Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

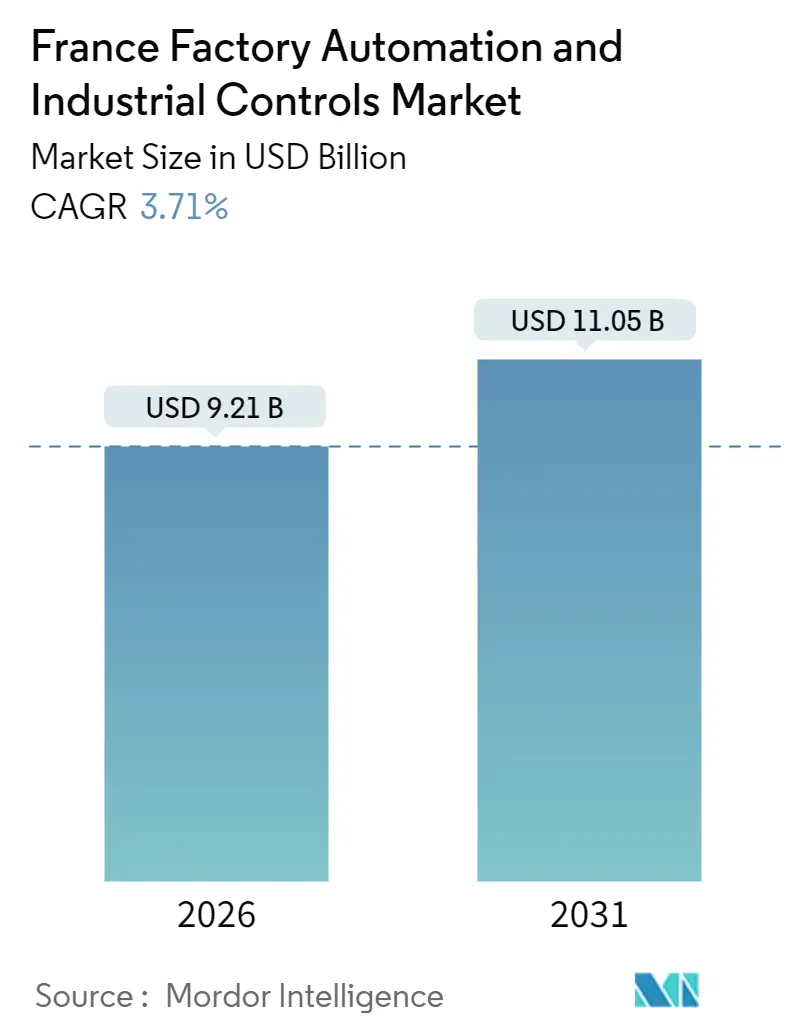

| Market Size (2026) | USD 9.21 Billion |

| Market Size (2031) | USD 11.05 Billion |

| Growth Rate (2026 - 2031) | 3.71% CAGR |

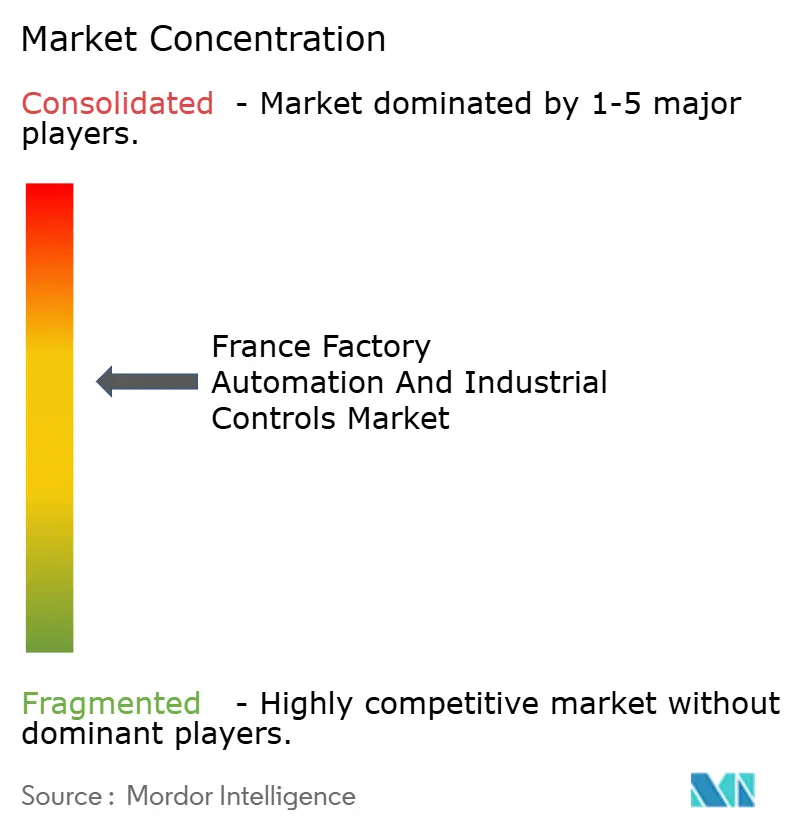

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Factory Automation And Industrial Controls Market Analysis by Mordor Intelligence

The France factory automation and industrial controls market size is valued at USD 9.21 billion in 2026 and is projected to reach USD 11.05 billion by 2031, advancing at a 3.71% CAGR. This expansion stems from a pivot toward sovereign-AI controllers, hydrogen-electrolyzer gigafactories that need sub-millisecond response times, and circular-economy traceability mandates that older systems cannot fulfil. Embedded AI edge controllers, 5G-ready distributed control architectures, and blockchain-enabled manufacturing-execution platforms are now central to capital-expenditure plans as firms chase regulatory compliance and energy-efficiency gains. Competitive focus is shifting from hardware to software-as-a-service offerings, while regional funding programs and tax credits shorten investment payback in small and mid-sized enterprises. At the same time, system integrator capacity constraints outside major industrial hubs drive interest in online industrial marketplaces that offer standardized plug-and-play modules, virtual commissioning, and remote support.

Key Report Takeaways

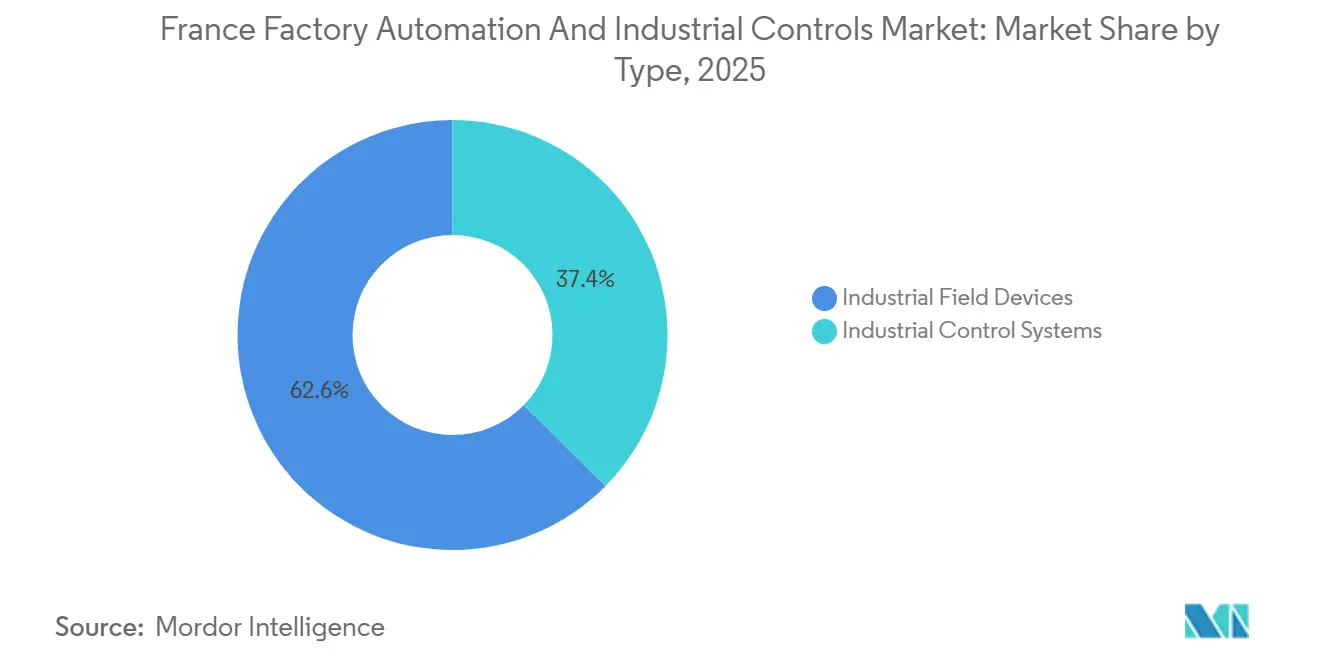

- By type, Industrial Control Systems led with 37.40% of the France factory automation and industrial controls market share in 2025; Industrial Robotics is forecast to grow at a 4.36% CAGR through 2031.

- By component, Hardware accounted for 46.20% of the France factory automation and industrial controls market size in 2025, while Software is advancing at a 4.38% CAGR to 2031.

- By end-user industry, Automotive and Transportation captured 28.50% share of the France factory automation and industrial controls market size in 2025, yet Food and Beverage is projected to expand at a 4.22% CAGR through 2031.

- By deployment mode, On-premises systems held 62.00% revenue share in 2025; cloud-based architectures are recording the highest expected CAGR at 4.7% to 2031.

- By sales channel, System Integrators controlled 41.30% revenue in 2025, while Online Industrial Marketplaces are set to rise at an 4.26% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Factory Automation And Industrial Controls Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Industry 4.0 Adoption Across Automotive and Aerospace | +2.10% | Île-de-France, Grand Est, Auvergne-Rhône-Alpes, Occitanie (Toulouse aerospace cluster) | Medium term (2-4 years) |

| Government Incentives for Energy-Efficient Upgrades in SMEs | +1.80% | National, with concentration in Hauts-de-France and Nouvelle-Aquitaine SME clusters | Short term (≤ 2 years) |

| Rising Labor Cost and Skill Shortages in Manufacturing | +2.30% | National, acute in Île-de-France and Auvergne-Rhône-Alpes high-wage zones | Short term (≤ 2 years) |

| Expansion of Renewable-Hydrogen Projects Requiring Advanced Controls | +1.50% | Normandy (Normand'Hy), Auvergne-Rhône-Alpes (Genvia gigafactory), Grand Est | Long term (≥ 4 years) |

| National AI Strategy Driving Intelligent Edge Control Systems | +1.40% | National, with early adoption in Île-de-France tech corridors and Lyon AI labs | Medium term (2-4 years) |

| Circular Economy Compliance Creating Need for Traceability Automation | +1.20% | National, with early gains in automotive (Grand Est), food and beverage (Brittany, Pays de la Loire) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Industry 4.0 Adoption in Automotive and Aerospace

Automotive and aerospace producers are embedding real-time analytics, collaborative robots, and augmented-reality work instructions to compress cycle times and reduce defects, an approach demonstrated by Airbus at its Toulouse A321 final assembly line.[1]Airbus, “A321 Final Assembly Line Digitalization,” airbus.com Predictive-maintenance platforms deployed by Renault across 22 plants save EUR 80 million (USD 90 million) annually and validate digital twins in brownfield settings. Electric-vehicle platforms require precision torque control and thermal monitoring that legacy programmable-logic controllers cannot natively support, spurring demand for modular PLCs with high-speed vision add-ons.[2]International Federation of Robotics, “World Robotics 2025,” ifr.org Although industrial-robot installations fell 24% to 4,900 units in 2024, renewed capital spending in 2026 is reviving backlogs. Regulatory frameworks such as ISO 9001 now insist on digital audit trails, anchoring the migration toward integrated manufacturing-execution software.

Rising Labor Cost and Skill Shortages in Manufacturing

Eighty-one percent of French manufacturers faced hiring difficulties in 2024, with wage levels above EUR 25 (USD 28) per hour in key regions and a looming retirement wave that removes experienced technicians.[3]Banque de France, “Manufacturing Hiring Difficulties 2024,” banque-france.fr The cost crossover that makes collaborative robots less expensive than manual labour over five years has already arrived in Île-de-France, accelerating robot uptake. Companies are digitizing tacit knowledge through AI-assisted troubleshooting before skilled workers exit, particularly in aerospace and defense clusters. Productivity growth slowed to 0.8% a year between 2019 and 2025, intensifying pressure to automate repetitive, hazardous, or precision tasks. ISO 45001 occupational-health standards further incentivize automated handling of chemicals and high-temperature welding to reduce employer liability.

Government Incentives for Energy-Efficient Upgrades in SMEs

France Relance allocated EUR 345 million (USD 388 million) to subsidize up to 40% of SME automation costs, directly narrowing payback periods. The Green Industry Tax Credit (C3IV) allows a 20% offset on purchases of variable-frequency drives and smart sensors, lifting demand for retrofits in food processing and chemicals. A EUR 4 billion (USD 4.5 billion) decarbonization grant pool promotes IoT-based upgrades of furnaces and compressors that lower energy use. R&D tax credits reimburse up to 30% of automation-related research, enabling small integrators to co-develop custom control algorithms. Hauts-de-France and Nouvelle-Aquitaine regions enhance these incentives with local matching funds, creating vibrant SME automation clusters.

Expansion of Renewable-Hydrogen Projects Requiring Advanced Controls

Air Liquide’s Normand'Hy 200-megawatt electrolyzer demands sub-second voltage regulation and 99.999% hydrogen-purity monitoring that legacy SCADA cannot achieve without middleware. Genvia’s solid-oxide electrolyzer gigafactory integrates more than 5,000 sensors per line, driving sales of high-density input-output modules and edge gateways. The AdvancedH2Valley program coordinates production, storage, and distribution across multiple sites through OPC UA and MQTT protocols, highlighting interoperability as a purchase criterion. Hydrogen’s emerging role in decarbonizing steel and ammonia plants propels distributed control upgrades in Grand Est and Hauts-de-France. ATEX and EN 17124 safety standards require automated leak detection and emergency shutdown functions, reinforcing demand for next-generation controllers.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Expenditure for Full-Scale Automation | -1.40% | National, acute in SME-heavy regions (Hauts-de-France, Nouvelle-Aquitaine) | Short term (≤ 2 years) |

| Integration Complexity with Legacy Brownfield Facilities | -1.10% | Grand Est, Île-de-France (older automotive and aerospace plants) | Medium term (2-4 years) |

| Cybersecurity Concerns Around IT/OT Convergence in Mid-Cap Firms | -0.70% | National, concentrated in mid-cap manufacturers lacking in-house IT security teams | Short term (≤ 2 years) |

| Limited Availability of Certified System Integrators Outside Industrial Hubs | -0.60% | Normandy, Brittany, Centre-Val de Loire (secondary manufacturing regions) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Expenditure for Full-Scale Automation

Even after subsidies, a comprehensive Industry 4.0 retrofit can cost EUR 500,000 – 2 million (USD 563,000 – 2.25 million) for a mid-size plant, exceeding annual capital budgets for 60% of French SMEs. Thin-margin sectors like food processing often defer investments despite labour shortages. European Central Bank rate hikes have raised borrowing costs, making lease-to-own and automation-as-a-service models attractive yet still limited to large suppliers. Many small firms still view automation as an all-or-nothing commitment, overlooking phased retrofits such as IoT modules on existing PLCs. ISO 9001 and ISO 14001 audits nonetheless increasingly favour automated data capture, pushing reluctant firms toward gradual adoption.

Integration Complexity with Legacy Brownfield Facilities

Plants built in the 1980s and 1990s rely on Profibus, DeviceNet, and Modbus RTU protocols that require costly converters to interoperate with Ethernet/IP and OPC UA networks. Legacy human-machine interfaces running obsolete operating systems create cybersecurity exposures if networked yet replacing them disrupts production and voids equipment warranties. Fewer than 20% of system integrators possess both legacy OT and modern IT skills, forcing multi-vendor projects that inflate timelines by 30-50%. Renault needed 18 months to connect 7,500 brownfield assets, illustrating time burdens even for resource-rich OEMs. Brownfield sites must also add secure data-logging modules to satisfy CE-marking and GDPR documentation requirements, raising retrofit costs.

Segment Analysis

By Type: Field Devices Reclaim Momentum as Robotics and Vision Accelerate

Industrial Control Systems commanded 37.40% of the France factory automation and industrial controls market share in 2025, a position anchored in distributed control architectures across chemicals and programmable controllers in automotive plants. Field Devices, however, are growing faster, with Industrial Robotics slated for a 4.36% CAGR through 2031 despite a 24% installation dip in 2024. Machine-vision sales are rising 18% annually in food and beverage lines that must meet AGEC traceability rules. Motors and drives benefit from C3IV tax credits, enabling 15-20% electricity savings in cement kilns.

Sensors, especially wireless LoRaWAN variants, facilitate brownfield retrofits where cabling is prohibitive, though encryption gaps remain a hurdle in critical infrastructure. Safety systems tied to ISO 13849 regulations track robot adoption with a lag of about nine months. Supervisory systems are shifting to cloud hosting, cutting on-premises server spend by 30% following AVEVA’s 2025 AWS validation. Human-machine interfaces increasingly use tablet-based augmented-reality overlays that shorten operator training cycles.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Component: Software Surges on Digital-Twin Adoption

Hardware retained 46.20% of the France factory automation and industrial controls market size in 2025, yet the fastest expansion is in Software at a 4.38% CAGR. Renault’s industrial metaverse exemplifies the shift, ingesting more than 3 billion data points daily from 15,000 assets and delivering EUR 700 million (USD 788 million) cumulative savings. Cloud-native MES platforms lower total cost of ownership by 30% against on-premises alternatives, spurring conversions, while open-source frameworks such as Eclipse 4diac commoditize base control logic.

Services evolve toward outcome-based contracts that guarantee uptime, aligning vendor incentives with manufacturer operating goals. Still, services growth is curbed in regions lacking certified integrators, a gap that marketplaces like EcoSpare address through standardized installation guides. Hardware demand remains resilient in hydrogen and battery gigafactories that require ruggedized gateways and redundant power supplies.

By End-User Industry: Traceability Push Lifts Food and Beverage

Automotive and Transportation accounted for 28.50% of the France factory automation and industrial controls market size in 2025, led by electric-vehicle investments. Yet Food and Beverage is set to post the highest 4.22% CAGR through 2031, propelled by EUR 2.3 billion (USD 2.6 billion) France 2030 funding and blockchain-based traceability mandates. Pharmaceutical producers accelerate continuous-manufacturing lines to meet EMA guidelines that condense batch release times.

Oil and Gas refiners invest in advanced process control to squeeze margins amid emissions caps, while chemicals retrofit SCADA for IEC 62443 cybersecurity compliance. Power utilities, especially renewable-hydrogen plants, migrate to distributed control systems that support sub-second latency. Metals and pulp sectors adopt predictive-maintenance modules where the return materializes within 18 months.

By Deployment Mode: Cloud Adoption Gains Certified Momentum

On-premises architectures still command 62.00% revenue share in 2025, reflecting air-gapped security preferences and motion-control latency needs. Cloud-based options are expected to log a 4.7% CAGR, buoyed by EUR 667 million (USD 750 million) sovereign-cloud funding and SecNumCloud certifications that satisfy GDPR data-sovereignty rules. Hybrid deployments bridge real-time control on site with analytics off site, an approach encouraged by the PEPR Cloud research program.

Subscription software replaces perpetual licenses, lowering upfront costs and smoothing cash outflows. Cloud growth is tempered by skill shortages in configuring virtual private clouds, which managed-service integrators aim to relieve. Seveso-classified chemical facilities and defense contractors still mandate on-premises or hybrid models to maintain air-gapped safety layers.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Sales Channel: Marketplaces Close Regional Service Gaps

System Integrators delivered 41.30% of revenue in 2025 and remain indispensable for complex retrofits that blend multiple vendors and demand regulatory documentation. Online Industrial Marketplaces, however, are forecast to rise at an 4.26% CAGR by offering self-install kits and remote support that bypass integrator bottlenecks in regions such as Normandy and Brittany. Direct sales persist among large OEMs with established framework agreements, while distributors face margin pressure as vendors build their own e-commerce portals.

Marketplace value propositions include 20-40% cost savings through refurbished equipment and reduced lead times for standardized modules. Virtual-commissioning software further reduces reliance on on-site technicians, letting in-house maintenance teams execute smaller projects. Integrators still dominate high-complexity work, such as multi-plant digital-twin rollouts at Renault and Airbus.

Geography Analysis

Île-de-France, Auvergne-Rhône-Alpes, Grand Est, and Hauts-de-France together contributed over 65% of 2025 installations, driven by automotive OEMs, aerospace clusters, and diversified manufacturing bases. Île-de-France hosts 81 AI labs, and more than 1,000 AI startups that collaborate on predictive-maintenance algorithms, giving local factories early access to embedded AI controllers. Auvergne-Rhône-Alpes attracts next-generation control-system suppliers through its Grenoble semiconductor ecosystem and Genvia’s electrolyzer gigafactory that needs sub-second latency across 5,000 sensors per line.

Grand Est saw a 24% decline in automotive robot installations to roughly 1,600 units in 2024, yet deferred EV projects are now reviving orders along a 10.80% CAGR trajectory. Hauts-de-France benefits disproportionately from SME-focused subsidies that lower automation payback thresholds in agri-food and chemicals factories. Occitanie’s aerospace corridor, anchored by Airbus’s Toulouse operations, pioneers collaborative-robot applications and augmented-reality guidance systems.

Normandy positions itself as a hydrogen hub through Air Liquide’s Normand'Hy project, which spurs demand for ATEX-compliant distributed controls. Brittany and Pays de la Loire accelerate traceability investments under AGEC law, adopting RFID gateways and blockchain MES modules for serialized product IDs. Secondary regions such as Centre-Val de Loire and Nouvelle-Aquitaine rely on online marketplaces for plug-and-play automation due to limited integrator capacity. The 2025 UK-France Industrial Strategy Partnership injects GBP 1 billion (USD 1.27 billion) into AI-driven robotics, boosting R&D nodes in Paris and Toulouse.

Competitive Landscape

The top five suppliers Schneider Electric, Siemens, ABB, Rockwell Automation, and Honeywell collectively hold an estimated 45-50% share, marking a moderately concentrated but competitive environment. Schneider Electric’s 2025 release of EcoStruxure Industrial Advisor and its 5G pilot with Orange illustrate a pivot toward software-as-a-service recurring revenue and ultra-low-latency wireless connectivity. Hardware-centric rivals face margin compression as control algorithms migrate to edge-compute modules. Outcome-based contracts that guarantee uptime remain an untapped opportunity, adopted by fewer than 10% of integrators.

Hydrogen-electrolyzer gigafactories create white-space demand for control systems that respond to voltage fluctuations within milliseconds, an area where traditional SCADA is inadequate. Circular-economy traceability mandates open niches for vision, RFID, and blockchain MES specialists. Online marketplaces such as EcoSpare reduce procurement cost by as much as 40%, challenging distributor margins.

Renault’s industrial metaverse processes 3 billion data points daily and has saved USD 788 million since 2019, shifting procurement criteria toward holistic simulation and predictive-maintenance platforms. Thales’s GBP 40 million AI R&D investment under the 2025 UK-France partnership underscores rising cross-border collaboration standards. IEC 62443 cybersecurity compliance and NIS2 incident-reporting mandates advantage suppliers with mature security portfolios.

France Factory Automation And Industrial Controls Industry Leaders

Schneider Electric SE

Rockwell Automation Inc.

Honeywell International Inc.

Emerson Electric Company

ABB Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: AVEVA validated its SCADA and MES suites on Amazon Web Services, cutting on-premises costs by 30% and enabling cloud monitoring.

- July 2025: The United Kingdom and France launched a GBP 1 billion (USD 1.27 billion) Industrial Strategy Partnership; Thales committed GBP 40 million to AI R&D for autonomous robotics.

- April 2025: Schneider Electric released EcoStruxure Industrial Advisor, pivoting toward software subscriptions and data-driven services.

France Factory Automation And Industrial Controls Market Report Scope

The study characterizes the market based on the type of products such as DCS, PLC, SCADA, and robotics among others, and by End-user industries that include Oil and Gas, Food and Beverage, Power and Utilities, Chemical and Petrochemical, Automotive, and Transportation, Pharmaceutical and among others. The scope of the study for factory automation and industrial control is currently focused on France market.

The France Factory Automation and Industrial Controls Market Report is Segmented by Type (Industrial Control Systems: DCS, PLC, SCADA, PLM, MES, HMI, Other; Field Devices: Machine Vision, Industrial Robotics, Motors and Drives, Safety Systems, Sensors and Transmitters, Other), Component (Hardware, Software, Services), End-user Industry (Oil and Gas, Chemical and Petrochemical, Power and Utilities, Food and Beverage, Automotive and Transportation, Pharmaceutical, Other), Deployment Mode (On-premise, Cloud-based, Hybrid), and Sales Channel (Direct to End-user, System Integrators, Distributor/Reseller, Online Industrial Marketplace). The Market Forecasts are Provided in Terms of Value (USD).

By Type

| Industrial Control Systems | Distributed Control System (DCS) |

| Programmable Logic Controller (PLC) | |

| Supervisory Control and Data Acquisition (SCADA) | |

| Product Lifecycle Management (PLM) | |

| Manufacturing Execution System (MES) | |

| Human Machine Interface (HMI) | |

| Other Industrial Control Systems | |

| Field Devices | Machine Vision |

| Industrial Robotics | |

| Motors and Drives | |

| Safety Systems | |

| Sensors and Transmitters | |

| Other Field Devices |

By Component

| Hardware |

| Software |

| Services |

By End-user Industry

| Oil and Gas |

| Chemical and Petrochemical |

| Power and Utilities |

| Food and Beverage |

| Automotive and Transportation |

| Pharmaceutical |

| Other End-user Industries |

By Deployment Mode

| On-premise |

| Cloud-based |

| Hybrid |

By Sales Channel

| Direct to End-user |

| System Integrators |

| Distributor / Reseller |

| Online Industrial Marketplace |

| By Type | Industrial Control Systems | Distributed Control System (DCS) |

| Programmable Logic Controller (PLC) | ||

| Supervisory Control and Data Acquisition (SCADA) | ||

| Product Lifecycle Management (PLM) | ||

| Manufacturing Execution System (MES) | ||

| Human Machine Interface (HMI) | ||

| Other Industrial Control Systems | ||

| Field Devices | Machine Vision | |

| Industrial Robotics | ||

| Motors and Drives | ||

| Safety Systems | ||

| Sensors and Transmitters | ||

| Other Field Devices | ||

| By Component | Hardware | |

| Software | ||

| Services | ||

| By End-user Industry | Oil and Gas | |

| Chemical and Petrochemical | ||

| Power and Utilities | ||

| Food and Beverage | ||

| Automotive and Transportation | ||

| Pharmaceutical | ||

| Other End-user Industries | ||

| By Deployment Mode | On-premise | |

| Cloud-based | ||

| Hybrid | ||

| By Sales Channel | Direct to End-user | |

| System Integrators | ||

| Distributor / Reseller | ||

| Online Industrial Marketplace | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the France factory automation and industrial controls market by 2031?

The market is forecast to reach USD 14.22 billion by 2031.

Why is Food and Beverage automation accelerating in France?

Software, driven by digital-twin platforms and cloud MES, is expanding at a 4.38% CAGR.

Why is Food and Beverage automation accelerating in France?

EUR 2.3 billion France 2030 funding and strict traceability rules under AGEC and the upcoming Digital Product Passport are driving a 4.22% CAGR.

How are hydrogen projects influencing automation demand?

Gigafactories such as Normand'Hy and Genvia need sub-second distributed controls and high-density sensor networks, creating new opportunities for advanced control vendors.

What limits cloud adoption in French manufacturing plants?

Data-sovereignty rules, cybersecurity skills shortages, and latency-sensitive motion-control workloads keep many facilities on hybrid or on-premise architectures.