Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

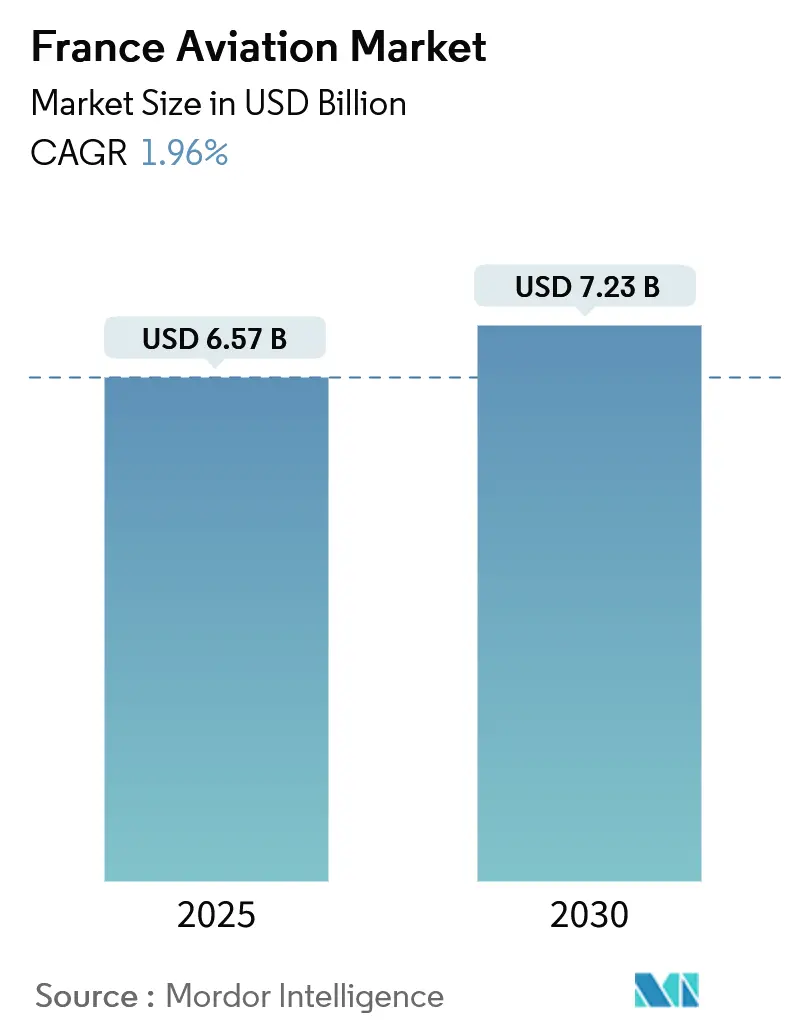

| Market Size (2025) | USD 6.57 Billion |

| Market Size (2030) | USD 7.23 Billion |

| Growth Rate (2025 - 2030) | 1.96% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

France Aviation Market Analysis by Mordor Intelligence

The France aviation market size is valued at USD 6.57 billion in 2025 and is forecast to reach USD 7.23 billion by 2030, registering a 1.96% CAGR. Growth is moderate because the country has reached a mature stage where airline and corporate operators focus on replacing aging fleets with fuel-efficient platforms rather than adding new capacity. Fleet renewal, recovery in international passenger demand, and rising business jet usage provide incremental lift even as supply chain bottlenecks delay new-aircraft deliveries. Investments in hydrogen demonstrators and sustainable aviation fuel position domestic manufacturers for future technology shifts while EU environmental policies continue to shape purchasing decisions. Meanwhile, cargo operators are accelerating freighter acquisitions to meet the booming e-commerce demand.

Key Report Takeaways

- By aircraft type, commercial aviation led with a 50.04% share of the France aviation market in 2024, while general aviation is projected to expand at a 2.53% CAGR through 2030.

- By propulsion technology, turbofan engines captured 54.26% of France aviation market size in 2024, whereas the turboshaft segment is advancing at a 2.27% CAGR through 2030.

- By end user, civil and commercial operators accounted for 58.97% of France's aviation market size in 2024; business and general aviation end users registered the fastest market expansion, with a 2.89% CAGR from 2024 to 2030.

France Aviation Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet renewal mandates to improve efficiency and reduce emissions | +0.8% | National (Paris CDG, Orly, Lyon) | Medium term (2-4 years) |

| Recovery in domestic and international air travel demand | +0.2% | National (Paris, Nice, Marseille) | Short term (≤ 2 years) |

| Growth in business aviation activity supporting premium connectivity | +0.6% | Paris Le Bourget, Cannes, Nice | Medium term (2-4 years) |

| Expansion of air cargo operations driven by e-commerce growth | +0.5% | CDG cargo hub, Lyon freight | Long term (≥ 4 years) |

| EU avgas tax exemptions encouraging general aviation training activity | +0.3% | Regional airports, flight schools | Long term (≥ 4 years) |

| Government-backed hydrogen aircraft development through CORAC funding | +0.4% | Toulouse aerospace cluster | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Fleet Renewal Mandates Drive Efficiency Transformation

New EU environmental rules are accelerating the replacement of legacy wide-body and narrow-body fleets, as operators retire older A340 and 777 aircraft in favor of A350 and A220 models.[1]Air France-KLM, “Annual Report 2024,” airfranceklm.com Orders for the A320neo family from French carriers climbed 15% in 2024, showing a growing preference for 20-30% fuel-burn gains over previous-generation jets. Regional airlines such as Air Corsica and French Bee adopt similar strategies to defend route profitability against carbon-pricing headwinds. Leasing companies benefit as carriers extend usage of existing aircraft while awaiting delayed deliveries, creating short-term demand for mid-life assets. Fleet renewal activity adds steady value to the French aviation market, even under modest topline growth.

Business Aviation Connectivity Demands Reshape Market Dynamics

Corporate jet movements at Le Bourget increased 12% year-over-year in 2024, as multinational executives prioritized flexibility over ticket costs. Luxury-goods leaders LVMH and Kering increased charter missions between Paris, Geneva, and New York, supporting Dassault’s record Falcon deliveries—60% directed to European buyers. On-demand air taxi networks, which cover Paris, Lyon, and regional areas, including those that serve Paris-Lyon and the Riviera resorts, further diversify revenue streams for operators. The rise of point-to-point business flying strengthens demand for light and super-midsize jets, reinforcing the premium on dispatch reliability and carbon efficiency.

E-Commerce Logistics Accelerate Air-Cargo Infrastructure Investment

Freight tonnage at Charles de Gaulle rose 8% in 2024 as Amazon and DHL expanded dedicated air-freight hubs to manage next-day delivery expectations. Cargo carriers placed incremental orders for converted narrowbody freighters and ATR turboprops, enabling flexible uplift to smaller cities such as Bordeaux and Nantes. Upgrades to cold-chain handling and automated sortation systems expand opportunities for avionics suppliers, ground-support equipment manufacturers, and maintenance providers specializing in cargo configurations.

Hydrogen Aircraft Development Positions France as Innovation Leader

The French government allocated EUR 300 million (USD 327 million) toward hydrogen-propulsion research under the CORAC program in 2024.[2]French Ministry of Ecological Transition, “CORAC Hydrogen Aircraft Program,” ecologie.gouv.fr Airbus’s Toulouse-based ZEROe demonstrator aims for commercial service by 2035, prompting airports and energy firms to prototype on-site green-hydrogen production and refueling infrastructure. Component makers and engineering consultancies secure early contracts to design cryogenic tanks, fuel cell stacks, and thermal management systems. A successful demonstration could pivot the France aviation market toward alternative-propulsion leadership over the long term.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising jet fuel prices and EU ETS-related cost inflation | -0.3% | Nationwide commercial operations | Short term (≤ 2 years) |

| Ongoing global supply chain disruptions in aerospace manufacturing | -0.2% | Toulouse, Paris clusters | Medium term (2-4 years) |

| Operational restrictions from night-time noise curfews at regional airports | -0.1% | Orly, Nice, Lyon | Long term (≥ 4 years) |

| Airspace congestion due to NATO and defense-related prioritization | -0.1% | Eastern France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU ETS Expansion Creates Cost Pressures Across Aviation Segments

Air France-KLM incurred EUR 120 million (USD 139.92 million) in additional compliance costs during 2024, prompting capacity cuts on unprofitable regional routes. Smaller carriers lack the scale to absorb carbon charges of EUR 50-80 (USD 58-93) per ton of CO₂, which pressurizes ticket pricing and potentially reduces service to secondary cities.[3]European Commission, “EU ETS Aviation Sector Report,” ec.europa.eu The cost gap versus non-EU competitors on intercontinental sectors also squeezes margins, compelling French airlines to accelerate fleet renewal and network optimization.

Supply Chain Bottlenecks Constrain Aircraft Delivery Schedules

CFM International reported a 6-month average delay in LEAP engine shipments, forcing Airbus to trim its A320neo delivery guidance by 10% for 2024. Titanium forging shortages and avionics chip scarcity extend lead times for new aircraft and helicopter programs. Operators keep older jets in service for longer, increasing maintenance costs and tempering carbon efficiency gains. The supply chain drag caps the near-term expansion of the France aviation market despite healthy underlying demand.

Segment Analysis

By Aircraft Type: Commercial Aviation Dominance Amid General-Aviation Acceleration

Commercial aviation accounted for 50.04% of France's aviation market size in 2024, reflecting the hub-and-spoke networks of Air France-KLM and the near return of passenger volumes to pre-pandemic levels. Narrowbody orders—anchored by the Airbus A320neo family—equaled 60% of all new commercial aircraft commitments in 2024, showing preference for fuel-efficient units on intra-European routes. Widebody demand remains tempered as airlines redeploy twin-aisle capacity selectively on long-haul lanes to North America and Asia.

General aviation is the fastest-growing category with a 2.53% CAGR, supported by EU avgas-tax exemptions that lower training costs and increase corporate jet adoption for executive travel. Business jet OEMs, such as Dassault, enjoy a 24-month Falcon backlog, while regional flight schools expand their fleets of piston trainers to address pilot shortage concerns. Military aviation delivers steady but low-growth revenues through ongoing Rafale and A400M procurement lots financed under France’s 2024-2030 defense spending plan.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Propulsion Technology: Turbofan Leadership Challenged by Emerging Technologies

Turbofan engines represent 54.26% of France's aviation market share in 2024, led by the CFM LEAP and Pratt & Whitney GTF programs, which provide 15-20% better fuel economy than preceding models.[4]International Air Transport Association, “Global Aviation Industry Report 2024,” iata.org Airlines prioritize twin-engine narrowbody efficiency to mitigate ETS-related charges and volatile jet-fuel prices.

Turboshaft propulsion posts the highest 2.27% CAGR through 2030 as helicopter demand rises for emergency medical flights, offshore wind farm support, and nascent urban-air-mobility services. Meanwhile, piston and turboprop segments keep niche relevance in training, regional passenger, and cargo roles, aided by established maintenance networks. Electric and hydrogen-propulsion prototypes are emerging, but are unlikely to influence market revenues before 2030 significantly.

By End User: Business Aviation Owners Drive Market Growth

Civil and commercial operators command 58.97% of France aviation market in 2024, comprising flag carriers, low-cost airlines, and dedicated cargo lines. Nevertheless, business and general aviation owners post the swiftest 2.89% CAGR as corporate flight departments and high-net-worth individuals acquire light and super-mid-size jets for intra-Europe trips.

Government and defense agencies consistently procure Rafale fighters, NH90 and H160M helicopters, and A330 MRTT tankers. The predictable military backlog provides long-term stability to domestic manufacturers and their tier-one suppliers, without materially altering the market growth hierarchy.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The Paris metropolitan zone accounted for 65% of national aircraft movements in 2024, anchored by Charles de Gaulle’s intercontinental hub, Orly’s dense point-to-point network, and Le Bourget’s premier business-aviation complex. Nice, Lyon, and Marseille airports serve secondary passenger flows and leisure travel, although each faces stricter night-time noise curfews that constrain slot availability.

Toulouse hosts Airbus final assembly lines and a critical aerospace supplier ecosystem, making the Occitanie region central to both domestic deliveries and export production. The CORAC-funded hydrogen technology programs further cement Toulouse as a long-term innovation hub.

Regional airports from Bordeaux to Brest cater to flight-training academies and low-cost carriers. Yet uneven infrastructure and localized environmental limits temper expansion outside Paris and the Mediterranean corridor.

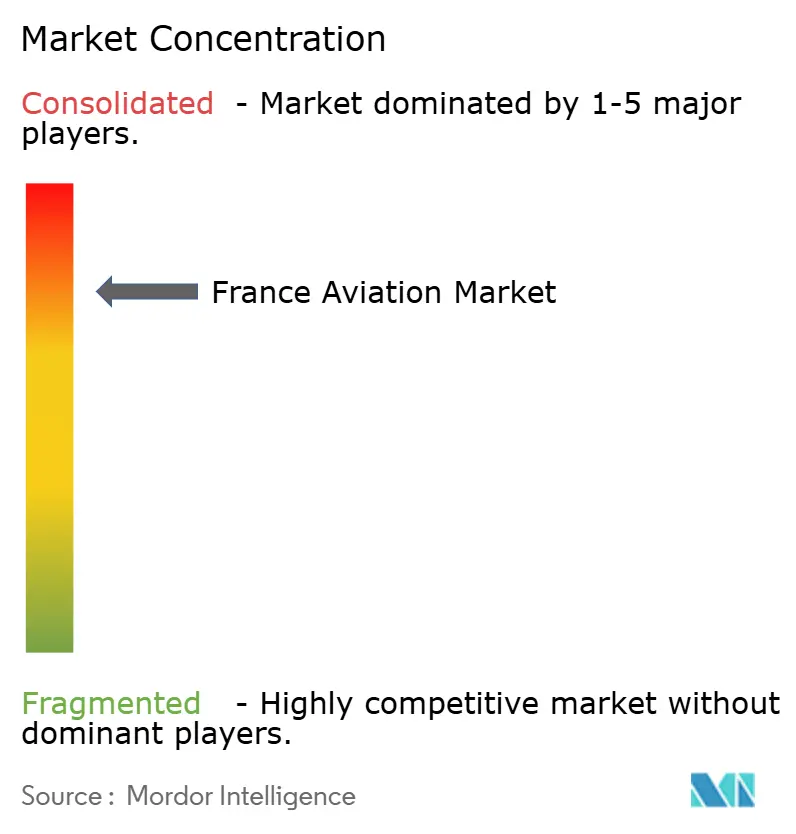

Competitive Landscape

Airbus SE and Dassault Aviation shape the French aviation market through vertical integration, proprietary technology, and scale advantages. Airbus leads in commercial jet deliveries, while Dassault dominates the niche of business jets and fighters. The top five manufacturers account for a majority of the market share in total domestic aviation value, indicating a moderately concentrated field with room for emerging technology challengers.

Electric-aircraft startups and sustainable-fuel producers pursue market entry in commuter, training, and cargo sub-segments. Patent applications for electric-propulsion components from French entities increased by 40% in 2024, underscoring the competitive tension surrounding future-tech leadership. Cooperative ventures—such as the 2024 Thales-Leonardo avionics pact—illustrate a shift toward strategic alliances that pool R&D funding and accelerate certification paths.

Traditional OEMs counter potential disruption by investing in digital manufacturing, SAF blending facilities, and hydrogen test beds to lock in early-stage regulatory compliance advantages. Supply chain dependencies remain critical vulnerabilities, compelling manufacturers to internalize key component production where feasible.

France Aviation Industry Leaders

-

Airbus SE

-

Dassault Aviation

-

The Boeing Company

-

ATR

-

DAHER

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: The French Directorate General of Armaments (DGA) selected the Pilatus PC-7 MKX as the basic training aircraft for the French Air and Space Force and the French Navy. The fleet of 22 trainer aircraft will begin delivery in 2027.

- January 2025: Airbus Helicopters delivered two H225M helicopters to the French Armament General Directorate (DGA) for operation by the French Air and Space Force. These aircraft will replace overseas-deployed Puma helicopters, standardize the force's helicopter fleet, and conduct operational, search and rescue, and utility missions.

- January 2024: France awarded a USD 5.5 billion contract to Dassault Aviation for 42 Rafale F4 standard fighter jets.

France Aviation Market Report Scope

Commercial Aviation, General Aviation, Military Aviation are covered as segments by Aircraft Type.

By Aircraft Type

| Commercial Aviation | Passenger Aircraft | Narrowbody Aircraft |

| Widebody Aircraft | ||

| Freighter | ||

| General Aviation | Business Jets | Large Jet |

| Mid-Size Jet | ||

| Light Jet | ||

| Helicopters | ||

| Others | ||

| Military Aviation | Fixed-Wing Aircraft | Multi-Role Aircraft |

| Training Aircraft | ||

| Transport Aircraft | ||

| Others | ||

| Rotorcraft | Multi-Mission Helicopter | |

| Transport Helicopter | ||

| Training | ||

By Propulsion Technology

| Turboprop |

| Turbofan |

| Piston Engine |

| Turboshaft |

| Others |

By End User

| Business and General Aviation Operators |

| Business and General Aviation Operators |

| Business and General Aviation Operators |

| By Aircraft Type | Commercial Aviation | Passenger Aircraft | Narrowbody Aircraft |

| Widebody Aircraft | |||

| Freighter | |||

| General Aviation | Business Jets | Large Jet | |

| Mid-Size Jet | |||

| Light Jet | |||

| Helicopters | |||

| Others | |||

| Military Aviation | Fixed-Wing Aircraft | Multi-Role Aircraft | |

| Training Aircraft | |||

| Transport Aircraft | |||

| Others | |||

| Rotorcraft | Multi-Mission Helicopter | ||

| Transport Helicopter | |||

| Training | |||

| By Propulsion Technology | Turboprop | ||

| Turbofan | |||

| Piston Engine | |||

| Turboshaft | |||

| Others | |||

| By End User | Business and General Aviation Operators | ||

| Business and General Aviation Operators | |||

| Business and General Aviation Operators | |||

Need A Different Region or Segment?

Customize Now

Market Definition

- Aircraft Type - All the aircraft related to commercial, military and general aviation have been included in this study

- Sub-Aircraft Type - Fixed-Wing passenger aircraft, freighter aircraft, business jets, piston fixed-wing aircraft, military fixed-wing aircraft, and rotorcraft are included under this study.

- Body Type - Body type includes all types of aircraft segmented based on application/size/capacity/role.

| Keyword | Definition |

|---|---|

| IATA | IATA stands for the International Air Transport Association, a trade organization composed of airlines around the world that has an influence over the commercial aspects of flight. |

| ICAO | ICAO stands for International Civil Aviation Organization, a specialized agency of the United Nations that supports aviation and navigation around the globe. |

| Air Operator Certificate (AOC) | A certificate granted by a National Aviation Authority permitting the conduct of commercial flying activities. |

| Certificate Of Airworthiness (CoA) | A Certificate Of Airworthiness (CoA) is issued for an aircraft by the civil aviation authority in the state in which the aircraft is registered. |

| Gross Domestic Product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| RPK (Revenue Passenger Kilometres) | The RPK of an airline is the sum of the products obtained by multiplying the number of revenue passengers carried on each flight stage by the stage distance - it is the total number of kilometers traveled by all revenue passengers. |

| Load Factor | The load factor is a metric used in the airline industry that measures the percentage of available seating capacity that has been filled with passengers. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| International Transportation Safety Association (ITSA) | International Transportation Safety Association (ITSA) is an international network of heads of independent safety investigation authorities (SIA). |

| Available Seats Kilometre (ASK) | This metric is calculated by multiplying Available Seats (AS) in one flight, defined above, multiplied by the distance flown. |

| Gross Weight | The fully-loaded weight of an aircraft, also known as “takeoff weight,” which includes the combined weight of passengers, cargo, and fuel. |

| Airworthiness | The ability of an aircraft, or other airborne equipment or system, to operate in flight and on the ground without significant hazard to aircrew, ground crew, passengers or to other third parties. |

| Airworthiness Standards | Detailed and comprehensive design and safety criteria applicable to the category of aeronautical product (aircraft, engine or propeller). |

| Fixed Base Operator (FBO) | A business or organization that operates at an airport. An FBO provides aircraft operating services like maintenance, fueling, flight training, charter services, hangaring, and parking. |

| High Net worth Individuals (HNWIs) | High Net worth Individuals (HNWIs) are individuals with over USD 1 million in liquid financial assets. |

| Ultra High Net worth Individuals (UHNWIs) | Ultra High Net worth Individuals (UHNWIs) are individuals with over USD 30 million in liquid financial assets. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| EASA (European Aviation Safety Agency) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| Airborne Warning and Control System (AW&C) aircraft | Airborne Warning and Control System (AEW&C) aircraft is equipped with a powerful radar and on-board command and control center to direct the armed forces. |

| The North Atlantic Treaty Organization (NATO) | The North Atlantic Treaty Organization (NATO), also called the North Atlantic Alliance, is an intergovernmental military alliance between 30 member states – 28 European and two North American. |

| Joint Strike Fighter (JSF) | Joint Strike Fighter (JSF) is a development and acquisition program intended to replace a wide range of existing fighter, strike, and ground attack aircraft for the United States, the United Kingdom, Italy, Canada, Australia, the Netherlands, Denmark, Norway, and formerly Turkey. |

| Light Combat Aircraft (LCA) | A light combat aircraft (LCA) is a light, multirole jet/turboprop military aircraft, commonly derived from advanced trainer designs, designed for engaging in light combat. |

| Stockholm International Peace Research Institute (SIPRI) | Stockholm International Peace Research Institute (SIPRI) is an international institute that provides data, analysis, and recommendations for armed conflict, military expenditure, and arms trade as well as disarmament and arms control. |

| Maritime Patrol Aircraft (MPA) | A maritime patrol aircraft (MPA), also known as maritime reconnaissance aircraft is a fixed-wing aircraft designed to operate for long durations over water in maritime patrol roles, in particular, anti-submarine warfare (ASW), anti-ship warfare (AShW), and search and rescue (SAR). |

| Mach Number | The Mach number is defined as the ratio of true airspeed to the speed of sound at the altitude of a given aircraft. |

| Stealth Aircraft | Stealth is a Common term applied to low observable (LO) technology and doctrine, that makes an aircraft near invisible to radar, infrared or visual detection. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF