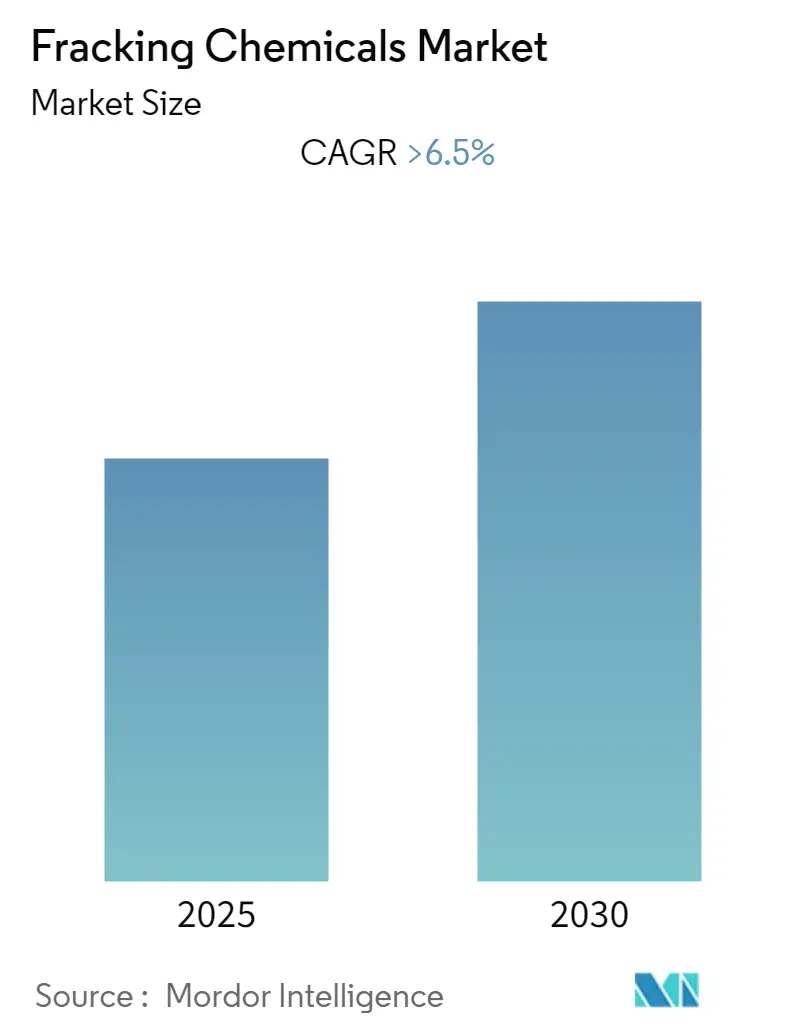

Fracking Chemicals Market Size

| Study Period | 2020 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 6.50 % |

