Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

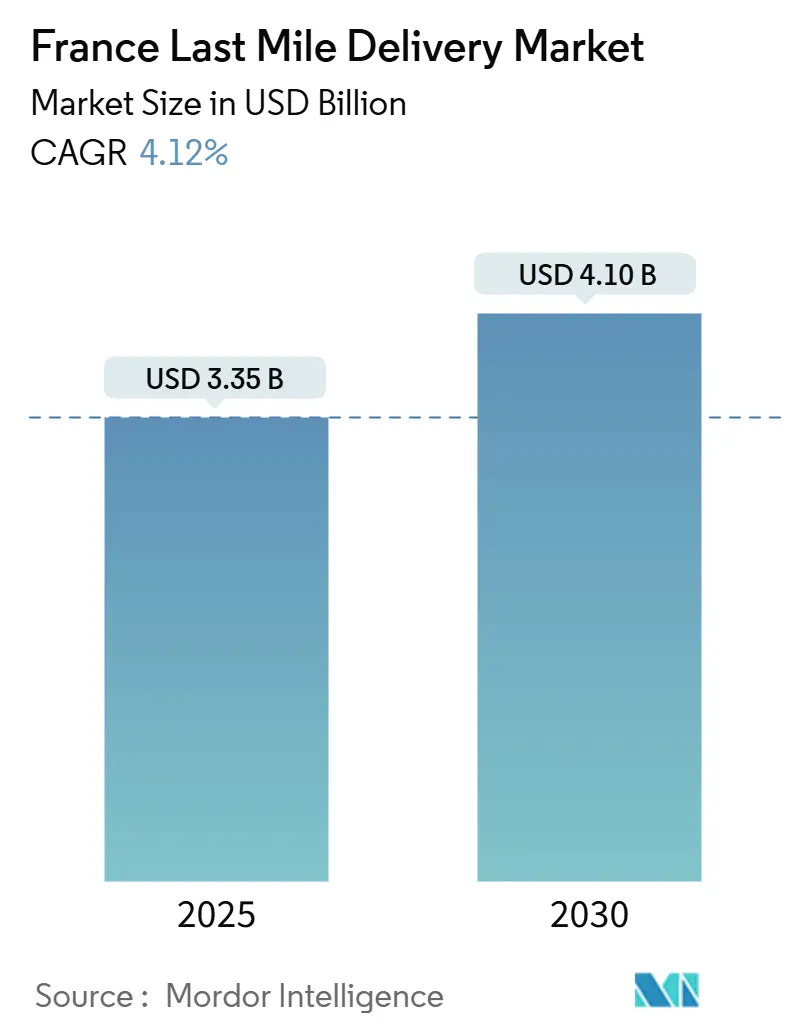

| Market Size (2025) | USD 3.35 Billion |

| Market Size (2030) | USD 4.10 Billion |

| Growth Rate (2025 - 2030) | 4.12% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Last Mile Delivery Market Analysis by Mordor Intelligence

The France last mile delivery market size stands at USD 3.35 billion in 2025 and is forecast to climb to USD 4.1 billion by 2030, yielding a 4.12% CAGR over the period. Demand scales with e-commerce volume growth, the densification of parcel-locker networks, and government incentives that accelerate fleet electrification. Competitive intensity has risen as global integrators, regional parcel specialists, and digital platforms jostle for route density and locker access, forcing operators to adjust tariffs in response to low-value cross-border parcels. Urban congestion, courier shortages, and scarce micro-hub real estate temper growth, yet investment in dark-store partnerships and temperature-controlled logistics continues to open premium service niches. Profitability now hinges on automated sortation, pickup-drop-off (PUDO) diversification, and zero-emission vehicle deployment, each delivering incremental cost and access advantages in heavily regulated urban cores.

Key Report Takeaways

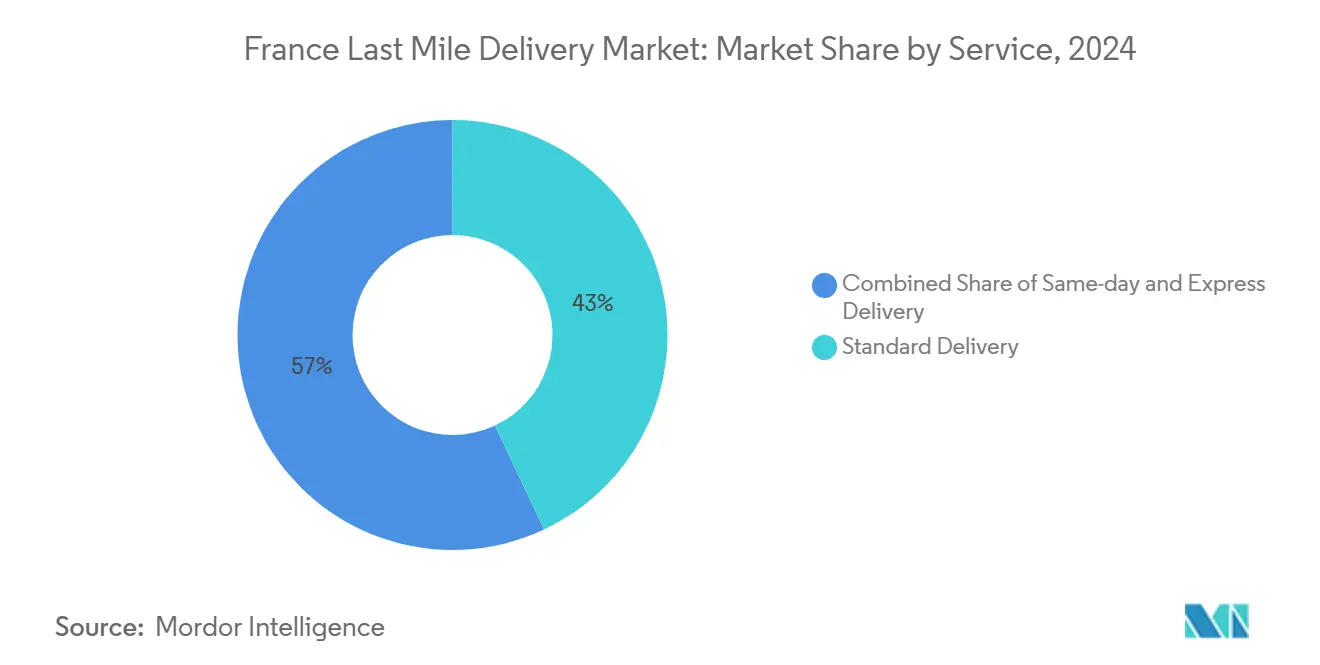

- By service, Standard Delivery held 43% of the France last mile delivery market share in 2024. Same-day delivery is projected to expand at a 3.80% CAGR through 2030.

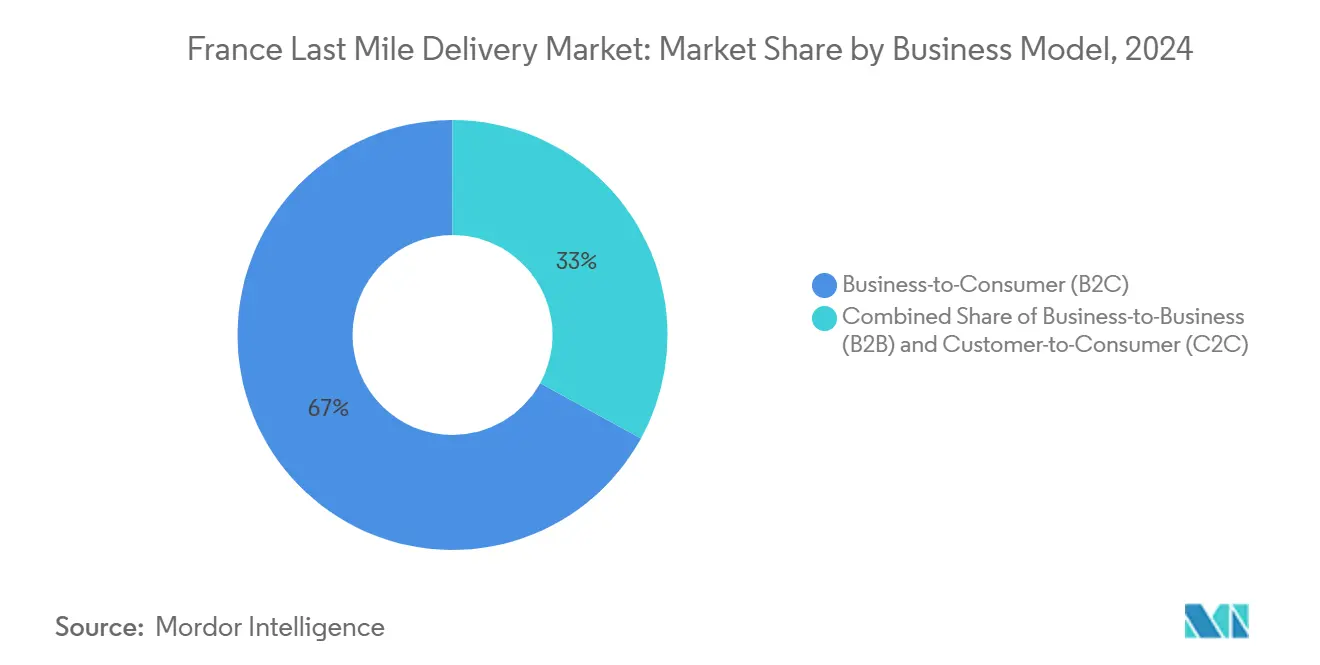

- By business model, the B2C segment accounted for a 67% share of the France last mile delivery market size in 2024. Customer-to-Consumer transactions are forecast to grow at a 4.10% CAGR between 2025-2030.

- By end-user industry, e-commerce retail commanded a 39% share of the France last mile delivery market size in 2024, and healthcare delivery is advancing at a 3.70% CAGR through 2030.

- By region, Île-de-France contributed 23% revenue in 2024 and is expected to register the highest regional CAGR of 3.50% to 2030.

France Last Mile Delivery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion in e-commerce order volume | +1.2% | National, concentrated in Île-de-France, Auvergne-Rhône-Alpes | Short term (≤ 2 years) |

| Expansion of parcel locker & PUDO infrastructure | +0.8% | Urban centers, expanding to suburban areas | Medium term (2-4 years) |

| Government incentives for zero-emission delivery fleets | +0.6% | Major metropolitan areas, Paris intra-muros priority | Medium term (2-4 years) |

| Growth of urban dark stores & nano-fulfilment | +0.5% | Île-de-France, Lyon, Marseille metropolitan areas | Short term (≤ 2 years) |

| Social commerce boosts micro-shipment frequency | +0.4% | National, higher penetration in urban areas | Long term (≥ 4 years) |

| Municipal mandates for urban consolidation centres | +0.3% | Major cities, pilot programs in Toulouse, Nantes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosion in e-commerce order volume

La Poste’s Colissimo processed millions of parcels in 2024. Higher order density fuels network expansion, evidenced by Geopost’s capital spend on automated sorters and depots in 2024. Yet profitability diverges: lightweight shipments from platforms such as Shein and Temu carry wafer-thin yields even as they lift headline volumes. Operators counter margin pressure by upselling tracked, scheduled, or carbon-neutral options that command premium fees.

Expansion of parcel locker & PUDO infrastructure

La Poste hosts 128,000 pickup points and lockers—the densest network in Europe, cutting failed-delivery costs and lifting customer satisfaction scores. InPost-owned Mondial Relay raised its automated locker count to 7,000 by 2025 while pruning low-traffic retail agents[1]Matthieu Guinebault, “Mondial Relay: moins de commerces, plus de consignes automatiques?,” fashionnetwork.com . Nearly 30% of Mondial Relay’s 62.3 million Q3-2024 parcels flowed through lockers, signaling shopper preference for flexible, contactless retrieval. For carriers, locker density collapses last-mile unit cost by consolidating multiple drop-offs into a single location, improving driver productivity and shrinking carbon intensity.

Government incentives for zero-emission delivery fleets

National grants plus municipal access mandates spur operators to electrify. Paris will restrict diesel parcel vans inside the Périphérique by the end of 2024, effectively granting zero-emission fleets exclusive curbside access during peak hours[2]La Poste Group, “La Poste Groupe 2024 results,” lapostegroupe.com . La Poste earmarked 40% of its 2024-2025 cap-ex for depot electrification and charging upgrades, positioning its 37,000-unit electric fleet to cover 50% of urban routes by 2026. Operators report 15% lower energy outlay and 30% lower maintenance expense per electric van versus diesel equivalents, narrowing total-cost-of-ownership gaps.

Growth of urban dark stores & nano-fulfillment

Consolidation trimmed France’s hyper-fast grocery sector, yet survivors pivot to profitable 30-minute windows by embedding micro-fulfillment inside legacy supermarkets. Stuart and Klareo now orchestrate sub-2-hour delivery for 1,320 Intermarché outlets, blending store inventory with courier fleets that average 13 orders per urban route. Chronofresh extended temperature-controlled coverage to seven European markets, validating vertical-specific micro-fulfillment. Dark-store economics depend on algorithmic demand forecasts and just-in-time inventory, prompting tech investments that squeeze out under-capitalized entrants.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban traffic & parking constraints | -0.7% | Major metropolitan areas, particularly Paris, Lyon, Marseille | Short term (≤ 2 years) |

| Courier labour shortages & wage inflation | -0.9% | National, acute in urban centers | Medium term (2-4 years) |

| Scarcity of urban micro-hub real estate | -0.5% | Dense urban centers, particularly Paris, Lyon metropolitan areas | Medium term (2-4 years) |

| Public resistance & drone-regulation hurdles | -0.3% | Urban areas, regulatory restrictions nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urban traffic & parking constraints

Paris ranks among Europe’s top three congestion hot spots, pushing average urban route speed below 13 km/h and inflating driver hours per stop[3]Cushman & Wakefield, “City Logistics,” cushmanwakefield.com. Municipal curb fees and reduced delivery windows squeeze capacity, forcing split-shift scheduling that raises labor requirements. Developers respond with urban consolidation centers like SEGRO’s Les Gobelins, a 1,600-m² hub fifteen minutes from central Paris. Such micro-hubs shave 1.3 km off average last-leg distance, yet the limited availability of industrial-zoned plots curtails widespread replication.

Courier labor shortages & wage inflation

France posts over 50,000 open courier positions, with urban attrition rates exceeding 25% annually[4]E-Commerce Mag, “Prestataire Logistique – Logistique : les dernières actualités,” ecommercemag.fr. Rising fuel and housing costs erode driver earnings; platforms counter with minimum-earning guarantees, but retention struggles persist. Wage inflation now runs 7-9% for licensed van drivers, lifting operators’ cost bases and prompting accelerated locker deployment to dilute driver reliance. Uncertainty around potential reclassification of gig couriers as employees could push cost structures another 15-20% higher over the medium term.

Segment Analysis

By Service: Standard Delivery remains volume anchor while Same-day scales premium niches

Standard Delivery captured 43% of the France last mile delivery market share in 2024 by leveraging established postal depots, long-haul line-hauls, and cost-efficient batch sorting. The segment supplies predictable workloads that optimize hub-and-spoke infrastructure, sustaining favorable drop‐density economics across suburban and rural routes. Volume leadership persists even as consumers upgrade to faster tiers for mission-critical items. Same-day services, advancing at a 3.80% CAGR, ride urban shopper expectations for immediacy and retailer promises of “order-by-1 pm-receive-today.” Operators bundle premium fees with carbon-neutral badges to preserve margin. Express Delivery holds steady as a business account staple for time-definite B2B shipments, filling the gap between economy and same-day.

Growth differentials hint at a bifurcated future where convenience-led SKUs flow through rapid-cycle channels, while bulkier, lower-value items continue in economy lanes. Retailers increasingly offer hybrid cart checkout, letting shoppers split baskets between same-day perishables and slower, free-shipping lines. That elasticity underpins incremental revenue while preventing network overload. For carriers, orchestrating multi-speed promises within a single route remains the primary optimization frontier, demanding dynamic dispatching and real-time capacity visibility.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Business Model: B2C dominance meets surging C2C circular-commerce flows

The B2C channel contributed 67% of the France last mile delivery market size in 2024 as omnichannel retailers punched up online conversion through click-and-collect, free returns, and locker integration. Scale affords negotiated carrier rates and fuels capital outlays for dedicated fulfillment centers. Yet C2C volumes, expanding at 4.10% CAGR, signal a structural pivot toward recommerce. Platforms like Vinted and Leboncoin tap La Poste’s Colissimo API, letting sellers print discounted labels and drop parcels at 17,000 post offices, radically lowering friction. Peer-to-peer trades diversify parcel weights and irregular dimensions, challenging sortation systems originally built for standardized e-tailer boxes. Carriers respond with mixed-flow sorters and AI-enhanced address verification to hold cost per piece roughly in line with B2C averages.

B2B traffic remains structurally important for office supplies and industrial spares but grows modestly amid digital procurement maturation and supplier fleet self-delivery. Strategic alliances between express carriers and manufacturers aim to preserve high-margin pre-9 am services where reliability trumps price sensitivity.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-user Industry: Healthcare unlocks regulated growth corridors

E-commerce Retail retained the largest revenue share at 39% in 2024, but its CAGR plateaus as penetration nears saturation in core consumer categories. Conversely, Healthcare & Medical Supplies charts a 3.70% CAGR through 2030, buoyed by aging demographics, telemedicine uptake, and relaxed regulations allowing direct-to-patient delivery of prescription drugs. La Poste’s “Mes Médicaments Chez Moi” service pilots temperature-controlled satchels and pharmacist teleconsult verification, underscoring compliance-led differentiation. Cold-chain specialists such as Chronofresh scale modular refrigerated vans and box-in-box payloads to guarantee stability.

Fashion & Lifestyle and Beauty & Personal Care continue mid-single-digit growth, supported by free-return policies and influencer-driven flash drops that migrate to same-day channels for launch-day buzz. Home & Furniture lags as oversized parcel handling inflates failed-delivery risk, prompting white-glove two-man crews for premium items. Consumer Electronics balances shrinkage concerns with rising average selling prices, steering high-value gadgets toward tracked, signature-required tiers that generate above-system average yields.

Geography Analysis

Île-de-France generated 23% of the revenue in 2024 and forecasts a 3.50% CAGR through 2030, mirroring its population density and corporate head-office concentration. The region’s early adoption of parcel lockers and consolidation centers like SEGRO Les Gobelins compresses last-mile distance and unlocks 15% operating cost savings relative to legacy suburban depots. Paris’s zero-emission zone mandates fast-track electric fleet rollout, incentivizing carriers to pool charging infrastructure and lobby for curb-space allocation.

Auvergne-Rhône-Alpes, Provence-Alpes-Côte d’Azur, and Hauts-de-France collectively account for 31% turnover, benefiting from multimodal connectivity via the A6, A7, and Channel Tunnel corridors. Growth runs just below the national mean as lower density inflates cost per stop, yet city councils in Lyon and Marseille broaden parcel-locker coverage, elevating first-attempt success rates by 8-10 points. These regions entice carriers with brownfield warehouses along ring roads, converting legacy manufacturing plots into cross-dock depots adapted for night-sort cycles.

Competitive Landscape

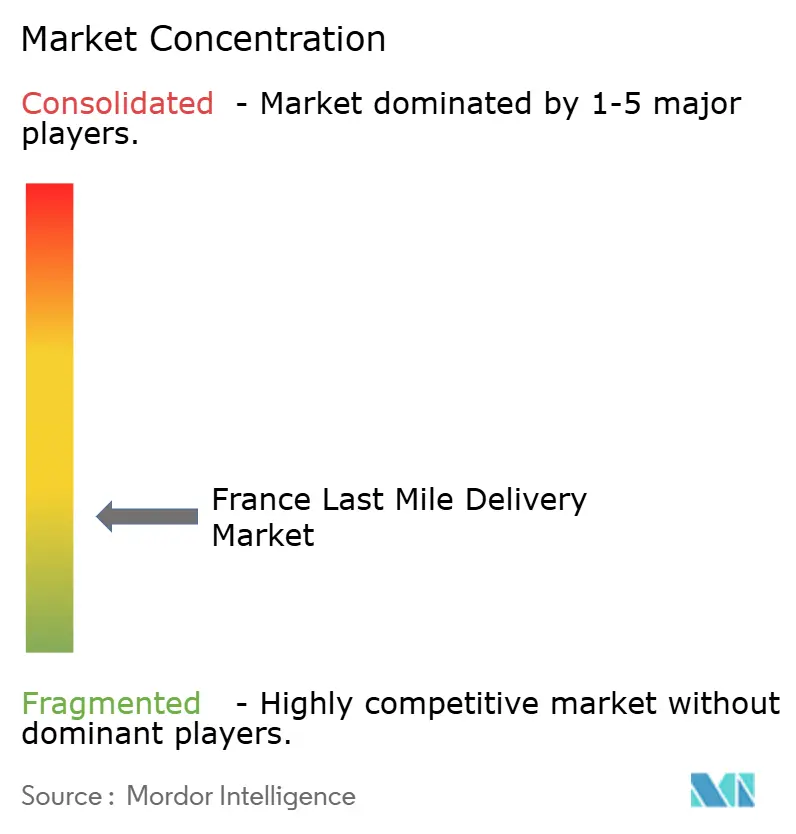

France’s last mile delivery arena exhibits moderate fragmentation. Incumbents DPD France, La Poste’s Colissimo and Chronopost, and Mondial Relay command route density, locker footprint, and customer familiarity. Global integrators DHL Express, FedEx, and UPS capture high-value international e-commerce traffic and time-definite B2B consignments, leveraging bonded hubs at Roissy-CDG and Lyon-Saint-Exupéry.

Strategic maneuvers center on infrastructure densification. Mondial Relay swapped 1,800 low-volume corner shops for 1,000 automated lockers in 2024, lifting parcel throughput per site by 35%. Colis Privé added 2,000 pickup points via Welco home-storage tie-ups, extending parcel reach into rural communes. DPD France launched the “Singular” digital showcase in 2025 to onboard SME sellers, bundling web storefronts with logistics APIs to defend the B2C share.

Technology disruptors Cubyn, Wing, and eShopWorld overlay cloud labels, predictive ETAs, and embedded carbon calculators to woo scaled Shopify merchants. Their asset-light model rents overnight sort capacity from mid-tier carriers, then purchases last-mile slots at volume-discount prices. Investors reward these platforms for software margins, yet route control still lies with incumbents who own vans, lockers, and depots.

France Last Mile Delivery Industry Leaders

Colissimo (La Poste Group)

Chronopost

DPD

Mondial Relay (InPost)

DHL Express

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2025: La Poste extends its Vinted partnership, enabling mailbox and post-office drop-off for second-hand parcels.

- June 2025: DHL Express opens a multi-service facility at Lyon-Saint-Exupéry Airport, integrating TDI and DDI flows.

- September 2024: GLS inaugurates a national hub at Coudray-Montceaux, adding 30% sort capacity to southern Paris routes.

- January 2024: La Poste extends its Vinted partnership, enabling mailbox and post-office drop-off for second-hand parcels.

France Last Mile Delivery Market Report Scope

In order to accommodate the growing demand, the companies are expanding its resources to increase the number of deliveries per day. With this, alternatives, such as click-to-collect locations and local regional carriers are also gaining popularity.

Besides these, the last mile delivery market is associated with some challenges, such as traffic in the urban areas leading to high fuel costs and the regulations of the government on trucks regarding the environmental concerns, which may hamper the growth of the market up to some extent. The lack of proper tracking systems and transportation management systems (TMS) to handle increasing services may lead to high costs effecting the final mile delivery market.

France Last Mile Delivery Market is segmented by service (Business-to-business (B2B), Business-to-consumer (B2C), Customer-to-customer (C2C)).

By Service

| Standard Delivery |

| Same-day |

| Express Delivery |

By Business Model

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Customer-to-Consumer (C2C) |

By End-user Industry

| E-commerce Retail |

| Fashion & Lifestyle |

| Beauty, Wellness & Personal Care |

| Home & Furniture |

| Consumer Electronics & Appliances |

| Healthcare & Medical Supplies |

| Others |

By French Region

| Île-de-France |

| Auvergne-Rhône-Alpes |

| Provence-Alpes-Côte d’Azur |

| Hauts-de-France |

| Nouvelle-Aquitaine |

| Occitanie |

| Grand Est |

| Brittany |

| Others |

| By Service | Standard Delivery |

| Same-day | |

| Express Delivery | |

| By Business Model | Business-to-Business (B2B) |

| Business-to-Consumer (B2C) | |

| Customer-to-Consumer (C2C) | |

| By End-user Industry | E-commerce Retail |

| Fashion & Lifestyle | |

| Beauty, Wellness & Personal Care | |

| Home & Furniture | |

| Consumer Electronics & Appliances | |

| Healthcare & Medical Supplies | |

| Others | |

| By French Region | Île-de-France |

| Auvergne-Rhône-Alpes | |

| Provence-Alpes-Côte d’Azur | |

| Hauts-de-France | |

| Nouvelle-Aquitaine | |

| Occitanie | |

| Grand Est | |

| Brittany | |

| Others |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How fast will parcel lockers expand in France by 2030?

Locker and PUDO points are growing 8-10% annually and could top 160,000 sites by 2030, cutting failed deliveries and per-parcel costs.

Which segment grows quickest through 2030?

Same-day services post the strongest lift at a 3.80% CAGR, fueled by urban shopper expectations and dark-store partnerships.

What is the role of electric vans in urban delivery?

Zero-emission vans already cover 37,000 routes; by 2026 they will service half of Paris stops, helped by grants and access privileges.

How large is healthcare’s share of parcel flows?

Healthcare & Medical Supplies still represent a single-digit share but grow at 3.70% CAGR, outpacing overall parcel growth.

Which region holds the greatest revenue share?

Île-de-France leads with 23% of national revenue and enjoys the fastest regional growth at 3.50% CAGR.

What constrains rural service expansion?

Lower parcel density inflates cost per stop; carrier economics rely on universal-service subsidies and new micro-hub pilots.