Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

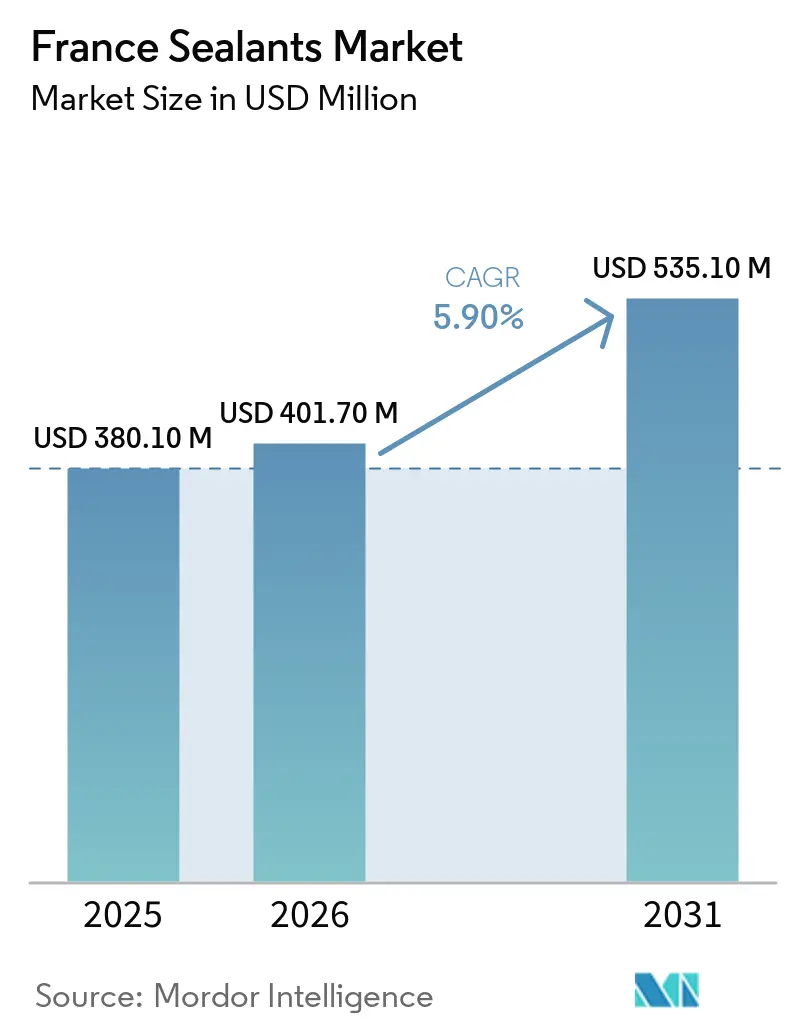

| Base Year Market Size (2025) | USD 380.10 Million |

| Market Size (2026) | USD 401.70 Million |

| Market Size (2031) | USD 535.10 Million |

| Growth Rate (2026 - 2031) | 5.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Sealants Market Analysis by Mordor Intelligence

The France Sealants Market size is projected to grow from USD 380.10 million in 2025 to USD 401.70 million in 2026, and reach USD 535.10 million by 2031, growing at a CAGR of 5.90% from 2026 to 2031. Structural retrofits to boost building-envelope airtightness, rapid electrification of domestic automotive production, and offshore renewable installations are widening the application set for advanced chemistries beyond classic weatherproofing. Silicone continues to dominate glazing and curtain-wall modules because of its ±50% joint movement capability and proven thirty-year durability, while polyurethane is gaining momentum in electric-vehicle (EV) battery enclosures where high peel strength, gap-filling, and vibration damping are decisive performance criteria. Government subsidies under MaPrimeRénov’ are accelerating residential renovation cycles, and the 2020 AGEC law’s repairability index is nudging consumers toward maintenance-grade sealants that extend appliance life. In parallel, Airbus composite output and Stellantis-Renault lightweighting mandates are creating downstream demand for polysulfide and structural epoxy grades that meet stringent aerospace or body-in-white certifications.