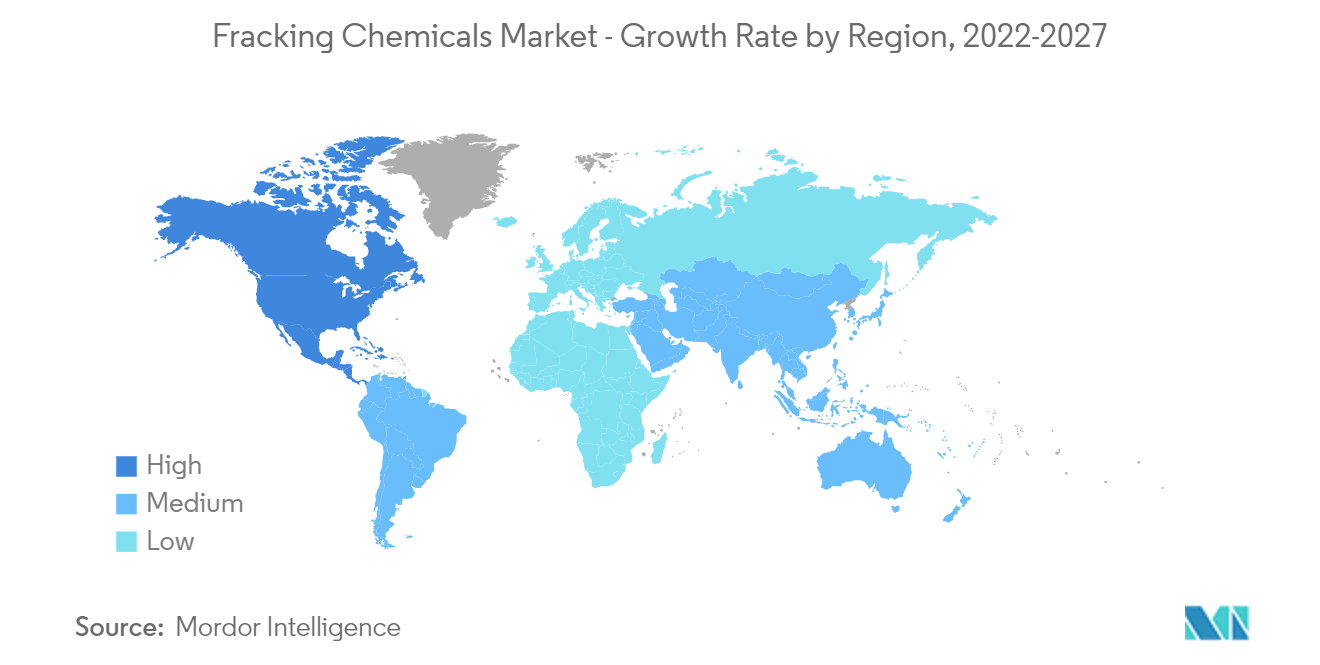

| Fastest Growing Market | North America |

| Largest Market | North America |

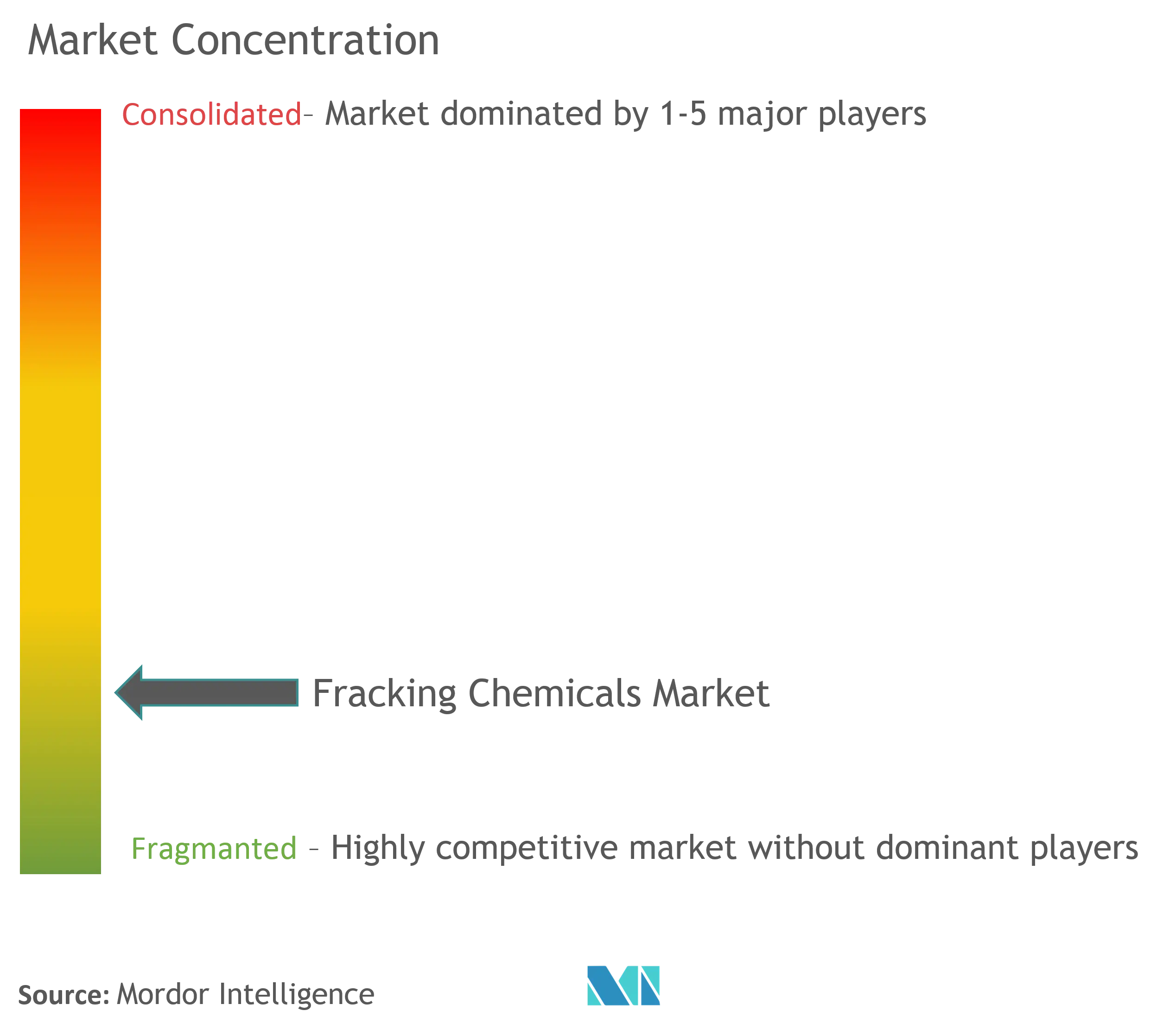

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Fracking Chemicals Market Analysis

The Fracking Chemicals Market is expected to register a CAGR of greater than 6.5% during the forecast period.

The horizontal or drilling segment is expected to grow at the fastest rate during the forecast period due to the increased number of horizontally drilled wells in many countries.

The new alternative fracking technologies, such as waterless fracking, the introduction of green chemicals, propane gel, and other technologies, are expected to create tremendous growth opportunities in the future.

The North American region is expected to dominate the market during the forecast period due to the high share of unconventional oil and gas production in petroleum production in the United States and Canada.

Fracking Chemicals Market Trends

This section covers the major market trends shaping the Fracking Chemicals Market according to our research experts:

