Foot And Mouth Disease Vaccines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.07 Billion |

| Market Size (2031) | USD 4.29 Billion |

| Growth Rate (2026 - 2031) | 6.94% CAGR |

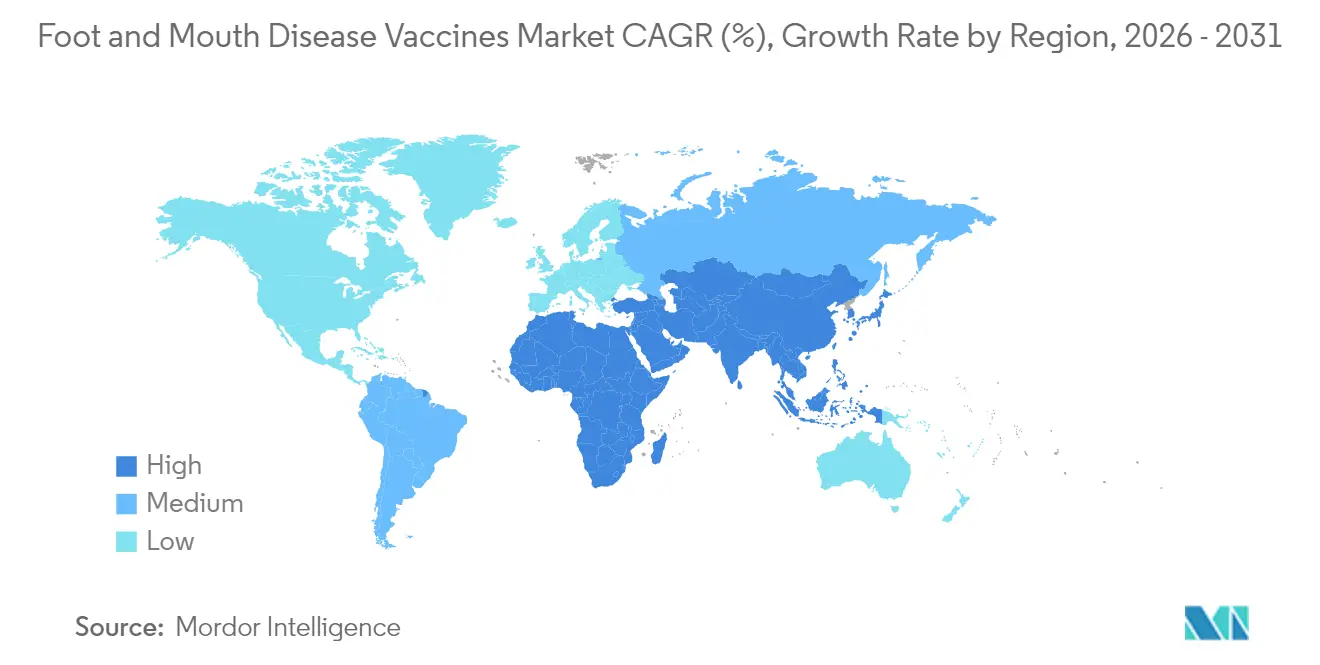

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Foot And Mouth Disease Vaccines Market Analysis by Mordor Intelligence

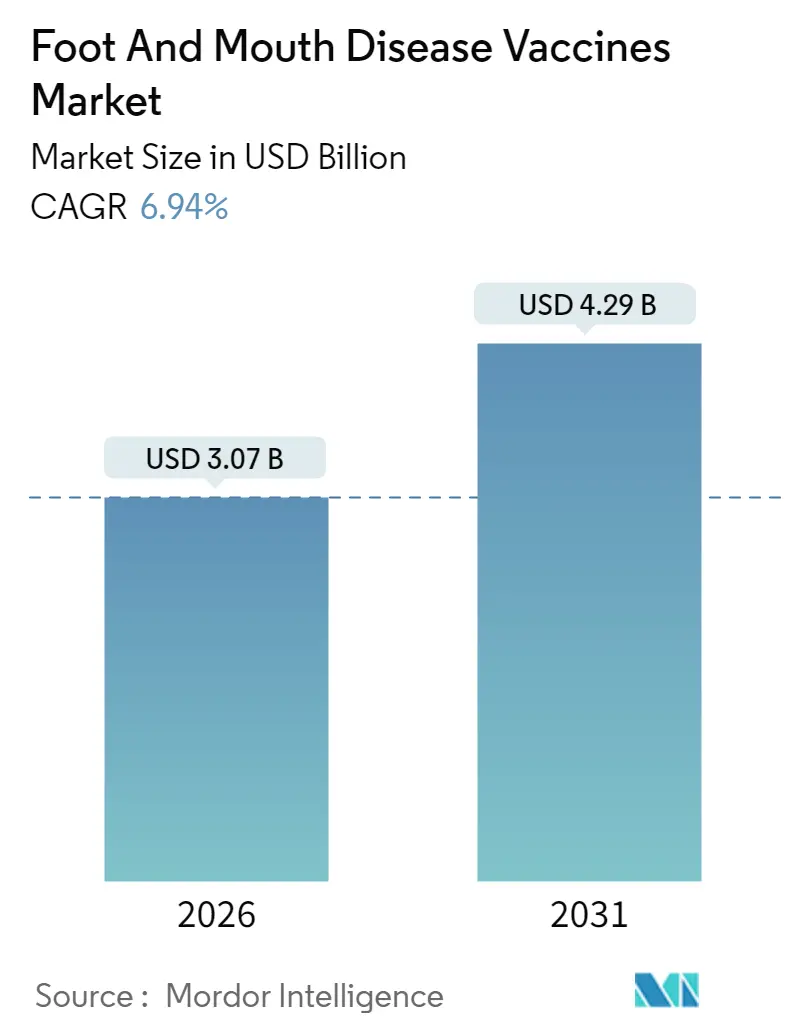

The foot and mouth disease vaccines market was valued at USD 2.87 billion in 2025 and estimated to grow from USD 3.07 billion in 2026 to reach USD 4.29 billion by 2031, at a CAGR of 6.94% during the forecast period (2026-2031). Strong demand reflects the move from reactive outbreak control toward routine preventive immunization as climate change pushes the virus into once-temperate zones. Intensified livestock trade, new government vaccine banks, and the wider use of DIVA technologies are reinforcing predictable procurement cycles that favor volume manufacturing. Regional antigen banks in Asia-Pacific and the Middle East are streamlining bulk purchases, while subcutaneous delivery formats improve farmer compliance and reduce animal stress. Supply-chain constraints around cold storage and surge capacity remain the main brakes on growth, especially in remote regions of Africa and South America.

Key Report Takeaways

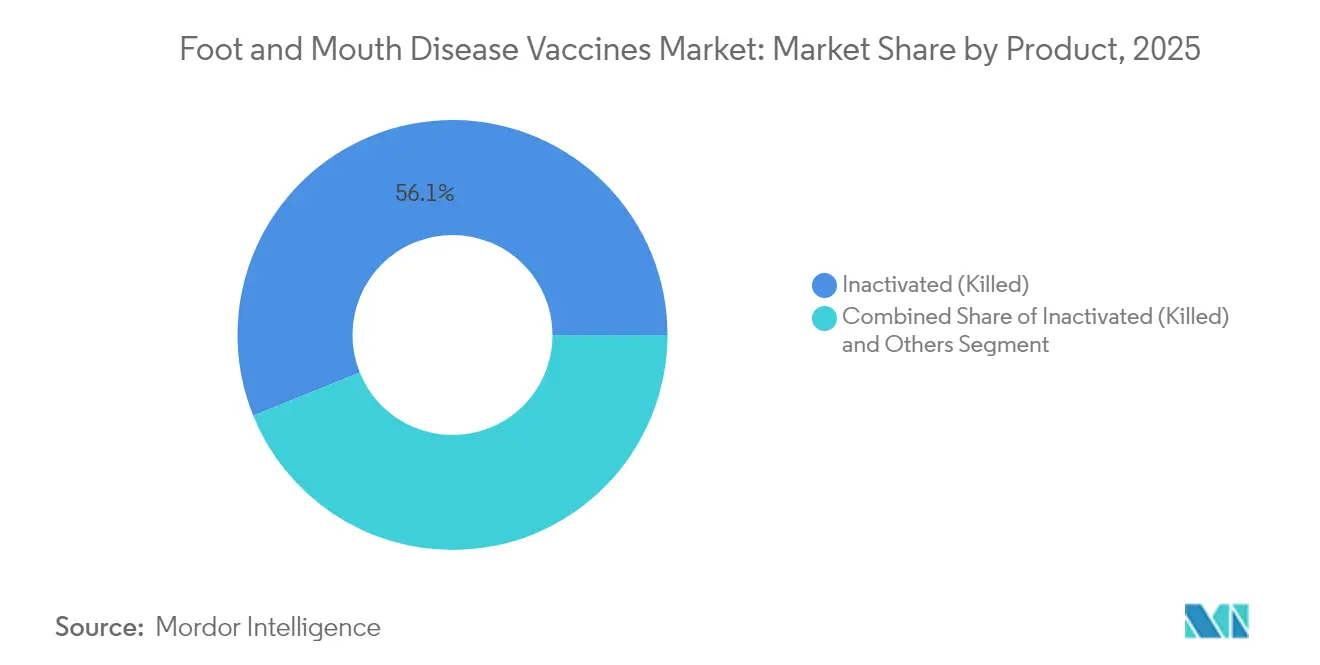

- By product type, inactivated formulations led with 56.12% revenue share in 2025; modified/attenuated live vaccines are forecast to expand at a 7.64% CAGR through 2031.

- By route of administration, intramuscular delivery held 75.96% of the foot and mouth disease vaccines market share in 2025, while subcutaneous methods post the highest growth at 7.72% CAGR.

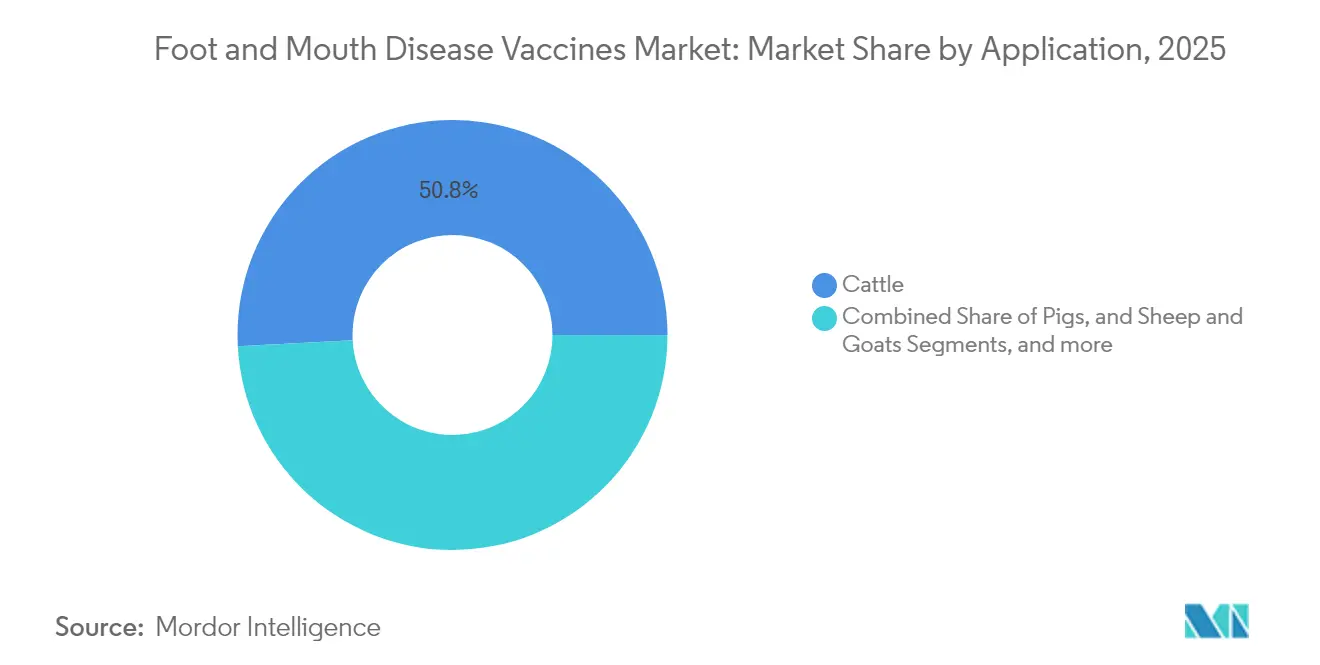

- By animal type, cattle vaccines commanded 50.84% of the foot and mouth disease vaccines market size in 2025; pig vaccines register the fastest growth at 7.31% CAGR to 2031.

- By distribution channel, veterinary hospitals and clinics controlled 59.02% share in 2025, whereas government institutions record a 7.51% CAGR over the forecast period.

- By geography, Asia-Pacific captured 49.96% of 2025 revenues; the Middle East & Africa region is set to grow at an 7.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Foot And Mouth Disease Vaccines Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising transboundary & zoonotic outbreaks | +1.2% | Global, with acute impact in Europe and Middle East | Short term (≤ 2 years) |

| Growing demand for animal-protein & livestock herd size | +1.8% | Asia-Pacific core, spill-over to MEA and South America | Medium term (2-4 years) |

| Government-funded vaccination programs & mandates | +1.5% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Trade-friendly DIVA/recombinant vaccine roll-outs | +0.9% | Global, with priority in export-dependent regions | Long term (≥ 4 years) |

| Regional antigen banks securing bulk procurement | +0.7% | Regional hubs in APAC, MEA, and South America | Long term (≥ 4 years) |

| Climate-driven FMD migration into temperate zones | +1.1% | Europe, North America, and temperate APAC regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Transboundary & Zoonotic Outbreaks

The January 2025 case in Germany, the country’s first since 1988, triggered import bans across five continents and proved that a single incursion can shut billion-dollar trade channels [1]United States Department of Agriculture, "Germany: First Outbreak of Foot-and-Mouth-Disease in Germany since 1988," fas.usda.gov. Molecular tracing showed the SAT2 XIV topotype arriving from East Africa, underscoring how modern logistics erase historical barriers. Libya’s 2024 losses, where delayed vaccine arrival decimated Misrata herds, highlighted the cost of reactive strategies. Neighboring Austria responded by closing multiple border posts, signaling that containment now relies on regional vaccination readiness rather than local quarantine alone. Climate-linked shifts that lengthen viral survival in cooler zones suggest that preventive vaccination in once-free areas will continue to enlarge the foot and mouth disease vaccines market.

Growing Demand for Animal-Protein & Herd Size

Expanding middle-class diets in Asia and Africa increase the economic risk of FMD, compelling authorities to safeguard production. East Africa houses 40% of the continent’s livestock, yet routine coverage is under 15%, a gap now targeted by the USD 17.68 million AgResults quadrivalent program that boosts six-month immunity. China’s dairy expansion, with 6.05% BVDV positivity across 13 provinces, mirrors similar scale-up imperatives where vaccination becomes foundational to export licensing [2]Yangyang Xiao, "Prevalence and genetic characterization of bovine viral diarrhea virus in dairy cattle in northern China," BMC Veterinary Research, bmcvetres.biomedcentral.com. South Africa’s 2024 campaign vaccinated 634,000 cattle, showing how food-security mandates are turning sporadic inoculations into annual routines. Export premiums enjoyed by FMD-free nations prove that vaccination outlays pay for themselves via price uplift, ensuring capital flows back into wider coverage programs.

Government-Funded Vaccination Programs & Mandates

Public procurement is reshaping demand predictability. Canada’s USD 57.5 million national vaccine bank adds dedicated inventory beyond the existing North American facility, assuring domestic stock on demand [3]Canadian Food Inspection Agency, “Establishing a National FMD Vaccine Bank,” inspection.canada.ca . The USDA’s USD 27.1 million countermeasures bank follows the same logic, emphasizing readiness while preserving inter-state livestock movements during outbreaks. Zambia’s World Bank-backed USD 50 million Livestock Development Project likewise embeds annual campaigns into its policy framework. Centralized buying reduces per-dose costs, rewards GMP-compliant suppliers, and incentivizes new capacity, reinforcing the global expansion of the foot and mouth disease vaccines market.

Trade-Friendly DIVA and Recombinant Vaccine Roll-outs

DIVA platforms resolve the trade dilemma by allowing serological distinction between infected and vaccinated herds, so exporting countries can vaccinate without forfeiting disease-free status. In East Africa, new DIVA products offer a pathway to replicate Brazil’s export success once regional freedom is certified. Recombinant vaccine technology shrinks strain-match timelines and curtails antigenic drift obsolescence, an edge demonstrated by isoprinosine-adjuvanted formulations that achieved 100% efficacy in challenge studies. As sanitary rules tighten in trade agreements, such innovations become indispensable growth drivers.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold-chain & storage cost burden | -1.4% | Sub-Saharan Africa, rural Asia, remote South America | Medium term (2-4 years) |

| Serotype-matching regulatory delays | -0.8% | Global, with acute impact in multi-serotype regions | Short term (≤ 2 years) |

| Antigenic drift causing inventory obsolescence | -0.6% | Endemic regions with high viral circulation | Medium term (2-4 years) |

| Limited surge capacity for high-potency vaccines | -0.9% | Global, particularly during concurrent outbreaks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cold-Chain & Storage Cost Burden

Maintaining 2-8 °C integrity is difficult where power grids are unreliable. Trials in Nepal found that temperature excursions cut potency and that bulky coolers hamper last-mile transport. FAO guidelines reiterate that cold-chain failure is the chief reason rural campaigns underperform. Freeze-drying can solve this, but current costs limit adoption in price-sensitive markets despite research showing 3-6% moisture content retains infectivity. As only 5% of cattle in sub-Saharan Africa receive systematic vaccination against 146.1% coverage in South America, cold-chain gaps materially restrict the foot and mouth disease vaccines market.

Serotype-Matching Regulatory Delays

FMD has seven serotypes and dozens of regional topotypes. When the SAT2 XIV strain reached the Middle East, manufacturers needed new seed virus in weeks, yet approval took months, leaving stocks mismatched. Multi-valent formulations meet biological complexity but face longer review cycles than monovalent doses. Although WOAH is promoting harmonization, many authorities still insist on domestic trials, stretching timelines and keeping inferior products in circulation. This drag erodes farmer confidence and slows adoption.

Segment Analysis

By Product: Modified Live Vaccines Drive Innovation

The segment generated 56.12% of 2025 revenue from inactivated formulations, yet modified live platforms are forecast to rise 7.64% annually. The rise stems from stronger, longer-lasting immunity and the growing availability of DIVA-compliant attenuated strains. Next-generation adjuvants reduce adverse reactions while improving both humoral and cellular responses, positioning live vaccines as the preferred choice in regions confronting emergent serotypes. In contrast, inactivated doses rely on mature regulatory pathways but face waste risk when antigenic drift outpaces production cycles. Emerging mRNA and recombinant protein methods promise rapid strain updates and could redefine the foot and mouth disease vaccines market over the next decade.

Second-generation products link formulation with route efficiency. Freeze-dried pellets, oil emulsion stabilizers, and nanoparticle carriers are under study to extend shelf life and minimize cold-chain reliance, directly addressing high-growth but infrastructure-poor geographies. Manufacturers able to balance potency, stability, and DIVA compatibility stand to capture an outsized share of the expanding foot and mouth disease vaccines market.

Note: Segment shares of all individual segments available upon report purchase

By Route of Administration: Subcutaneous Gains Momentum

Intramuscular injection remained dominant with 75.96% revenue share in 2025, securing the largest slice of the foot and mouth disease vaccines market size for delivery technologies. Nevertheless, subcutaneous delivery is rising at 7.72% CAGR as it requires less precision, lowers carcass blemish risk, and aligns with welfare regulations. Long-acting subcutaneous depots could soon halve dosing frequency, driving compliance in pastoral systems where veterinary visits are sporadic.

Formulation customizations for subcutaneous use include modified emulsion viscosities and higher antigen loads to compensate for slower uptake. Companies that tailor vaccines for both routes can appeal to large commercial feedlots prioritizing speed as well as smallholder farmers needing flexible techniques, broadening total addressable volumes within the foot and mouth disease vaccines market.

By Animal Type: Pig Vaccination Accelerates

Cattle vaccines accounted for 50.84% of 2025 revenues, continuing to anchor the foot and mouth disease vaccines market. Yet pig vaccines are moving faster, supported by 7.31% CAGR as vertically integrated pork supply chains tighten biosecurity to protect export licenses. Swine producers view vaccination as an insurance premium after recent African swine fever disruptions, with China’s import demand amplifying pressure for certification compliance.

Sheep, goats, and water buffalo represent nascent subsegments. Water buffalo were prominent during Germany’s 2025 case, a reminder that changing herd compositions can redirect vaccine demand. Multi-pathogen combination studies, such as PRRSV-PCV2 bivalent formulations, hint at future FMD combos that may further grow the foot and mouth disease vaccines industry by bundling value for producers.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Government Procurement Surges

Veterinary hospitals and clinics maintained 59.02% share in 2025, but public procurement posts a faster 7.51% CAGR as states formalize preventive schemes. National vaccine banks in Canada and the United States enable bulk purchase contracts that smooth production planning for suppliers. Community animal-health workers extend reach into pastoral belts, addressing service gaps highlighted in Ethiopian field studies where only 10-15% of cattle had prior coverage.

Cooperative buying by large agribusinesses and direct manufacturer-to-farm models form the “other” channel, leveraging digital ordering platforms that shorten delivery windows. As governments set reference prices, private channels may pivot to value-added services such as cold-chain rental, sustaining a dual-track dynamic inside the foot and mouth disease vaccines market.

Geography Analysis

Asia-Pacific held 49.96% of the foot and mouth disease vaccines market in 2025. China’s dairy provinces, where 6.05% of tested herds showed BVDV antibodies, signal how intensification fuels vaccination budgets. India’s Haryana surveillance recorded 5.3% NSP seroreactors, yet high protective titers against serotypes O, A, and Asia-1 point to program effectiveness. Indonesia’s receipt of 4 million doses from Australia demonstrates cross-border cooperation to stabilize supply. Although coverage is nearing saturation in tier-one producers, growth continues in emerging Southeast Asian economies shifting toward export-oriented livestock models.

The Middle East & Africa region leads growth at an 7.78% CAGR. Libya’s 2024 losses emphasized vulnerability when vaccine shipments lag demand. South Africa’s campaign that vaccinated 634,000 cattle, including 97,000 in Eastern Cape, illustrates the pivot from selective to blanket immunization. Eastern Africa’s AgResults project is developing quadrivalent doses that secure six-month immunity, closing performance gaps that previously discouraged farmer uptake. Ethiopia’s large but under-served herd underscores latent volume that could materialize if cold-chain financing and regulatory fast-tracking improve.

South America shows mature penetration but faces climate-driven threats to disease-free status. Brazil’s experience proves vaccination can unlock exports; yet shifting weather patterns may re-introduce risk, renewing demand. North American and European markets, once considered post-FMD, have acknowledged new exposure. Germany’s 2025 case and Canada’s subsequent USD 57.5 million bank reveal how temperate regions are adding proactive capacity. The geographic redistribution of risk is enlarging the overall foot and mouth disease vaccines market beyond its historical endemic base.

Competitive Landscape

The market is moderately fragmented. Multinationals such as Zoetis, Merck Animal Health, and Boehringer Ingelheim leverage vertically integrated R&D, GMP plants, and global channels, yet regional manufacturers gain share by customizing strains and forming government alliances. Zoetis sold non-core medicated feed assets for USD 350 million to focus on biologics, illustrating portfolio tightening. Merck’s USD 895 million expansion in Kansas adds high-potency production that will boost global supply.

Technology is a prime differentiator. Boehringer Ingelheim’s takeover of Saiba Animal Health adds virus-like particle expertise that can accelerate strain matching. Regional champions in Botswana, India, and Argentina are building cGMP sites to meet state procurement standards, aligning with the shift to centralized vaccine banks. Conditional licensing pathways at USDA APHIS favor companies with surge capacity, creating a premium on idle but validated lines ready for emergency runs.

New entrants exploring mRNA formulations promise 60-day concept-to-batch timelines. If regulatory harmonization keeps pace, such platforms could undercut legacy lead times and raise competitive pressure. Cold-chain service providers may also gain relevance as logisticians partner with manufacturers to de-risk last-mile delivery, reinforcing integration trends inside the foot and mouth disease vaccines industry.

Foot And Mouth Disease Vaccines Industry Leaders

-

Biogénesis Bagó

-

Boehringer Ingelheim GmbH

-

VECOL S.A

-

VETAL Animal Health Products

-

Merck & Co. Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Canada awarded Boehringer Ingelheim and Biogénesis Bagó contracts to supply multiple FMD vaccine types for the country’s first dedicated vaccine bank.

- June 2025: South Africa expanded inoculations and built additional stocks to curb a growing outbreak.

- May 2025: Merck Animal Health committed USD 895 million to enlarge vaccine manufacturing and R&D capacity in De Soto, Kansas, with significant allocations for FMD formulations.

- January 2025: Indonesia initiated a nationwide vaccination program after FMD spread to 11 provinces, infecting thousands of animals.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the foot-and-mouth disease vaccines market as all prophylactic and emergency biologics targeting serotypes O, A, C, Asia-1, and SAT 1-3 for cloven-hoofed livestock, valued at ex-factory prices and tracked through formal channels worldwide.

Scope exclusions include diagnostic kits, antivirals, wildlife bait vaccines, and informal barter trades that are not sized.

Segmentation Overview

-

By Product

- Modified/ Attenuated Live

- Inactivated (Killed)

- Others

-

By Route of Administration

- Intramuscular

- Subcutaneous

-

By Animal Type

- Cattle

- Pigs

- Sheep & Goats

- Others

-

By Distribution Channel

- Veterinary Hospitals and Clinics

- Government Institutions

- Others

-

By Geography

-

Asia-Pacific

- China

- India

- South Korea

- Rest of APAC

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

- Rest of the World

-

Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Interviews with formulators, provincial animal-health officers, and cold-chain distributors across Asia, Latin America, and Africa let us verify selling prices, campaign seasonality, and wastage; insight desk work alone could not yield.

Desk Research

We built our baseline from WOAH outbreak logs, FAO herd tables, UN Comtrade antigen codes, and peer-reviewed potency studies; then we enriched it with company 10-Ks, tender notices, and veterinary association bulletins. Mordor analysts also tapped D&B Hoovers for producer splits and Volza for oil-emulsion shipment tallies.

Government vaccination budgets, patent filings for DIVA platforms, and regional cattle-to-pig ratios rounded assumptions. The sources named are illustrative; many additional references informed validation.

Market-Sizing & Forecasting

We estimated demand through a top-down "dose requirement" pool built from susceptible herd counts, coverage rates, and multivalent-dose frequency; then we cross-checked it with sampled supplier roll-ups (capacity x utilization x ASP). Key variables include outbreak incidence, public program spend, antigen-bank reserves, oil-adjuvant adoption, and average three-dose regimens. A multivariate regression using lagged outbreaks and protein-consumption growth drives 2025-2030 projections, while bottom-up channel checks anchor near-term variance.

Data Validation & Update Cycle

Models face peer review, anomaly checks against fresh WOAH briefs and pricing decks, and refresh annually; interim updates trigger when large outbreaks or policy shifts alter a core input.

Why Mordor's Foot and Mouth Disease Vaccines Market Baseline Commands Dependability

Published estimates diverge because firms choose different scopes, price anchors, and refresh cadences. External releases peg the 2024-2025 market between USD 1.82 billion and USD 3.15 billion.

Main gaps arise when emergency antigen banks are skipped, partially FMD-free regions are discounted, or dose-to-revenue conversions omit regional ASP lift. Mordor's model covers every commercial formulation globally and refreshes yearly, whereas others often freeze inputs longer or track only conventional shots.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.87 bn (2025) | Mordor Intelligence | - |

| USD 1.82 bn (2024) | Regional Consultancy A | narrow product and geography scope |

| USD 2.42 bn (2024) | Global Consultancy B | lower ASP, omits smallholder tenders |

| USD 3.15 bn (2025) | Industry Association C | folds wider ruminant biologics |

Our USD 2.87 billion baseline comes from the latest Mordor Intelligence study. The disciplined scope, live variables, and yearly refresh give decision-makers a transparent, repeatable benchmark.

Key Questions Answered in the Report

What is the current size of the foot and mouth disease vaccines market?

The market stands at USD 3.07 billion in 2026 and is projected to reach USD 4.29 billion by 2031.

Which region commands the largest market share?

Asia-Pacific leads with 49.96% of global revenue in 2025.

Which vaccine type is growing the fastest?

Modified or attenuated live vaccines are advancing at a 7.64% CAGR through 2031.

Why are government institutions becoming a major distribution channel?

National vaccine banks and compulsory immunization programs create steady bulk orders, giving this channel a 7.51% forecast CAGR.

How do DIVA-compatible vaccines benefit exporting countries?

They let authorities vaccinate herds yet still prove disease-free status, keeping trade routes open.

What operational challenge most limits uptake in rural markets?

Weak cold-chain infrastructure undermines vaccine potency and slows adoption, especially in sub-Saharan Africa and remote Asia.