Market Size of Frankfurt Data Center Industry

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2023 |

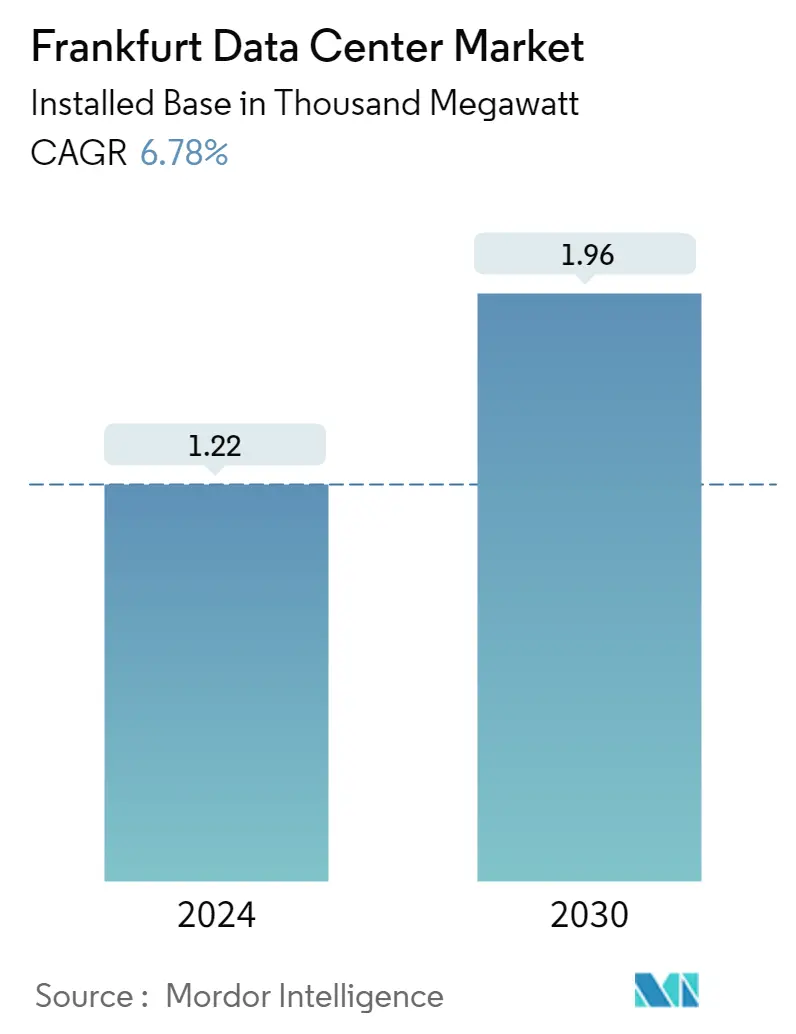

| Market Volume (2024) | 1.22 Thousand megawatt |

| Market Volume (2030) | 1.96 Thousand megawatt |

| CAGR (2024 - 2030) | 6.78 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Frankfurt Data Center Market Analysis

The Frankfurt Data Center Market size in terms of installed base is expected to grow from 1.22 Thousand megawatt in 2024 to 1.96 Thousand megawatt by 2030, at a CAGR of 6.78% during the forecast period (2024-2030).

- The main drivers anticipated to drive the market expansion are the increasing demand for energy-efficient data centers, considerable investment by colocation service and managed service providers, and expanding hyperscale data center building. Additionally, the development of big data, cloud computing, and the Internet of Things (IoT) has made it possible for businesses to invest in new data centers to preserve business continuity. Additionally, industrial development is expected to prosper due to the rising need for security, operational efficiency, improved mobility, and bandwidth. Software-based data centers boost industry growth by providing a higher level of automation.

- Frankfurt has undergone significant economic growth, becoming a financial and commercial center in Germany and then throughout Europe. The city's significance as the most significant financial center on the European mainland is highlighted by the presence of the European Central Bank, the German Stock Exchange, the German Central Bank, hundreds of commercial banks, and branches of foreign central banks. The city's digital transition has been accelerated by all of these financial institutions driving the data center demand in the country.

- The outbreak of the COVID-19 pandemic affected data center construction in the market studied as it has delayed the construction of several new facilities. Ongoing construction from enterprises and colocation service providers witnessed a halt. Projects pipeline with openings across Q4 2020 and Q1 2021 are majorly affected. The same has been attributed to data center infrastructure-related supply chain disruptions. With problematic imports already in place, the situation worsened as many vendors are dependent on importing IT and power and cooling infrastructure solutions.

- The increased demand from logistics, healthcare, e-commerce, and manufacturing sectors has attracted several cloud and colocation service providers to invest and expand their presence in the country. For instance, recently, Worldstream, a global IaaS services provider with company-owned data centers in the Netherlands and more than 15,000 dedicated servers installed announced the expansion of its presence across Europe with the deployment of a new data center in maincubes' FRA01 facility in Frankfurt, Germany. It includes the installation of a new Point-of-Presence for Worldstream's10Tbit/s global network. It allows Worldstream to offer a private cloud, dedicated servers, block and object storage, DDoS protection, colocation, and other IaaS services from Frankfurt.

- Moreover, to meet the rising demands of the customer, the firms are constructing new data centers in the region. For instance, in February 2022, The second stage of construction of one of Vantage's data center complexes in Frankfurt, Germany, has been revealed. On its 55MW EU campus (FRA1) in Offenbach, the business announced it would erect the second of three buildings there. When fully constructed, the plant would have a 16MW capacity and be 13,000 square meters (140,000 square feet) in size. It will begin serving customers in the first half of 2024.

- While the basic prices for electricity are similar across Europe, the electricity costs of German data centers are over six times higher than those of their European competitors due to taxes, charges, and network fees. Electricity accounts for approximately 50% of the operating costs of German data centers, which weakens the competitiveness of German data centers immensely. According to DgtlInfra (Digital Infrastructure), In 2020, the power supply of the existing data centers in Frankfurt, Germany, was 425 Megawatts, compared to Amsterdam at 390 Megawatts and Paris at 210 Megawatts, with leases to Amazon Web Services (AWS), Microsoft Azure, and Google Cloud, among others.

Frankfurt Data Center Industry Segmentation

A data center is a physical room, building, or facility that holds IT infrastructure used to construct, run, and provide applications and services and store and manage the data connected with those applications and services.

The Frankfurt Data Center Market is segmented by DC Size (Small, Medium, Large, Massive, Mega), by Tier Type (Tier 1&2, Tier 3, Tier 4), by Absorption (Utilized (Colocation Type (Retail, Wholescale, Hyperscale), End User ( Cloud & IT, Telecom, Media & Entertainment, Government, BFSI, Manufacturing, E-Commerce)) , Non-Utilized).

The market sizes and forecasts are provided in terms of volume (MW) for all the above segments.

| DC Size | |

| Small | |

| Medium | |

| Large | |

| Massive | |

| Mega |

| Tier Type | |

| Tier 1 & 2 | |

| Tier 3 | |

| Tier 4 |

| Absorption | |||||||||||||||||

| |||||||||||||||||

| Non-Utilized |

Frankfurt Data Center Market Size Summary

The Frankfurt Data Center market is poised for significant growth, driven by the increasing demand for energy-efficient solutions and substantial investments from colocation and managed service providers. The expansion of hyperscale data centers, coupled with advancements in big data, cloud computing, and the Internet of Things, has spurred businesses to invest in new facilities to ensure business continuity. Frankfurt's status as a major financial hub in Europe, with institutions like the European Central Bank and the German Stock Exchange, has further accelerated the digital transition, boosting data center demand. Despite challenges posed by the COVID-19 pandemic, which delayed construction and disrupted supply chains, the market has seen continued interest from sectors such as logistics, healthcare, and e-commerce, attracting global players like Worldstream and Vantage to expand their presence in the region.

The market landscape is moderately consolidated, with key players like Equinix, Digital Realty, and NTT actively investing in strategic partnerships and product developments to enhance their market share. The high operational costs due to electricity prices in Germany pose a challenge, yet the demand for faster and more efficient data processing continues to drive upgrades in network speeds. The introduction of Tier III facilities and the adoption of data center as a service (DCaaS) models offer businesses flexibility and cost-effectiveness, supporting their digital transformation efforts. Notable developments include the construction of a hyperscale data center campus by CloudHQ and the establishment of new facilities by companies like Mainova and Stack Infrastructure, highlighting the ongoing investment and expansion in Frankfurt's data center market.

Frankfurt Data Center Market Size - Table of Contents

-

1. MARKET SEGMENTATION

-

1.1 DC Size

-

1.1.1 Small

-

1.1.2 Medium

-

1.1.3 Large

-

1.1.4 Massive

-

1.1.5 Mega

-

-

1.2 Tier Type

-

1.2.1 Tier 1 & 2

-

1.2.2 Tier 3

-

1.2.3 Tier 4

-

-

1.3 Absorption

-

1.3.1 Utilized

-

1.3.1.1 Colocation Type

-

1.3.1.1.1 Retail

-

1.3.1.1.2 Wholesale

-

1.3.1.1.3 Hyperscale

-

-

1.3.1.2 End User

-

1.3.1.2.1 Cloud & IT

-

1.3.1.2.2 Telecom

-

1.3.1.2.3 Media & Entertainment

-

1.3.1.2.4 Government

-

1.3.1.2.5 BFSI

-

1.3.1.2.6 Manufacturing

-

1.3.1.2.7 E-Commerce

-

1.3.1.2.8 Other End User

-

-

-

1.3.2 Non-Utilized

-

-

Frankfurt Data Center Market Size FAQs

How big is the Frankfurt Data Center Market?

The Frankfurt Data Center Market size is expected to reach 1.22 thousand megawatt in 2024 and grow at a CAGR of 6.78% to reach 1.96 thousand megawatt by 2030.

What is the current Frankfurt Data Center Market size?

In 2024, the Frankfurt Data Center Market size is expected to reach 1.22 thousand megawatt.