Horizontal or Directional Segment Expected to Witness Significant Growth

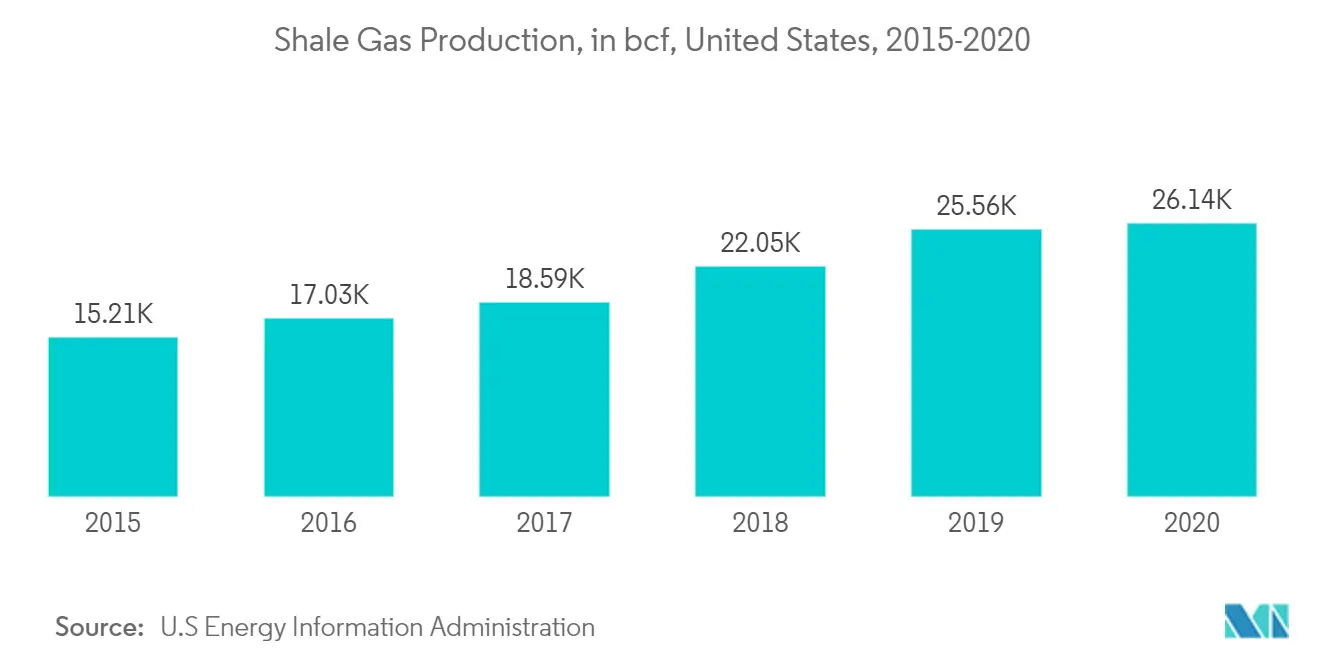

Horizontal drilling is a technique in which drilling is done at an at least 80 degrees angular direction to the vertical wellbore. The technique involves hydraulic fracturing to extract oil or gas deposits, a process in which fracking fluid is injected at high pressure toward difficult rock formations. The process is generally carried out in the case of unconventional petroleum resources.

The process became a widely used technique, particularly after the US shale gas boom, when hydraulic fracturing became an indispensable part of gas extraction from tight unconventional resources. The shale gas production in the United States reached 26,139 billion cubic feet in 2020, an increase of around 70% over the last five years.

Furthermore, in other parts of the world too, unconventional petroleum production is expected to get a spike over the coming years. For example, in January 2022, CNOOC, China's veteran oil and gas industry player, announced plans to increase domestic unconventional oil and gas production in 2022. The domestic sources include three unconventional coal bed methane and tight gas projects, with a total peak output of 18,100 boe/d or 3.05 Mcm/day.

In November 2021, Saudi Aramco announced the commencement of the development of the Jafurah unconventional gas field, the largest non-associated gas field in Saudi Arabia with shale gas resources. The field is expected to commence production in 2025, with 200 million standard cubic feet per day (scfd).

Owing to such developments, the horizontal drilling segment is expected to get major opportunities in the near future.

North America Expected to Dominate the Market

The North American region is likely to continue as the largest market in the fracking chemicals industry due to the increased demand for crude oil and LNG, which is ultimately likely to be reflected in a high rate of petroleum production in the United States and Canada.

In the United States, tight oil production accounted for a significant share of the overall crude production in 2020, specifically from the prominent unconventional oil and gas players like Eagle Ford, Spraberry, Bakken, Wolfcamp, Woodford, etc. According to the US Energy Information Administration, crude oil production is expected to reach record-high levels in the country by 2023, reaching a forecast of 12.6 million barrels per day (b/d). The Permian Basin, which has a significant share of unconventional resources, is expected to steer the overall US crude oil production growth.

Furthermore, the US government invested around USD 20 billion annually toward boosting the value of new oil and gas projects in the last two decades, which increased companies' expected profits during the shale booms in the Bakken Formation, Haynesville Shale and Appalachian, Eagle Ford, and Permian Basins. Such initiatives by the government are expected to attract more private investments for production.

In January 2022, the Canadian Association of Petroleum Producers (CAPP) forecast a 22% increase in natural gas and oil investment in 2022 due to the increased global demand for oil and gas. The growth in oil sands investment (unconventional) in Canada is forecast to increase by around 33% to USD 11.6 billion in 2022 as compared to USD 8.7 billion in 2021.

Such developments are likely to make the region the largest market for the fracking chemicals industry.

Fracking Chemicals Industry Overview

The fracking chemicals market is moderately fragmented. Some of the key players include Dow Chemical Company, Parchem Fine & Specialty Chemicals, Flotek Industries Inc., BASF SE, and Solvay SA, among others.

Fracking Chemicals Market Leaders

-

The Dow Chemical Company

-

Parchem Fine and Specialty Chemicals Inc.

-

Flotek Industries Inc.

-

BASF SE

-

Solvay SA

*Disclaimer: Major Players sorted in no particular order

Fracking Chemicals Market News

In March 2021, Exxon Mobil submitted a proposal to the Colombian government for conducting a hydraulic fracturing pilot project in the country. The Platero Project includes fracking investigations in the Valle Medio del Magdalena basin, Colombia.

Fracking activity in Vaca Muerta increased by more than 55% month-on-month in November 2020. The number of fracturing stages in the play rose to 545 in November 2020 from 345 in October 2020. These numbers are similar to November 2019, which is an indication that shale production might return to pre-COVID levels.

Fracking Chemicals Market Report - Table of Contents

1. INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD billion, till 2027

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.2 Restraints

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitute Products and Services

4.7.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

5.1 Fluid Type

5.1.1 Water-based Fluid

5.1.2 Foam-based Fluid

5.1.3 Other Fluid Types

5.2 Well Type

5.2.1 Vertical

5.2.2 Horizontal or Directional

5.3 Geography

5.3.1 North America

5.3.2 Europe

5.3.3 Asia-Pacific

5.3.4 South America

5.3.5 Middle-East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 The Dow Chemical Company

6.3.2 Parchem Fine and Specialty Chemicals Inc.

6.3.3 Halliburton Company

6.3.4 Baltimore Aircoil Company

6.3.5 Solvay SA

6.3.6 SNF Group

6.3.7 DuPont de Nemours Inc.

6.3.8 BASF SE

6.3.9 Flotek Industries Inc.

6.3.10 CES Energy Solutions Corp.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Fracking Chemicals Industry Segmentation

The fracking chemicals market report includes:

| Fluid Type | |

| Water-based Fluid | |

| Foam-based Fluid | |

| Other Fluid Types |

| Well Type | |

| Vertical | |

| Horizontal or Directional |

| Geography | |

| North America | |

| Europe | |

| Asia-Pacific | |

| South America | |

| Middle-East and Africa |

Fracking Chemicals Market Research FAQs

What is the current Fracking Chemicals Market size?

The Fracking Chemicals Market is projected to register a CAGR of greater than 6.5% during the forecast period (2025-2030)

Who are the key players in Fracking Chemicals Market?

The Dow Chemical Company, Parchem Fine and Specialty Chemicals Inc., Flotek Industries Inc., BASF SE and Solvay SA are the major companies operating in the Fracking Chemicals Market.

Which is the fastest growing region in Fracking Chemicals Market?

North America is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Fracking Chemicals Market?

In 2025, the North America accounts for the largest market share in Fracking Chemicals Market.

What years does this Fracking Chemicals Market cover?

The report covers the Fracking Chemicals Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Fracking Chemicals Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Fracking Chemicals Industry Report

Statistics for the 2025 Fracking Chemicals market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Fracking Chemicals analysis includes a market forecast outlook for 2025 to 2030 and historical overview. Get a sample of this industry analysis as a free report PDF download.

Fracking Chemicals Market Report Snapshots