France Electric Vehicle Charging Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

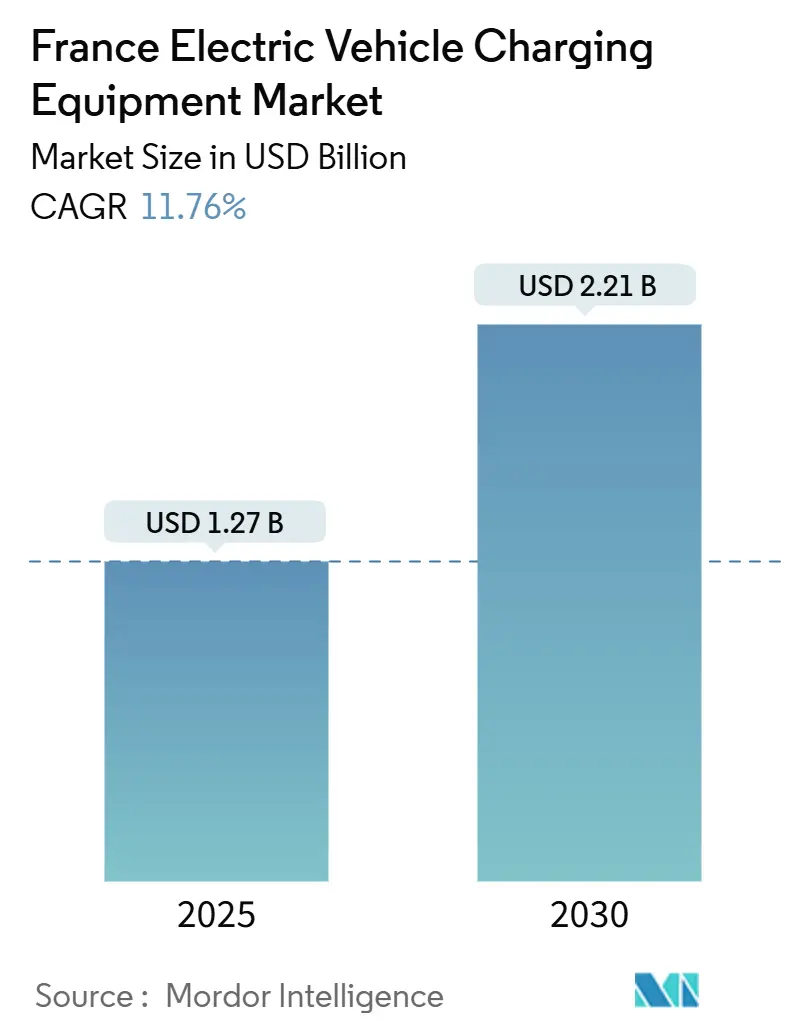

| Market Size (2025) | USD 1.27 Billion |

| Market Size (2030) | USD 2.21 Billion |

| Growth Rate (2025 - 2030) | 11.76% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Electric Vehicle Charging Equipment Market Analysis by Mordor Intelligence

The France Electric Vehicle Charging Equipment Market size is estimated at USD 1.27 billion in 2025, and is expected to reach USD 2.21 billion by 2030, at a CAGR of 11.76% during the forecast period (2025-2030).

Ongoing public-sector allocations of EUR 700 million for 2025 infrastructure, accelerating CAC-40 fleet electrification, and rapid megawatt-class deployments create a dual-track growth narrative in which high-utilization nodes coexist with still-dominant residential charging. Grid-ready urban cores capture a disproportionate share of capacity additions because connection queues average six months versus 18 months in rural areas. Corporate demand is amplifying competitive intensity as energy majors, utilities, and pure-play operators drive consolidation fueled by cybersecurity compliance costs and ISO 15118 upgrades. Meanwhile, dynamic residential tariffs and wallbox tax credits nurture the legacy home-charging base, even as depot economics reshape capital allocation strategies.