Key Report Takeaways

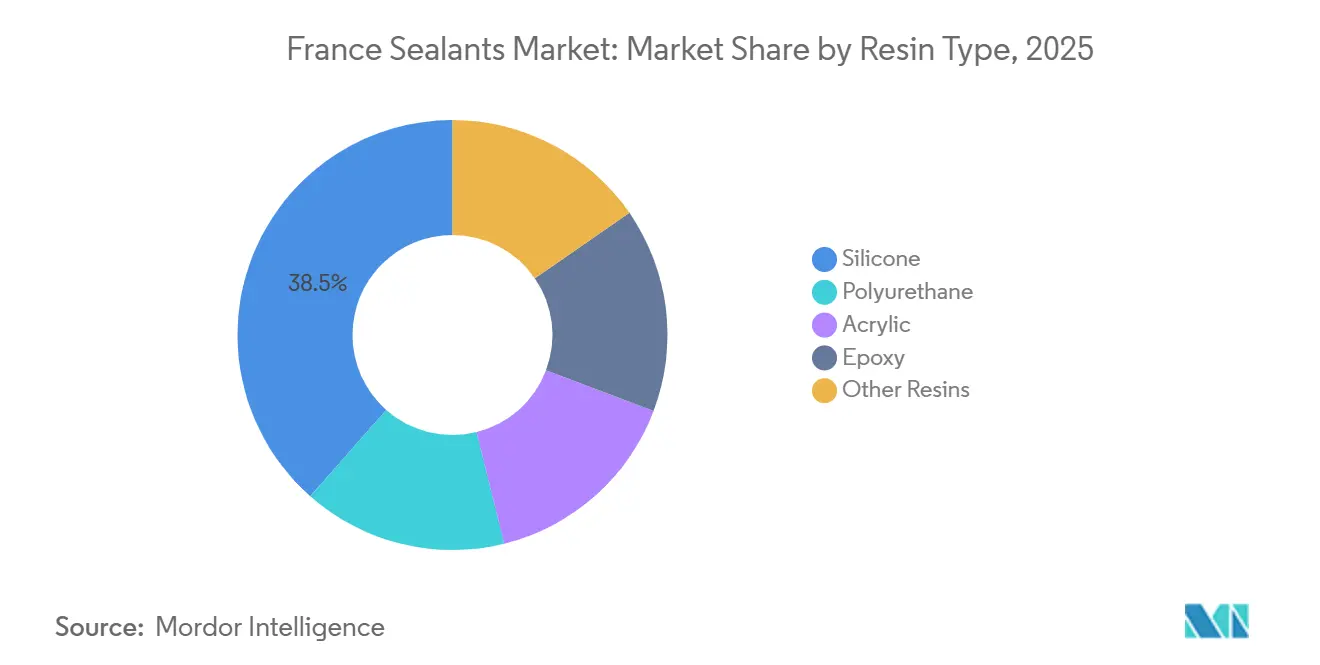

- By resin type, silicone led with 38.5% of the France sealants market share in 2025 . Polyurethane is forecast to expand at a 7.24% CAGR between 2026-2031, the fastest pace among resins.

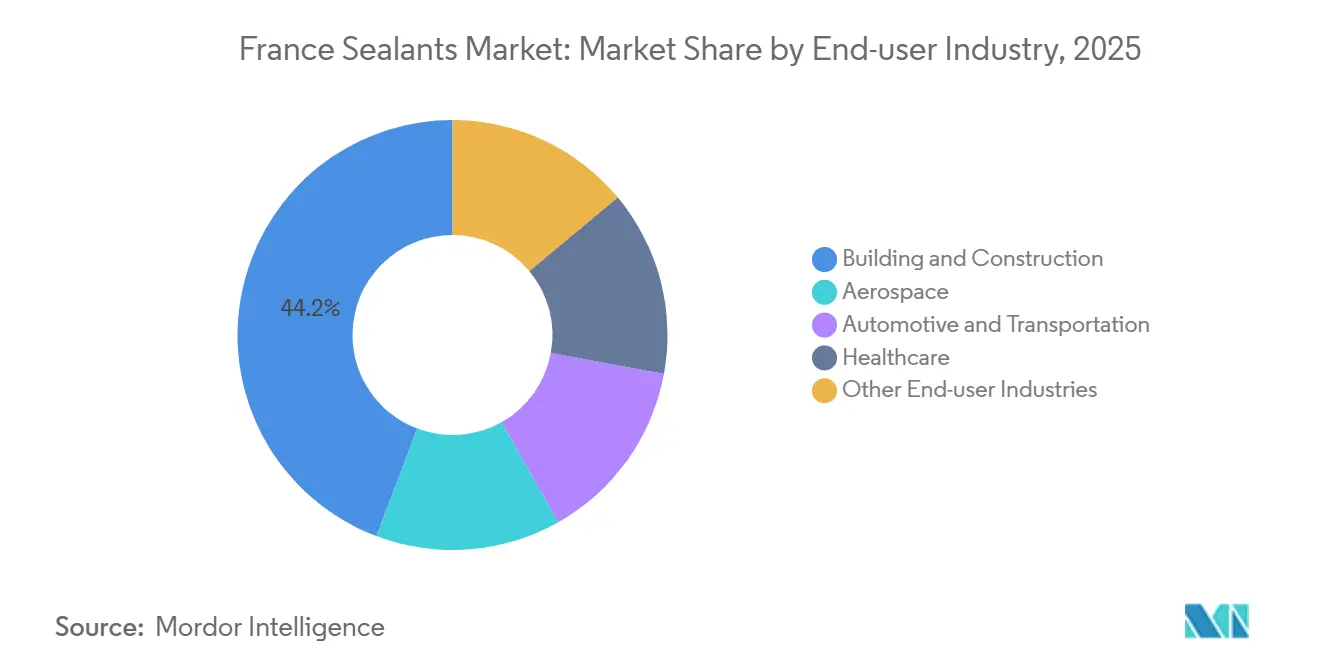

- By end user, building and construction captured 44.25% of the France sealants market size in 2025. Healthcare sealant offtake is projected to advance at a 7.01% CAGR through 2031, the quickest among all industries.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Sealants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renovation-led demand surge in energy-efficient building envelope upgrades | +1.8% | National, concentrated in Île-de-France, Auvergne-Rhône-Alpes | Medium term (2-4 years) |

| EV lightweighting requirements in French automotive production | +1.3% | National, with Stellantis and Renault assembly corridors in Hauts-de-France, Grand Est | Medium term (2-4 years) |

| Composite bonding growth in Airbus and regional aerospace clusters | +0.9% | Regional, Toulouse-Occitanie and Nantes-Pays de la Loire aerospace hubs | Long term (≥ 4 years) |

| Repairability-index law boosting DIY and appliance maintenance sealant sales | +0.7% | National, consumer-facing retail channels | Short term (≤ 2 years) |

| Marine-grade sealants demand from French offshore-wind build-out | +0.5% | Coastal regions, Bay of Biscay and Mediterranean offshore zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Renovation-Led Demand Surge in Energy-Efficient Building Envelope Upgrades

MaPrimeRénov’ extended cash advances up to 50% for very modest households through December 2025, stimulating immediate purchases of silicone and polyurethane sealants for thermal bridges, roof junctions, and duct penetrations[1]Service-public.fr, “MaPrimeRénov’: aides à la rénovation énergétique,” service-public.fr. Fluid-applied silicone air-and-water barriers such as Momentive Elemax 2600 can reduce HVAC energy use by as much as 35% by limiting uncontrolled airflow, an attractive payback lever in retrofit settings where sheet membranes are difficult to place[2]Momentive Performance Materials, “Elemax 2600 Air & Water Barrier,” momentive.com. The subsidy’s raised cost ceiling to 80% for middle-income households broadens access to premium low-VOC products carrying French FDES declarations, ensuring airtightness compliance under HQE Cible 8 targets. Mandatory ISO 11600 Class 25 movement and EN 15651-2 designations safeguard joint durability in glazing and façade works. These policy and standard frameworks collectively lock in a multi-year demand cycle for high-performance building sealants.

EV Lightweighting Requirements in French Automotive Production

Multi-material bonding, aluminum to carbon-fiber-reinforced polymer and steel to composites, is displacing mechanical fasteners in EV body-in-white architecture, pushing consumption of shear-resistant epoxy and polyurethane adhesives that double as vibration dampers and battery-case sealants. Henkel’s April 2025 reveal of AI-generated virtual adhesives and debondable chemistries anticipates EU battery-passport rules that will require traceability and end-of-life disassembly. Acrylic-epoxy hybrids activated by UV in minutes are improving line takt times and adhesion to low-energy plastics when pre-treated with plasma, enabling higher throughput at Stellantis and Renault plants. Evolving LEED v4 and SCAQMD Rule 1168 thresholds below 250 g/L VOC are giving MS polymers an advantage, delivering ±25% to ±50% movement without isocyanate exposure. The combined regulatory and production drivers keep automotive grade sealants on a robust growth path.

Composite Bonding Growth in Airbus and Regional Aerospace Clusters

Fraunhofer IFAM’s robotic vacuum-suction blasting paired with automated paste-adhesive dispensing cut contamination-related defects in Airbus composite sub-assemblies, winning the JEC Composites Innovation Award 2026 and supporting higher build rates in Toulouse lines. Weight-optimized polysulfide sealants such as 3M AC-380 provide 33% mass reduction versus legacy grades while resisting fuel immersion and temperature cycling from –54 °C to +121 °C, meeting Class B requirements for integral tanks. DIN 35255, effective November 2025, overlays ISO 9001 with process-oriented bonding protocols, tightening documentation and inline quality control obligations for French aerospace suppliers. Conformance will likely favor firms equipped with electrical capacitance tomography for resin-mix verification. The resulting certification hurdle entrenches high-performance sealants in aerospace supply chains.

Repairability-Index Law Boosting DIY and Appliance Maintenance Sealant Sales

DGCCRF enforcement of repairability and durability scores, with fines up to EUR 15,000 per legal entity for non-compliance, is obligating retailers to display indices and stock consumer-grade silicone cartridges and gaskets. The January 2025 durability index layers reliability metrics atop reparability, prompting appliance OEMs to specify longer-life sealants and guarantee spare-part supply. SikaSeal-112 Vitrage, an acetoxy silicone requiring no primer on glass and anodized aluminum, simplifies DIY usage and meets Class G 25 E glazing requirements, thus aligning with the law’s intent to lower skill barriers. Despite EU harmonization excluding smartphones, the French scheme remains a differentiator in white-goods regulation and is influencing neighboring markets. The evidence points to sustained growth in retail sealant volumes.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petrochemical feedstock price volatility | -1.2% | Global, with acute exposure in polyurethane and acrylic value chains | Short term (≤ 2 years) |

| Stricter EU REACH limits on di-isocyanates raising compliance costs | -0.8% | EU-wide, affecting polyurethane sealant formulators and end-users | Medium term (2-4 years) |

| Emerging bio-based adhesive substitutes eroding conventional sealant share | -0.4% | National and EU, concentrated in wood-panel and construction adhesive segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Petrochemical Feedstock Price Volatility

With raw materials representing roughly 50% of revenue, French formulators struggle to pass spikes through quarterly construction contracts, compressing EBITDA. BASF’s MDI expansion in Geismar may ease tightness by 2027, yet geopolitical risk continues to swing benzene and naphtha costs, exposing sealant makers to margin whiplash. Those without hedging must choose between volume attrition and profit erosion, especially given the persistence of lower-priced Asian imports.

Stricter EU REACH Limits on Di-Isocyanates Raising Compliance Costs

Since August 2023, all professional users of polyurethane products containing ≥0.1% free monomeric di-isocyanate require accredited training renewed every five years, generating administrative overhead and lost labor hours. Sika advises either switching to Purform micro-emission lines that avoid training or enrolling staff via FEICA’s e-learning platform code FEICA_21_C20, both adding cost layers. Smaller formulators must revamp production to MS polymers or invest in new isolation systems, straining capex budgets. While the rule aims to curb occupational asthma, it disadvantages EU supply chains compared with jurisdictions lacking equivalent mandates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Silicone Retains Leadership While Polyurethane Accelerates

Silicone captured 38.5% of the France sealants market share in 2025, powered by irreplaceable demand in structural glazing, insulating glass units, and weatherproof façades. Sikasil IG-25 HM Plus meets EN 1279-4 and ASTM C1184, securing gas-retention in vacuum-insulated glazing which commands premium unit prices. Polyurethane is set to pace the France sealants market size expansion, growing 7.24% CAGR during 2026-2031 as EV assemblers bond aluminum, CFRP, and steel modules, substituting welds to cut weight and extend battery range.

Acrylics remain relegated to interior static joints where paintability and near-zero VOC confer decorative advantages, but low movement capability limits outdoor use. Epoxies command niche industrial flooring and aerospace applications where tensile strength and chemical resistance justify slow cure; Baxxodur EC 151 allows functional cure at 5 °C, expanding winter construction windows. Polysulfides and MS polymers fill specialized roles, fuel-tank sealing and isocyanate-free construction joints, respectively, but face medium-term substitution risk from bio-based entrants.

By End-User Industry: Construction Anchors Volume, Healthcare Drives Margin

Building and construction consumed 44.25% of the France sealants market size in 2025 because single-gesture insulation subsidies and non-residential façade retrofits pull through large cartridge volumes. Saint-Gobain’s Lead & Grow roadmap aims to lift global construction-chemicals revenue from EUR 6.5 billion to beyond EUR 9 billion by 2030, ensuring sustained formulation and specification investment in French projects.

Healthcare exhibits the fastest trajectory at 7.01% CAGR to 2031. Corza Medical’s TachoSil collagen-fibrin patch commands premium hospital pricing, reflecting high regulatory barriers and cost tolerance in surgical hemostasis. Aerospace and automotive segments converge on composite bonding, with polysulfide fuel-tank sealants and structural epoxies heading to Airbus lines while EV battery modules rely on moisture-cure polyurethanes for crash energy absorption. Fire-retardant MS polymers such as Teroson MS 949 FR meet EN 45545-2, facilitating uptake in rail and tunnel works.

Geography Analysis

Île-de-France, Auvergne-Rhône-Alpes, and Occitanie together account for the bulk of France sealants market demand owing to dense housing stock, industrial aerospace activity, and regional renovation subsidies. MaPrimeRénov’ funding at up to 50% of project cost for modest households has fostered brisk uptake of silicone air-barriers and polyurethane foams in these areas. Offshore, the Bay of Biscay and Mediterranean coasts are fueling marine-grade consumption as Noirmoutier and EOLMED wind arrays require polysulfide flange gaskets and solvent-free silicone coatings rated for two-decade sea immersion .

Hauts-de-France and Grand Est automotive corridors, home to Stellantis and Renault EV facilities, draw on structural epoxies and polyurethane chemistries for multi-material bonding that meets battery-safety protocols. Toulouse-Occitanie and Nantes-Pays de la Loire aerospace hubs leverage Fraunhofer IFAM’s SAUBER 4.0 robotic dispensing to trim composite scrap rates, which in turn raises throughput for high-modulus polysulfide and two-part silicones. DIN 35255 certification effective November 2025 will likely consolidate aerospace sealant supply toward firms with in-house process analytics.

Nationwide enforcement of the repairability index under the 2020 AGEC law is nudging DIY retailers to broaden silicone and acrylic ranges, while EU REACH di-isocyanate training pushes professional users toward micro-emission and MS polymer options that bypass compliance overhead.

Competitive Landscape

The France sealants market is moderately concentrated. Henkel’s February 2026 agreement to acquire Dutch coatings group Stahl for EUR 2.1 billion and its earlier purchase of Swiss tape maker ATP bring nearly EUR 1 billion of incremental sales, deepening its reach in automotive interiors and façade tapes. Saint-Gobain plans USD 13 billion of growth capex and acquisitions between 2026-2030, explicitly earmarking sealants and waterproofing to lift construction-chemicals turnover past EUR 9 billion.

Technology differentiation is emerging through AI-driven virtual adhesives for EV battery repair, debond-on-command chemistries for recycling, and automated dispensing for composite aerostructures, as showcased by Henkel and Fraunhofer IFAM. Smaller French players are switching to isocyanate-free MS polymers and micro-emission polyurethanes to sidestep REACH training, but investment hurdles could limit their scale-up. Collaborative research and development, exemplified by BASF-Sika’s Baxxodur EC 151, which cuts VOC by 90% while curing at 5 °C, blurs competitive boundaries and accelerates sustainable formulations. These dynamics suggest an intensifying rivalry within premium and sustainable sealant niches.

France Sealants Industry Leaders

3M

Henkel AG & Co. KGaA

Sika AG

DOW

Arkema

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Arkema completed a EUR 40 million modernization of its Lacq/Mourenx platform, adding a sulfur-effluent unit that trims sulfur-dioxide emissions 40% and greenhouse gases 10%, partially financed under France 2030 via ADEME.

- February 2025: Lactips, a French company specializing in the production of 100% biobased natural polymers that are water-soluble and biodegradable in various environments, expanded its paper coating product range. The CareTips PFP344MAX sealant grade is introduced to address the market demand for a cost-effective, durable, and high-performance solution.

France Sealants Market Report Scope

Sealants are elastomeric materials used to fill gaps, joints, or cracks, preventing water, air, dust, and fluid passage. Widely applied in construction and industrial sectors, they ensure waterproofing and structural flexibility in buildings, windows, automotive components, and appliances.

The France sealants market is segmented by resin type and end-user industry. By resin type, the market is segmented into silicone, polyurethane, acrylic, epoxy, and other resins. By end-user industry, the market is segmented into aerospace, automotive and transportation, building and construction, healthcare, and other end-user industries. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Resin Type

| Silicone |

| Polyurethane |

| Acrylic |

| Epoxy |

| Other Resins |

By End-user Industry

| Aerospace |

| Automotive and Transportation |

| Building and Construction |

| Healthcare |

| Other End-user Industries |

| By Resin Type | Silicone |

| Polyurethane | |

| Acrylic | |

| Epoxy | |

| Other Resins | |

| By End-user Industry | Aerospace |

| Automotive and Transportation | |

| Building and Construction | |

| Healthcare | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Healthcare, and Others are the end-user industries considered under the sealants market.

- Product - All sealant products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Silicone, and Others are considered

- Technology - For the purpose of this study, One component and Two component sealant technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms