Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

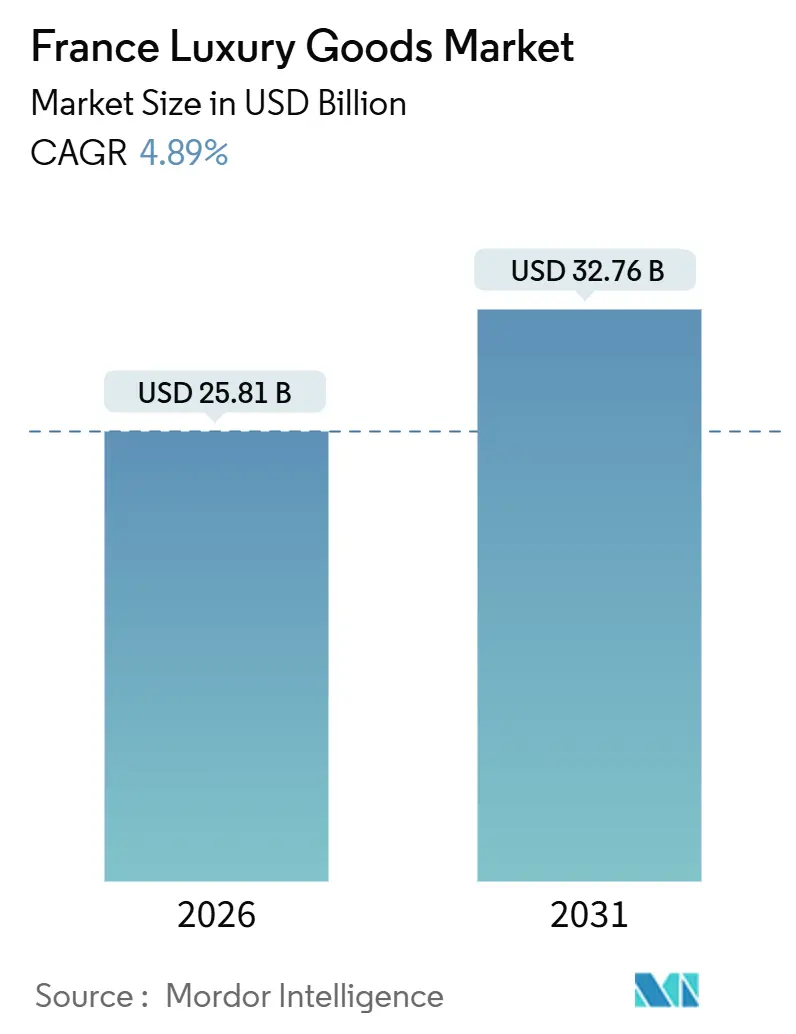

| Market Size (2026) | USD 25.81 Billion |

| Market Size (2031) | USD 32.76 Billion |

| Growth Rate (2026 - 2031) | 4.89% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

France Luxury Goods Market Analysis by Mordor Intelligence

The France luxury goods market size is estimated at USD 25.81 billion in 2026, and is expected to reach USD 32.76 billion by 2031, at a CAGR of 4.89% during the forecast period (2026-2031). This trajectory reflects France's enduring position as the birthplace of modern luxury, where heritage maisons continue to anchor global prestige even as digital channels and sustainability mandates reshape consumer expectations. The market's momentum stems from a confluence of forces: inbound tourism rebounded sharply in 2024 when France welcomed over 100 million visitors who generated EUR 71 billion in revenue, with Chinese arrivals surging 40% and Japanese tourists climbing 20% year-on-year, according to the French Republic. Meanwhile, the European Union's Digital Product Passport regulation, which took effect in 2024, compels every luxury item sold in France to carry verifiable provenance and circularity data, effectively turning transparency into a competitive weapon. Paris alone captured more than half of total tourist spending in 2025, and tourist receipts now exceed pre-pandemic peaks as long-haul travelers from China, Japan, and North America return at scale. Luxury houses are also capitalizing on the Digital Product Passport regime, turning provenance data into a storytelling asset that reinforces brand equity.

Key Report Takeaways

- By product type, clothing and apparel led with 43.03% revenue share in 2025, while leather goods are forecast to advance at a 4.96% CAGR through 2031.