Key Report Takeaways

- By charging level, Level 2 equipment held 65.1% of the France electric vehicle charging equipment market share in 2024, while Megawatt Class units are poised to expand at a 30.8% CAGR to 2030.

- By installation site, Residential installations dominated with 79.9% revenue share in 2024, whereas Transportation Hubs are forecast to accelerate at a 27.5% CAGR through 2030.

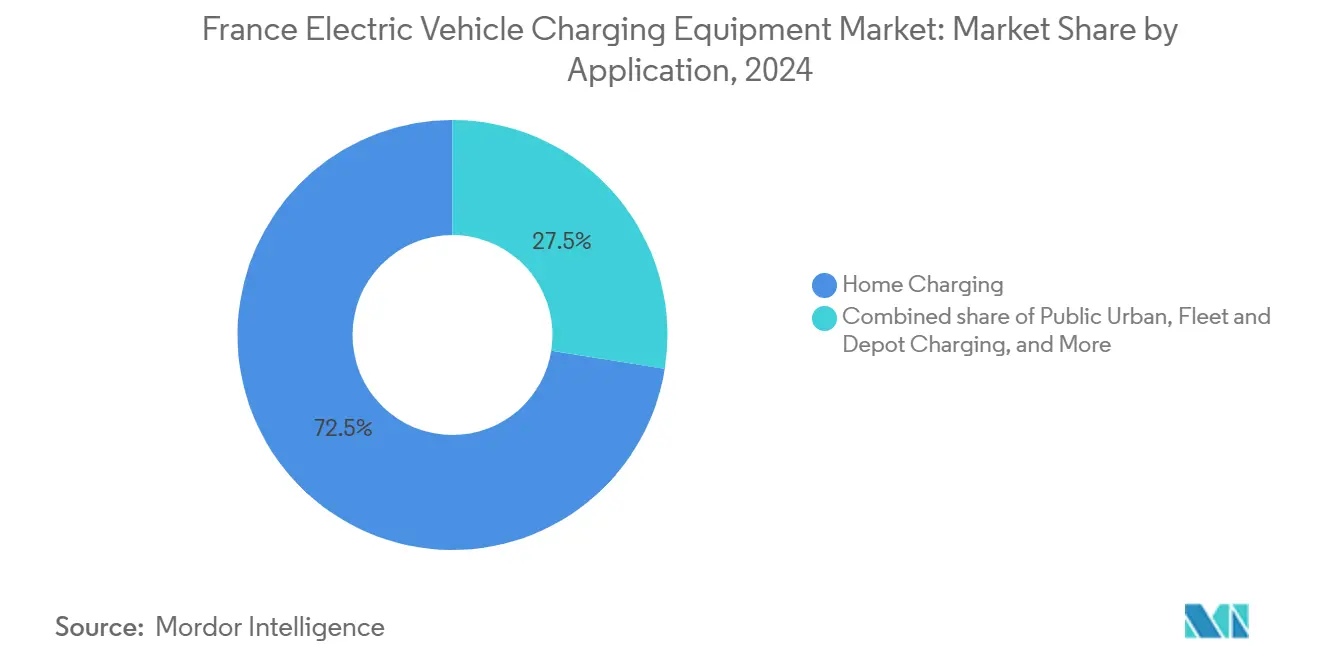

- By application, Home Charging accounted for 72.5% of the France electric vehicle charging equipment market size in 2024; Fleet and Depot Charging is advancing at a 32.1% CAGR between 2025-2030.

France Electric Vehicle Charging Equipment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government subsidies & purchase-bonus schemes | +2.3% | National, with concentration in Île-de-France, Auvergne-Rhône-Alpes | Short term (≤ 2 years) |

| Nationwide roll-out of fast-charging corridors (France Relance) | +1.8% | National, prioritizing TEN-T corridors and autoroute concessions | Medium term (2-4 years) |

| Corporate-fleet electrification targets of CAC-40 companies | +2.1% | National, with early gains in Paris, Lyon, Marseille metropolitan areas | Medium term (2-4 years) |

| Dynamic tariffs fostering residential smart-charger uptake | +1.4% | National, accelerated in Linky-equipped households (95% penetration) | Short term (≤ 2 years) |

| Second-life battery integration cutting TCO for operators | +0.9% | National, pilot deployments in Île-de-France, Nouvelle-Aquitaine | Long term (≥ 4 years) |

| ISO 15118 'Plug & Charge' compliance in public tenders | +1.2% | National, mandatory in AFIR-aligned public procurement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Subsidies & Purchase-Bonus Schemes

France’s EUR 700 million budget for 2025 stretches beyond consumer rebates to include grid-connection grants that cover up to 40% of transformer upgrades, smoothing capex hurdles for operators.[1]Ministère de l’Économie, “700 M€ pour accélérer l’infrastructure de recharge,” economie.gouv.fr Residential tax credits of EUR 300-500 per wallbox spurred 147,000 commercial charging ports by November 2024, yet fiscal tightening, evident in the suspension of the EUR 100-per-month EV lease after 50,000 sign-ups, signals a pivot toward high-utilization public assets.[2]International Energy Agency, “Global EV Outlook 2025,” iea.org The ecological bonus now caps eligible vehicle prices at EUR 47,000, pushing mass-market models toward Level 2 home chargers. Grid-connection co-financing drives rural deployments but leaves commercial capital clustering around urban retail sites. The resulting utilization gap challenges operators’ profit models outside metropolitan zones.

Nationwide Roll-Out of Fast-Charging Corridors (France Relance)

The program delivered 1,780 fast points by 2024, surpassing the European Commission’s 1,500-point goal, yet only 60% of TEN-T core rest areas hit the AFIR benchmark of a 150 kW charger every 60 km. VINCI Autoroutes achieved 100% service-area coverage with 2,000 dispensers, but rural utilization lingers below 15% during off-peak months, stressing subsidy reliance. Atlante’s ISO 15118-enabled sites aim to trim transaction overhead and raise throughput. Megawatt mandates for heavy trucks bring EUR 630 million in grid upgrades that face two-year transformer delays. Corridor charging is thus shifting from public-good status to a commercial asset class only where traffic warrants grid investment.

Corporate-Fleet Electrification Targets of CAC-40 Companies

LOM legislation forces a 20% zero-emission share by 2025, yet 60% of CAC-40 firms trail the target because depot charging can cost EUR 400,000 for a six-dispenser megawatt site. EDF’s internal program illustrates vertical-integration benefits by spreading 17,200 chargers across homes and offices. Sonepar’s 1,000-unit rollout across 400 branches shows how dispersed real estate can house network charging at scale. France’s EUR 3 billion fund faces 18-month grid queues that delay revenue. Operators with captive sites and predictable routing strategies clearly gain a cost advantage.

Dynamic Tariffs Fostering Residential Smart-Charger Uptake

EDF’s Tempo and Zen Flex tariffs cut overnight rates by up to 40%, incentivizing homeowners to install responsive Level 2 hardware. Linky smart-meter penetration tops 95%, allowing utilities to shape load without new devices.[3]Commission de Régulation de l’Énergie, “Subventions de raccordement,” cre.fr Residential demand management trims peak grid stress and aligns with low-cost renewable generation windows. Tariff sophistication boosts the France electric vehicle charging equipment market by embedding energy-management logic into wallbox specifications. Hardware vendors now bundle software updates that synchronize with EDF price curves to protect customer TCO.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-connection bottlenecks & capacity upgrade costs | -1.7% | National, acute in rural and peri-urban industrial zones | Medium term (2-4 years) |

| Complex municipal permitting & zoning timelines | -0.9% | National, concentrated in historic-district municipalities | Short term (≤ 2 years) |

| Cyber-security compliance costs (EU NIS2) | -1.3% | National, affecting operators above 300 MW capacity | Short term (≤ 2 years) |

| Low utilisation economics in rural ultra-fast sites | -1.1% | Rural départements, secondary TEN-T corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid-Connection Bottlenecks & Capacity Upgrade Costs

Annual reinforcement needs of EUR 5.4 billion through 2050 underscore systemic grid strain.[4]Eurelectric, “Power System Readiness for EV Charging,” eurelectric.org A 2024 Essonne model showed smart-charging plus V2G could shave 25% of required spend, yet V2G uptake remains under 1%. Transformer lead times stretch past two years, forcing operators to pre-finance EUR 150,000-300,000 upgrades with no revenue certainty. Consequently, capacity clusters around metros, sidelining rural adoption.

Cybersecurity Compliance Costs (EU NIS2)

NIS2 mandates 24-hour incident warnings and ISO 27001 certification, carrying fines of EUR 10 million or 2% of turnover for violations. Virta estimates annual compliance adds EUR 50,000-150,000 in opex per operator. Smaller networks lack scale to absorb this burden, triggering M&A and reinforcing incumbent advantage. Insurance premiums rise as liability shifts from hardware to back-office data integrity, further squeezing margins for independent players.

Segment Analysis

By Charging Level: Megawatt Class Redefines Infrastructure Economics

Megawatt-class chargers are slated to grow at a 30.8% CAGR, recalibrating the France electric vehicle charging equipment market toward heavy-duty logistics as Milence commissioned 1 MW hubs in Rouen and Perpignan. Level 2 units held 65.1% of 2024 revenue thanks to LOM retrofits in buildings with over 20 parking spaces. DC Fast installations dominate highways but underperform in rural traffic nodes, prompting subsidy dependence. Ultra-Fast chargers address passenger-vehicle journeys yet risk margin squeeze between cheap home charging and higher-margin megawatt corridors. One structural insight is that the France electric vehicle charging equipment market size is increasingly split between high-frequency, low-power residential usage and capital-dense, ultra-high-power freight nodes.

The France electric vehicle charging equipment market consequently exhibits divergent investment logics: Level 2 projects depend on modest capex and tariff incentives, whereas megawatt assets hinge on long-term offtake, high grid-connection fees, and AFIR heavy-duty mandates. Operators that straddle both ends, such as TotalEnergies and EDF, gain portfolio optionality, while mid-tier DC Fast specialists confront stranded-asset risks if utilization stagnates below breakeven thresholds. Cost per installed kilowatt therefore widens from EUR 650 for residential wallboxes to EUR 2,000-plus for megawatt dispensers, underscoring different payback horizons.

Note: Segment shares of all individual segments available upon report purchase

By Installation Site: Transportation Hubs Capture Commercial Fleet Demand

Residential sites retained 79.9% revenue share in 2024, reflecting broad single-family home ownership and generous wallbox credits. Transportation Hubs, however, are projected to leap at a 27.5% CAGR as airports, ports, and major rail stations electrify support fleets, taxis, and drayage trucks. Lyon-Saint Exupéry’s 800-point concession exemplifies the franchising model through which operators lock in 15-year revenue certainty. Retail-parking alliances like Voltalia-Auchan-DECATHLON-Leroy Merlin plan 5,000 points by 2028, illustrating how high-dwell-time locations monetize existing foot traffic.

Municipal deployments lag because austerity budgets slow rollouts, especially where historic-district zoning inflates permitting costs. The France electric vehicle charging equipment market share of hub-based installations is thus primed to expand as concession models shift risk to capital-rich operators capable of absorbing transformer lead-time uncertainty. Airports and ports, benefiting from captive vehicle flows, generate utilization profiles that surpass public urban chargers by 2-3×, supporting premium pricing and shortening ROI cycles to under five years.

By Application: Fleet and Depot Charging Emerges as Capital-Intensive Growth Vector

Home Charging produced 72.5% of 2024 application revenue on the back of dynamic tariffs that lower overnight costs up to 40%. Yet Fleet and Depot Charging is forecast to accelerate at 32.1% CAGR, fueled by LOM’s 20% zero-emission corporate-fleet mandate and logistics electrification. GT Solutions’ EUR 400,000 megawatt depot at Garonor highlights the capital intensity that restricts entry to fleets with 50+ vehicles. Workplace charging adoption remains tepid because liability and reimbursement logistics deter employers.

Public urban chargers cater to apartment dwellers but confront vandalism and low session counts, holding profitability back. The France electric vehicle charging equipment market size attached to depot projects climbs as financiers demand long-term offtake agreements before underwriting megawatt hardware. B2B players negotiate energy prices directly with utilities, sometimes at wholesale-linked tariffs, cementing a cost edge over B2C segments exposed to full retail rates.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Île-de-France, Auvergne-Rhône-Alpes, and Provence-Alpes-Côte d’Azur together house 55% of installed capacity, illustrating how metropolitan density and grid readiness drive deployment speed. The AFIR target of a 150 kW charger every 60 km along TEN-T corridors remains unmet in 40% of core-network rest areas, especially in Nouvelle-Aquitaine and Occitanie. Île-de-France hosts over 35,000 public points versus fewer than 200 in Lozère and Creuse, creating adoption asymmetries that self-reinforce through operator revenue expectations.

Megawatt corridors focus on high-traffic freight routes; Milence’s hubs anchor a planned 25-site lattice requiring EUR 630 million in grid reinforcement, still awaiting full funding. France’s EUR 3 billion program aims to bridge autoroute gaps by 2028, yet transformer shortages threaten delays up to two years. Historic-district rules in Lyon and Bordeaux raise per-point costs by EUR 5,000-10,000, inflating downtown session fees 20% above suburban prices.

Cross-border roaming fees of 15-35% complicate EV travel despite AFIR interoperability mandates, throttling single-market ambitions in the near term. The France electric vehicle charging equipment market, therefore, bifurcates into grid-ready urban cores with competitive tariffs and capital-starved rural corridors dependent on public subsidies or EU co-financing, suggesting that regional equity hinges on targeted grid spending rather than pure private-sector momentum.

Competitive Landscape

TotalEnergies, EDF/Izivia, Engie, Ionity, and Allego jointly hold around 45% of public-charging revenue, leaving a moderately fragmented field where numerous regional and retail-linked players divide the remainder. Energy majors leverage existing retail and grid footprints. TotalEnergies’ 800-point airport concession showcases scale economics and captive traffic synergies. EDF’s internal fleet rollout spreads capex across in-house demand, demonstrating utility advantages in amortizing infrastructure.

Cybersecurity compliance under NIS2 pushes smaller operators toward M&A; Virta pegs annual ISO 27001 and monitoring spend at up to EUR 150,000, unsustainable for narrow portfolios. Technology differentiation revolves around ISO 15118 readiness; Thales secures municipal tenders by embedding digital-identity layers that align with future V2G sophistication. Hardware makers such as ABB and Schneider Electric increasingly pair with software-native CPMS providers, reflecting a shift from hardware count to utilization optimization via AI-driven load balancing.

White-space remains in fleet depots and regional airports where predictable utilization supports megawatt infrastructure; however, these segments demand long leases and strong credit, filters that privilege capitalized incumbents. The France electric vehicle charging equipment industry thus migrates from site acquisition races toward operational excellence metrics such as revenue per kilowatt and uptime, rewarding integrated platforms able to fuse hardware, energy supply, and data analytics.

France Electric Vehicle Charging Equipment Industry Leaders

Schneider Electric SE

ABB Ltd

EVBox Group

DBT-CEV

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Just outside of Paris, near the A10 motorway, France unveiled the world's inaugural highway that wirelessly charges electric vehicles on the move. This 1.5-kilometre stretch can simultaneously power buses, cars, and heavy-duty trucks as they drive.

- December 2024: Shell completed the transfer of its home and workplace charging operations in six European markets, including France, to 50five, allowing Shell to prioritize public and fleet assets while 50five inherits 15,000 customers.

- December 2024: Voltalia, a global leader in renewable energy, teamed up with three prominent retailers: Auchan, DECATHLON, and Leroy Merlin. Together, they're set to install and manage electric vehicle charging stations across more than 350 parking lots in France.

France Electric Vehicle Charging Equipment Market Report Scope

Electric vehicle (EV) charging equipment refers to the equipment and infrastructure used to charge electric vehicles at home or in commercial and public spaces. The EV charging equipment plays a crucial role in the widespread adoption of electric vehicles in the country. The availability of robust EV charging infrastructure is essential for overcoming range anxiety, a primary concern for potential EV buyers. It helps in reducing carbon emissions and improving air quality.

The France vehicle charging equipment market is segmented into charging level, installation site, and application. By charging level, the market is segmented into level 1, level 2, DC fast, ultra-fast, and megawatt-class. By installation site, the market is segmented into residential, commercial and retail, public municipal, and transportation hubs. By application, the market is segmented into home, workplace, public urban, highway corridor, and fleet and depot. For each segment, the market size and forecasts are provided in terms of revenue (USD).

| Level 1 (Up to 3 kW) |

| Level 2 (3 to 50 kW) |

| DC Fast (50 to 150 kW) |

| Ultra-Fast (150 to 350 kW) |

| Megawatt Class (Above 350 kW) |

| Residential |

| Commercial and Retail |

| Public Municipal |

| Transportation Hubs (Airports, Ports) |

| Home Charging |

| Workplace Charging |

| Public Urban Charging |

| Highway Corridor/En-Route Fast Charging |

| Fleet and Depot Charging |

| By Charging Level | Level 1 (Up to 3 kW) |

| Level 2 (3 to 50 kW) | |

| DC Fast (50 to 150 kW) | |

| Ultra-Fast (150 to 350 kW) | |

| Megawatt Class (Above 350 kW) | |

| By Installation Site | Residential |

| Commercial and Retail | |

| Public Municipal | |

| Transportation Hubs (Airports, Ports) | |

| By Application | Home Charging |

| Workplace Charging | |

| Public Urban Charging | |

| Highway Corridor/En-Route Fast Charging | |

| Fleet and Depot Charging |

Key Questions Answered in the Report

What is the current market size of France vehicle charging equipment market?

The current market size is USD 1.27 billion and is projected to reach USD 2.21 billion by 2030, reflecting a 11.76% CAGR over 2025-2030.

How fast is heavy-duty charging infrastructure expanding in France?

Megawatt Class dispensers are forecast to grow at 30.8% CAGR to 2030 as freight corridors comply with AFIR mandates and operators like Milence build 1 MW hubs.

What share do residential installations hold today?

Residential sites commanded 79.9% of 2024 revenue, supported by EUR 300-500 wallbox tax credits and widespread single-family parking.

Which region has the densest public charging network?

Île-de-France leads with more than 35,000 public points, driven by high EV penetration and faster grid connection timelines.

How will EU NIS2 affect small charge-point operators?

Compliance costs of EUR 50,000-150,000 per year are likely to push smaller networks toward mergers or exits, strengthening incumbent positions.

What CapEx does a typical fleet depot in France require?

A six-dispenser megawatt-capable depot typically costs about EUR 400,000, covering hardware, grid upgrades, and software management.

Why are highway fast chargers under-utilized in rural areas?

Traffic density drops outside core corridors, keeping rural site utilization below 15%, which weakens the business case without subsidies.