dynamics and technological advancements. According to the International Air Transport Association (IATA), air cargo currently transports over USD 6 trillion worth of goods annually, accounting for approximately 35% of world trade by value. The industry's digital transformation is accelerating, with carriers increasingly investing in artificial intelligence and automation for process optimization. Major airlines are implementing advanced tracking systems and digital booking platforms, enabling real-time shipment monitoring and streamlined operations. The focus on sustainability has also intensified, with carriers exploring Sustainable Aviation Fuel (SAF) options that can potentially reduce net carbon emissions by up to 80% compared to traditional jet fuel.

The e-commerce boom continues to reshape the air cargo landscape, creating unprecedented demand for cargo aircraft and conversion services. IATA forecasts that cross-border e-commerce sales will surge by 13% year-over-year in 2023, reaching USD 2.1 trillion, with approximately 80% of international online sales being delivered via air shipping. This growth has sparked a wave of passenger-to-freighter conversion projects globally, with major aviation companies establishing new conversion facilities. In 2023, significant developments include Boeing's partnership with GMR Aero Technic in India for B737 conversions, Embraer's establishment of a conversion line in China, and Israel Aerospace Industries' new facility in Abu Dhabi.

The industry is witnessing substantial fleet modernization and capacity expansion initiatives by major carriers. Air India announced plans in 2023 to increase its cargo-handling capacity by 300% over the next five years through strategic fleet expansion and infrastructure investments. Airlines are increasingly focusing on developing specialized cargo handling facilities and implementing advanced logistics solutions to improve operational efficiency. The integration of digital technologies has led to the emergence of sophisticated cargo management systems, enabling better capacity utilization and route optimization.

The cargo aircraft sector is experiencing a notable shift towards more efficient and environmentally conscious operations. Airlines are investing in next-generation freighter aircraft that offer improved fuel efficiency and reduced environmental impact. The industry is also seeing increased adoption of predictive maintenance technologies and smart cargo handling systems. Major carriers are forming strategic partnerships with technology providers to enhance their digital capabilities, while simultaneously working on developing sustainable practices in their cargo operations. These developments are complemented by the growing trend of airport modernization projects worldwide, focusing on creating dedicated cargo handling facilities with advanced automation capabilities.

Global Freighter Aircraft Market Trends and Insights

Growth in Air Cargo Volume Driving Deliveries of Freighter Aircraft

The expansion of the global economy and rising air cargo volumes are driving significant investments in freighter aircraft deliveries worldwide. According to the International Air Transport Association (IATA), global air freight traffic reached 60.3 million metric tons in 2022, demonstrating the robust demand for cargo aircraft services. This sustained demand has prompted various airline companies to expand their freighter aircraft fleets through new aircraft acquisitions and passenger-to-freighter conversions. For instance, in July 2023, Atlas Air took delivery of a Boeing B777-200 Freighter to operate on behalf of MSC Mediterranean Shipping Company SA, marking the second of four planned B777-200 Freighters for their long-term ACMI agreement.

The increasing air cargo volumes have catalyzed multiple strategic fleet expansions across the industry in 2023. UPS Airlines welcomed its latest Boeing B767-300F freighter in July 2023, pushing its freighter aircraft purchases to 75 units. In another significant development, Air Tanzania received its first B767-300 Freighter from Boeing in June 2023, marking the first direct B767 Freighter delivery from Boeing to an African carrier. The Cargo Management team, a subsidiary of Air Transport Services Group (ATSG), demonstrated the industry's momentum by delivering six converted freighters under lease in August 2023 to customers globally, including strategic placements with operators like Raya Airways, Cargojet, Georgian Airlines, and Amerijet.

Understand The Key Trends Shaping This Market

Download PDF

Formation of Bilateral Trade Agreements to Foster Air Cargo Volumes

The establishment of new bilateral trade agreements and the strengthening of existing partnerships have become crucial drivers for air cargo growth, creating enhanced opportunities for air freighter operations. According to global trade data from the United Nations, trade growth remained positive for both goods and services during the first quarter of 2023, with global trade in goods witnessing an increase of 1.9% compared to Q4 2022. These figures have been achievable owing to the revival in China's economic activity and the growing trade of pharmaceuticals, leading to increased demand for air cargo services.

Recent trade agreements have directly impacted air cargo operations and infrastructure development. In March 2023, the United States and Japan entered into a strategic agreement to strengthen critical mineral supply chains, building upon their 2019 trade agreement and fostering increased air cargo movement between the two nations. The impact of such agreements is evident in regional developments, such as Delhi Air Cargo's expansion in reefer cargo exports in April 2023, leveraging recent bilateral free trade deals to increase Indian air freight shippers' global market reach. The geographical proximity of international trade has remained relatively stable, with notable growth in the physical proximity of trade since late 2022, while there has been a strategic concentration of global trade among major trade relationships, necessitating robust cargo plane capabilities to support these evolving trade patterns.

Segment Analysis: Aircraft Type

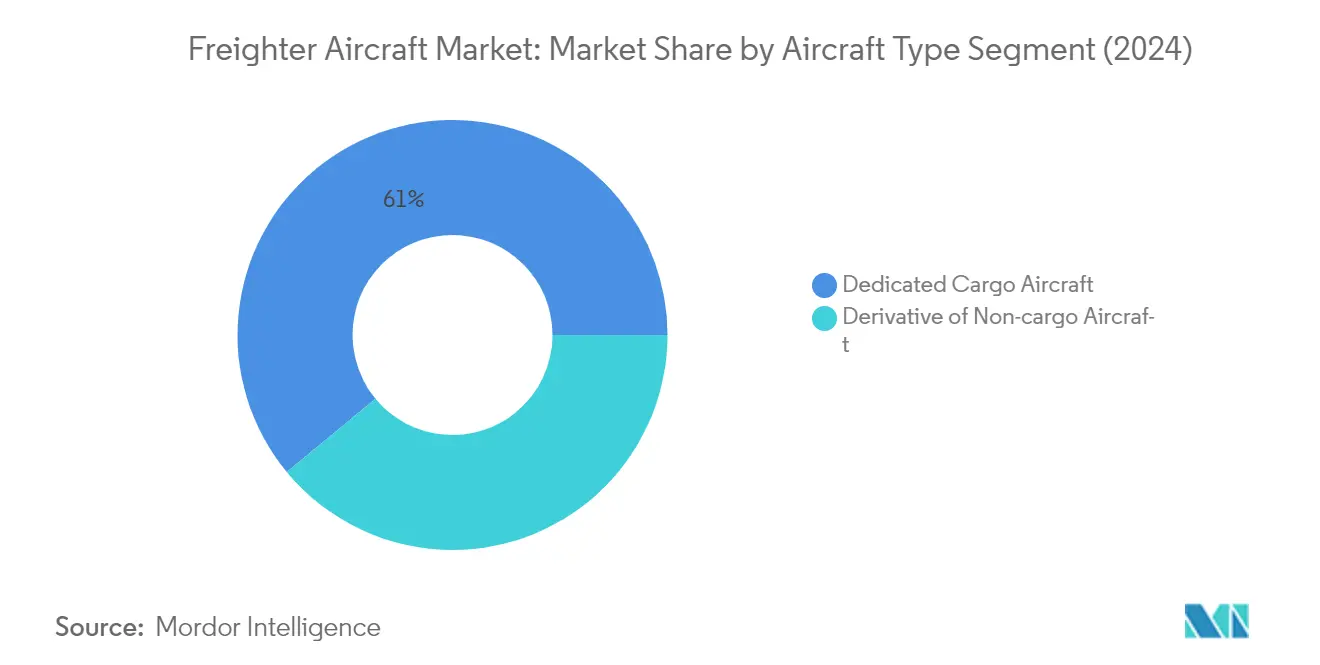

Dedicated Cargo Aircraft Segment in Freighter Aircraft Market

The Dedicated Cargo Aircraft segment continues to dominate the global freighter aircraft market, commanding approximately 61% market share in 2024. This segment's prominence is driven by the increasing expenditure on the procurement of new dedicated freighter planes by major carriers worldwide. Airlines are investing heavily in purpose-built cargo airplanes to meet the growing demands of global air freight transportation. The segment's strength is further reinforced by the robust demand from e-commerce businesses and the need for specialized cargo handling capabilities. Major manufacturers like Boeing and Airbus are focusing on developing newer generation dedicated freighter aircraft with improved fuel efficiency and larger cargo capacities, which continues to attract investments from air cargo operators looking to modernize their fleets.

Derivative of Non-cargo Aircraft Segment in Freighter Aircraft Market

The Derivative of Non-cargo Aircraft segment is experiencing the fastest growth in the freighter aircraft market, with an expected CAGR of approximately 6% during 2024-2029. This remarkable growth is primarily driven by the surge in passenger-to-freighter conversions, which provides a cost-effective solution for airlines facing air cargo capacity constraints. These converted passenger planes are particularly well-suited for carrying lighter, more voluminous cargo such as e-commerce packages. The conversion process involves significant modifications, including floor reinforcement for freight handling and changes to fire detection, ventilation, and temperature control systems to comply with cargo aircraft standards. The segment's growth is further supported by various passenger-to-freighter (P2F) programs for aircraft types including B737, B757, A320, and A321, offering airlines flexible options to expand their cargo capabilities.

Segment Analysis: Engine Type

Turbofan Segment in Freighter Aircraft Market

The turbofan segment continues to dominate the global freighter aircraft market, commanding approximately 88% market share in 2024. This substantial market position is attributed to the increasing expenditure on the procurement of new dedicated freighter aircraft and the rising focus on converting passenger aircraft to freighter configurations. The segment's growth is particularly driven by wide-body aircraft that can accommodate containerized and palletized freight on upper and lower (belly) decks, making them versatile for both short domestic and long international routes. Major developments supporting this segment include Airbus's newest freighter, the A350F, which brings latest-generation innovation with reduced fuel burn and CO2 emissions, and the A330-200F that meets cargo business needs in mid-size and long-haul segments. Additionally, conversion programs like A330P2F and A321P2F are providing cost-effective options to end-users, further strengthening the turbofan segment's market position.

Turboprop Segment in Freighter Aircraft Market

The turboprop segment plays a crucial role in regional and short-haul cargo operations within the freight aircraft market. These aircraft are particularly well-suited for accessing airports with shorter runways and operating in challenging environments. Turboprop cargo aircraft, with payload capacities of up to 10,000 pounds, are ideal for carrying small packages and perishable goods, making them essential for regional air cargo networks. The segment's efficiency in short-haul operations and lower operating costs compared to turbofan aircraft make it an attractive option for regional cargo operators. Companies like ATR have been actively developing new turboprop freighter variants and conversion options to meet the growing demand for regional air cargo transportation.

Freighter Aircraft Market Geography Segment Analysis

Freighter Aircraft Market in North America

North America represents a dominant force in the global freighter aircraft market, driven by the presence of major cargo airlines and extensive air transportation infrastructure. The United States and Canada form the key markets in this region, with both countries showing strong commitment to modernizing their freighter aircraft fleets and expanding air freight capabilities. The region benefits from well-established aerospace manufacturing facilities, advanced technological capabilities, and strategic partnerships between airlines and freight operators. The presence of major players like FedEx, UPS, and Atlas Air continues to drive market growth through fleet expansion and modernization initiatives.

Freighter Aircraft Market in United States

The United States maintains its position as the largest market in North America, commanding approximately 99% of the regional market share in 2024. The country's dominance is supported by the presence of the world's largest freighter aircraft fleet and continued investments in aviation infrastructure. Major American carriers are actively expanding their freighter fleets, with FedEx Express operating 697 aircraft across eight different variants. The country's robust e-commerce sector and growing international trade relations continue to drive demand for air cargo services. Boeing's establishment of new freighter conversion facilities and increasing focus on developing fuel-efficient aircraft further strengthen the United States' position in the market.

Freighter Aircraft Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 4% during 2024-2029. The country's strategic focus on expanding air cargo capabilities and modernizing existing infrastructure drives this growth. Canadian airlines are actively investing in fleet expansion and future programs, with major carriers like Air Canada and WestJet establishing dedicated cargo divisions. The country's domestic e-commerce market has shown remarkable growth, creating increased demand for freighter aircraft services. Cargojet's significant investment in aircraft conversion programs and strategic partnerships with global logistics providers further demonstrates Canada's commitment to expanding its presence in the freighter aircraft market.

Freighter Aircraft Market in Europe

Europe represents a significant market for freighter aircraft, characterized by a diverse mix of established carriers and emerging players across various countries. The region's market is primarily driven by countries including Germany, the United Kingdom, France, and Russia, each contributing uniquely to the market dynamics. The European market benefits from strong trade relationships, advanced aviation infrastructure, and increasing focus on sustainable air cargo operations. The presence of major aircraft manufacturers and conversion facilities further strengthens the region's position in the global market.

Freighter Aircraft Market in United Kingdom

The United Kingdom stands as the largest market in Europe, holding approximately 41% of the regional market share in 2024. The country's strategic position as a global trading hub and its well-developed aviation infrastructure support this leadership position. Major carriers like DHL Aviation UK and West Atlantic UK continue to expand their operations, while new entrants like One Air are introducing innovative freighter aircraft solutions. The country's airports, particularly Heathrow and London Luton, serve as crucial cargo handling points, facilitating significant freight movement across the region.

Freighter Aircraft Market in Germany

Germany emerges as the fastest-growing market in Europe, with a projected growth rate of approximately 5% during 2024-2029. The country's strong manufacturing base and position as a key logistics hub drive this growth trajectory. Major operators like Lufthansa Cargo and DHL are actively expanding their freighter aircraft fleets and establishing new cargo routes. The country's airports, particularly Frankfurt and Leipzig/Halle, serve as major cargo hubs, while increasing investment in sustainable aviation solutions and digital transformation initiatives further support market expansion.

Freighter Aircraft Market in Asia-Pacific

The Asia-Pacific region demonstrates robust growth potential in the freighter aircraft market, driven by rapid industrialization and expanding e-commerce sectors across various countries. The region encompasses major markets including China, India, Japan, and South Korea, each contributing to the dynamic market landscape. Increasing trade volumes, growing domestic consumption, and significant investments in aviation infrastructure characterize the regional market. The emergence of new freighter aircraft carriers and expansion of existing operators further strengthens the market's growth trajectory.

Freighter Aircraft Market in China

China maintains its position as the largest market in the Asia-Pacific region, driven by its extensive manufacturing base and growing e-commerce sector. The country's strategic focus on expanding air cargo capabilities includes establishing new conversion facilities and partnerships with global aviation players. Major Chinese airlines are actively expanding their freighter fleets, while increasing domestic and international trade volumes support continued market growth.

Freighter Aircraft Market in China - Growth Leader

China also leads the region in terms of growth rate, supported by significant investments in aviation infrastructure and increasing demand for air cargo services. The country's focus on developing new cargo routes and expanding existing facilities drives market expansion. The establishment of new passenger-to-freighter conversion lines and partnerships with global aviation players further strengthens China's position as a growth leader in the region.

Freighter Aircraft Market in Latin America

The Latin American freighter aircraft market shows promising development, with Brazil emerging as both the largest and fastest-growing market in the region. The market benefits from increasing e-commerce activities and growing trade relationships with global partners. Major carriers in the region are actively expanding their freighter fleets and establishing new cargo routes to meet growing demand. The establishment of new cargo facilities and increasing focus on modernizing existing infrastructure support continued market growth across the region.

Freighter Aircraft Market in Middle East and Africa

The Middle East and Africa region demonstrates significant potential in the freighter aircraft market, with the United Arab Emirates leading as both the largest and fastest-growing market. The region benefits from its strategic geographic position connecting major global trade routes. Countries including Saudi Arabia and Turkey are making significant investments in aviation infrastructure and expanding their cargo capabilities. The establishment of new logistics centers and increasing focus on developing air cargo hubs support continued market growth across the region.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Top Companies in Freighter Aircraft Market

The freighter aircraft market is dominated by established aerospace manufacturers and conversion specialists, with Boeing and Airbus leading the pack, followed by companies like Textron, ATR, and IAI. The industry shows a strong focus on product innovation through the development of next-generation fuel-efficient freighter aircraft and conversion programs for passenger aircraft. Companies are investing heavily in expanding their conversion facilities globally while forming strategic partnerships with airlines and cargo operators. Operational agility is demonstrated through the integration of digital technologies and automation in aircraft manufacturing and conversion processes. Market leaders are also emphasizing sustainability initiatives, particularly in developing aircraft with reduced carbon emissions and improved fuel efficiency. Strategic expansion is evident through the establishment of new conversion lines, maintenance facilities, and technical support centers across key aviation hubs globally.

Consolidated Market with High Entry Barriers

The freighter aircraft market exhibits a highly consolidated structure dominated by global aerospace conglomerates with extensive manufacturing capabilities and technical expertise. These major players benefit from significant economies of scale, established supply chains, and long-standing relationships with airlines and cargo aircraft operators. The market shows limited penetration from new entrants due to high capital requirements, complex regulatory frameworks, and the need for specialized technical knowledge. The industry landscape is characterized by a mix of original equipment manufacturers and conversion specialists, with the latter focusing on passenger-to-freighter market conversions to meet growing cargo demand.

The market demonstrates active merger and acquisition activity, particularly in the freighter conversions market segment, as companies seek to expand their capabilities and geographic presence. Strategic partnerships and joint ventures are common, especially between manufacturers and regional maintenance, repair, and overhaul (MRO) providers. These collaborations enable companies to enhance their service offerings, access new markets, and share technical expertise. The industry also sees vertical integration attempts as larger players acquire smaller specialized firms to strengthen their position in specific market segments or geographic regions.

Innovation and Sustainability Drive Future Success

Success in the freighter aircraft market increasingly depends on companies' ability to innovate while maintaining operational efficiency and environmental sustainability. Incumbent players must focus on developing more fuel-efficient aircraft, expanding their conversion capabilities, and strengthening their aftermarket services to maintain their market position. Companies need to invest in digital technologies and automation to streamline operations and enhance customer experience. Building strong relationships with airlines and cargo operators through customized solutions and comprehensive support services is becoming increasingly crucial for market success.

For contenders looking to gain market share, specialization in niche segments and focus on regional markets present viable opportunities. Success factors include developing cost-effective conversion solutions, establishing strategic partnerships with established players, and investing in emerging technologies. The industry faces moderate substitution risk from alternative cargo transport modes, but air freight's speed and reliability advantages maintain its appeal. Regulatory requirements, particularly regarding emissions and safety standards, continue to shape market dynamics and influence investment decisions. Companies must maintain strong compliance frameworks while adapting to evolving environmental regulations and safety standards.

Freighter Aircraft Industry Leaders

-

The Boeing Company

-

Airbus SE

-

Textron Inc.

-

ATR

-

Singapore Technologies Engineering Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

June 2023: BBN Airlines launched the first Airbus A321 Passenger-to-Freighter converted cargo aircraft to Turkey. With this addition of the converted freighter, BBN Airlines' Turkish subsidiary now has five aircraft.

January 2023: Mountain Cargo, a FedEx feeder airline, announced it had become the first to operate Textron Aviation's new Cessna SkyCourierfreighter. Moreover, Textron Inc. delivered the first 50 Cessna SkyCouriertwin utility turboprop freighters to FedEx Express.

Global Freighter Aircraft Market Report Scope

A freighter or cargo aircraft is designed or converted for transportation of cargo rather than passengers. These aircraft types usually do not carry passengers and feature one or more large doors for loading cargo. They are operated by cargo airlines, civil passengers, private individuals, or the armed forces of individual countries.

The freighter aircraft market is segmented by aircraft type, engine type, and geography. By aircraft type, the market is segmented into dedicated cargo aircraft and derivative of non-cargo aircraft. By engine type, it is segmented into turboprop and turbofan. The report also offers the market size and forecasts for the freighter aircraft market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

Aircraft Type

| Dedicated Cargo Aircraft |

| Derivative of Non-cargo Aircraft |

Engine Type

| Turboprop Aircraft |

| Turbofan Aircraft |

Geography

| North America | United States |

| Canada | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Latin America | Brazil |

| Rest of Latin America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East and Africa |

| Aircraft Type | Dedicated Cargo Aircraft | |

| Derivative of Non-cargo Aircraft | ||

| Engine Type | Turboprop Aircraft | |

| Turbofan Aircraft | ||

| Geography | North America | United States |

| Canada | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Latin America | Brazil | |

| Rest of Latin America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the Freighter Aircraft Market?

The Freighter Aircraft Market size is expected to reach USD 6.95 billion in 2025 and grow at a CAGR of 5.76% to reach USD 9.19 billion by 2030.

What is the current Freighter Aircraft Market size?

In 2025, the Freighter Aircraft Market size is expected to reach USD 6.95 billion.

Who are the key players in Freighter Aircraft Market?

The Boeing Company, Airbus SE, Textron Inc., ATR and Singapore Technologies Engineering Ltd. are the major companies operating in the Freighter Aircraft Market.

Which is the fastest growing region in Freighter Aircraft Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Freighter Aircraft Market?

In 2025, the North America accounts for the largest market share in Freighter Aircraft Market.

What years does this Freighter Aircraft Market cover, and what was the market size in 2024?

In 2024, the Freighter Aircraft Market size was estimated at USD 6.55 billion. The report covers the Freighter Aircraft Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Freighter Aircraft Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: