| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 4.87 Billion |

| Market Size (2030) | USD 7.23 Billion |

| CAGR (2025 - 2030) | 8.22 % |

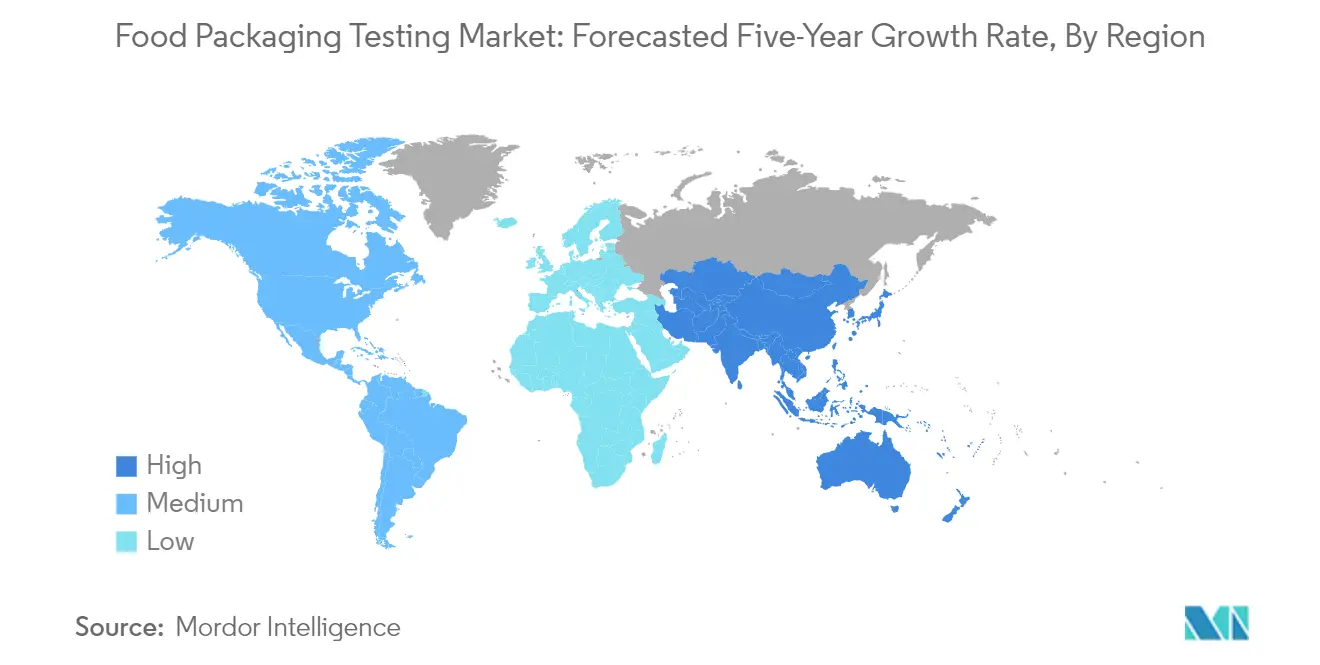

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

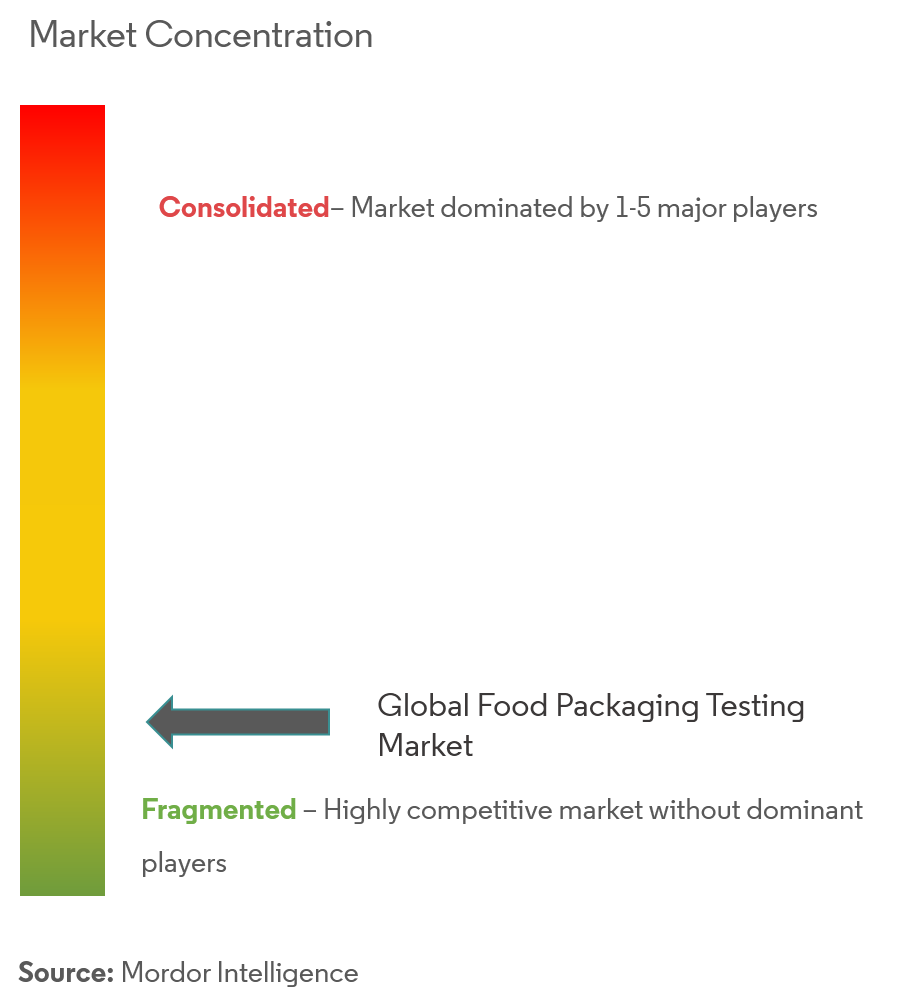

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Food Packaging Testing Market Analysis

The Food Packaging Testing Market size is estimated at USD 4.87 billion in 2025, and is expected to reach USD 7.23 billion by 2030, at a CAGR of 8.22% during the forecast period (2025-2030).

The food packaging testing industry is experiencing significant transformation driven by evolving consumer preferences and technological advancements in packaging materials. The shift towards sustainable and eco-friendly packaging options has led to the emergence of innovative materials like nanocomposites, edible/biodegradable packaging, and intelligent packaging systems that require comprehensive testing protocols. These developments have prompted testing laboratories to expand their capabilities to evaluate new parameters like biodegradability, compostability, and the interaction between smart packaging components and food products. The integration of nanotechnology in food packaging testing has particularly accelerated the need for specialized testing methodologies to ensure both safety and functionality.

The industry is witnessing a notable shift towards comprehensive food packaging analysis approaches that encompass both traditional and emerging safety parameters. Testing facilities are increasingly adopting advanced analytical techniques such as high-performance liquid chromatography (HPLC), gas chromatography-mass spectrometry (GC-MS), and inductively coupled plasma mass spectrometry (ICP-MS) for more precise detection of chemical migrants and contaminants. This evolution in testing methodologies is particularly crucial as packaging manufacturers experiment with recycled materials and novel polymer blends, requiring more sophisticated analysis of potential contaminants and their migration patterns.

The market landscape is being reshaped by the rising adoption of modified atmosphere packaging (MAP) and active packaging technologies, which necessitate specialized testing protocols. Testing service providers are expanding their capabilities to evaluate gas composition, barrier properties, and the effectiveness of active packaging components such as oxygen scavengers and antimicrobial agents. The industry is also seeing increased demand for testing services related to layered packaging materials, as food manufacturers seek to optimize shelf life while maintaining product safety and quality through multi-layer packaging solutions.

The sector is experiencing a significant transformation in testing requirements due to the growing complexity of food packaging materials and designs. The rise in demand for convenience foods and ready-to-eat products has led to more sophisticated packaging solutions that combine multiple materials and technologies, requiring comprehensive testing protocols. Testing facilities are adapting their services to address these complexities, incorporating evaluations for chemical interactions between different packaging layers, seal integrity in flexible packaging, and the performance of smart packaging features like time-temperature indicators and freshness sensors. This evolution is particularly evident in the beverage packaging segment, where new designs for extended shelf life and product protection require specialized testing methodologies. The packaging testing services market is evolving to meet these demands, ensuring that the food packaging material testing processes remain robust and reliable.

Food Packaging Testing Market Trends

Ongoing Expansion of Processed Food Industry

The continuous growth of the processed and packaged food industry is driving significant demand for food packaging testing services. The retail landscape for packaged foods shows dairy products leading with a 22.3% market share, followed by bakery at 16.1%, and processed meat and seafood at 11% of retail value sales globally. This expanding processed food sector has prompted strategic investments by major food companies to increase production capacity and develop innovative packaging solutions that require rigorous food packaging material testing protocols. For instance, in December 2021, Tyson Foods announced an investment of USD 1.8 billion for capacity expansion across different facilities over two years, while other companies like Nestlé, Cargill, and Aryzta AG have undertaken similar operational efficiency programs.

The emergence of new product categories and changing consumer preferences are further accelerating the need for comprehensive food package testing services. Food manufacturers are increasingly launching products with longer shelf-life requirements, frozen foods, ready-to-cook items, and ready-to-eat meals, each demanding specific packaging designs and corresponding testing protocols. This trend is exemplified by recent market entries such as OTS Holdings Limited's launch of a plant-based ready-to-eat food brand ANEW in June 2022, and Wipro Consumer Care & Lighting's entry into the packaged foods business covering snack foods, spices, and ready-to-eat products in July 2022. These developments necessitate advanced testing services to ensure packaging integrity, safety, and compliance with various regulatory standards while meeting consumer expectations for quality and convenience.

Understand The Key Trends Shaping This Market

Download PDF

Stringent Regulations for the Food Packaging Industry

The increasing complexity and stringency of food packaging regulations across global markets are fundamentally driving the demand for comprehensive testing services. Regulatory bodies worldwide are implementing stricter controls on food contact materials, with recent developments including the Belgian Federal Public Service's 2021 regulation on specific release limits for metal and alloy components, and Denmark's 2020 ban on per- and polyfluoroalkyl substances (PFAS chemicals) in food contact paper and board materials. These evolving regulations require manufacturers to conduct extensive testing across various parameters, including migration testing, heavy metal content analysis, and overall packaging integrity assessment to ensure compliance and product safety.

The regulatory framework continues to evolve with new guidelines being introduced for emerging packaging materials and technologies. Testing laboratories are required to be accredited by various authorities, including the FDA, CPSIA, ASTM International, The European Commission, Standards Australia, and FSSAI, to provide certified testing services. For instance, in India alone, there are more than 120 laboratories accredited by FSSAI and NABL to facilitate food safety and food packaging testing safety testing. The scope of testing has expanded beyond basic safety parameters to include specific aspects such as migration testing, contamination analysis, and chemical trace analysis, particularly for new packaging innovations like active and intelligent packaging systems. This comprehensive regulatory environment necessitates manufacturers to invest in regular and thorough testing procedures to maintain compliance and ensure product safety throughout the supply chain.

Segment Analysis: By Testing Type

Chemical Testing Segment in Food Packaging Testing Market

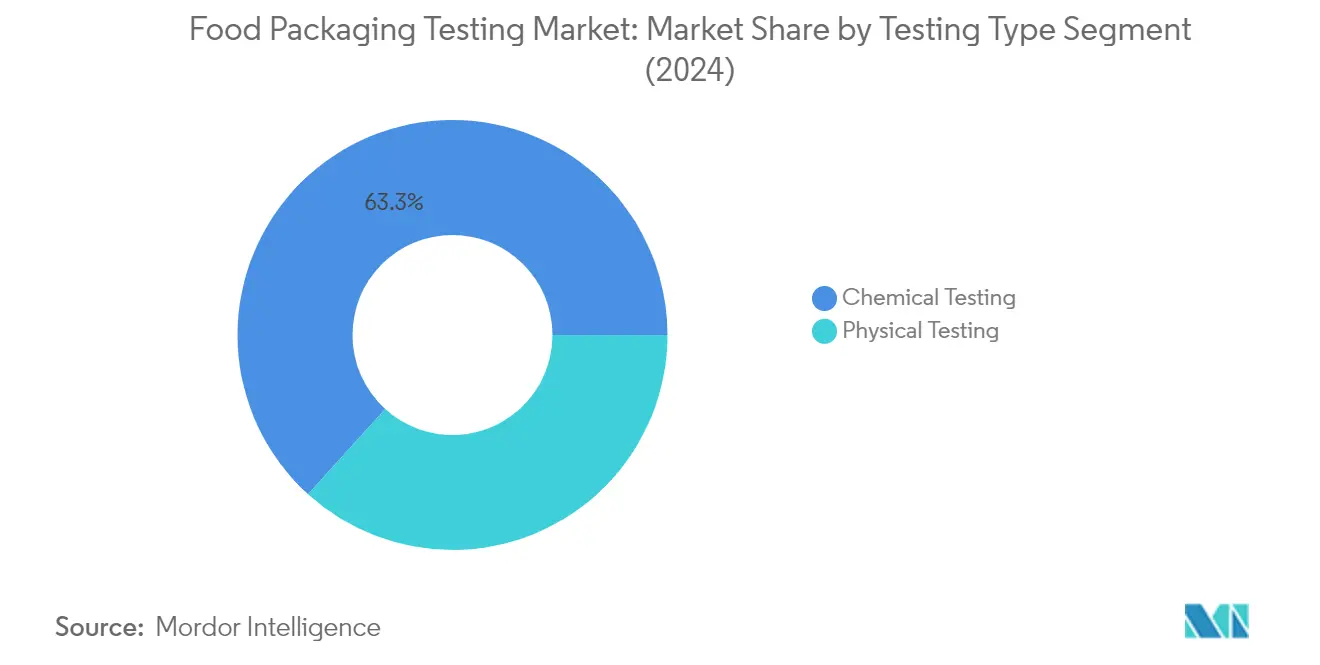

Chemical testing dominates the food packaging testing market, holding approximately 63% market share in 2024. This segment's prominence is driven by the increasing importance of migration testing and extractable testing to determine contamination and chemical migration in food packaging materials. The segment encompasses various critical testing methods, including migration testing, extractable testing, leachable testing, and other specialized chemical analyses. Migration testing, which represents the largest sub-segment, is particularly crucial as it helps determine whether chemical substances are transferred from food packaging to food and beverages. The growing concerns about non-intentionally added substances (NIAS) in food, which are chemicals not intentionally added during production but present due to migration from packaging, have significantly boosted the demand for chemical testing services. Additionally, the segment's growth is supported by stringent regulatory requirements across different regions requiring comprehensive chemical analysis of food packaging materials.

Physical Testing Segment in Food Packaging Testing Market

The physical testing segment plays a vital role in ensuring the structural integrity and performance of food packaging materials. This segment includes crucial testing parameters such as durability testing, heat resistance testing, and water vapor/gas permeability testing. Physical testing is essential for determining the durability, handling capabilities, and stability of packaging products in different atmospheres. The testing process involves both manual and mechanical durability checks aimed at identifying faults and ensuring market suitability. Durability testing can be further categorized into various tests such as drop test, edge crush test, burst test, packaging vibration test, stacking crush resistance test, and packaging moisture test. These tests are particularly important for manufacturers to understand the shelf life of products and evaluate package reliability against material or seal failure during manufacture, distribution, and storage.

Segment Analysis: Packaging Material

Plastic Segment in Food Packaging Testing Market

The plastic segment continues to dominate the food packaging testing market, holding approximately 37% of the market share in 2024. This significant market position is driven by the widespread use of plastic packaging across various food and beverage applications, particularly in processed and ready-to-eat food products. The increasing concerns regarding the toxicological effects of certain plastic packaging variants have intensified the need for comprehensive testing protocols. Food manufacturers and packaging companies are particularly focused on testing various plastic materials, including polyethylene terephthalate (PETE or PET), high-density polyethylene (HDPE), polyvinyl chloride (PVC), and low-density polyethylene (LDPE), to ensure compliance with evolving regulations and safety standards. The demand for plastic packaging testing is further bolstered by the growing emphasis on sustainable and recyclable packaging solutions, requiring additional testing parameters to verify environmental compliance while maintaining food safety.

Paper and Board Segment in Food Packaging Testing Market

The paper and board segment is emerging as the fastest-growing segment in the food packaging testing market, projected to grow at approximately 9% during the forecast period 2024-2029. This accelerated growth is primarily attributed to the increasing adoption of sustainable packaging solutions and the rising environmental consciousness among consumers and manufacturers. The segment's growth is further driven by innovations in paper-based packaging technologies, including the development of advanced barrier coatings and smart packaging solutions that require specialized testing protocols. Testing requirements for paper and board packaging have become more stringent, encompassing various parameters such as burst strength, folding endurance, moisture resistance, and migration testing for recycled content. The segment is also witnessing increased testing demands due to the introduction of novel bio-based coatings and treatments designed to enhance the protective properties of paper-based packaging materials.

Remaining Segments in Packaging Material

The metal, glass, and layered packaging segments each play crucial roles in the food packaging testing market with their unique testing requirements and applications. Metal packaging testing focuses on corrosion resistance, seal integrity, and chemical migration testing, which are particularly important for canned foods and beverages. The glass segment emphasizes thermal shock resistance and mechanical strength testing, crucial for ensuring product safety during transportation and storage. Layered packaging, while representing a smaller market share, requires complex testing protocols due to its multi-material composition, including tests for delamination resistance and barrier properties. These segments collectively contribute to the comprehensive nature of the food packaging testing market, each addressing specific safety and quality requirements for different food products and storage conditions.

Food Packaging Testing Market Geography Segment Analysis

Food Packaging Testing Market in North America

The North American food packaging testing market demonstrates a robust framework supported by stringent regulatory requirements and advanced testing infrastructure. The United States leads the regional packaging testing market, followed by Canada and Mexico, with each country contributing significantly to the overall market dynamics. The region's growth is primarily driven by the ongoing expansion of the processed food industry and increasing consumer awareness regarding food safety. The presence of major packaging testing services market providers and their extensive laboratory networks further strengthens the market position in North America.

Food Packaging Testing Market in the United States

The United States dominates the North American food packaging testing market, holding approximately 77% of the regional market share. The country's market leadership is attributed to its comprehensive regulatory framework governed by the FDA and other regulatory bodies. The presence of numerous food processing companies and their increasing focus on quality assurance drives the demand for testing services. The country has also witnessed significant investments in testing infrastructure and technological advancements, particularly in chemical and physical testing capabilities. The market is characterized by the presence of both international and domestic testing service providers who offer a wide range of testing solutions.

Food Packaging Testing Market in Mexico

Mexico emerges as the fastest-growing market in North America, with a projected growth rate of approximately 10% during 2024-2029. The rapid growth is fueled by the expanding food processing sector and increasing exports to the United States and Canada. The country has been strengthening its testing infrastructure and regulatory framework to align with international standards. Mexican authorities have been actively collaborating with international bodies to enhance food safety measures, particularly in food packaging testing protocols. The market has attracted significant investments from major testing service providers who are expanding their presence through new laboratories and testing facilities.

Food Packaging Testing Market in Europe

The European food packaging testing market showcases a mature and well-established testing ecosystem supported by stringent EU regulations and standards. The market encompasses major economies including Germany, the United Kingdom, France, Italy, Spain, and Russia, each contributing significantly to the regional market dynamics. The region's focus on sustainable packaging solutions and innovative testing methodologies drives market growth. The presence of leading testing service providers and their extensive laboratory networks ensures comprehensive testing coverage across the region.

Food Packaging Testing Market in Germany

Germany maintains its position as the largest market in Europe, commanding approximately 18% of the regional market share. The country's leadership is attributed to its strong industrial base and presence of major food processing companies. German testing facilities are known for their technological advancement and comprehensive testing capabilities, particularly in migration testing and chemical analysis. The market benefits from strong research and development activities and collaboration between industry stakeholders and testing service providers. The country's emphasis on quality control and safety standards continues to drive demand for testing services.

Food Packaging Testing Market in the United Kingdom

The United Kingdom demonstrates the highest growth potential in Europe, with a projected growth rate of approximately 8% during 2024-2029. The growth is driven by increasing emphasis on food safety regulations and rising demand for sustainable packaging solutions. The UK market has shown resilience and adaptation to regulatory changes, particularly in developing new testing protocols for emerging packaging materials. The country's testing infrastructure continues to evolve with investments in advanced testing technologies and expansion of testing capabilities. The market is characterized by strong collaboration between testing service providers and food manufacturers.

Food Packaging Testing Market in Asia-Pacific

The Asia-Pacific food packaging testing market demonstrates dynamic growth potential driven by rapid industrialization and increasing food safety awareness. The region encompasses major markets including China, Japan, India, and Australia, each contributing uniquely to the market landscape. The market is characterized by increasing adoption of international testing standards and growing investments in testing infrastructure. Regional authorities are strengthening regulatory frameworks to ensure compliance with global food safety standards.

Food Packaging Testing Market in China

China emerges as the dominant force in the Asia-Pacific region's food packaging testing market. The country's leadership is attributed to its massive food processing industry and stringent regulatory requirements. Chinese testing facilities have undergone significant modernization with increased focus on advanced testing methodologies. The market is characterized by the presence of both international and domestic testing service providers offering comprehensive testing solutions. The country's emphasis on food safety and quality control continues to drive market growth.

Food Packaging Testing Market in India

India stands out as the fastest-growing market in the Asia-Pacific region. The growth is driven by rapid expansion of the processed food industry and increasing awareness about food safety standards. The country has witnessed significant investments in testing infrastructure and capabilities, particularly in chemical and physical testing facilities. Indian regulatory authorities are actively updating testing requirements to align with international standards. The market shows strong potential for further expansion with increasing focus on quality assurance in food packaging.

Food Packaging Testing Market in South America

The South American food packaging testing market demonstrates growing potential with Brazil and Argentina as key contributors. The market is characterized by increasing adoption of international testing standards and growing investments in testing infrastructure. Brazil emerges as the largest market in the region, while Argentina shows the fastest growth potential. The region's focus on export quality compliance and domestic food safety regulations drives the demand for testing services. Regional testing service providers are expanding their capabilities to meet the growing demand for comprehensive testing solutions.

Food Packaging Testing Market in the Middle East and Africa

The Middle East and African food packaging testing market shows promising growth potential with South Africa and Saudi Arabia as key markets. The region is witnessing increasing investments in testing infrastructure and growing adoption of international testing standards. South Africa leads the regional market in terms of market size, while Saudi Arabia demonstrates the fastest growth potential. The market is driven by increasing focus on food safety regulations and growing awareness about packaging quality. Regional authorities are strengthening regulatory frameworks to ensure compliance with international standards.

Get Analysis on Important Geographic Markets

Download PDF

Food Packaging Testing Industry Overview

Top Companies in Food Packaging Testing Market

The food packaging testing market is led by established players like SGS SA, Bureau Veritas, Eurofins Scientific, and Intertek Group, who have built a strong global presence through extensive laboratory networks. These companies are actively pursuing innovation through the development of new testing methodologies and advanced analytical platforms, particularly in areas like migration testing, chemical analysis, and durability assessment. Market leaders are expanding their geographical footprint through strategic laboratory acquisitions and new facility establishments, especially in emerging markets across the Asia-Pacific region. Companies are increasingly focusing on digital transformation by implementing automated testing processes and offering digital result reporting platforms. The industry is witnessing a trend toward comprehensive service offerings, where providers are bundling multiple testing services with consulting and certification solutions to create end-to-end quality assurance packages for food manufacturers.

Fragmented Market with Strong Regional Players

The packaging testing services market exhibits a fragmented structure with a mix of global testing conglomerates and specialized regional laboratories. The major global players leverage their extensive networks and accreditations to serve multinational food companies, while regional specialists focus on local regulatory compliance and customized testing solutions. The market is characterized by ongoing consolidation activities, particularly in emerging markets where larger players are acquiring local laboratories to expand their presence and enhance their service portfolios. These acquisitions are driven by the need to gain local market expertise, expand testing capabilities, and achieve economies of scale in laboratory operations.

The competitive dynamics are shaped by the presence of both diversified testing organizations that offer services across multiple industries and specialized food safety testing providers. Market leaders are increasingly investing in expanding their testing capabilities through new laboratory establishments and technology upgrades, while also focusing on obtaining various international accreditations to enhance their credibility. The industry is witnessing a trend toward vertical integration, with some players expanding their services to include consulting, training, and regulatory compliance support alongside traditional testing services.

Innovation and Compliance Drive Market Success

Success in the packaging testing market increasingly depends on providers' ability to adapt to evolving regulatory requirements and technological advancements in packaging materials. Companies need to continuously invest in advanced testing equipment and methodologies to address new packaging innovations, particularly in sustainable and smart packaging solutions. Market players must also focus on building strong relationships with food manufacturers and regulatory bodies while maintaining a robust quality management system and obtaining relevant accreditations. The ability to provide rapid testing results while ensuring accuracy and reliability has become crucial for maintaining a competitive advantage.

Future growth opportunities lie in developing specialized testing solutions for emerging packaging materials and expanding service offerings to include sustainability assessments and regulatory compliance consulting. Companies need to focus on digital transformation initiatives to improve operational efficiency and enhance customer experience through online result reporting and tracking systems. Success also depends on maintaining a balance between standardized testing procedures and customized solutions to meet specific client requirements. Market players must stay ahead of regulatory changes and invest in training their technical staff to handle increasingly complex testing requirements while maintaining cost competitiveness. Additionally, the integration of food packaging analysis into service offerings is becoming essential for addressing the evolving needs of the industry.

Food Packaging Testing Market Leaders

-

SGS SA

-

Bureau Veritas Group

-

Intertek Group plc

-

Merieux NutriSciences Corporation

-

TÜV SÜD South Asia Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Food Packaging Testing Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

-

4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 By Testing Type

- 5.1.1 Physical Testing

- 5.1.1.1 Durability Testing

- 5.1.1.2 Heat Resistance Testing

- 5.1.1.3 Water Vapor /Gas Permeability Testing

- 5.1.2 Chemical Testing

- 5.1.2.1 Migration Testing

- 5.1.2.2 Extractable Testing

- 5.1.2.3 Leachable Testing

- 5.1.2.4 Others

-

5.2 By Packaging Material

- 5.2.1 Plastic

- 5.2.2 Glass

- 5.2.3 Metal

- 5.2.4 Paper & Board

- 5.2.5 Layer Packaging

-

5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Spain

- 5.3.2.2 United Kingdom

- 5.3.2.3 Germany

- 5.3.2.4 France

- 5.3.2.5 Italy

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Most Active Companies

- 6.2 Most Adopted Strategies

- 6.3 Market Share Analysis

-

6.4 Company Profiles

- 6.4.1 SGS SA

- 6.4.2 Bureau Veritas Group

- 6.4.3 Intertek Group plc

- 6.4.4 Merieux NutriSciences Corporation

- 6.4.5 TUV SUD South Asia Pvt. Ltd.

- 6.4.6 Eurofins Scientific

- 6.4.7 Microbac Laboratories Inc.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Food Packaging Testing Industry Segmentation

Theglobalfood packaging testingmarkethasbeen segmentedbycategoryintophysical and chemical tests. Thephysical testsegment can be further bifurcated intodurability, heat resistance and water vapor/gas permeability tests; and the chemical test is bifurcated into migration, extractable, leachable and other tests.Bypackaging material, the market is segmentedintoplastic, glass, metal, paper & boardandlayer packaging such as Tetrapack.Also, the study provides an analysis of the drinkable yogurtmarket in the emerging and established markets across the globe, including North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

| By Testing Type | Physical Testing | Durability Testing | |

| Heat Resistance Testing | |||

| Water Vapor /Gas Permeability Testing | |||

| Chemical Testing | Migration Testing | ||

| Extractable Testing | |||

| Leachable Testing | |||

| Others | |||

| By Packaging Material | Plastic | ||

| Glass | |||

| Metal | |||

| Paper & Board | |||

| Layer Packaging | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Spain | ||

| United Kingdom | |||

| Germany | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Food Packaging Testing Market Research FAQs

How big is the Food Packaging Testing Market?

The Food Packaging Testing Market size is expected to reach USD 4.87 billion in 2025 and grow at a CAGR of 8.22% to reach USD 7.23 billion by 2030.

What is the current Food Packaging Testing Market size?

In 2025, the Food Packaging Testing Market size is expected to reach USD 4.87 billion.

Who are the key players in Food Packaging Testing Market?

SGS SA, Bureau Veritas Group, Intertek Group plc, Merieux NutriSciences Corporation and TÜV SÜD South Asia Pvt. Ltd. are the major companies operating in the Food Packaging Testing Market.

Which is the fastest growing region in Food Packaging Testing Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Food Packaging Testing Market?

In 2025, the North America accounts for the largest market share in Food Packaging Testing Market.

What years does this Food Packaging Testing Market cover, and what was the market size in 2024?

In 2024, the Food Packaging Testing Market size was estimated at USD 4.47 billion. The report covers the Food Packaging Testing Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Food Packaging Testing Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Food Packaging Testing Market Research

Mordor Intelligence offers comprehensive insights into the food packaging testing market, drawing on decades of expertise in packaging testing services and industry analysis. Our extensive research covers key aspects of food packaging analysis, such as safety compliance, material performance, and quality assurance protocols. The report provides a detailed examination of food packaging material testing methodologies, emerging technologies, and industry best practices across global markets. It includes a specialized focus on the testing of packaged foods and environmental impact assessment.

Stakeholders gain valuable insights through our detailed analysis of packaging testing market trends, technological advancements, and regulatory frameworks. The report, available as an easy-to-download PDF, offers in-depth coverage of food package testing procedures, industry standards, and certification requirements. Our research encompasses food and environment manual testing protocols and examines the evolving landscape of the market for food packaging testers and equipment. The comprehensive analysis includes detailed sections on Central South America food safety testing developments and global industry innovations, providing stakeholders with actionable intelligence for strategic decision-making.