Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 1.41 Billion |

| Market Size (2031) | USD 1.67 Billion |

| Growth Rate (2026 - 2031) | 3.38% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Ceramic Tiles Market Analysis by Mordor Intelligence

The France Ceramic Tiles Market size is estimated at USD 1.41 billion in 2026, and is expected to reach USD 1.67 billion by 2031, at a CAGR of 3.38% during the forecast period (2026-2031).

Growth is steady rather than rapid as residential renovation demand offsets a still-recovering new-build cycle, while premiumization in porcelain formats supports value expansion despite volume pressures in price-sensitive segments. Producer turnover signals margin tension at the factory gate, with the manufacturing turnover index for porcelain and ceramic products at 105.19 in August 2025 on a 2021 equals 100 base, below 2024 averages, even as installed-flooring demand remains resilient. Price momentum in floor and wall covering works has stayed positive through 2025, suggesting sustained replacement activity that underpins the France ceramic tiles market during a period of construction normalization. Policy support geared to energy retrofits, including 2026 household renovation funding allocated by the national housing agency, keeps residential consumption in focus and will continue to pull ceramic specifications into bundled upgrades.

Key Report Takeaways

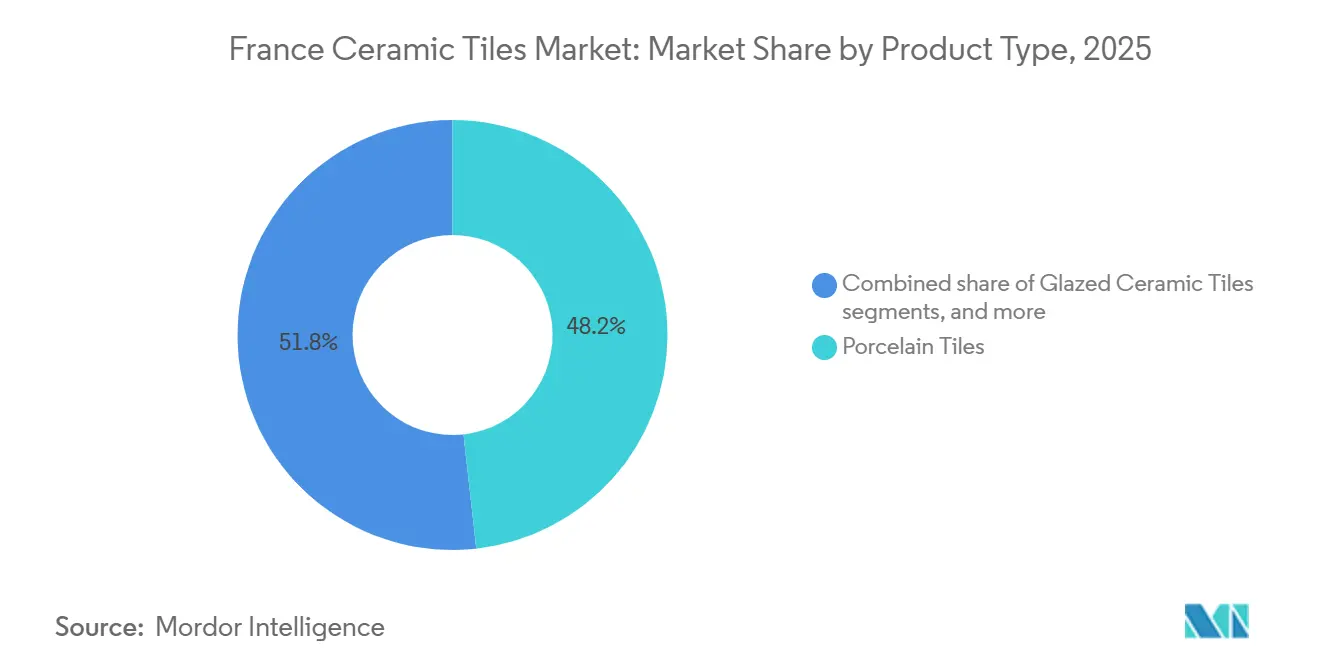

- By product type, porcelain tiles held 48.23% of the France ceramic tiles market share in 2025, while mosaic tiles are expected to post the fastest growth at a 3.68% CAGR through 2031.

- By application, floor use accounted for 63.11% of the France ceramic tiles market share in 2025, and roofing is projected to grow at a 3.56% CAGR to 2031.

- By end-user, residential reached 57.81% of the France ceramic tiles market share in 2025, and it is forecast to grow at a 3.89% CAGR through 2031.

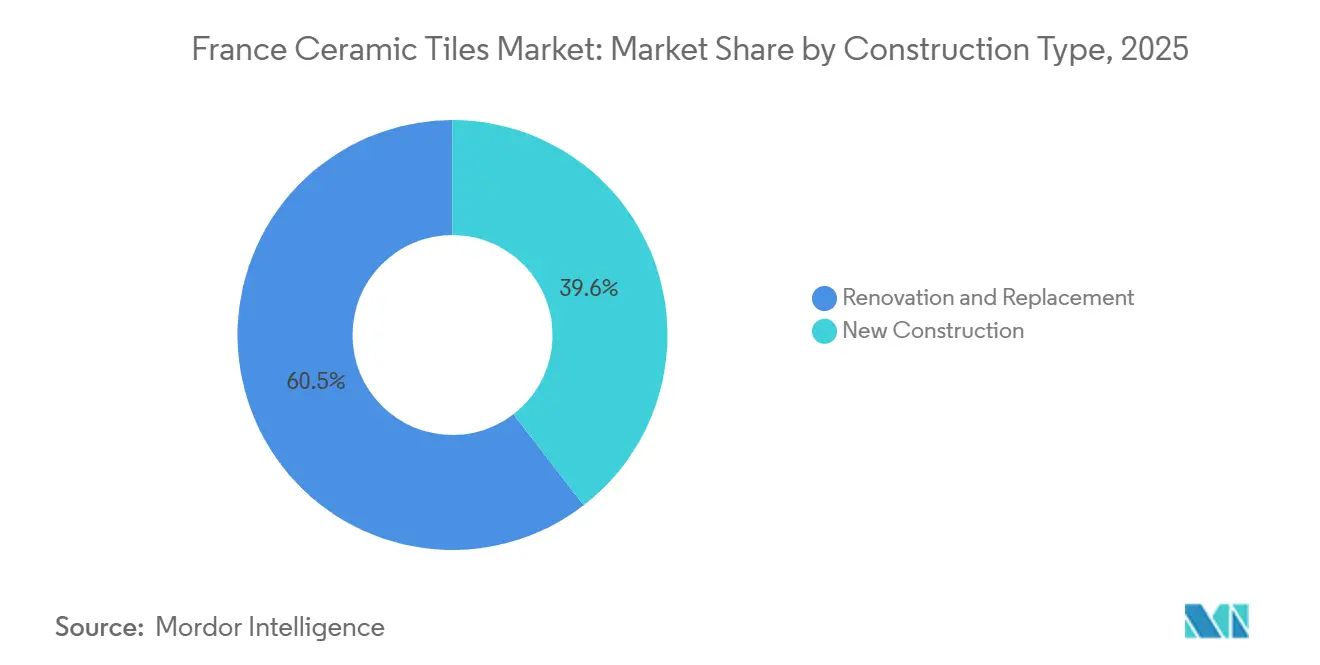

- By construction type, renovation and replacement captured 60.45% of the France ceramic tiles market share in 2025, while new construction is projected to advance at a 3.62% CAGR to 2031.

- By distribution channel, specialty tile and stone stores held 37.73% of the France ceramic tiles market share in 2025, and online retail is set to expand at a 4.34% CAGR through 2031.

- By geography, Île-de-France accounted for 36.82% of the France ceramic tiles market share in 2025, and Provence-Alpes-Côte d’Azur is forecast to grow at a 3.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renovation wave backed by MaPrimeRénov & CEE subsidies | +1.2% | National, with the highest uptake in Île-de-France, Auvergne-Rhône-Alpes, and energy-inefficient housing stock in northern regions | Medium term (2-4 years) |

| Post-COVID home-improvement culture sustains DIY tile demand | +0.4% | National, with outsized gains in peri-urban and rural communes where remote work adoption is highest | Short term (≤ 2 years) |

| Shift to large-format porcelain for premium aesthetics & durability | +0.6% | Île-de-France, Provence-Alpes-Côte d’Azur, Lyon metropolitan area, affluent urban cores with high design consciousness | Medium term (2-4 years) |

| Pilot green-hydrogen kilns lower the embodied carbon of French tiles | +0.2% | Provence's proximity to Novoceram’s Laveyron plant and to Lhyfe’s Bessières facility, with potential expansion to Auvergne-Rhône-Alpes production clusters | Long term (≥ 4 years) |

| Antibacterial glazed tiles gain traction in hospital upgrades | +0.3% | National, focused on university hospital centres in Paris, Lyon, Marseille, Toulouse | Medium term (2-4 years) |

| Italy–Spain–France rail corridor cuts delivery lead-time & cost | +0.5% | Mediterranean Arc including Provence-Alpes-Côte d’Azur and Occitanie | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Renovation Wave Backed by MaPrimeRénov & CEE Subsidies

France’s renovation funding pipeline continues to reinforce residential flooring upgrades, which anchors near-term demand in the France ceramic tiles market. The national housing agency’s board adopted a provisional budget of USD 5.4 billion (EUR 4.6 billion) for 2026, assigning USD 5.1 billion (EUR 4.4 billion) to household aid with a target of nearly 350,000 homes, including at least 120,000 high-quality energy renovations and a minimum of 150,000 single-action renovations, which sustains the flow of eligible projects where flooring work is bundled with envelope and systems upgrades [1]Agence nationale de l’habitat, “Board adopts 2026 orientations and budget,” ANAH, anah.gouv.fr. The energy savings certificates scheme runs in parallel to this allocation, and the government’s 2025–2035 program blueprint indicates continued obligations and policy continuity that keep renovation volumes stable across the medium term. These supports keep spending directed at durable finishes in kitchens, bathrooms, and entryways, where ceramic provides hygiene, water resistance, and long life. The program design favors projects that lift energy performance categories, which encourages comprehensive scopes that include surface renewals alongside thermal retrofits.

Shift to Large-Format Porcelain for Premium Aesthetics & Durability

Large-format porcelain is consolidating value in the France ceramic tiles market because it delivers a clean-lined aesthetic with fewer grout joints while retaining low water absorption and high strength. Design-driven residential projects in metropolitan cores and premium commercial programs are specifying rectified-edge products, which support a mix shift toward higher ticket items. French production linked to established champions can leverage group-scale capabilities to offer formats up to 120 centimetres while maintaining local finishing and quality control, aligning with buyer preference for certified, low-emission portfolios. The technical profile of porcelain, including low porosity and abrasion resistance, also matches the maintenance objectives in high-traffic venues. As formats scale up, specialized handling, levelling systems, and pro installers remain important, which helps specialty tile stores maintain relevance in a channel mix that is otherwise opening to digital journeys.

Pilot Green-Hydrogen Kilns Lower Embodied-Carbon of French Tiles

Energy transition pilots are moving from concept to field tests, and that is beginning to change procurement criteria for ceramic tiles in France. In July 2025, Lhyfe completed combustion tests demonstrating hydrogen as a full substitute for natural gas in ceramic firing, using a mixing kit that allows scaling up hydrogen injection and burner replacement, with hydrogen supplied from its Bessières plant rated up to 2 tonnes per day [2]Lhyfe, “Lhyfe successfully completes first combustion tests using green hydrogen,” Lhyfe, lhyfe.com. These trials show a credible decarbonization route for energy-intensive firing steps, an important lever since firing dominates the ceramic sector’s emissions profile in Europe. While cost and supply of green hydrogen remain constraints until broader infrastructure matures, early adopters can differentiate in public tenders that include embodied carbon criteria. Sector roadmaps to 2050 outline the investment scale and sequencing needed to align with net-zero pathways, reinforcing the long-term relevance of these pilots.

Antibacterial Glazed Tiles Gain Traction in Hospital Upgrades

In healthcare settings, ceramics’ hygiene properties and options for antibacterial glazing are aligning with upgrade cycles and indoor air quality expectations. Hospital and clinic renovations prioritize impermeable, low-emission finishes, and French-made portfolios with EU Ecolabel coverage and ISO 17889-1 sustainability certification fit these specification criteria. Products tested under relevant antibacterial standards, combined with A+ VOC labeling that confirms zero emissions of toxic substances for certified ranges, are well placed for procurement frameworks that screen on emissions and cleanliness. As the France ceramic tiles market follows broader public infrastructure updates, these attributes take on higher weight in product selection alongside lifecycle cost and maintenance performance. Manufacturer disclosures of full-range certifications help reduce qualification friction in public tenders and can speed adoption.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile energy tariffs inflate firing costs | -0.7% | National, acute where industrial electricity contracts are less competitive under TURPE 7 | Short term (≤ 2 years) |

| Vinyl & LVT products erode price-sensitive residential share | -0.9% | Suburban belts in Grand Est, Hauts-de-France, and Normandy | Medium term (2-4 years) |

| Skilled tile-layer shortage delays project timelines | -0.5% | National, acute in Brittany, Burgundy-Franche-Comté, and rural departments | Short term (≤ 2 years) |

| Tighter EU-ETS Phase IV benchmarks raise compliance outlays | -0.3% | National, domestic producers are most exposed to any CBAM scope change post-2027 review | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Energy Tariffs Inflate Firing Costs

Energy is a core input in ceramic firing, and the price dynamics across the French electricity and gas landscape keep cost pass-through and margin management in the foreground. Producer price indicators for energy-linked utilities show that energy costs in 2025 remained above the 2021 baseline, which sustained a higher cost floor for energy-intensive production even after the acute phase of the energy crisis had passed. Changes to grid access charges under the TURPE 7 framework reflect step-ups in planned network investments at the transmission and distribution levels through 2028, which translate into structural upward pressure on grid fees that manufacturers pay regardless of commodity price swings. The restoration and subsequent increase of the electricity excise duty for businesses in 2024 and 2025 added to the total delivered power cost, complicating hedging strategies for kiln operations that benefit from steady baseload. While Eurostat data point to a 9.0% decline in non-household electricity prices in the first half of 2025 compared with the first half of 2024, which offers some temporary relief, the totality of regulated charges and tax changes continues to weigh on unit economics. [3]Eurostat, “Electricity price statistics,” Eurostat, ec.europa.eu.

Skilled Tile-Layer Shortage Delays Project Timelines

Labor bottlenecks in skilled installation trades are a practical constraint on growth, particularly in residential renovation, where homeowner timelines and budgets are sensitive to availability. Through 2025, the construction employment picture stabilized after a period of decline, but hiring remains uneven by region and role, and vacancies in building trades take longer to fill than before the pandemic. Sector surveys and labour market intelligence show persistent tightness for specific construction roles, which adds time and cost to ceramic jobs that require qualified setters and finishers. These dynamics make planning more complex for contractors and specialty retailers who must align deliveries, jobsite readiness, and installer schedules. As a result, some projects trade off toward materials with faster installation profiles, a pressure that tile suppliers can partially offset through ready-to-use installation systems and training that expand the pool of competent installers.

Segment Analysis

By Product Type: Porcelain Dominates, Mosaics Climb on Artisan Appeal

Porcelain tiles accounted for 48.23% in 2025, leading the category with a performance profile that suits heavy footfall and wet-area demands where low water absorption and high strength are essential. This leadership anchors product mix in the France ceramic tiles market, even as mosaics post the fastest growth on the back of design flexibility for feature walls and complex surfaces. Certified low-VOC portfolios and sustainability labels support glazed lines in projects that specify indoor air quality outcomes, which helps French-made collections maintain preference in public and private tenders. Large-format porcelain formats are widening in availability through group-scale platforms while local finishing maintains domestic brand equities, a combination that strengthens showroom appeal and supports premium price points. As price differentials between porcelain and standard glazed ceramic continue to narrow, project specifications tip more often toward porcelain in main living areas while mosaics and specialty pieces lift the decorative end of the range.

Mosaic tiles are expected to post the fastest growth at a 3.68% CAGR through 2031. Developers and homeowners use porcelain for high-wear floors and high-moisture zones, while mosaics gain in spas, pools, and accent walls, which diversifies growth drivers within the France ceramic tiles market. Specialty retailers are adapting with larger display bays and handling fixtures for formats up to 120 centimetres, which improves the path to purchase for premium collections. The balance of in-store curation and digital visualization helps communicate finish, texture, and scale, which are pivotal for large-format adoption. In this context, the France ceramic tiles market size attributed to mosaics is expected to expand in line with their segment-leading growth, with designers favouring colourways and modularity that suit boutique hospitality and residential upgrades. Certified ranges that combine aesthetics with low emissions and traceable production carry an advantage in procurement and deliver longer-term brand loyalty.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Flooring Anchors Volume, Roofing Emerges in Heritage Work

Floor installations represented 63.11% of value in 2025, and they remain the core application where service life, cleanability, and abrasion resistance justify total installed cost in residential and commercial settings. The France ceramic tiles market continues to rely on floors for scale, while roofing grows from a smaller base at a 3.56% CAGR through 2031, on projects that combine envelope repairs with energy upgrades in heritage contexts. Wall applications keep a stable role in wet zones and in feature settings where decorative glazes are specified to meet moisture control and visual design outcomes. Positive pricing indicators for floor and wall covering works in 2025 line up with steady renovation activity, which supports flooring volumes despite competitive alternatives in new-build segments. Public and private facility standards increasingly emphasize durability and hygiene in high-traffic areas, further reinforcing floor application selection in transport and institutional environments.

Within the segment, the France ceramic tiles market size linked to roofing applications is projected to expand in line with the forecast growth rate as municipalities and owners combine envelope interventions with climate adaptation aims. Where projects are procurement-driven, hard-surface preferences and compliance requirements support ceramic use in corridors, lobbies, and restrooms. The main line of defence for flooring against substitutes is total lifecycle cost, which remains favourable where heavy use and frequent cleaning are expected. As large-format options proliferate, floors can achieve a seamless look that meets contemporary design briefs while reducing grout line maintenance. Taken together, these conditions keep floors central to demand while roofing captures incremental value in specialized retrofit programs.

By End-User: Residential Renovation Drives Growth Across Income Segments

Residential accounted for 57.81% of the value in 2025 and is forecast to grow fastest at a 3.89% CAGR through 2031, reflecting policy-led retrofits and a persistent desire to improve home environments. The France ceramic tiles market is therefore weighted toward households undertaking bathroom and kitchen upgrades and entry area refreshes, with subsidies easing up-front budget constraints. Commercial end-use remains attractive for premium lines where lifecycle costing matters, including hospitality, healthcare, offices, education, retail, and transport hubs that demand durability and non-combustibility. In 2025, business sentiment in building construction improved modestly, and expected activity for maintenance and improvement turned positive, which helps contractor pipelines and supports material flows for commercial refits. Certifications that validate low emissions and hygienic performance add value in healthcare and education, where procurement checklists prioritize verified attributes.

Household demand remains broad-based across income bands, since program designs target both comprehensive retrofits and single-action projects, which keeps volumes moving for a range of price tiers. That dynamic helps the France ceramic tiles market sustain volumes even when new-build momentum is muted, because renovation decisions are less cyclical in commercial, transport hubs, and public facilities set high bars for floor performance under heavy pedestrian loads, which keeps ceramic in the consideration set for concourses and terminals. Offices and retail increasingly use large-format surfaces for contemporary fit-outs, while hospitality fosters demand for mosaics and specialty finishes. Together, these consumption patterns diversify end-user risk and support steady mix improvement across the forecast horizon.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Construction Type: Renovation Dominates, New Construction Rebounds from Trough

Renovation and replacement represented 60.45% of the value in 2025, confirming the central role of retrofit activity in France’s built environment priorities. Policy signals through 2026 support this emphasis, and they sustain project pipelines that include flooring as part of complete room or whole-home upgrades. New construction is projected to grow faster at a 3.62% CAGR to 2031 from a low base, which supports a gradual rebalancing of demand between replacement and new-build channels later in the period. Regional housing authorization data for 2024 show weak private activity in some areas, but social housing financing trends improved, which points to a mixed yet stabilizing outlook for new unit delivery that will feed flooring work later in construction cycles. These factors support a steady base of orders for suppliers while they prepare for a modest new-build upswing.

As a result, the France ceramic tiles market size tied to new construction should expand in line with the projected growth rate, although it will likely remain smaller than the renovation value through 2031. Renovation’s dominance continues to favour channels that serve homeowners and small contractors, with specialty retailers and pro networks central to project execution. Where developers resume projects, direct sales to contractors pick up, and bidders will weigh total installed cost, schedule, and maintenance in material selection. Installing system innovations and installer training can help manage jobsite schedules and quality on both new-build and retrofit projects. With this split, suppliers can balance product portfolios to match order patterns across project types.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Specialty Stores Lead, Online Retail Accelerates

Specialty tile and stone stores held 37.73% share in 2025, reflecting the importance of in-person evaluation for texture, finish, and colour, and the value of pro installer referrals offered by these outlets. The France ceramic tiles market continues to rely on this channel for premium and complex projects, as large-format handling and technical advice remain differentiators. At the same time, online retail is projected to post the fastest growth at a 4.34% CAGR to 2031 as visualization tools shorten selection cycles and logistics improvements support direct-to-consumer fulfilment for small and medium-sized orders. Big-box home improvement stores capture demand for standard sizes and DIY-friendly kits, especially for simple wall upgrades or small rooms. The rebalancing of channel mix is therefore gradual, and omnichannel models that pair online discovery with in-store pickup or consultation are gaining traction.

In this context, the France ceramic tiles market size fulfilled through digital channels will rise from a small base, while specialty stores retain leadership by elevating service and curation. Pure-play online platforms will continue to penetrate categories that ship well and do not require palletized freight, such as mosaics and accessory packs. For project-based purchases, the need to coordinate adhesives, grouts, trims, and installers keeps customers engaged with specialists who can recommend full systems. As professional installers remain in short supply in some regions, retailers that can mobilize reliable networks hold an advantage. This mix supports steady store traffic even as e-commerce grows.

Geography Analysis

In 2025, Île-de-France accounted for 36.82% of the market value, establishing itself as the largest regional consumer base due to significant renovation activities across dense residential areas and extensive commercial facilities. The ceramic tiles market in France remains concentrated in and around Paris, supported by project pipelines spanning private housing, hospitality, and institutional buildings. Provence-Alpes-Côte d’Azur is projected to grow at a 3.85% CAGR through 2031, driven by an extended construction season and sustained demand for premium residential and hospitality projects. In Auvergne-Rhône-Alpes, a decline in new housing authorizations in 2024 contrasts with increased social housing financing, indicating a shift in construction priorities. Elsewhere, regional markets are shaped by local labor availability and the pace of subsidy-driven home improvements.

In Île-de-France, tight project schedules and complex logistics favor established specialty retailers and professional networks, as project teams rely on trusted suppliers and installers. The region benefits from high-value renovations in commercial and institutional buildings, which prioritize durable, low-emission finishes, alongside household upgrades. Evolving rental regulations and environmental performance objectives incentivize property owners to enhance unit quality and communal spaces, maintaining ceramic tiles as a preferred choice. Public procurement cycles for schools, hospitals, and transport hubs further contribute to stable demand for compliant hard surfaces, reinforcing the region’s market leadership.

Provence-Alpes-Côte d’Azur combines steady renovation activity with selective new construction, favoring aesthetics and outdoor living elements that align with ceramic surfaces. Hospitality projects adopting large-format porcelain and designer mosaics enhance guest experiences, further driving demand. However, skilled installer availability varies across departments, influencing project timelines and product choices. Suppliers that coordinate with installer networks and align deliveries with project schedules are well-positioned to capture market share. Meanwhile, Auvergne-Rhône-Alpes and other regions face diverse labor and demand dynamics, with social housing programs stabilizing tile consumption despite private demand fluctuations. Digital adoption aids planning, but project execution depends on securing qualified crews, particularly for complex installations. Late 2025 improvements in construction employment and business sentiment suggest a cautiously optimistic recovery trajectory.

Competitive Landscape

The France ceramic tiles market is moderately fragmented with top suppliers dominating. This profile reflects strong import competition coupled with domestic players that differentiate through local manufacturing, sustainability certifications, and service. Product innovation and format premiumization are critical levers for share gain, and established firms continue to invest in digital printing lines and rectified-edge capabilities. As procurement frameworks place more emphasis on environmental criteria, manufacturers with credible pathways to lower embodied carbon can strengthen their bids.

On the sustainability front, manufacturers are aligning portfolios with certifications that validate low emissions and responsible production, which helps in public tenders and green building projects. French-made collections with EU Ecolabel coverage and ISO 17889-1 certification provide an advantage in specifications that require documented credentials. Decarbonization pilots, including the use of green hydrogen for kiln firing, signal future differentiation on carbon intensity that may influence project selection in segments sensitive to embodied carbon. Commercial buyers, especially in healthcare and education, give weight to these attributes alongside lifecycle cost and maintenance. Early adopters who translate pilot learnings into repeatable operations will be positioned for medium-term gains.

Channel strategy is also a point of differentiation, as specialty retailers retain their place in complex and premium projects while e-commerce grows fastest from a low base. The France ceramic tiles market rewards brands and distributors that can combine digital visualization, quick availability on core SKUs, and reliable pro installer networks. Suppliers that offer complete installation systems, training, and after-sales support can mitigate labour constraints and reduce callbacks, which creates loyalty among contractors. Digital tools that simplify format selection and pattern planning reduce decision friction for homeowners and designers. Over time, omnichannel investments should help close the gap between discovery and purchase, especially in mid-market renovations.

France Ceramic Tiles Industry Leaders

Saint-Gobain Weber

Novoceram

Porcelanosa Grupo

Roca Cerámica

Marazzi Group

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: Porcelanosa Group expanded its network by opening 18 company-owned stores in Spain and internationally, including France and other European markets. The Spanish multinational, with over 200 proprietary stores and 1,000 authorized sales points globally, launched new outlets in Cáceres, Oviedo, Gijón, Andorra, and Cascais, with Bilbao and Huelva openings scheduled for December.

- November 2025: Saint-Gobain Ceramics and Eurodia Industrie announced a strategic partnership to address the growing Direct Lithium Extraction (DLE) market. By integrating Saint-Gobain's advanced lithium-selective adsorbent materials with Eurodia's process engineering expertise, the collaboration aims to accelerate the deployment of sustainable, high-efficiency lithium extraction systems, supporting global electrification and energy transition efforts while minimizing environmental impact.

- September 2025: Marazzi, the Italian tile manufacturer, expanded its Lume porcelain stoneware collection for 2025 by introducing four new colors: Bone, Caramel, Emerald, and Ocean, alongside two 3D structures, Rake and Swing. Known for its zellige-like appearance and ultra-glossy surfaces, the collection now offers enhanced design versatility, complementing its existing shades and catering to modern interior aesthetics.

- August 2025: ABK Group presented innovative ceramic tile products and highlighted prestigious collaborations at the Cersaie exhibition in Bologna. For Cersaie 2025, the Group plans to showcase its offerings and partnerships globally. A new stand in Hall 29 will, for the first time, consolidate all its brands, showcasing diverse ceramic interpretations in a unified space.

France Ceramic Tiles Market Report Scope

Ceramic Tiles are made up of sand, natural products, and clays and once it is molded into a shape, they are fired into a kiln. Ceramic tiles are durable, resistant to water, moisture, and fire, and cheap as compared to other flooring products.

The France Ceramic Tiles Market Report is Segmented by Product Type (Porcelain, Glazed Ceramic, and More), Application (Floor, Wall, and More), End-User (Residential, Commercial), Construction Type (New Construction, Renovation), Distribution Channel (Specialty Tile & Stone Stores, Home Improvement & DIY Stores, and More), and Geography (Île-de-France, Auvergne-Rhône-Alpes, and More). Market Forecasts are Provided in Value (USD).

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Others |

By Construction Type

| New Construction |

| Renovation & Replacement |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| Île-de-France |

| Auvergne-Rhône-Alpes |

| Provence-Alpes-Côte d’Azur |

| Rest of France |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation & Replacement | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | Île-de-France | |

| Auvergne-Rhône-Alpes | ||

| Provence-Alpes-Côte d’Azur | ||

| Rest of France | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current France ceramic tiles market size and projected growth to 2031?

The France ceramic tiles market size is USD 1.41 billion in 2026 and is projected to reach USD 1.67 billion by 2031 at a 3.38% CAGR.

Which product segment leads and which one grows fastest in France?

Porcelain tiles lead with 48.23% in 2025, while mosaic tiles are projected to grow fastest at a 3.68% CAGR through 2031.

How are policy subsidies affecting residential demand in France?

The ANAH board set a 2026 budget with EUR 4.4 billion for household aid targeting nearly 350,000 homes, which sustains project pipelines that include ceramic flooring upgrades.

Which region holds the largest share, and which region grows fastest?

Île-de-France holds 36.82% of the value in 2025, and Provence-Alpes-Côte d’Azur is projected to grow fastest at a 3.85% CAGR to 2031.

What energy and cost factors are most constraining for French tile producers?

Elevated network charges under TURPE 7 and the restored excise duty raise delivered electricity costs, though non-household electricity prices fell 9.0% in H1 2025 versus H1 2024.

Which sales channels are gaining the most traction in France?

Specialty stores remain the largest at 37.73% in 2025, while online retail is projected to grow fastest at a 4.34% CAGR through 2031 with the help of visualization tools and improved logistics.