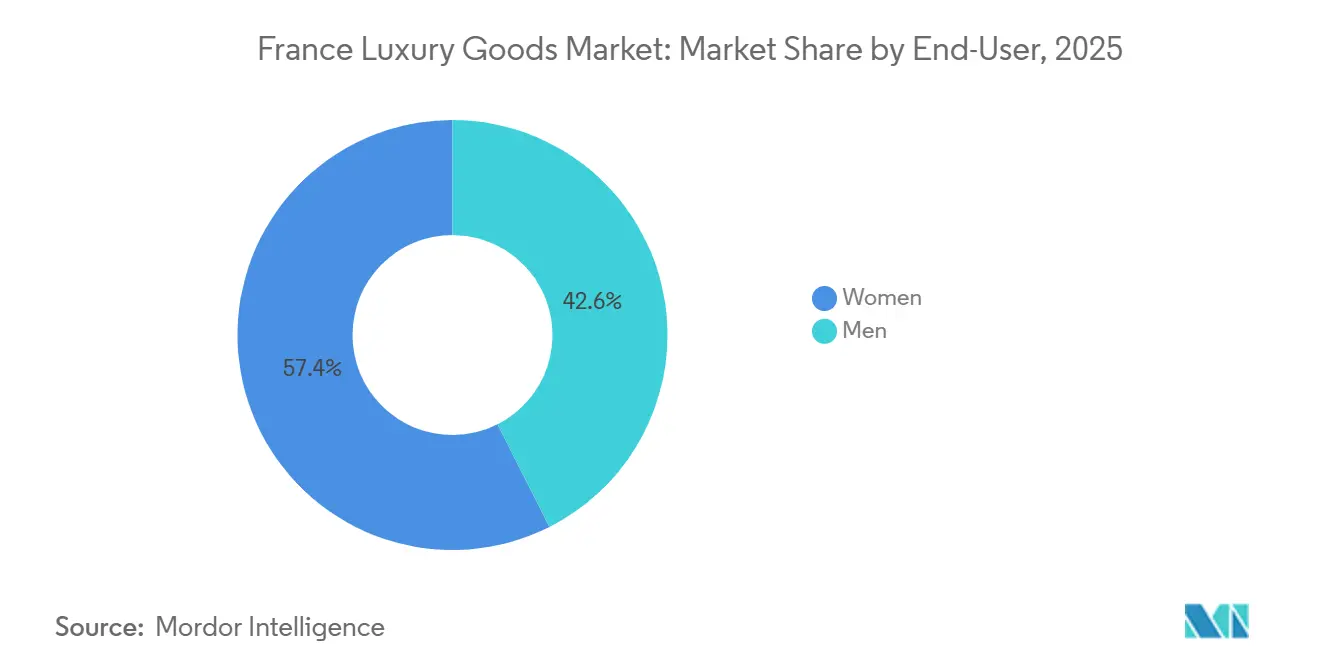

- By end user, women accounted for 57.44% of the French luxury goods market share in 2025; however, the men's segment is projected to post the highest growth at 5.27% over the forecast period.

- By distribution channel, single-brand stores held 38.05% of sales in 2025, whereas online stores are expected to expand at a 5.66% CAGR to 2031.

France Luxury Goods Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer Emphasis on Sustainability | +0.8% | Paris, Lyon, Premium paid for low-impact goods lifts sales | Medium term (2–4 years) |

| Influence of Social Media and Celebrity Endorsement | +0.6% | Paris, Nice, Influencer buzz converts younger shoppers quickly | Short term (≤ 2 years) |

| High Demand from Inbound Tourist | +1.2% | Paris, Riviera, High-spend visitors boost flagship revenues | Medium term (2–4 years) |

| Product Innovation in Raw Material and Design | +0.7% | Paris, Auvergne-Rhône-Alpes, Recycled materials and tech add desirability | Long term (≥ 4 years) |

| Rising Disposable Income Boosts Luxury Spending | +0.4% | Greater Paris, Bordeaux, Higher household earnings widen buyer pool | Short term (≤ 2 years) |

| Expansion of E-commerce Channels Enhances Accessibility | +0.5% | Nationwide metro areas, Online access extends reach beyond boutiques | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Consumer Emphasis on Sustainability

French luxury consumers increasingly prioritize circularity and traceability, reshaping product development and marketing narratives. Chanel launched its Nevold resale platform in 2024, enabling authenticated pre-owned handbag transactions that extend product lifecycles and capture secondary-market margin previously lost to third-party resellers. LVMH's LIFE 360 initiative, unveiled in 2024, commits the group to 100% renewable energy across European operations by 2026 and mandates that 70% of raw materials meet biodiversity-positive criteria by 2030. Kering's 2025 Environmental Profit & Loss statement quantified the house's EUR 400 million investment in regenerative agriculture for cashmere and leather, a move that signals a willingness to absorb near-term cost for long-term supply security. The EU's Digital Product Passport, effective from 2024, requires every luxury item to carry a scannable record of origin, materials, and repair history, effectively turning sustainability claims into auditable commitments. This regulatory backdrop favors incumbents with vertically integrated supply chains and penalizes brands reliant on opaque third-party sourcing.

Influence of Social Media and Celebrity Endorsement

Digital platforms and celebrity partnerships now drive discovery and conversion in ways that traditional advertising cannot replicate. Louis Vuitton's 2025 collaboration with makeup artist Pat McGrath generated over 500 million social media impressions within 72 hours of launch, demonstrating how influencer co-creation amplifies reach beyond paid media budgets. LVMH's 10-year partnership with Formula 1, announced in 2024, integrates TAG Heuer, Louis Vuitton, and Moët Hennessy into race-day activations that target affluent male audiences aged 25-45, a demographic historically underrepresented in luxury marketing. Hermès's entry into haute couture in 2024, led by creative director Nadège Vanhée-Cybulski, leveraged Instagram and TikTok teasers that generated 1.2 billion views before the first collection debuted, illustrating how heritage brands now embrace digital-first storytelling. Micro-influencers with 10,000 to 100,000 followers deliver engagement rates 3 times higher than celebrity mega-influencers, prompting brands like Longchamp and A.P.C. to seed products with niche fashion commentators rather than mass-market celebrities. This shift reflects a broader recognition that authenticity and niche credibility often outperform reach alone, particularly among Gen Z consumers who distrust overt sponsorship.

High Demand from Inbound Tourist

France continues to reinforce its status as the world's leading tourist destination, a position that has significantly driven the growth of the luxury goods market. The 2024 Olympic Games acted as a major catalyst for tourism, with international visitors playing a critical role in boosting luxury retail sales. Luxury brands, renowned for their country-of-origin appeal, maintain a strong presence across both online and offline channels in France. As one of Europe’s most visited destinations, France attracts a substantial number of Asian tourists, particularly for fashion and leisure activities. In 2024, France attracted 100 million international visitors, generating an international revenue of EUR 71 billion [1]Ministry of Economy and Finance, France, "2024, a Record Year for International Tourism in France", www.economie.gouv.fr . In response to this heightened demand, luxury retailers have implemented strategic expansion plans to capitalize on the growing market. For instance, Phoebe Philo expanded into the French luxury retail market by opening her first physical store in Galeries Lafayette Haussmann, Paris, in February 2025. This marks a significant step for the brand, which had previously only been available through online sales and limited in-person events.

Product Innovation in Raw Material and Design

Material innovation increasingly differentiates luxury offerings as consumers demand both novelty and sustainability. Hermès invested EUR 50 million in 2024 to expand its tannery network in France, focusing on vegetable-tanned leathers that eliminate chromium, a toxic byproduct of conventional tanning, while maintaining the supple hand-feel that defines the house's aesthetic. Chanel's 2025 Métiers d'Art collection incorporated lab-grown diamonds from Diamond Foundry, a move that addresses ethical sourcing concerns while preserving the visual and physical properties of mined stones. Kering's partnership with Mylo, a mycelium-based leather alternative, yielded commercial-scale production in 2024; the material debuted in limited-edition Gucci handbags priced at EUR 3,500, testing consumer willingness to pay premiums for bio-fabricated inputs. Richemont's Cartier division launched a modular jewelry line in 2025 that allows wearers to reconfigure gemstone settings, effectively transforming a single purchase into multiple designs and extending product utility. These innovations reflect a strategic pivot: luxury houses now compete on material provenance and adaptability rather than static design alone, recognizing that younger consumers value versatility and traceability as much as heritage craftsmanship.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of Counterfeit Products | –0.5% | Paris markets, Marseille port, Fakes erode brand trust and revenue | Medium term (2–4 years) |

| Lesser Demand From Price-Sensitive Consumers | –0.7% | Lille, Nantes, Inflation steers buyers to second-hand options | Short term (≤ 2 years) |

| Stringent Government Regulations | –0.4% | Nationwide, ESG and advertising rules raise compliance costs | Long term (≥ 4 years) |

| High Import Duties on Luxury Goods | –0.3% | Major ports, customs zones, Tariffs inflate input costs and retail prices | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Availability of Counterfeit Products

The surge in counterfeiting poses a significant threat to the luxury market. French customs seized more than 20 million counterfeit items in 2023, representing a twofold increase from 2022, with luxury goods being the primary target [2]The Manufacturers' Union Museum, “Annual customs report 2023”, musee-contrefacon.com. The rise of e-commerce has intensified the problem, with counterfeit networks increasingly turning to online platforms for their distribution. The widespread availability of counterfeit products acts as a significant restraint on the market, as it undermines the exclusivity and perceived value of genuine luxury items. Counterfeit goods often attract price-sensitive consumers, diverting demand away from authentic luxury products and impacting the revenue streams of legitimate brands. Additionally, the presence of counterfeit items in the market dilutes brand equity and creates challenges in maintaining consumer loyalty. In response to this escalating challenge, the French government rolled out the 2024–2026 National Anti-Counterfeiting Plan, bolstering enforcement ahead of the 2024 Olympics. Beyond mere economics, counterfeits tarnish brand reputation and diminish consumer trust. In a bid to safeguard their intellectual property, luxury brands are turning to cutting-edge authentication technologies, such as RFID (Radio-Frequency Identification) and NFC (Near Field Communication).

Lesser Demand from Price-Sensitive Consumers

Luxury price escalation outpaces wage growth, constraining access for aspirational buyers who historically fueled entry-level product sales. Chanel raised handbag prices by an average of 12% in 2024, pushing the Classic Flap to EUR 10,000, a threshold that excludes younger professionals and first-time luxury purchasers. Louis Vuitton's Neverfull tote, long positioned as an accessible gateway product, now retails at EUR 1,800, up from EUR 1,200 in 2020, reflecting a 50% cumulative increase that outstrips French inflation rates. This pricing strategy prioritizes margin over volume, a deliberate shift that insulates brands from discounting but alienates price-sensitive cohorts. Middle-income French consumers, facing stagnant real wages and elevated housing costs, increasingly defer luxury purchases or trade down to contemporary brands like Sandro and Maje that offer similar aesthetics at 60% lower price points. The bifurcation creates strategic tension: brands must balance exclusivity, which demands high prices and limited availability, with the need to cultivate the next generation of loyal customers who may lack purchasing power in their 20s and 30s.

Segment Analysis

By Product Type: Apparel Dominates, Leather Goods Accelerates

Clothing and Apparel held 43.03% of the market share in 2025, reflecting France's historical dominance in haute couture and ready-to-wear. However, Leather Goods is forecast to grow at 4.96% from 2026 to 2031, outpacing apparel's more modest trajectory. Hermès's scarcity-driven model exemplifies this dynamic: the house limits Birkin and Kelly bag production to preserve artisan craftsmanship, sustaining waitlists that span years and reinforcing the perception of unattainable luxury. Louis Vuitton's 2024 launch of the Twist bag in vegan leather, priced at EUR 2,500, tested consumer acceptance of bio-fabricated materials, with initial sell-through rates exceeding 80%. Footwear benefits from the casualization of luxury: Chanel's 2025 introduction of a EUR 1,200 sneaker line, blending heritage tweeds with technical soles, captured younger buyers who prioritize comfort without sacrificing brand signaling.

Eyewear and Watches cater to distinct buyer motivations; eyewear serves as an accessible entry point, while watches function as investment-grade collectibles. Cartier's 2024 launch of the Panthère de Cartier sunglasses, retailing at EUR 800, leveraged the house's jewelry heritage to command premium pricing in a category dominated by EssilorLuxottica's licensed brands. Rolex maintained production discipline in 2025, restricting supply to sustain secondary-market premiums that often exceed retail prices by 30-50%. Jewelry and Beauty & Personal Care segments benefit from gifting occasions and repeat purchase behavior. Chanel's integration of lab-grown diamonds in its 2025 Métiers d'Art collection addressed ethical sourcing concerns while preserving the visual properties of mined stones.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User: Women Lead, Men Surge

Women accounted for 57.44% of market share in 2025, yet Men's luxury is projected to grow at 5.27% through 2031, reflecting shifting gender norms and the rise of male grooming and fashion consciousness. Hermès's 2024 expansion of its men's ready-to-wear line, including tailored suiting priced at EUR 5,000 per piece, targets professionals who view luxury as a career investment rather than discretionary spending. Louis Vuitton's men's fragrance line, launched in 2024, generated EUR 200 million in first-year sales, demonstrating latent demand for male-targeted luxury beyond apparel and accessories. Younger men, particularly those aged 25-40, increasingly purchase luxury sneakers, watches, and grooming products as identity markers, with average transaction values rising year-on-year in 2024.

Women's luxury remains anchored in handbags, ready-to-wear, and beauty, with Chanel, Dior, and Hermès commanding the highest brand loyalty. The Unisex segment, while smaller, benefits from gender-fluid design trends; brands like A.P.C. and Longchamp position core products, tote bags, outerwear, and accessories as non-gendered essentials that appeal across demographics. This segmentation reflects broader cultural shifts where luxury increasingly signals personal values and identity rather than conforming to traditional gender roles.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Single-Brand Stores Hold, Online Surges

Single-brand stores maintain the largest market share at 38.05% in 2024, offering controlled brand experiences and direct consumer relationships. However, online stores are growing most rapidly at 5.66% CAGR through 2030, reflecting the sector's digital transformation. This shift in channels mirrors broader retail trends, a change hastened by the pandemic. Consumers are now more at ease buying luxury goods online, sidestepping the need for in-store testing. This online surge is especially beneficial for brands as it allows them to connect with specific consumer segments without the need for a physical retail presence.

The penetration of e-commerce in the luxury market has accelerated, with digital platforms particularly appealing to millennials and Gen Z, who increasingly prefer purchasing high-value products online. For instance, as of January 2024, the fashion category accounted for the majority of online purchases in France, according to the Federation of E-commerce and Distance Selling [3]Federation of E-commerce and Distance Selling (Fevad), “Chiffres Clés E-Commerce”, fecad.com. Social media and influencer marketing have expanded the visibility and aspirational appeal of luxury brands to a broader audience. Multi-brand department stores remain key for discovery, especially among tourists who bundle purchases with tax-refund services. The France luxury goods market size attached to omnichannel services grows because clients now expect to reserve products online, try them offline and finalize payment on either channel.

Competitive Landscape

The French luxury goods market is moderately concentrated, with domestic and international players striving to capture significant market share. Prominent players dominating the market include Hermès International S.A., LVMH Moët Hennessy Louis Vuitton SE, L'Oreal SA, Compagnie Financière Richemont S.A., and Kering SA, among others. These brands compete by leveraging factors such as premium packaging, attractive offers, exceptional quality, comfort, and an extensive product portfolio. LVMH manages 75 brands across fashion, jewelry, cosmetics, wines, and hospitality, delivering EUR 19.6 billion operating profit in 2024.

Competition has intensified in the area of sustainability, with Kering setting benchmarks through science-based targets and transparent reporting practices. Additionally, digital capabilities have become a critical competitive factor, prompting brands to invest significantly in omnichannel strategies and content development. To enhance their market positions, leading companies are also focusing on strategies such as collaborating with regional brands and introducing innovative luxury products.

The certified pre-owned programs play a pivotal role in safeguarding brand equity. By tagging serial numbers on a public blockchain, luxury houses can verify ownership transfers, a move that not only deters counterfeiting but also resonates with younger consumers. Brands maintain a disciplined approach to pricing, steering clear of widespread discounts. Instead, they opt for personalized clienteling, discreetly managing seasonal leftovers. Collectively, these strategies bolster the French luxury goods market against potential disruptors and heighten the switching costs for its loyal clientele.

France Luxury Goods Industry Leaders

-

Compagnie Financière Richemont S.A.

-

LVMH Moët Hennessy Louis Vuitton SE

-

Kering SA

-

L'Oreal SA

-

Hermès International S.A.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: Hermès Paris released six handbags in its Fall-Winter 2025 collection. The designs incorporate geometric elements, featuring angular edges, structured shoulders, and contoured silhouettes.

- March 2025: Chanel acquired a 20% stake in Tuscany-based Leo France, bolstering its supply chain and manufacturing prowess of costume jewelry and metal accessories for clothing, bags, and other leather goods.

- February 2025: L'Oréal strengthened its luxury portfolio in the France market by acquiring niche fragrance brands, Jacquemus and Amouage, aiming to capitalize on the expanding premium fragrance market.

- January 2024: Prada Beauty, a division of L’Oréal Groupe, established its first permanent beauty counter in France at Samaritaine Paris through a strategic partnership with DFS Group. The counter features the brand’s comprehensive range of skincare, makeup, and fragrance products.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our team defines the France luxury goods market as the annual domestic and tourist spend on premium fashion, leather goods, watches, jewelry, eyewear, and prestige beauty products that command consistently high price points, limited production runs, and branded craftsmanship. Goods are tracked at the sell-through stage across physical flagships, multi-brand boutiques, duty-free outlets, and direct-to-consumer digital storefronts.

Scope Exclusions: Products such as super-premium automobiles, luxury hospitality services, fine wines, and real estate are not counted because they follow markedly different demand drivers and valuation logics.

Segmentation Overview

- Product Type

- Clothing and Apparel

- Footwear

- Eyewear

- Leather Goods

- Jewelry

- Watches

- Beauty and Personal Care

- End-User

- Men

- Women

- Unisex

- Distribution Channel

- Single-Brand Stores

- Multi-Brand Stores

- Online Stores

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed brand executives, specialty retailers, supply-chain consultants, and tax-free refund operators across Paris, Nice, and Lyon. Conversations confirmed average transaction values, tourist share of sales, and e-commerce conversion rates, enabling us to bridge gaps found in public statistics and adjust preliminary estimates.

Desk Research

We mapped the demand pool using tier-1 public datasets, including INSEE retail trade surveys, Eurostat household expenditure sheets, French Customs CN8 export codes, UN Comtrade re-imports, and tourism VAT refund tallies, supplemented with press releases, company filings, and news retrieved through D&B Hoovers and Dow Jones Factiva. These sources established baseline consumption levels, price corridors, and category splits.

Industry association white papers from the Fédération de la Haute Couture et de la Mode, Banque de France consumer confidence dashboards, and patent abstracts from Questel helped us sense-check innovation pipelines and pricing power. The sources listed are illustrative; numerous additional publications and databases informed data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down build began with retail sales and inbound tourist outlays, which are then filtered through category-level penetration, average selling price trends, and return rates before being validated via selective bottom-up roll-ups of flagship store counts and sampled volumes. Key model inputs include high-net-worth individual growth, international visitor arrivals, duty-free ticket volumes, exchange-rate movements, and domestic online luxury penetration. Forecasts rely on a multivariate regression blend that relates those indicators to historical spending curves. Scenario analysis is applied when regulatory or macro shocks alter baseline trajectories. Where outlet-level data were sparse, interpolation was guided by price elasticity benchmarks gathered in primary interviews.

Data Validation & Update Cycle

All outputs pass a two-step analyst review, with variance checks against external market barometers and anomaly flags routed back to respondents when necessary. We refresh models annually and issue interim revisions after material events so clients receive a current, reconciled view.

Why Mordor's France Luxury Goods Baseline Remains Dependable

Published figures often diverge because providers choose different product baskets, capture points, and refresh cadences, which can push totals meaningfully apart.

Key gap drivers stem from whether tourist purchases are counted, the breadth of beauty and accessories lines included, currency translation dates, and how quickly post-pandemic rebound data are embedded.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 24.81 B (2025) | Mordor Intelligence | - |

| €19.25 B (2025) | Regional Consultancy A | Omits prestige cosmetics and excludes tourist spend, relying solely on domestic retail registers |

| USD 17.1 B (2024) | Global Consultancy B | Uses prior-year base and drops digital sales; limited segmentation depth |

| USD 4.3 B (2024) | Industry Association C | Focuses on ultra-luxury tier only and samples listed firms, overlooking independent maisons |

The comparison shows that once scope, channels, and exchange assumptions are aligned, gaps narrow considerably, underscoring why Mordor's balanced, source-traceable model offers decision-makers a dependable starting point for strategy and valuation.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the France luxury goods market in 2026?

The market is valued at USD 25.81 billion in 2026.

What is the expected CAGR for luxury goods sales in France to 2031?

Sales are projected to rise at a 4.89% CAGR through 2031.

Which product category is growing the fastest in France?

Leather goods are forecast to grow at a 4.96% CAGR, outpacing other categories.

Why is men’s demand expanding so quickly?

Younger male consumers treat premium sneakers, grooming, and tailoring as expressions of identity, driving a 5.27% CAGR for the segment.

Page last updated on: