Food Waste Disposers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

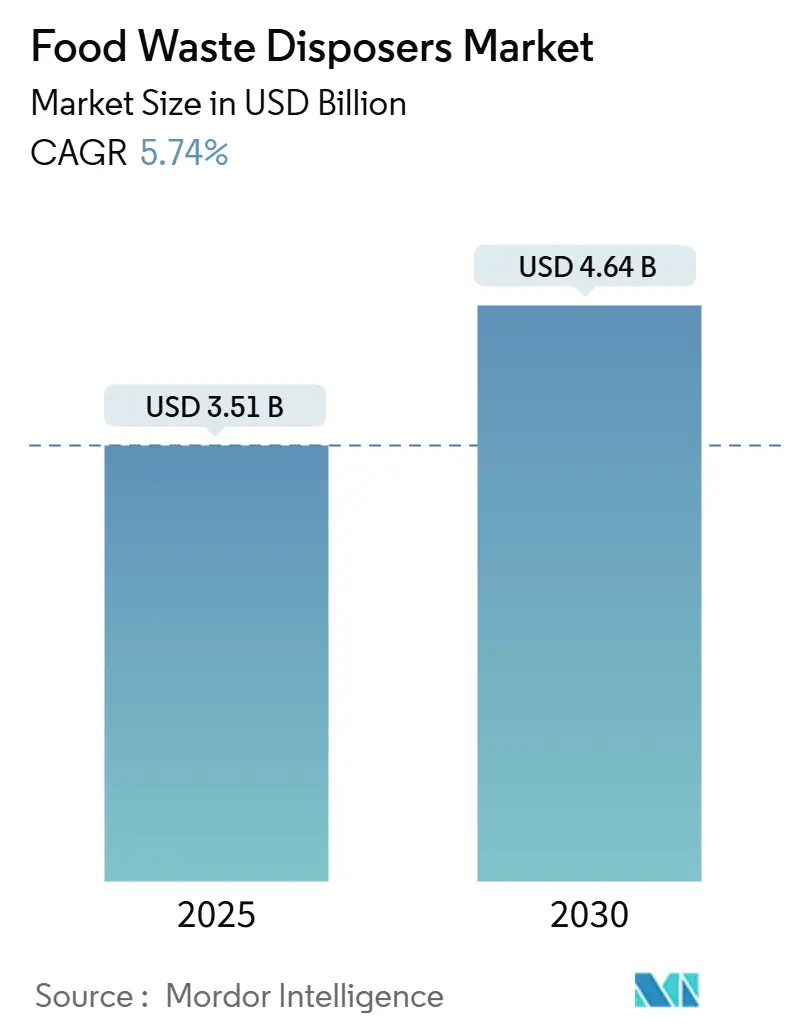

| Market Size (2025) | USD 3.51 Billion |

| Market Size (2030) | USD 4.64 Billion |

| Growth Rate (2025 - 2030) | 5.74% CAGR |

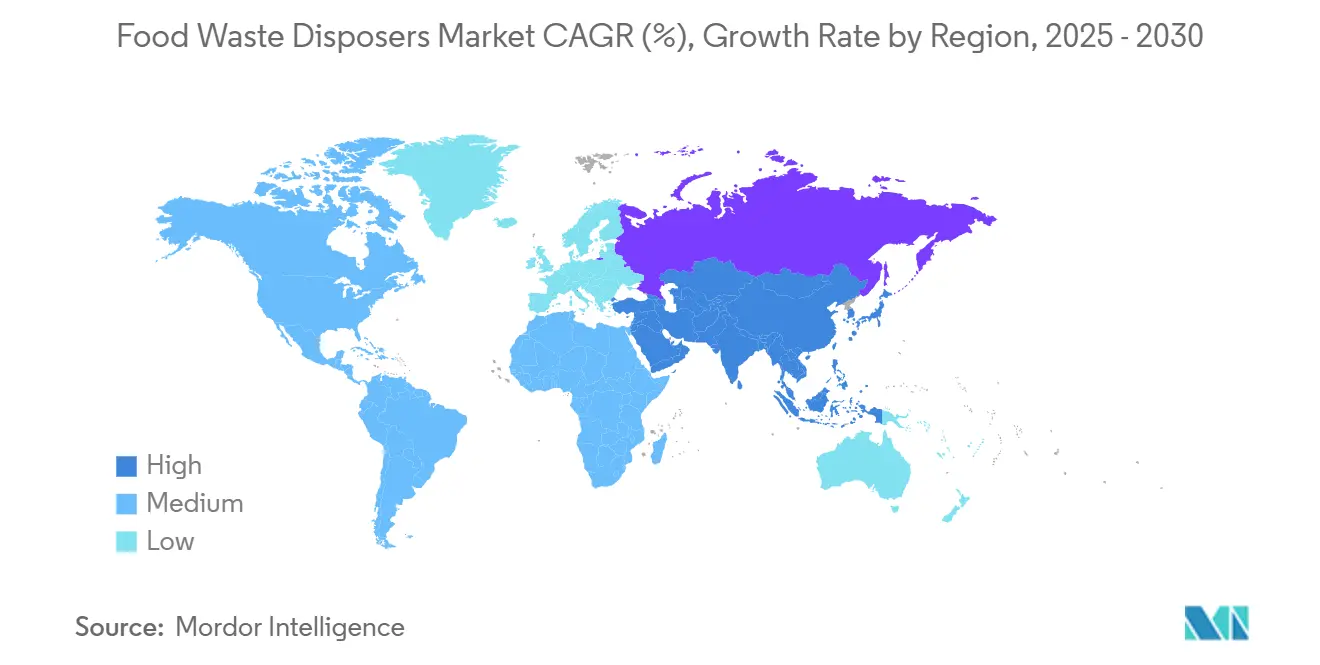

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

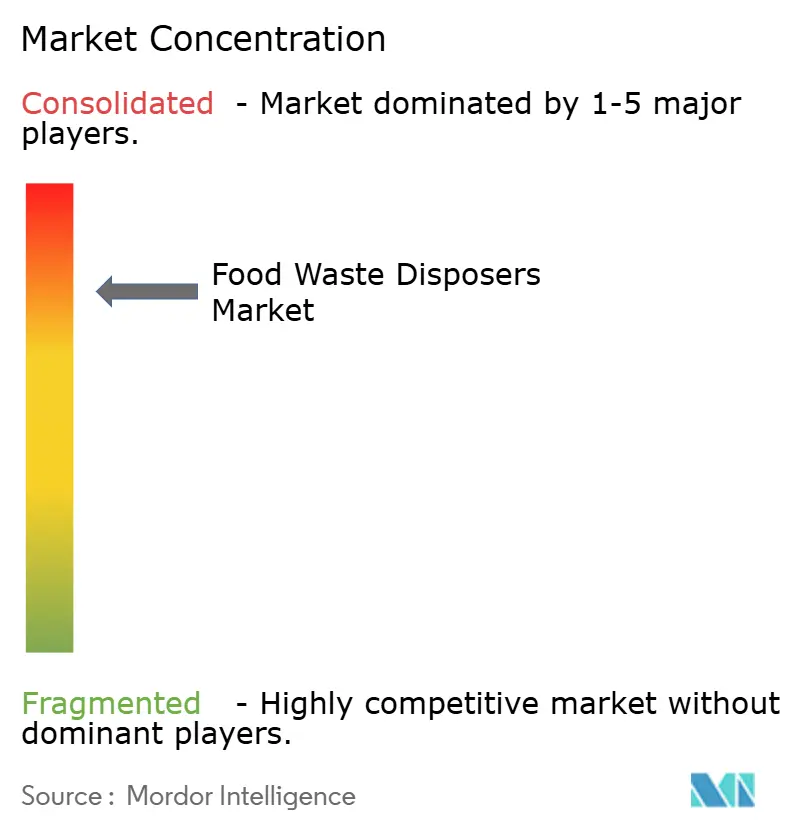

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food Waste Disposers Market Analysis by Mordor Intelligence

The food waste disposers market stood at USD 3.51 billion in 2025 and is forecast to reach USD 4.64 billion by 2030, registering a 5.74% CAGR during the forecast horizon. Stringent landfill-diversion mandates, the steady rollout of municipal anaerobic-digestion capacity, and rising consumer demand for connected kitchen appliances are reinforcing a multiyear growth runway for the food waste disposers market. The California SB 1383 framework has become a template for other jurisdictions, accelerating adoption cycles and shortening payback periods for disposer investments. Technology shifts—particularly MultiGrind cutters, torque-managed permanent-magnet motors, and real-time IoT telemetry—help vendors defend margin while converting latent demand into installed base. Additionally, drought-prone regions now reward water-saving impellers, linking disposer uptake with broader resource-efficiency goals that were once viewed in isolation.

Key Report Takeaways

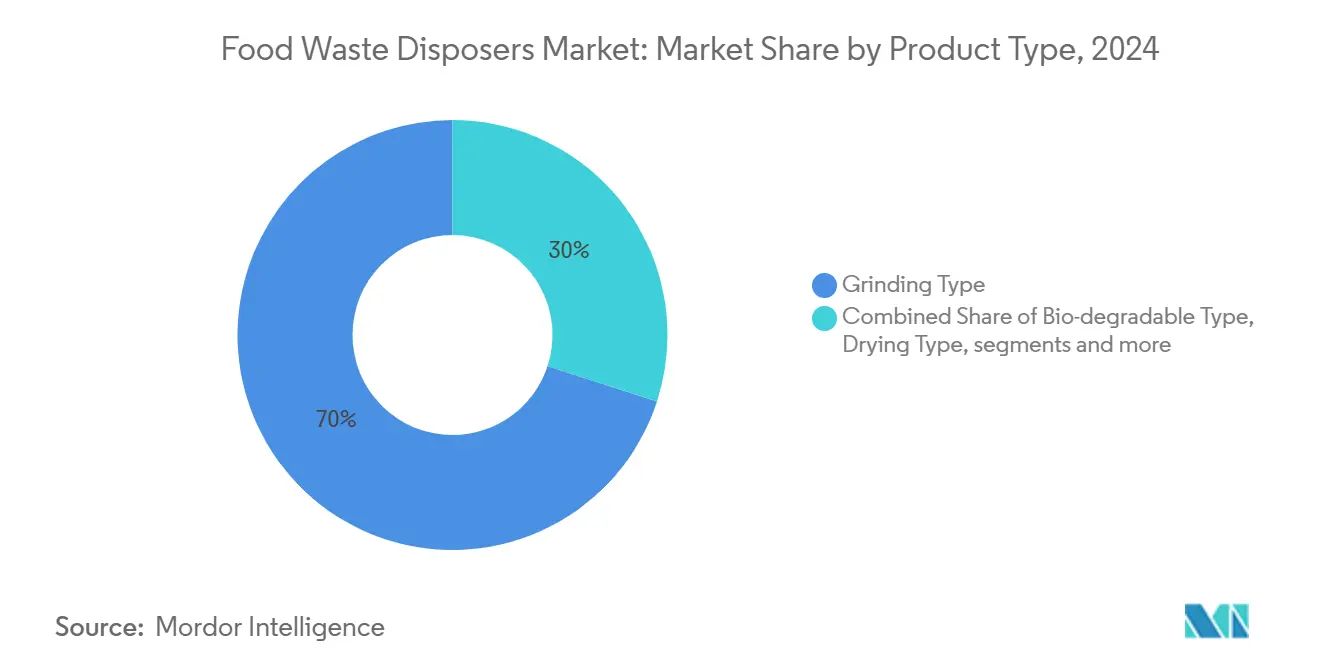

- By product type, grinding units contributed 70.00% revenue of the food waste disposers market in 2024; bio-degradable alternatives are expanding at a 7.60% CAGR toward 2030.

- By feed type, continuous-feed models represented 55.00% of the food waste disposers market size in 2024, with batch-feed units advancing at a 6.70% CAGR.

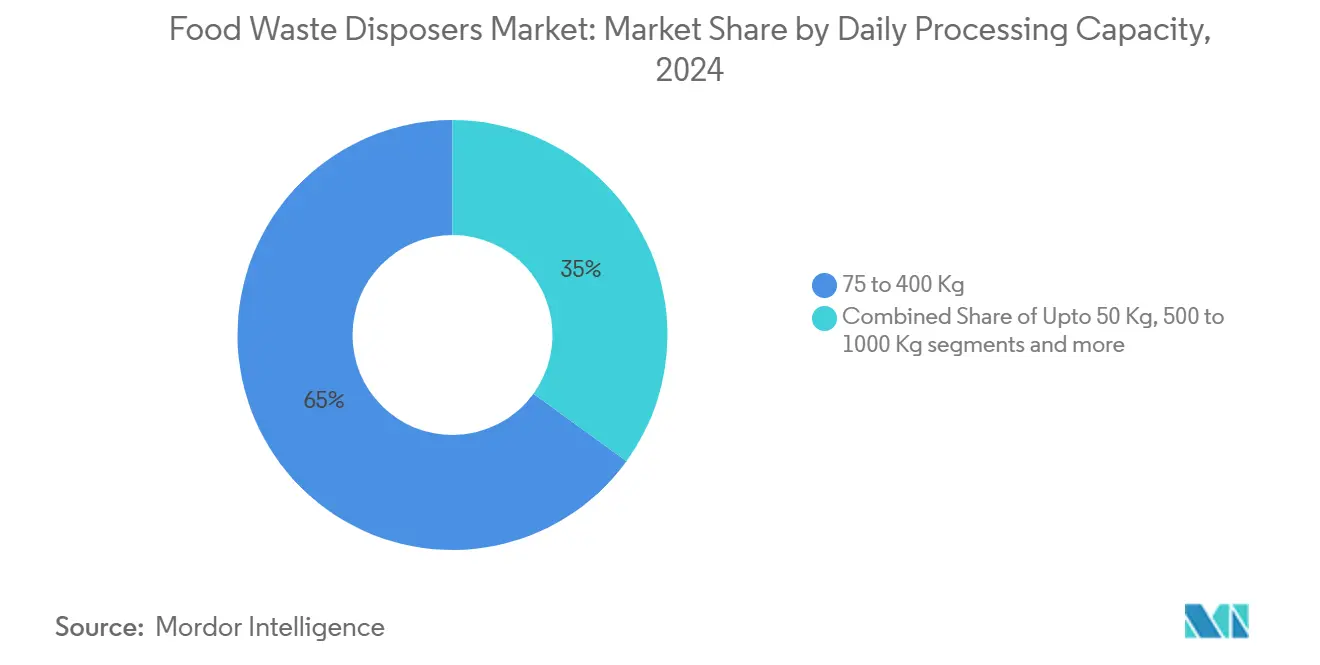

- By daily processing capacity, 75-400 kg systems captured 65.00% share of the food waste disposers market size in 2024 and are growing at a 7.10% CAGR.

- By operation, electric units secured 65.00% revenue of the food waste disposers market in 2024 and sustained a 6.60% CAGR outlook through 2030.

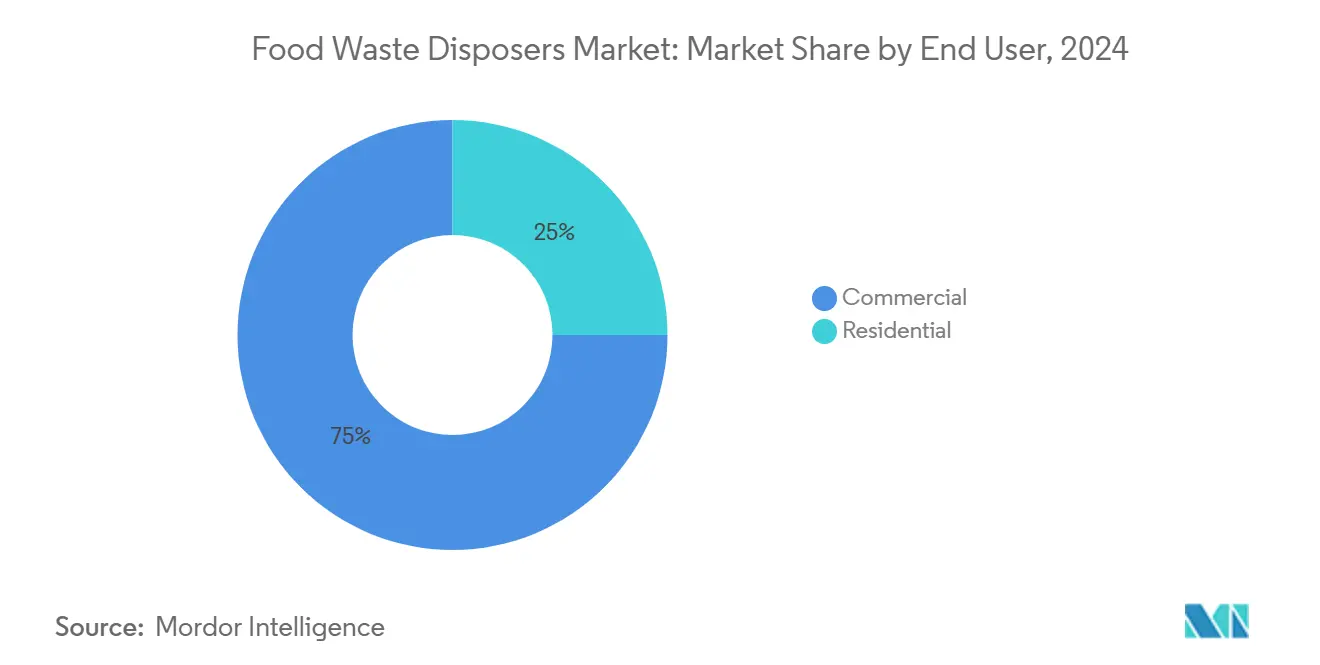

- By end user, commercial facilities held 75.00% of the food waste disposers market share in 2024, while residential installations are projected to rise at a 6.90% CAGR through 2030.

- By distribution channel, B2B/Directly from the Manufacturers held 68.00% of the food waste disposers market share in 2024, while B2C/Retail (online) is projected to rise at an 8.30% CAGR through 2030.

- By region, North America led with 38.00% revenue of the food waste disposers market in 2024, whereas Asia-Pacific is on track for a 7.20% CAGR to 2030.

Global Food Waste Disposers Market Trends and Insights

Drivers Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising household demand for convenience-oriented kitchen appliances | +1.2% | Global, with a concentration in North America & Europe | Medium term (2-4 years) |

| Stringent landfill-diversion mandates & municipal incentives | +1.8% | North America core, expanding to APAC & Europe | Short term (≤ 2 years) |

| Expansion of anaerobic-digestion facilities accepting disposer slurry | +0.9% | North America & Europe, emerging in APAC | Long term (≥ 4 years) |

| Proliferation of zero-waste certification programs in foodservice chains | +0.7% | Global, led by North America & Europe | Medium term (2-4 years) |

| Emergence of smart, IoT-enabled premium disposers | +0.6% | Developed markets, premium segments globally | Medium term (2-4 years) |

| Water-efficient disposer designs gaining approval in drought-prone regions | +0.4% | Western North America, Australia, select EU regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Household Demand for Convenience-Oriented Kitchen Appliances

Connected homes have normalized fixture-level sensing, prompting consumers to elevate disposers from optional accessories to baseline utilities. Mill Industries’ February 2024 AI-driven recycler shortens cycle time while logging diversion metrics compliant with SB 1383, showing how data transparency converts sustainability intent into measurable results [1]Mill Industries, “Mill Kitchen Food Recycler,” mill.com . Voice-assistant integration allows hands-free activation that meshes with modern cooking routines and hygiene expectations. Real-time monitoring encourages correct loading behavior, curbing clogs and warranty claims. Accordingly, premium SKUs achieve higher attachment rates in new-home packages, cementing long-term growth for the food waste disposers market. Appliance retailers report that disposer attach rates rise 18 percentage points when bundled with smart faucets, underscoring ecosystem pull-through.

Stringent Landfill-Diversion Mandates & Municipal Incentives

Policy intervention remains the chief accelerator for the food waste disposers market. New Hampshire’s February 2025 disposal ban for generators exceeding 1 ton of weekly food waste within 20 miles of an organics facility instantly redirected procurement budgets to in-sink solutions [2]New Hampshire Department of Environmental Services, “Organics Disposal Ban Rulemaking,” des.nh.gov . California’s SB 1383 enforces escalating fines, pushing municipalities to subsidize disposers' retrofits for low-income multifamily units. Industrial parks in Texas and Arizona negotiate sewer-rate discounts for verified disposer effluent routed to biogas partners, translating regulations into direct OPEX savings. Analysts tracking state-level legislative calendars expect five additional U.S. states to introduce partial organics bans by 2027, extending the compliance-driven adoption cycle. Similar momentum is evident in Australia, where the National Food Waste Strategy Action Plan 2026 drafts diverted-tonnage targets that explicitly name disposers among acceptable on-site technologies.

Proliferation of Zero-Waste Certification Programs in Food-Service Chains

The hospitality sector views third-party certification as competitive currency. SCS-110 v4.0 extends zero-waste auditing to events and projects, prompting chain-wide retrofit mandates across quick-service restaurants [3]SCS Global Services, “SCS-110 Certification Standard for Zero Waste v4.0,” scsglobalservices.com . Starbucks’ 2024 pledge under the U.S. Food Waste Pact sets a precedent for peers racing to memorialize diversion achievements. Disposers simplify audit workflows by providing digital logs of processed tonnage, replacing manual bin-weighing. Corporate sustainability officers highlight these logs in ESG disclosures, reinforcing board-level support for ongoing upgrades. As GHG-linked performance bonuses proliferate, disposer adoption becomes both an operational and financial imperative.

Emergence of Smart, IoT-Enabled Premium Disposers

Whirlpool’s InSinkErator MultiGrind platform garnered a 2025 Fortune innovation award for integrating accelerometers that detect vibration anomalies and trigger self-clearing reversals. Firmware updates delivered over Wi-Fi fine-tune torque curves based on aggregated usage patterns across thousands of units, embodying the shift toward continuous product-as-a-service. Predictive maintenance scheduling shaves field-service visits, decreasing downtime for high-throughput commissaries. Homeowners benefit from push notifications that advise optimal water flow, reducing environmental impact. These new capabilities anchor premium price tiers and cement brand loyalty in the increasingly data-centric food waste disposers market.

Restraints Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plumbing-code bans & building-level restrictions | -0.8% | Select municipalities globally, concentrated in older urban areas | Long term (≥ 4 years) |

| Water-use / septic compatibility concerns among homeowners | -0.6% | Rural North America, emerging markets with limited infrastructure | Medium term (2-4 years) |

| Rapid urban compost-collection roll-outs cannibalising demand | -0.4% | Urban centers in developed markets | Short term (≤ 2 years) |

| Stainless-steel & rare-earth price volatility pressuring BOM costs | -0.3% | Global manufacturing, concentrated impact on premium segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Plumbing-Code Bans & Building-Level Restrictions

Section 416 of the 2021 International Plumbing Code stipulates indirect drainage and specific trap arm geometry for disposers, complicating upgrades in pre-1970 high-rises. New York statutes reinforce indirect waste-pipe requirements, driving up retrofit costs for brownstone conversions. Boston’s Back Bay still restricts disposers due to undersized sewer laterals that risk surcharge during storm events. Manufacturers address these zones through low-flow, batch-feed units but concede slower adoption curves. Regulatory advocacy committees are pushing pilot studies that show negligible hydraulic load increases when grinders operate within revised water-usage standards, yet code changes move slowly.

Water-Use / Septic Compatibility Concerns Among Homeowners

In rural North America, septic drain fields designed decades ago can fail under incremental hydraulic loads, heightening homeowner anxiety. Field trials in Ontario reveal that proper enzyme dosing and tank pumping schedules accommodate disposer inflow without compromising effluent clarity, but myths persist. Awareness campaigns led by county health departments are beginning to show impact, with webinar attendance topping 2,000 participants in 2024. Still, negative perceptions limit the food waste disposers market in off-grid communities and emerging economies where sanitation infrastructure lags. Vendors respond with dual-mode appliances offering dehydration cycles for septic settings, but uptake remains incremental.

Segment Analysis

By Product Type: Grinding Dominance Faces Bio-Degradable Disruption

In 2024, grinding disposers accounted for 70.00% of the market revenue, driven by their longstanding recognition in building codes and widespread consumer trust. The introduction of advanced four-stage cutting technology has significantly reduced particle sizes, streamlining sewer transport processes, and addressing utility concerns. These disposers continue to dominate due to their established infrastructure compatibility and operational efficiency. In contrast, biodegradable presses, which compress food scraps into odorless pucks, are experiencing a robust 7.60% CAGR, reflecting growing demand for sustainable waste management solutions. Their compostable outputs align with zero-waste initiatives, making them increasingly popular in high-standard certifications such as LEED Platinum projects.

Emerging start-ups are capitalizing on this segment by developing odor-adsorption substrates that extend cartridge lifespans to 90 days, reducing the frequency of filter replacements and enhancing user convenience. Established grinding disposer manufacturers are responding by introducing enzyme-based cartridges that pre-treat waste slurry, optimizing its suitability for digesters, and maintaining their competitive edge. The market is expected to evolve toward multi-modal hybrid devices capable of switching between grinding and dehydrating functions to comply with varying local regulations. This adaptability not only protects customer investments but also extends product lifecycles, ensuring sustained vendor relevance. Such innovations are likely to reinforce vendor lock-in by addressing diverse regulatory requirements and enhancing operational flexibility.

Note: Segment shares of all individual segments available upon report purchase

By Feed Type: Continuous Systems Drive Operational Efficiency

In 2024, continuous-feed models accounted for 55.00% of the revenue, driven by their capability to ensure uninterrupted processing, which enables quick-service restaurants to meet stringent sanitation timeframes. The operational efficiency of these models aligns with the fast-paced requirements of the foodservice industry, making them a preferred choice. On the other hand, batch-feed units are projected to grow at a 6.70% CAGR, primarily due to their enhanced safety features. These units are particularly favored in environments like schools and elder-care facilities, where lid-based activation mechanisms mitigate the risk of accidental operation. The contrasting growth trajectories of these feed types highlight the varying priorities of end-users, ranging from operational speed to safety considerations.

Technological advancements, such as enhanced interlocks capable of detecting metal cutlery, have significantly improved product reliability by reducing jam incidents by one-third. Retailers are increasingly adopting augmented-reality demonstrations to address consumer concerns about under-sink clearance, thereby simplifying the decision-making process. This strategic use of technology not only educates consumers but also reduces perceived installation complexities, fostering greater adoption. Feed-type segmentation reflects a nuanced understanding of factors such as operational risk tolerance, energy tariff structures, and compliance with local plumbing codes. Manufacturers are optimizing their production processes by utilizing modular motor housings compatible with both feed mechanisms, which helps streamline inventory management and reduce lead times.

By Daily Processing Capacity: Mid-Range Dominance Reflects Market Maturity

In 2024, mid-range units within the 75-400 kg range generated 65.00% of the market's revenue, reflecting their dominant position in the segment. These units are forecasted to expand at a CAGR of 7.10% through 2030, driven by their compatibility with standard 90 mm sink flanges, which minimizes the need for costly counter modifications during retrofitting. The integration of six-kilowatt motors with gear-drive reducers enhances operational efficiency by increasing blade dwell time, enabling effective processing of fibrous materials without blockages. This segment's growth is further supported by its ability to meet the specific requirements of retrofit crews, who prioritize ease of installation and performance reliability. As a result, mid-range units continue to solidify their role as a preferred choice in the food waste disposers market.

Smaller units (≤ 50 kg) remain prevalent in single-family homes, but their growth potential is constrained by market saturation in developed economies. In contrast, ultra-large systems (≥ 500 kg) cater to niche industrial and institutional applications, such as naval galleys and amusement parks, where centralized slurry recovery systems justify higher capital investments. The introduction of cascaded mid-range units operating in parallel offers a cost-effective alternative to larger industrial models by providing redundancy and simplifying maintenance processes. Lifecycle-cost calculators, now integrated into OEM quoting tools, increasingly default to mid-range units for most applications, reinforcing their market leadership. These advancements highlight the strategic importance of mid-range systems in addressing diverse operational needs while maintaining cost efficiency.

Note: Segment shares of all individual segments available upon report purchase

By Operation: Electric Systems Leverage Infrastructure Maturity

In 2024, electric-drive disposers accounted for 65.00% of the revenue share, driven by the reliability of power grids in developed economies. The adoption of permanent-magnet motors, which achieve a 0.95 power factor, has significantly reduced reactive power penalties, optimizing commercial utility expenses. Variable-frequency drives have further enhanced operational efficiency by managing inrush currents, enabling the integration of disposers and dishwashers on 20-amp circuits without requiring costly panel upgrades. These advancements underscore the growing preference for electric-drive systems in markets with stable infrastructure. The combination of technological innovation and infrastructure reliability continues to position electric-drive disposers as a leading choice in the market.

Manual crank and hydraulic drives maintain relevance in niche applications such as off-grid resorts, disaster-response kitchens, and regions with inconsistent power supply, particularly in emerging markets. Hybrid hydro-mechanical units, which leverage pressurized water jets to amplify torque, provide a viable alternative by reducing electrical consumption by 24%. However, these systems face operational challenges, including higher maintenance requirements due to nozzle scaling in areas with hard water. Despite these limitations, hybrid units cater to specific market needs where electricity access is limited or unreliable. The ongoing trends in global electrification and decreasing motor costs are expected to sustain the competitive advantage of electric systems, while tailored innovations will ensure market segmentation remains adaptable.

By End User: Commercial Leadership Faces Residential Acceleration

In 2024, commercial venues contributed 75.00% of the total revenue, underscoring the impact of high waste density and stringent regulatory requirements in food-service operations. The rapid growth of ghost kitchens, a niche yet expanding subsegment, is driving the adoption of disposers as landlords enforce restrictions on organic bin storage to mitigate pest issues. Institutions such as schools, prisons, and hospitals are adopting batch-feed disposers, prioritizing safety while maintaining operational efficiency. This preference highlights the balance these institutions seek between compliance with safety standards and throughput optimization. The commercial segment's dominance reflects its critical role in addressing waste management challenges in high-density environments.

Residential demand is witnessing robust growth, supported by a 6.90% CAGR, as smart kitchen remodeling trends gain traction among homeowners. Homebuilders are increasingly integrating disposers into sustainability-focused packages, targeting eco-conscious millennials entering the housing market. This demographic shift is driving the adoption of disposers as a standard feature in modern, environmentally friendly homes. Over the long term, the market is expected to transition toward a 65/35 revenue split between commercial and residential segments, signaling a gradual diversification of the market base. While commercial applications will remain significant, the growing residential adoption will contribute to a more balanced and sustainable growth trajectory for the food waste disposers market.

By Distribution Channel: B2B Dominance Reflects Commercial Focus

In 2024, B2B factory-direct contracts accounted for 68.00% of shipments, driven by the specific requirements of commercial kitchens for site surveys, customized flange fabrication, and preventive maintenance guarantees. These contracts enable OEMs to secure consistent parts revenue and maintain stable cash flow through multiyear service agreements. The demand for tailored solutions highlights the critical role of direct engagement in addressing the operational needs of commercial kitchens. This approach ensures a reliable supply chain while fostering long-term partnerships between OEMs and their clients. The factory-direct model remains a cornerstone strategy in meeting the specialized demands of the food waste disposers market.

Online D2C portals are expanding at a CAGR of 8.30%, as consumers increasingly trust configurators to select horsepower, sound-shielding, and sink-mount kits. The convenience of e-commerce reduces search costs and enhances customer experience by offering detailed installation tutorials, which in turn minimizes reliance on professional plumbers. Big-box retailers continue to capture a share of casual replacement purchases, although their growth rate lags behind that of online channels. Professional installer networks, in collaboration with OEMs, facilitate same-day drop shipments, reducing lead times and safeguarding profit margins. This diversified channel strategy ensures broad market coverage while preserving the integrity of factory-direct relationships, a critical factor in the concentrated food waste disposers market.

Geography Analysis

In 2024, North America contributed 38.00% to the total revenue, reflecting its significant market share. The Canadian market exhibits a mixed adoption pattern, with Metro Vancouver banning disposers due to concerns over pipe capacity. In contrast, Toronto is actively piloting an in-sink disposal program for high-rise condominiums, scheduled for implementation in 2025. Mexico's updated solid-waste regulation, NOM-251, introduces stringent hygienic disposal requirements for food processors. This regulatory change is expected to drive early-stage growth in the region by promoting compliance and innovation in waste management practices.

Asia-Pacific is the fastest-rising region, logging a 7.20% CAGR toward 2030. China’s November 2024 Anti-Food Waste Action Plan seeks to trim grain losses below OECD averages by 2027, sparking subsidies for hotel disposer installations in Beijing and Guangzhou. Shanghai’s Pudong district allows property-tax rebates for commercial buildings that send disposer slurry to the Laogang biogas park. India, grappling with 78.2 million tonnes of annual food waste, positions disposers within its Smart Cities Mission to modernize sanitation [4]Invest India, “Indian Food Processing Sector Overview,” investindia.gov.in . Bengaluru amends building codes to award floor-area-ratio bonuses for large complexes installing on-site grinder-fed digesters. Southeast Asia follows a tourism-led pathway; Singapore’s hawker-centre pilot ties disposers to small-scale digesters to hit 2025 waste-cut targets.

Europe maintains mid-single-digit expansion anchored by the EU Circular Economy Action Plan’s mandate for separate biowaste collection by 2025. Germany’s phosphorus-recovery regulations complicate grinder rollout, yet utility Emschergenossenschaft opened a three-year study on nutrient-loop impacts. Nordic uptake remains modest; Stockholm’s preference for vacuum tubes competes with disposers, but a 2025 city-funded LCA comparison may reopen the debate. Eastern-European markets show early promise, as Poland channels EU cohesion funds into wastewater-digester upgrades that welcome high-BOD inflows.

South America and Middle East & Africa are smaller today but feature growth pockets tied to hospitality construction and resource-conservation agendas. Chile’s Santiago concession agreements now incorporate renewable natural-gas quotas met via disposer-fed digesters. Brazil’s São Paulo ordinance 17.471/2024 incentivizes in-sink technologies in school kitchens to combat trash-truck strikes. Saudi Arabia’s Red Sea tourism megaproject specifies premium disposers across 50 planned hotels, signalling region-wide adoption potential. Water-scarce Gulf states will likely bundle grinders with greywater-recycling systems to close resource loops.

Competitive Landscape

The food waste disposers market is highly consolidated; the top five players command the majority of the revenue. In 2024, Whirlpool's acquisition of InSinkErator strengthened its portfolio with advanced features, including multistage cutting, anti-jam algorithms, and vibration damping. Concurrently, Emerson retained ownership of specific sensor intellectual properties, leveraging licensing agreements to maintain a strategic presence in the technology domain. Salvajor doubles down on commercial IoT telemetry through its 2025 Guardian Gateway, connecting grinders to building-management systems for alert scheduling. Hobart leverages dish-room dominance to cross-sell disposers bundled with warewashing stations, shielding share from upstarts.

Innovation pipelines focus on water savings, noise suppression, and cloud-connected diagnostics. Patent litigation remains a strategic lever; 2024 U.S. district suits over splash-guard geometry resulted in preliminary injunctions against two low-cost importers, tightening market gatekeeping. Aftermarket ecosystems also matter: Whirlpool’s 24-hour part-fulfillment rate exceeds 98%, a hurdle that smaller players struggle to match. With water utilities nudging toward volume-based sewer charges, suppliers that integrate effluent-metering sensors may carve out fresh differentiation. Overall, incumbents combine brand equity, service networks, and regulatory lobbying to fortify their lead in the food waste disposers market.

Food Waste Disposers Industry Leaders

-

Emerson Electric (Co.) – InSinkErator

-

Moen Incorporated

-

Anaheim Mfg. – Waste King

-

Franke Holding AG

-

Whirlpool (KitchenAid)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: WELTEC BIOPOWER broke ground on a new biomethane plant for Eco Sustainable Solutions in Dorset, England, marking a strategic expansion that will use household food waste as feedstock when it comes online in 2025.

- October 2024: SCS Global Services released SCS-110 Zero Waste Standard v4.0, expanding the scope to facilities, events, and projects.

- April 2024: Whirlpool and Arçelik finalized the formation of Beko Europe B.V., an expansion move that realigns Whirlpool’s European appliance portfolio while keeping InSinkErator under its direct ownership for global growth synergies.

- February 2024: Mill Industries launched an AI-enabled residential food-waste recycler that processes scraps faster and quieter while automatically reporting diversion metrics to support SB 1383 compliance.

Global Food Waste Disposers Market Report Scope

A complete background analysis of the Food Waste Disposers Market, which includes an assessment of the parental market, emerging trends by segments and regional markets, Significant changes in market dynamics and a market overview is covered in the report. The report also features a qualitative and quantitative assessment by analyzing data gathered from industry analysts and market participants across key points in the industry's value chain. The food Waste Disposers Market is Segmented By Type (Shattered Type Disposers, Dry Type Disposers, and Grinding Type Disposers), By End-User (Residential, and Commercial), By Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online, and Others), and By Geography (North America, Europe, Asia-Pacific, South America, and the Middle East and Africa). The Report Offers Market Size and Forecasts for the Food Waste Disposers Market in Value (USD Billion) for all the above

| Bio-degradable Type |

| Drying Type |

| Regrigerate/Cold Type |

| Grinding Type |

| Continuous Feed |

| Batch Feed |

| Upto 50 Kg |

| 75 to 400 Kg |

| 500 to 1000 Kg |

| Above 1000 Kg |

| Manual |

| Electric |

| Residential | |

| Commercial | HoReCa |

| Institutional (Schools, Hospitals, Office Canteens) | |

| Housing Societies | |

| Government (Municipal Wards, Defence, etc.) |

| B2C/Retail Channels | Home-Improvement Stores |

| Specialty Appliance Stores | |

| Online | |

| Other Distribution Channels | |

| B2B/Directly from the Manufacturers |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Bio-degradable Type | |

| Drying Type | ||

| Regrigerate/Cold Type | ||

| Grinding Type | ||

| By Feed Type | Continuous Feed | |

| Batch Feed | ||

| By Daily Processing Capacity | Upto 50 Kg | |

| 75 to 400 Kg | ||

| 500 to 1000 Kg | ||

| Above 1000 Kg | ||

| By Operation | Manual | |

| Electric | ||

| By End User | Residential | |

| Commercial | HoReCa | |

| Institutional (Schools, Hospitals, Office Canteens) | ||

| Housing Societies | ||

| Government (Municipal Wards, Defence, etc.) | ||

| By Distribution Channel | B2C/Retail Channels | Home-Improvement Stores |

| Specialty Appliance Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Directly from the Manufacturers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2030 forecast for the food waste disposers market?

The food waste disposers market is projected to reach USD 4.64 billion by 2030 on a 5.74% CAGR.

Which product type currently dominates?

Grinding disposers hold 70.00% revenue because multistage cutters deliver wastewater-compliant particle sizes and long-proven reliability.

Why is Asia-Pacific the fastest-growing region?

Regulatory initiatives like China’s Anti-Food Waste Action Plan and rapid food-service expansion underpin a 7.20% CAGR for Asia-Pacific.

How do landfill-diversion mandates affect adoption?

Policies such as California’s SB 1383 and New Hampshire’s organics ban force waste generators to adopt disposers or face escalating penalties.

Are disposers safe for septic systems?

Field studies show properly maintained septic tanks handle disposer effluent well, and daily water use rises by less than 1%.

What new technology drives premium pricing?

IoT-enabled disposers with cloud diagnostics, torque-adaptive motors, and WaterSense-certified impellers justify higher margins through efficiency and real-time insights.

Page last updated on: