Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

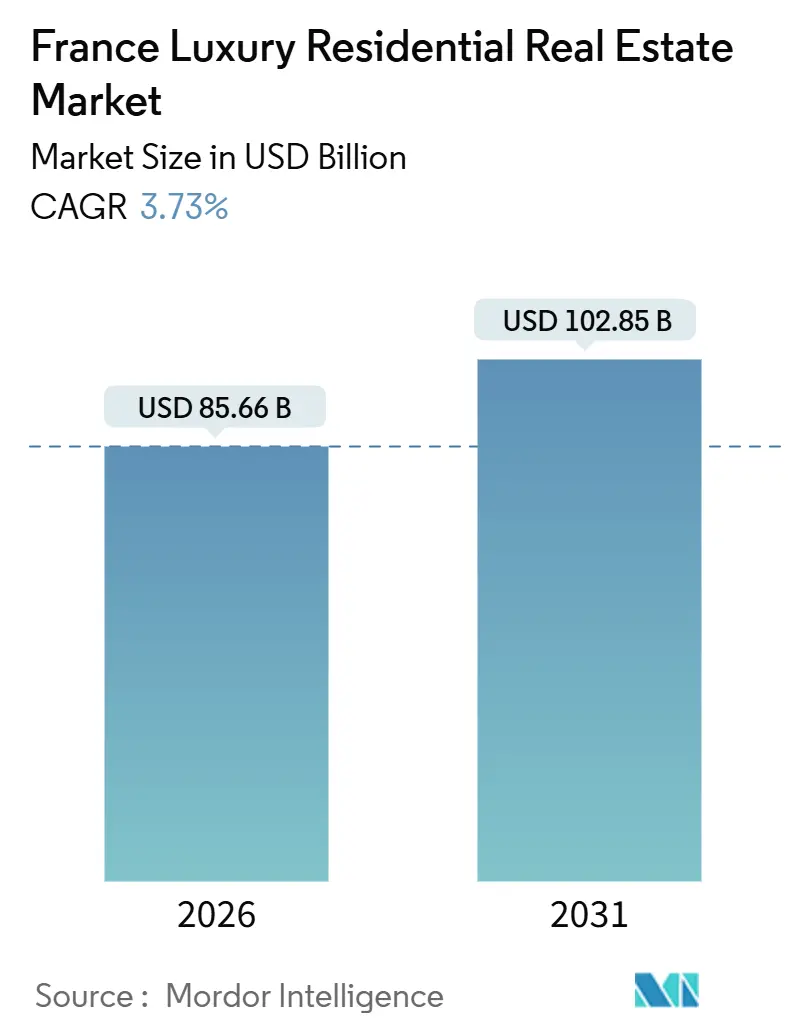

| Market Size (2026) | USD 85.66 Billion |

| Market Size (2031) | USD 102.85 Billion |

| Growth Rate (2026 - 2031) | 3.73% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Luxury Residential Real Estate Market Analysis by Mordor Intelligence

The France Luxury Residential Real Estate Market size is estimated at USD 85.66 billion in 2026, and is expected to reach USD 102.85 billion by 2031, at a CAGR of 3.73% during the forecast period (2026-2031). Scarce ultra-prime inventory in Paris, the Riviera, and key Alpine resorts underpins price resilience, while rising wealth taxes, transaction costs, and energy-retrofit mandates curb short-term speculation. Rental demand is expanding more rapidly than sales as buyers deploy yield-seeking strategies in resort towns that sit outside Parisian short-let caps. A stable legal framework, deep cultural capital, and elite educational institutions sustain inflows from global high-net-worth households even when euro volatility erodes headline returns. Brokerage competition remains moderate because off-market sourcing and heritage expertise still outweigh scale-driven marketing efficiencies.

Key Report Takeaways

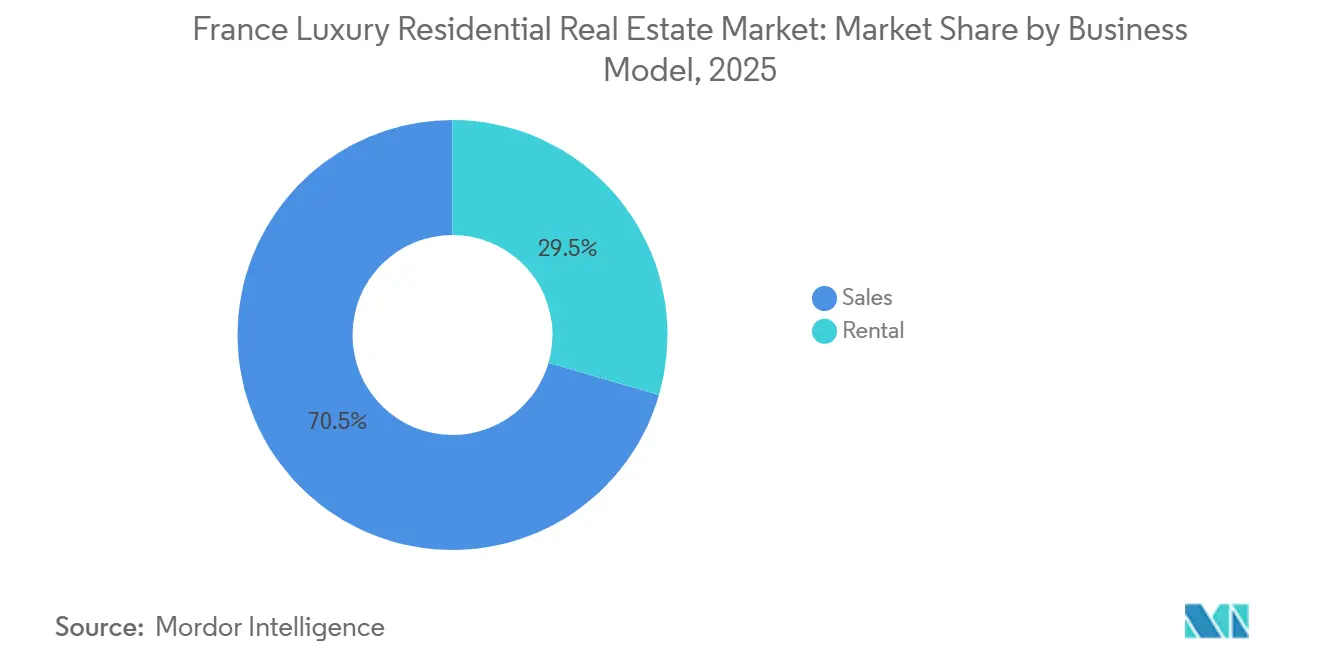

- By business model, sales transactions captured 71.2% of France luxury residential real estate market share in 2025; rental activity is projected to post a 4.80% CAGR through 2031.

- By property type, apartments accounted for 66.1% of France luxury residential real estate market size in 2025, while villas are forecast to grow at a 5.05% CAGR through 2031.

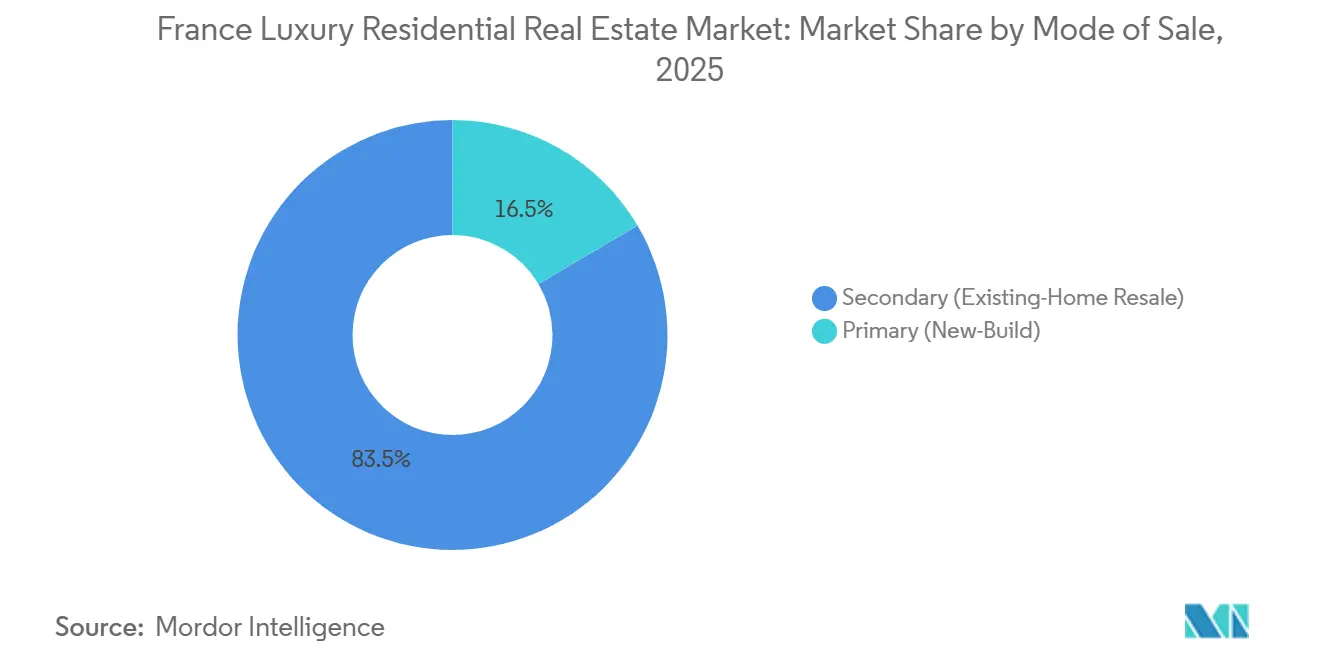

- By mode of sale, the secondary segment held 83.5% of France luxury residential real estate market share in 2025; primary supply is advancing at a 5.21% CAGR to 2031.

- By city, Paris retained 45.3% of France luxury residential real estate market size in 2025, whereas Marseille is expanding at the fastest 5.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Luxury Residential Real Estate Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global HNW demand underpinned by rule-of-law and top schools | +1.0% | Paris, Lyon, Riviera gateway cities | Long term (≥ 4 years) |

| Extreme scarcity of ultra-prime assets in top arrondissements | +0.8% | Paris 1st, 6th, 7th, 8th, 16th; Neuilly-sur-Seine | Long term (≥ 4 years) |

| Riviera and Alpine second-home markets with rental upside | +0.6% | Provence-Alpes-Côte d’Azur; Courchevel, Val d’Isère, Megève | Medium term (2-4 years) |

| Periodic euro weakness that lifts USD/GBP purchasing power | +0.5% | National, strongest in Paris and Riviera | Short term (≤ 2 years) |

| Value-add premiums from heritage renovations and green upgrades | +0.4% | Paris historic districts, Lyon Presqu’île, Bordeaux | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Extreme Scarcity of Ultra-Prime Assets in Paris Golden Triangle

Annual supply of apartments above 300 m² in Paris’s 1st, 6th, 7th, 8th, and 16th arrondissements has stayed below 50 units since 2024, creating a structural shortage that fuels double-digit bidding premiums[1]“Paris Property Prices Hit Record High as Luxury Buyers Return,” Financial Times, ft.com . Branded conversions such as Maybourne Riviera illustrate the valuation gap, with 2024 launch prices near USD 58,300 per m², almost twice nearby non-branded stock. Heritage-protection rules prohibit demolition and vertical expansion, permanently capping new inventory. Knight Frank ranked Paris fourth worldwide for ultra-high-net-worth density, yet logged a 12% drop in EUR 10 million-plus trades in 2025 as scarcity outpaced liquidity. Sellers are able to wait for the right match now average sub-60-day closings, while secondary stock lingers several months longer, reinforcing the scarcity premium.

Global HNW Demand Anchored by Rule-of-Law, Culture, and Schools

France’s clear property title regime, absence of capital controls, and concentration of elite schools keep it at the top of relocation shortlists for American, Gulf, and Asian families. Notarial data show 8% average price growth in 2025 around the Musée d’Orsay and Opéra Garnier catchments as remote-work professionals sought cultural proximity[2]Chambre des Notaires de Paris, “Notarial Real Estate Statistics 2025,” notaires.fr . GCC buyer volume rose 15% during the year despite tougher European AML checks. Post-Olympics branding in 2024 raised Paris’s global visibility, but the enduring magnet remains eurozone legal certainty and European Court of Justice oversight. Institutional landlords accept 2-3% gross yields because wealth preservation, rather than income, drives allocations at the top end.

Riviera and Alpine Second-Home Markets with Rental Upside

Lifestyle migration and yield-seeking capital are increasingly directed toward Côte d’Azur villas and Alpine chalets. Courchevel’s 2024-25 season closed at USD 33,500 per m², while fractional-ownership models generated 4-6% gross yields during peak weeks[3]“Courchevel Ski Property Prices Surge 12% Year-on-Year,” Les Echos, lesechos.fr . The extended Loi Montagne now restricts new Alpine construction, making renovation the only path to fresh supply and embedding scarcity into future pricing. Saint-Tropez and Cannes benefit from year-round tourism and the absence of Paris’s 120-day short-let limit, letting owners defray carrying costs through Airbnb Luxe. Savills found French Alpine resorts outperformed Swiss and Austrian peers on 2025 price appreciation, a trend supported by EUR 106 billion of recovery-plan infrastructure upgrades.

Euro Weakness Boosts USD/GBP Purchasing Power

The euro’s slide to parity in mid-2024 discounted French luxury assets by 14% in dollar terms, spurring 38% of American clients surveyed by Knight Frank to accelerate Paris closings. Sterling strength also lifted British participation on the Riviera by nine percentage points year-over-year. While the euro rebounded to USD 1.06 in early 2026, monetary-policy divergence suggests further softness if U.S. rate cuts outpace the ECB. Yet buyers still face 7-8% deal fees that require at least 18 months’ hold to break even, tempering speculative flips.

Restraints Impact Analysis

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High transaction and ownership taxes (IFI and levies) | −0.9% | National, strongest in Paris and Riviera ultra-prime markets | Long term (≥ 4 years) |

| Strict planning rules and energy mandates that lift capex | −0.7% | Paris historic districts, Lyon, Bordeaux, Provence classified communes | Medium term (2-4 years) |

| Tighter financing, AML checks, and thin liquidity at top end | −0.5% | National, concentrated in deals above USD 5.3 million | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Transaction and Ownership Taxes Erode Net Returns

The Impôt sur la Fortune Immobilière imposes a 0.5-1% annual tax on net real-estate wealth above USD 1.38 million, shrinking income streams for non-resident landlords. Buyers also pay 7-8% in notary, registration, and agent fees, equating to USD 371,000-424,000 in upfront costs on a USD 5.3 million Paris purchase. These frictions compress already thin 2-3% gross yields, steering yield-focused capital toward equities or credit markets instead. Senate proposals to ease thresholds stalled in 2025, keeping the levy an enduring drag on market velocity and France luxury residential real estate market growth.

Strict Planning Rules and Energy Mandates Raise Capex and Timelines

Any façade change or roof extension in protected quarters needs approval from the Architectes des Bâtiments de France, with a permit lasting as long as 24 months. Retrofit obligations ban leasing of G-rated homes from 2025 and F-rated from 2028, forcing USD 31,800-106,000 retrofits per unit. Owners of monuments historiques must hire certified artisans, potentially tripling renovation budgets. Unrenovated stock trades at 15-20% discounts, while B-rated assets achieve quick sales at premium prices. Consequently, some investors pivot to new-build projects outside strict heritage zones, shifting capital away from the densest parts of Paris.

Segment Analysis

By Business Model: Sales Dominance Prevails, but Rental Accelerates

Sales accounted for 71.2% of France's luxury residential real estate market share in 2025, underscoring the continued dominance of trophy acquisitions for long-term wealth preservation. Owner-occupiers and family offices remain the core buyers, while international investors target secondary-market heritage assets that can be held across generations. Despite this dominance, rental income strategies gain traction in Riviera and Alpine resorts, where short-let regulations are more permissive than in Paris. Institutional vehicles, including insurers and REITs, increasingly view turnkey villas as inflation-hedged alternatives to bonds, raising allocations to the rental pool.

Rental revenue is forecast to expand at a 4.80% CAGR through 2031, outpacing overall market growth. Corporate relocation programs and France’s 2024 green-industry tax incentives lift demand for furnished executive housing in Lyon, Marseille, and Toulouse. Branded-residence operators structure fractional-ownership models that guarantee 50-60% of gross rental to owners, blending lifestyle access with predictable cash flow. This hybrid approach blurs the historic divide between sale and lease strategies, further embedding rental economics into acquisition decisions.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Property Type: Apartments Lead, Villas Win Growth

Apartments held 66.1% of France luxury residential real estate market size in 2025. Parisian Haussmannian stock—defined by high ceilings, parquet floors, and wrought-iron balconies—remains the global benchmark, attracting diplomats and families needing proximity to international schools. Duplexes above 200 m² in the 7th and 16th arrondissements trade at USD 21,200-26,500 per m², a level few buyers resist because true alternatives are scarce.

Villas are projected to record the fastest 5.05% CAGR through 2031 as remote work and lifestyle migration highlight the value of outdoor space. Côte d’Azur houses within 10 minutes of the shoreline averaged USD 12,700-19,100 per m² in 2025, while Provence bastides with vineyard parcels generate 3-4% seasonal yields. Branded-service packages, including concierge and asset management, lower operational barriers for foreign owners and further encourage villa acquisitions over large urban apartments.

By Mode of Sale: Secondary Resales Command, Primary Supply Gains Pace

Secondary stock represented 83.5% of France luxury residential real estate market share in 2025 because buyers trust proven construction quality and appreciate immediate occupancy in heritage districts. Average turnover for USD 5.3 million properties is 18-24 months, reflecting cautious liquidity at the top end. Buyers prize original moldings and fireplaces that cannot be replicated in new projects, maintaining firm price resistance when authentic details are absent.

Primary transactions are forecast to expand at a 5.21% CAGR, the fastest within this segmentation. Developers retrofit industrial sites and waterfront parcels into energy-compliant residences bundled with hotel-grade services. Branded projects such as Peninsula Paris command 30-40% premiums by eliminating renovation risk and providing turnkey compliance with energy rules. In Lyon and Marseille, new-build pricing sits 20-25% below Paris equivalents, courting entrepreneurs priced out of the capital yet wanting urban convenience.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Paris remains the anchor, but its 45.3% share stabilizes rather than expands because extreme scarcity in the EUR 10 million-plus bracket dampens transaction counts when euro strength briefly compresses USD purchasing power. Prime arrondissements posted USD 21,200-31,800 per m² averages in 2025, and trophy listings exceeding USD 53,000 per m² still clear within 60 days, underscoring enduring safe-haven appeal even as IFI liabilities discourage pure yield hunters. North American buyers, benefiting from favorable exchange rates, added 11 percentage points to their Paris presence in 2025.

Lyon’s share inches upward thanks to 4-5% rental yields that double Paris norms. Presqu’île apartments at USD 5,300-7,420 per m² offer 60-70% discounts to twin-size Paris equivalents, attracting biotech executives aligned with Sanofi and bioMérieux expansions. Marseille grows the fastest at 5.56% CAGR as the USD 1.59 billion port and transport overhaul tightens links to Aix-en-Provence and Cassis, catalyzing tech-sector relocations into Euroméditerranée offices. Waterfront lofts at USD 8,480-12,720 per m² remain half Côte d’Azur pricing, positioning the city as the relative-value outlier.

Beyond the big three, Bordeaux leverages UNESCO-listed heritage and nearby vineyards to sustain USD 6,360-9,540 per m² tags in the Triangle d’Or. Toulouse feeds off Airbus-anchored aerospace growth, while rural Provence and the Alpine arc absorb lifestyle-driven inflows seeking land, privacy, and seasonal rental income. Overall, capital flows diversify geographically as buyers weigh Paris’s scarcity premium against easier regulation, higher yields, and lifestyle perks in secondary hubs.

Competitive Landscape

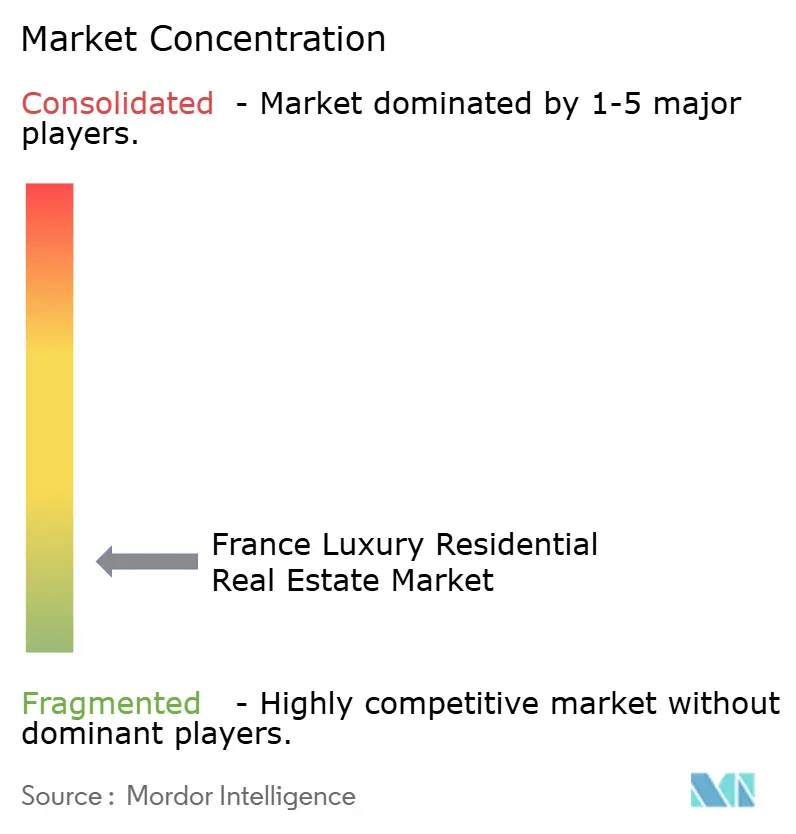

France luxury residential real estate market competition stays fragmented, with no player crossing even a 5% national share. Global franchises—Sotheby’s International Realty, Christie’s International Real Estate, Knight Frank, and Engel & Völkers—use cross-border databases to funnel overseas demand into Paris, the Riviera, and ski resorts. Regional specialists such as Barnes, Daniel Feau, and Emile Garcin counter with hyper-local knowledge and off-market access, retaining high-net-worth loyalty for discreet trophy transactions. Roughly 60% of deals above USD 10 million still close off-portal to protect seller privacy.

Strategic positioning now pivots on energy-retrofit advisory, compliance expertise, and technology adoption. Knight Frank opened a heritage-retrofit desk in 2025, cutting approval times by 20% through Compagnons du Devoir partnerships. Sotheby’s acquired 40% of Junot Immobilier to deepen its reach into Paris’s Marais and Left Bank micro-markets. Engel & Völkers formed a joint marketing with Le Figaro to combine international reach with domestic credibility, strengthening Riviera and Alpine funnel efficiency.

Technology investment escalates as agencies implement AI-driven matching and virtual staging. LuxuryEstate’s 2024 tool reduced time-on-market for renovation-heavy listings by 15%. Barnes opened a Marseille branch in 2024 to ride the city’s outsized 5.56% CAGR, exemplifying the geographic diversification strategy. Compliance workloads under Tracfin’s AML rules favor firms able to absorb overhead, tilting share toward larger networks even as boutique expertise remains critical at the ultra-prime end.

France Luxury Residential Real Estate Industry Leaders

Sotheby’s International Realty Affiliates LLC

Daniel Feau

Barnes International Realty

John Taylor

Propriétés Le Figaro

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: Knight Frank France launched an energy-retrofit advisory service for heritage assets, cutting permit timelines by 20%

- November 2024: Sotheby’s International Realty bought 40% of Junot Immobilier to expand Left Bank coverage

- September 2024: Maybourne Riviera delivered 69 branded residences at USD 58,300 per m², a Côte d’Azur record

- July 2024: Barnes opened a Marseille office to capture demand in the fastest-growing city segment

- June 2024: BNP Paribas Real Estate introduced green mortgages 25 bps below market for B-rated homes

France Luxury Residential Real Estate Market Report Scope

The Luxury Residential Real Estate Market encompasses high-end housing characterized by premium amenities, prime locations, and superior architectural designs. This segment includes luxury villas, penthouses, mansions, and high-rise apartments situated in exclusive neighborhoods. Catering primarily to high-net-worth individuals (HNWIs) and ultra-high-net-worth individuals (UHNWIs), the market offers not just homes, but prestige, privacy, and lucrative investment opportunities. Demand is fueled by factors such as economic growth, urbanization, and shifting lifestyle preferences. Noteworthy trends shaping the market include a focus on sustainability, the integration of smart home technology, and the rise of branded residences.

France Luxury Residential Real Estate Market is segmented by type (apartments and condominiums, villas and landed houses), and by key cities (Paris, Nantes, Lyon and Other Cities). The report offers market size and forecast values (USD) for all the above segments.

By Business Model

| Sales |

| Rental |

| By Business Model | Sales |

| Rental |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the France luxury residential real estate market in 2026?

The market is valued at USD 85.66 billion in 2026 and is heading toward USD 102.85 billion by 2031 at a 3.73% CAGR.

Which French city shows the fastest luxury-property growth through 2031?

Marseille leads with a projected 5.56% CAGR, thanks to port upgrades and a burgeoning technology hub.

Why are rental strategies gaining traction in French luxury housing?

Rental revenue is projected to grow 4.80% annually as resort areas allow flexible short-lets and branded residences guarantee pooled income.

What tax costs most affect foreign buyers of French luxury homes?

The Impôt sur la Fortune Immobilière levies 0.5-1% annually on net real-estate wealth over USD 1.38 million, in addition to 7-8% upfront transaction fees.

How does energy regulation impact property values?

Homes upgraded to Diagnostic de Performance Énergétique B or C ratings command 12-15% premiums and qualify for cheaper green mortgages, while unrated stock faces rental bans.