France Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

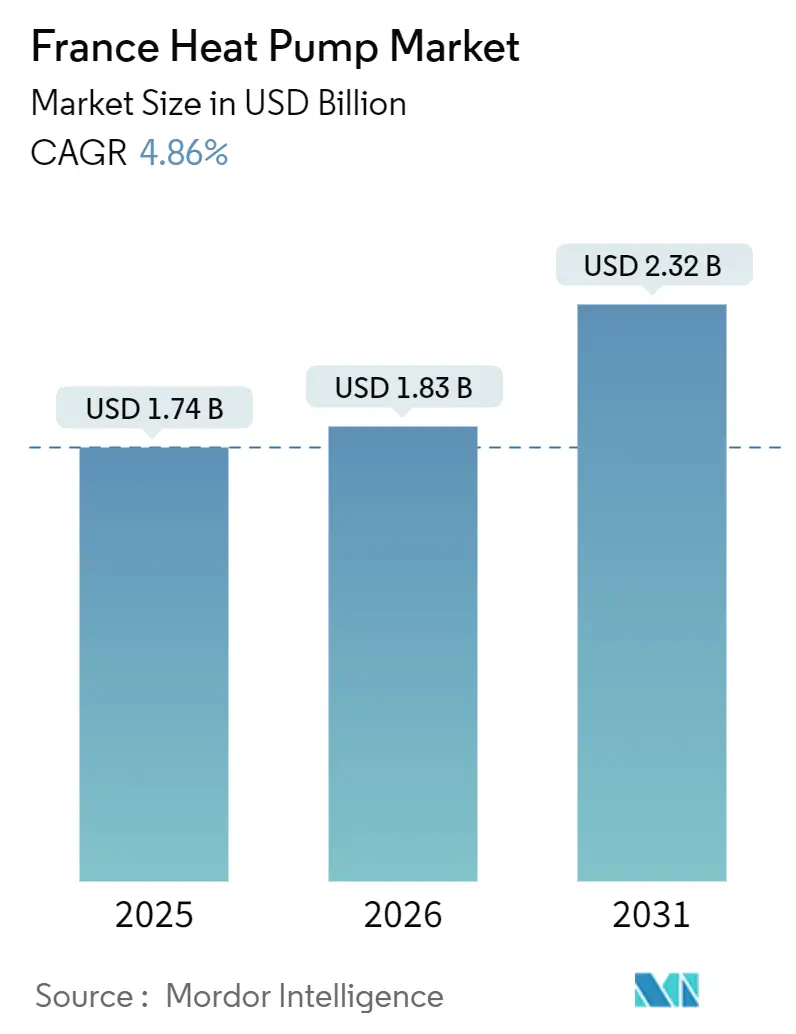

| Base Year Market Size (2025) | USD 1.74 Billion |

| Market Size (2026) | USD 1.83 Billion |

| Market Size (2031) | USD 2.32 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

France Heat Pump Market Analysis by Mordor Intelligence

The France heat pump market size is valued at USD 1.83 billion in 2026, up from USD 1.74 billion in 2025, and is projected to reach USD 2.32 billion by 2031, growing at a 4.86% CAGR over 2026-2031. A steep 12% volume decline in 2024 reset the growth base, but robust subsidies, strict carbon ceilings, and a domestic-manufacturing tilt are reinforcing the rebound in 2026. Policy levers such as the RE2020 building code favor heat pumps over fossil boilers, while the January 2026 revision of MaPrimeRénov’ channels premium rebates toward European-built equipment. These conditions encourage localized assembly, evidenced by Atlantic’s Saône-et-Loire plant and Bosch’s acquisition-driven capacity expansion. Vendor strategies coalesce around R290 refrigerant platforms, smart-grid functionality, and pay-per-use contracting models that transfer capital risk away from households.

Key Report Takeaways

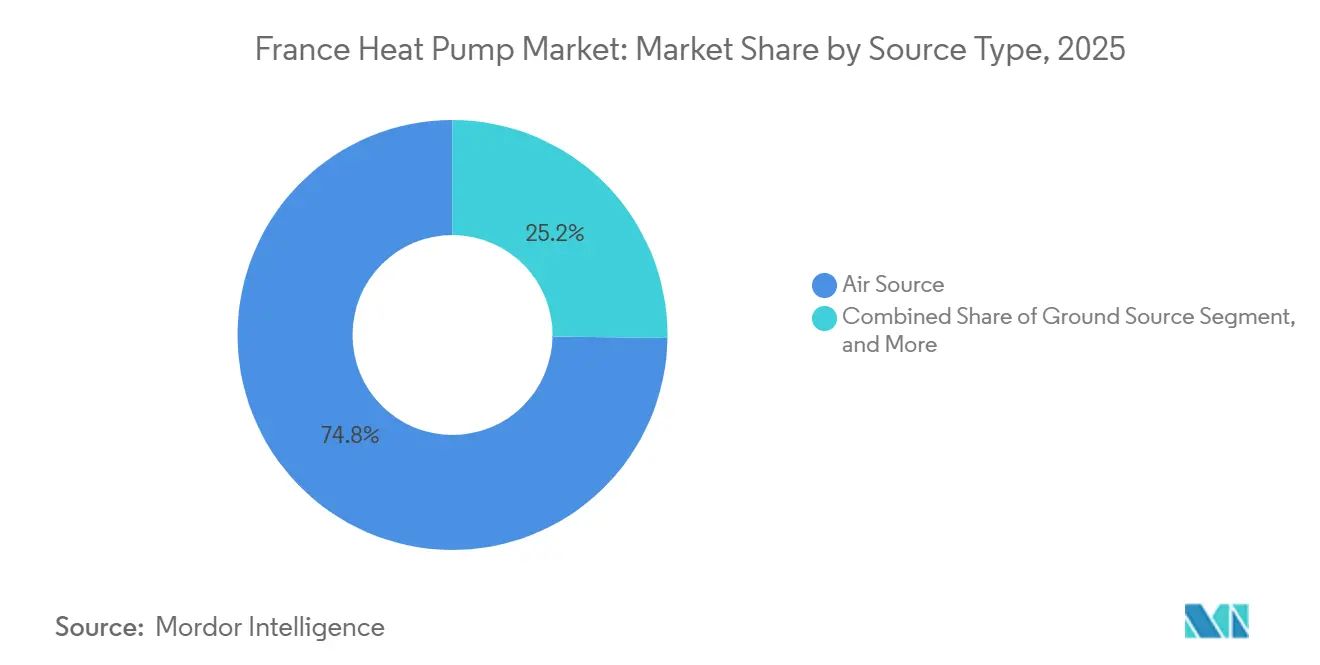

- By type, air-source systems led with 74.78% revenue share in 2025; ground-source alternatives are forecast to expand at a 5.31% CAGR through 2031.

- By technology, air-to-water held 65.86% of the France heat pump market share in 2025, while ground-to-water is projected to grow at 5.14% CAGR.

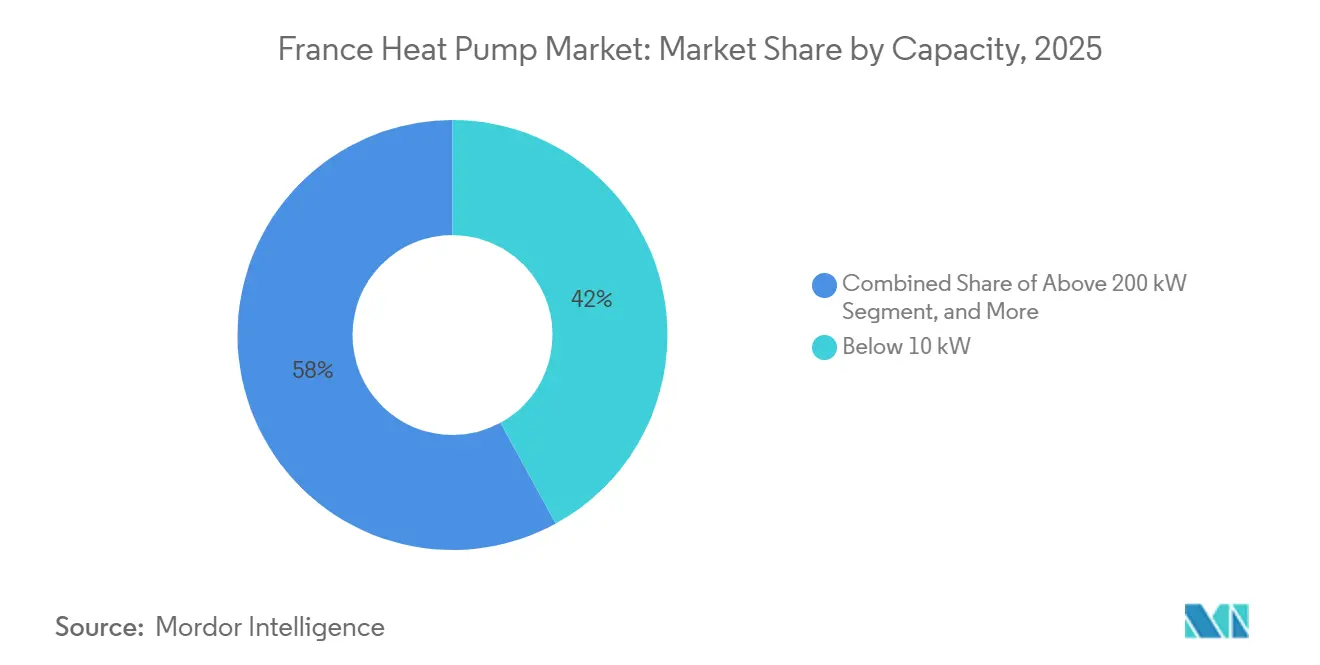

- By capacity, sub-10 kW units accounted for 42.03% of 2025 sales; the 50-200 kW band shows the highest projected CAGR at 5.34% to 2031.

- By application, space heating represented 62.74% of 2025 revenue and space cooling is advancing at a 5.27% CAGR through 2031.

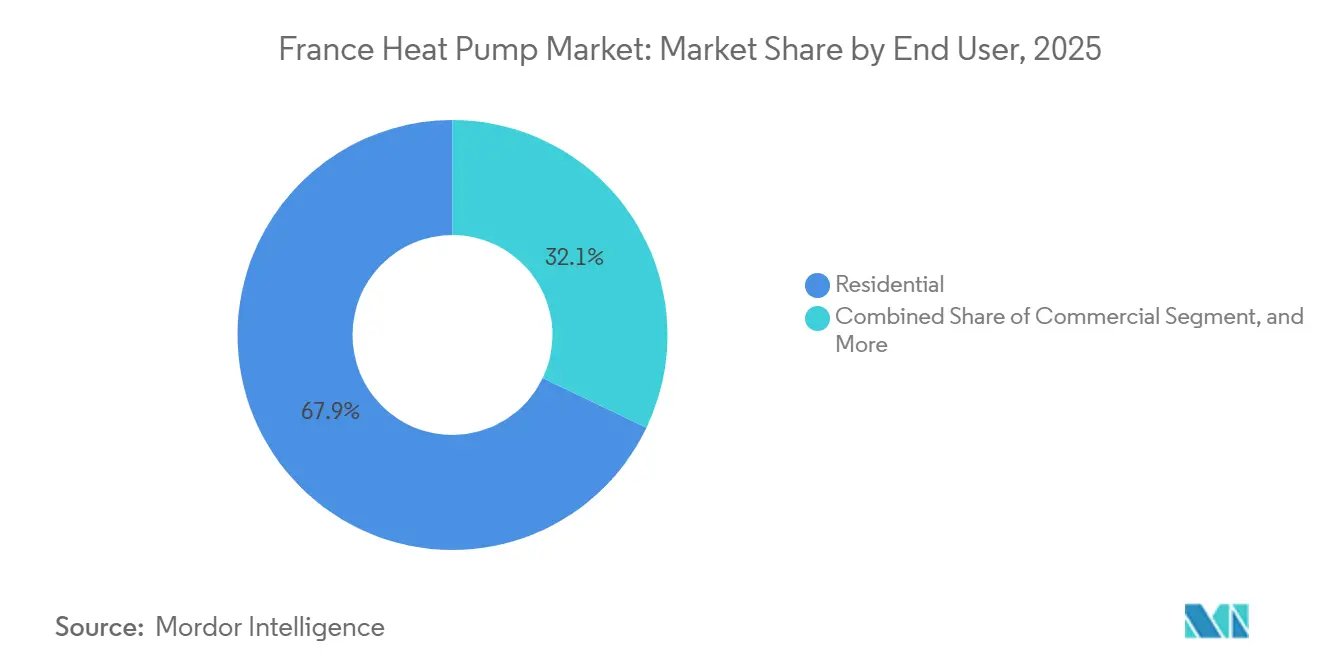

- By end user, residential customers contributed 67.91% of 2025 value, whereas commercial deployments are growing at 5.26% CAGR.

- By installation, retrofit projects held 63.12% of 2025 activity and new-construction installations are forecast to grow at 5.43% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Heat Pump Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| MaPrimeRénov’ Subsidies Expand Addressable Market | +1.2% | National, led by Île-de-France, Auvergne-Rhône-Alpes, Occitanie | Short term (≤ 2 years) |

| RE2020 Building Energy Code Mandates Low-Carbon Heating | +1.0% | National, strongest around Lyon, Toulouse, Nantes | Medium term (2-4 years) |

| Heat-as-a-Service Models Lower Up-Front Costs | +0.8% | Paris metro and Provence-Alpes-Côte d’Azur | Medium term (2-4 years) |

| Smart-Grid Demand Response Revenues Improve ROI | +0.6% | Brittany and Grand Est pilot zones | Long term (≥ 4 years) |

| Cold-Climate R290 Units Boost Seasonal Performance | +0.5% | Northern regions of Hauts-de-France and Grand Est | Medium term (2-4 years) |

| Industrial Waste-Heat Recovery via High-Temp HPs | +0.4% | Auvergne-Rhône-Alpes, Grand Est, Hauts-de-France clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

MaPrimeRénov’ Subsidies Expand Addressable Market

Premium-tier rebates now require European factory origin, steering roughly EUR 2 billion (USD 2.24 billion) of annual funding toward local brands.[1]Ministère de la Transition Écologique, “MaPrimeRénov’ Subsidy Program,” ecologie.gouv.fr Payback periods for rural air-to-water retrofits fall from eight to five years for low-income households. The raised EUR 5,000 (USD 5,600) cap on geothermal systems narrows the cost gap with air-source equipment, supporting an 18% unit-sales bump in 2026. Market share vacated by Asian importers, previously 25% in the sub-10 kW tier, creates immediate runway for Atlantic and Bosch. Verification through the EHPA database adds three-week approval lags but improves supply-chain transparency.[2]European Heat Pump Association, “Product Database and Compliance Verification,” ehpa.org

RE2020 Building Energy Code Mandates Low-Carbon Heating

The 4 kg CO₂e m⁻²-year ceiling makes gas boilers non-compliant, prompting 86% of single-family completions in 2023 to choose heat pumps.[3]Observatoire BBC, “Chiffres Clés 2023 de la Construction Neuve,” observatoirebbc.org Developers accept EUR 8,000-12,000 (USD 8,960-13,440) extra envelope cost to avoid lifetime carbon penalties that can exceed EUR 40,000 (USD 44,800). Pairing rooftop photovoltaics with heat pumps cuts primary-energy factors by up to 40%, freeing carbon budget for other systems and tilting specification toward reversible units in the south.

Heat-as-a-Service Models Lower Up-Front Costs

Contracts from Dalkia and Engie bundle equipment, installation, and maintenance into EUR 80-120 (USD 90-134) monthly fees, eliminating the EUR 12,000-18,000 (USD 13,440-20,160) lump-sum barrier.[4]Dalkia, “Heat-as-a-Service Contracts,” dalkia.fr Early pilots show 22% higher adoption among renters and low-income owners. Providers capture MaPrimeRénov’ funds directly, while renters pay only for thermal output. Secondary-market complications arise when a property is sold because the asset remains with the service firm, yet demand-response revenue and avoided debt provide measurable gains.

Smart-Grid Demand Response Revenues Improve ROI

RTE and Enedis pilots compensate households EUR 0.15-0.25 (USD 0.17-0.28) per curtailed kWh during winter peaks.[5]RTE, “Demand Response Programs,” rte-france.com Smart controllers cut compressor load 30-50% without comfort loss, generating EUR 150-250 (USD 168-280) per home annually and trimming simple payback by as much as 12 months. Rural coverage gaps in three-phase meters limit early participation, yet regulators weigh a 2027 mandate for built-in demand-response interfaces.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Refrigerant Phase-Down Drives Costly Redesigns | -0.7% | National, supply bottlenecks in Île-de-France and Auvergne-Rhône-Alpes | Short term (≤ 2 years) |

| Shortage of Certified Installers Limits Deployments | -0.5% | Rural départements of Creuse, Lozère, Cantal | Medium term (2-4 years) |

| Grid Congestion Fees in Rural Areas Raise Opex | -0.3% | Brittany, Occitanie, Nouvelle-Aquitaine | Medium term (2-4 years) |

| Used-Equipment Grey Market Undercuts OEM Margins | -0.2% | National, online marketplaces and southern borders | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Refrigerant Regulations Accelerate Technology Transition

EU Regulation 2024/573 reduces HFC quotas 79% by 2030, forcing a pivot to flammable R290 or R454B blends.[6]European Commission, “EU Legislation to Control F-gases,” climate.ec.europa.eu R290’s higher pressure demands thicker tubing and new compressor housings, adding EUR 300-500 (USD 336-560) per unit. Mitsubishi Electric’s Ecodan 2026 range illustrates the trade-off: 15% higher efficiency at -7 °C but indoor placement limited to rooms above 20 m².

Shortage of Certified Installers Limits Deployments

QualiPAC certification throughput met only 12,000 technicians in 2025 versus 30,000 additional installers needed by 2027.[7]Qualit’EnR, “QualiPAC Certification Program,” qualit-enr.org Limited training-center capacity and wage competition from solar and EV-charger sectors extend waiting lists: average retrofit lead time climbed to 14 weeks in late 2025, with some rural households waiting six months. Elevated day rates, EUR 550 (USD 616) in 2025, erode the operating-cost advantage over gas in regions with dense pipeline networks.

Segment Analysis

By Source Type: Air Source Dominates, Ground Source Gains Industrial Traction

Air-source configurations led the France heat pump market with 74.78% revenue share in 2025. Favorable capex of EUR 8,000-12,000 (USD 8,960-13,440) installed keeps air units attractive for retrofit scenarios where existing radiators match 40 °C-55 °C water supply. Ground-source projects commanded a smaller base but show 5.31% annual growth potential thanks to industrial waste-heat integration and drilling-cost declines. Water-source units remain niche, bound by Water Framework permitting complexity, while hybrid gas-plus-heat-pump systems appeal to households reluctant to decommission boilers despite carbon penalties.

Granite geology, shallow aquifers, and supportive subsidies make Brittany the national stronghold for ground-source, lowering borehole expenditures 20-30% relative to northern sedimentary zones. Industrial actors in Auvergne-Rhône-Alpes deploy brine-to-water loops achieving seasonal performance factors above 4.5 when ambient air-source rivals stall at 3.2, validating the economic thesis for deeper geothermal adoption.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Air-to-Water Leads, Ground-to-Water Fastest Growing

Air-to-water systems controlled 65.86% of 2025 sales, underscoring their fit with legacy hydronic circuits and RE2020 compliant supply temperatures. Geothermal ground-to-water solutions, although smaller, are the fastest expanding at 5.14% CAGR as drilling prices fall to EUR 48 (USD 54) per meter and RE2020’s primary-energy factor of 0.6 rewards ultra-low-carbon heat. Air-to-air units, accounting for 28% of revenue, meet rising cooling loads in the south but lose out on premium MaPrimeRénov’ subsidies, curbing retrofit momentum. Water-to-water remains confined to select lakeside or district-heating pilots.

Viessmann’s Vitocal 350-G, unveiled January 2026, puts a R290 inverter compressor in geothermal service, posting a 5.2 COP at 0 °C brine inlet, 35% better than air-equivalent units. Bosch counters with the Compress 7800i LW, an air-to-water platform embedding a 300-liter tank and native demand-response interface, signaling competition on both efficiency and grid service.

By Capacity: Sub-10 kW Dominates Residential, 50-200 kW Band Accelerates

Sub-10 kW models supplied 42.03% of 2025 sales, mirroring the 6-8 kW design loads typical of 120 m² single-family homes and underpinning the baseline France heat pump market size for residential retrofits. The 50-200 kW segment, serving multifamily blocks and small commerce, is forecast to expand 5.34% per year as unit capex drops to EUR 800 (USD 896) per kW and condominium boards replace aging gas boilers.

Installations rated 10-50 kW bridge large dwellings and small retail, holding 35% revenue share in 2025, while above-200 kW machines remain specialized because integration with steam or high-temperature loops raises complexity. Atlantic’s AI-driven defrost logic trims auxiliary heat 25%, solidifying sub-20 kW leadership, whereas Daikin’s 70 °C high-temperature platform simplifies direct oil-boiler swaps, accelerating upgrades in rural estates.

Note: Segment shares of all individual segments available upon report purchase

By Application: Space Heating Leads, Cooling Demand Rises in South

Space heating captured 62.74% of 2025 revenue, anchored by 2,500-3,000 heating degree-days in northern départements, and remains the core service driving the France heat pump market. Space cooling demand is projected to grow 5.27% annually through 2031 as Mediterranean regions log rising summer peaks and developers specify reversible units to satisfy both loads. Domestic hot-water heaters took 18% share, giving homeowners a phased approach to electrification, while industrial process heating at 90-120 °C, although only 6% of value, posts quick paybacks in food and chemical plants.

Smart-grid incentives allow reversible units to curtail load for cash during peak winter evenings, shaving payback by up to a year and tightening the linkage between application mix and return on investment. Integrated hot-water cylinders, like those in Mitsubishi Electric’s Ecodan QUHZ, cut resistance-element use and lift household savings, reinforcing the multi-service value proposition across climate zones.

By End User: Residential Dominates, Commercial Adoption Accelerates

Residential customers supplied 67.91% of 2025 value, reflecting a retrofit pool of 19 million gas-heated dwellings and policy aims to convert 3 million units by 2030. Commercial uptake is advancing at a 5.26% CAGR as office parks, retail centers, and hotels sign heat-as-a-service agreements that roll equipment, maintenance, and energy into predictable operating leases. Industrial facilities contribute 9% of revenue and are concentrating new investment in high-temperature units that recycle refrigeration waste heat.

Energy-service firms collect MaPrimeRénov’ incentives directly, lowering household friction and enlarging the France heat pump market, while commercial landlords capture demand-response revenue worth 8-12% of annual electricity cost. Industrial operators in Auvergne-Rhône-Alpes and Grand Est reach seasonal performance factors above 4.0, translating natural-gas avoidance into three-to-five-year paybacks that now satisfy corporate decarbonization mandates.

Note: Segment shares of all individual segments available upon report purchase

By Installation: Retrofit Leads, New Construction Grows Faster

Retrofit work represented 63.12% of 2025 activity and anchors near-term France heat pump market size, despite four-to-six-week project durations driven by hydraulic balancing and panel upgrades. MaPrimeRénov’ cuts retrofit capex EUR 4,000-5,000 (USD 4,480-5,600) and keeps paybacks attractive even with rising installer day rates.

New-construction deployments, forecast to grow 5.43% yearly, benefit from RE2020’s de-facto boiler ban and six-week geothermal permits in compliant municipalities. Developers bundle rooftop photovoltaics and pre-plumbed heat-pump modules, reducing primary energy by 40% and allocating their carbon budget toward larger window areas. Atlantic’s upcoming Saône-et-Loire plant will ship factory-configured hydraulic kits that shave on-site labor 30%, supporting faster throughput in both new-build and retrofit channels of the France heat pump market.

Geography Analysis

Auvergne-Rhône-Alpes accounted for more than 18% of national installations in 2025, helped by a dense cluster of manufacturers within 200 kilometers of Lyon that shortens supply lines and keeps lead times below the national average. Brittany led ground-source adoption, capturing 29% of those projects as granite bedrock and shallow water tables trim drilling costs by up to 30% relative to northern sedimentary basins. Provence-Alpes-Côte d’Azur and Occitanie favor reversible air-to-air units because cooling degree-days rose to roughly 20 in 2025, yet the absence of premium MaPrimeRénov’ rebates for non-hydronic systems slows retrofit penetration even as temperatures climb. Île-de-France, home to 18% of the housing stock, lags on per-capita uptake since condominium boards must approve boiler replacements and central metering splits incentives between owners and tenants.

Northern départements such as Hauts-de-France and Grand Est record 2,500-3,000 heating degree-days annually and therefore rely on air-to-water equipment that mates easily with radiator networks, yet rural grid congestion triggers locational tariffs under TURPE 7 that add as much as EUR 500 (USD 560) to three-phase connections, increasing capital outlay for geothermal projects. Overseas territories including Réunion and Martinique install air-to-air heat pumps at rates 40% above mainland France, but freight premiums inflate delivered prices by 25-35%, undermining lifetime savings relative to electric-resistance heaters. Regional installer density deepens the divide: rural Creuse and Lozère host fewer than two QualiPAC-certified technicians per 10,000 households, compared with eight in Île-de-France, meaning the France heat pump market expands fastest where labor is already plentiful.

The Programmation Pluriannuelle de l’Énergie 3 target of three million additional units by 2030 implies a 6.2% annual rise from the 2025 installed base of 5.8 million, yet that objective risks clustering around peri-urban belts if training backlogs persist. Municipalities that streamline geothermal permitting to six weeks attract new-build developers bundling rooftop photovoltaics with low-carbon heating, while towns that keep twelve-week approval windows cede demand to air-source retrofits. As climate zones, subsidy rules, and grid capacity vary widely, regional policy coordination remains critical for balanced growth across the overall France heat pump market.

Competitive Landscape

The France heat pump market remains fragmented because no brand exceeds 15% share, but merger activity is narrowing the field and elevating scale economies. Bosch Thermotechnology’s EUR 7 billion purchase of Johnson Controls’ light-commercial HVAC assets in September 2024 merged two top-ten suppliers and produced the R290-based Compress 3800i AW platform that debuted in the second quarter of 2026. Atlantic allocates EUR 140-150 million (USD 157-168 million) to a Saône-et-Loire plant that will triple its air-to-water output by 2027, securing preferential MaPrimeRénov’ treatment tied to European manufacturing thresholds. Mitsubishi Electric, Daikin, and Viessmann race to certify R290 lines that satisfy EU Regulation 2024/573, each balancing higher material costs against marketing gains from ultra-low-GWP credentials.

Strategic differentiation now revolves around grid connectivity, financing creativity, and localized assembly. Voltalis distributes no-cost smart controllers that modulate compressor cycles for demand-response revenue worth EUR 150-250 (USD 168-280) per household each year, cutting simple payback by up to twelve months and raising customer stickiness. Engie Solutions and Dalkia compete with heat-as-a-service contracts that convert EUR 12,000-18,000 (USD 13,440-20,160) of capital expense into EUR 80-120 (USD 90-134) monthly fees, freeing household cash and enlarging the addressable base for the France heat pump market. Manufacturers court these service firms by offering extended warranties and remote-diagnostics APIs that minimize truck rolls and bolster uptime guarantees.

Emerging white-space centers on high-temperature industrial pumps and megawatt-scale river-water systems for district heating, yet expertise gaps and Water Framework permitting hurdles restrict annual deployments to fewer than 200 large units. Smaller challengers such as Stiebel Eltron outflank incumbents on speed by importing finished R290 units that immediately satisfy EU-origin rules, although freight and currency volatility compress margins. Overall, rising consolidation, factory localization, and service-based revenue models suggest a gradual shift from a highly fragmented arena toward a moderately concentrated structure, positioning the top five suppliers to capture a growing slice of the expanding France heat pump market.

France Heat Pump Industry Leaders

-

Trane Inc. (Trane Technologies Plc)

-

LG Electronics

-

Daikin Industries Ltd.

-

Johnson Controls International Plc

-

Carrier Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mitsubishi Electric rolled out its Ecodan 2026 R290 range, reporting 15% better seasonal performance at –7 °C compared with R410A predecessors.

- March 2026: Mitsubishi Electric and Aldes agreed to bundle heat pumps with mechanical ventilation, raising whole-home efficiency 12% in RE2020 builds.

- February 2026: Mitsubishi Electric partnered with Evhacs to twin heat pumps and EV chargers, leveraging vehicle batteries for thermal storage and cutting peak power bills 18%.

- January 2026: The government limited MaPrimeRénov’ premium rebates to EU-manufactured heat pumps, reallocating EUR 2 billion (USD 2.24 billion) of subsidies toward domestic suppliers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the French heat-pump market as all factory-built air, water, and ground-source units (residential, commercial, and light-industrial) sold inside mainland France for space-conditioning or domestic hot-water applications.

Exclusions include portable spot coolers, chillers above 1 MW, and second-hand imports, which are outside the scope.

Segmentation Overview

-

By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

-

By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

-

By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

-

By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

-

By End User

- Residential

- Commercial

- Industrial

-

By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed French heat-pump assemblers, wholesaler associations, certified installers across Ile-de-France, Occitanie, and Auvergne-Rhone-Alpes, plus energy-policy advisors. These conversations validated channel mark-ups, installer capacity constraints, and likely uptake of RE2020 building codes, helping us refine penetration curves and price trajectories.

Desk Research

We began by mapping the regulatory and demand context through open datasets from ADEME, INSEE energy-price statistics, Eurostat trade code 8418, the EU F-Gas registry, and the European Heat Pump Association's annual sales panel, which together anchor historical shipments and policy milestones. Company filings, installer price lists, and reputable press were reviewed to benchmark average selling prices (ASPs). Paid resources such as D&B Hoovers for OEM financials and Volza for shipment-level import data filled corporate and channel gaps. This list is illustrative; many additional sources informed the evidence base.

Our desk review also extracted 2024-2025 revenue estimates published by external consultancies for later variance checks, while patent trends from Questel hinted at refrigerant migration patterns that feed technology adoption assumptions.

Market-Sizing & Forecasting

A top-down model starts with EHPA-reported unit sales, adjusts for re-exports, and multiplies by respondent-validated ASP bands to construct the value. Bottom-up cross-checks roll up revenues of leading suppliers captured in Hoovers and distributor audits, with gaps bridged by sampled ASP x volume estimates for long-tail brands. Key drivers include housing completions, MaPrimeRenov subsidy outlays, retail electricity-to-gas price ratio, installer workforce growth, and refrigerant phase-down milestones; these feed a multivariate regression that projects demand through the forecast period. Scenario analysis addresses subsidy-funding swings and grid-capacity constraints.

Data Validation & Update Cycle

Triangulation of model outputs against customs values, inverter-compressor import trends, and energy-efficiency certificate issuances flags anomalies. Senior reviewers sign off after variance thresholds (<5 %) are met. The dataset refreshes annually, with interim updates triggered by policy changes or >10 % sales shocks; clients always receive the latest pass.

Why Mordor's France Heat Pump Baseline Commands Reliability

Published estimates often diverge because firms pick different product mixes, price bases, and forecast cadences.

Key gap drivers include some studies that bundle air-conditioner-only systems, others that assume aggressive subsidy continuity, and several that inflate revenue by using retail rather than ex-factory prices. Mordor discloses its scope, refreshes yearly, and blends policy, price, and capacity signals vetted with on-ground experts, producing a balanced midpoint.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.74 B (2025) | Mordor Intelligence | - |

| USD 3.36 B (2024) | Global Consultancy A | Includes AC-only heat-pump hybrids and applies retail ASPs |

| USD 18.50 B (2024) | Regional Consultancy B | Treats air-source units over multiple MW plus service revenue as market value |

| 546 k units (2024) | Industry Association C | Reports units only, no value conversion or commercial/industrial split |

In sum, our disciplined scope choices, dual-track modeling, and yearly refresh provide decision-makers with a transparent, dependable baseline that remains traceable to measurable French demand signals.

Key Questions Answered in the Report

How large is the France heat pump market in 2026?

The France heat pump market size stands at USD 1.83 billion in 2026 and is on track to reach USD 2.32 billion by 2031.

What CAGR is expected for French heat pump sales between 2026 and 2031?

Market revenue is projected to rise at a 4.86% CAGR during the 2026-2031 period.

Which heat pump type leads sales today?

Air-source configurations dominate, accounting for 74.78% of 2025 revenue.

Why are ground-source systems gaining traction?

Industrial waste-heat recovery and lower drilling expenses underpin a 5.31% annual growth outlook for ground-source units.

How do French subsidies influence purchase decisions?

MaPrimeRénov' rebates cut payback periods from eight to five years and now favor EU-built equipment, boosting domestic production.

What is the biggest operational hurdle to faster deployment?

A shortage of QualiPAC-certified installers lengthens installation queues to 14 weeks on average and inflates labor costs.