Market Size of Food Packaging Industry

| Study Period | 2019 - 2029 |

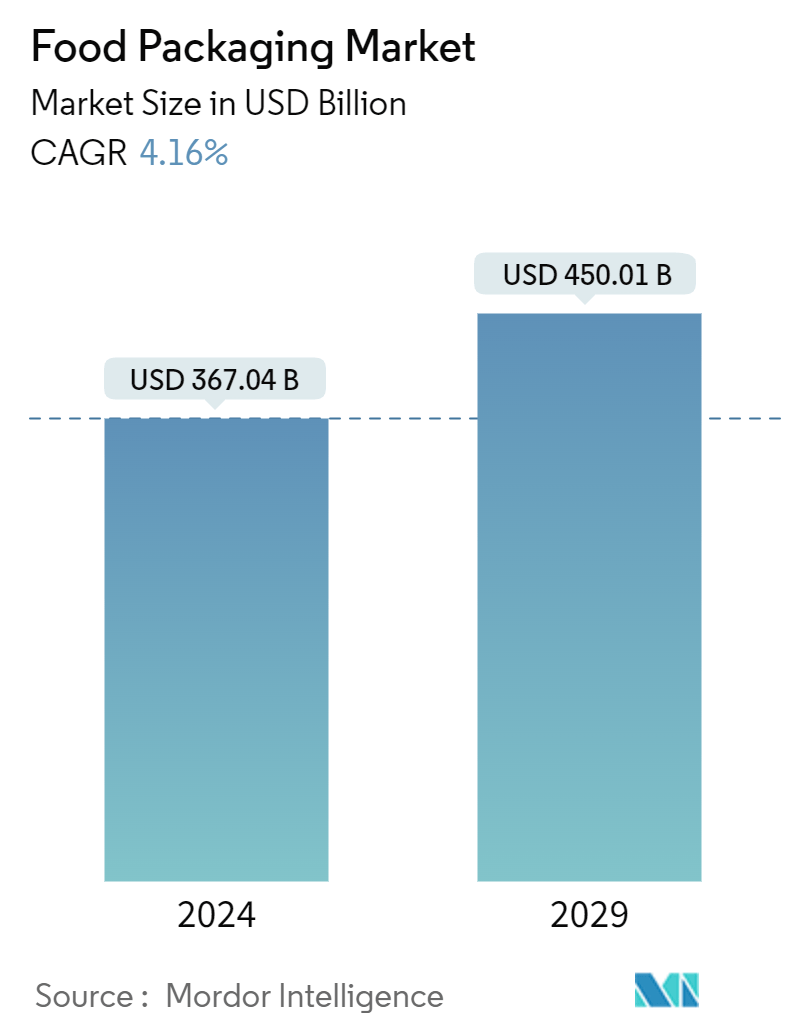

| Market Size (2024) | USD 367.04 Billion |

| Market Size (2029) | USD 450.01 Billion |

| CAGR (2024 - 2029) | 4.16 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Food Packaging Market Analysis

The Food Packaging Market size is estimated at USD 367.04 billion in 2024, and is expected to reach USD 450.01 billion by 2029, growing at a CAGR of 4.16% during the forecast period (2024-2029).

- The food packaging industry has experienced significant growth in recent years, primarily driven by factors such as urbanization, a rising middle-income population, and an increase in disposable income. The demand for packaged food has been steadily climbing, leading to a surge in the need for efficient and sustainable packaging solutions.

- One of the primary factors influencing the trajectory of the food packaging market is the increasing demand for convenience. Urbanization, changing dietary preferences, and busy lifestyles are driving consumers toward convenient, ready-to-eat meals. Consequently, there is a growing preference for packaging solutions that offer portability, user-friendliness, and extended shelf life to the food.

- The growth of the food packaging industry offers significant opportunities but also highlights a critical concern of sustainability. The excessive use of plastic packaging has raised alarms about environmental damage and pollution. In response, the food packaging industry is increasingly prioritizing sustainable packaging solutions. Biodegradable materials, such as compostable plastics, plant-based packaging, and recycled materials, are gaining momentum.

- As a result, manufacturers are increasingly exploring eco-friendly alternatives to traditional plastic packaging, driven by both regulatory pressures and consumer demand for greener options. For instance, in June 2024, Saica Group and Mondelez collaboratively introduced a new paper-based product targeting multipack products for the confectionery, biscuits, and chocolate markets to meet the sustainability standards set by the Confederation of European Paper (CEPI). This packaging solution is suitable for heat-sealable packing processes and can be produced coated or uncoated.

- The COVID-19 pandemic heightened consumer awareness regarding product hygiene. Consequently, the emphasis on food protection, freshness, safety, and hygiene has increased, driving demand for improved food packaging solutions. The food packaging market encountered a multifaceted scenario during the pandemic. Initially, demand surged for shelf-stable and single-use packaging due to stockpiling and hygiene concerns. This increase, however, temporarily sidelined sustainability efforts. Moving forward, the market is expected to experience sustained growth, driven by the ongoing shift toward e-commerce and convenience foods, with a renewed focus on innovative, eco-friendly packaging solutions.

Food Packaging Industry Segmentation

Food packaging encompasses the materials and containers used to wrap, protect, preserve, transport, and display food products. It is essential in the food supply chain to ensure food safety and hygiene, extend shelf life, and maintain food quality, convenience, and consumer information.

The food packaging market is segmented by type of material (plastic, metal, glass, and paper & paperboard), packaging type (rigid, semi-rigid, flexible), product type (cans, converted roll stock, gusseted box, corrugated box, and boxboard), application (dairy products, poultry & meat products, fruits & vegetables, and bakery & confectionery) and geography (North America, Europe, Asia-Pacific, and Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Type of Material | |

| Plastic | |

| Metal | |

| Glass | |

| Paper and Paperboard |

| By Packaging Type | |

| Rigid | |

| Semi Rigid | |

| Flexible |

| By Product Type | |

| Cans | |

| Converted Roll Stock | |

| Gusseted Box | |

| Corrugated Box | |

| Boxboard | |

| Other Packaging Types (Pouches and bottles) |

| By Application | |

| Dairy Products | |

| Poultry and Meat Products | |

| Fruits & Vegetables | |

| Bakery & Confectionery | |

| Other Applications (Seafood, Convenience Food, Snacks and Side Dishes, Sauces, Dressings, and Condiments) |

| By Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| Rest of the World |

Food Packaging Market Size Summary

The food packaging market is poised for substantial growth, driven by factors such as urbanization, increased demand for eco-friendly solutions, and heightened safety concerns. As lifestyles and food preferences evolve, particularly in developing regions, the market is experiencing a surge in demand for processed foods. This trend is further fueled by rising disposable incomes and the migration from rural to urban areas. Innovations in packaging technologies, including active and intelligent packaging, are enhancing the market's appeal. Companies are increasingly adopting biodegradable materials to meet environmental standards, although regulatory challenges from entities like the FDA and European Commission persist. The COVID-19 pandemic and geopolitical events, such as the Russia-Ukraine war, have also influenced the market dynamics, emphasizing the importance of packaging in preserving food quality and extending shelf life.

The Asia-Pacific region is witnessing significant growth in the food packaging market, driven by increased disposable incomes and a rising interest in healthy eating. The demand for packaged food is on the rise as consumers seek high-quality, nutritious options to combat lifestyle-related health issues. This shift is creating opportunities for both large and small packaging companies to cater to urban and convenience-oriented consumer bases. The market is characterized by intense competition, with numerous players offering customized and sustainable packaging solutions. Companies like Amcor, Smurfit Kappa, and Mondi are leading the charge in innovation, introducing recyclable and eco-friendly packaging materials. Recent developments, such as Walki's recyclable packaging for frozen foods and SIG's acquisition of Scholle IPN, highlight the industry's commitment to sustainability and efficiency in the supply chain.

Food Packaging Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Buyers/Consumers

-

1.2.2 Bargaining Power of Suppliers

-

1.2.3 Threat of New Entrants

-

1.2.4 Threat of Substitute Products

-

1.2.5 Intensity of Competitive Rivalry

-

-

1.3 Industry Value Chain Analysis

-

1.4 Assessment of the Impact of COVID-19 on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Type of Material

-

2.1.1 Plastic

-

2.1.2 Metal

-

2.1.3 Glass

-

2.1.4 Paper and Paperboard

-

-

2.2 By Packaging Type

-

2.2.1 Rigid

-

2.2.2 Semi Rigid

-

2.2.3 Flexible

-

-

2.3 By Product Type

-

2.3.1 Cans

-

2.3.2 Converted Roll Stock

-

2.3.3 Gusseted Box

-

2.3.4 Corrugated Box

-

2.3.5 Boxboard

-

2.3.6 Other Packaging Types (Pouches and bottles)

-

-

2.4 By Application

-

2.4.1 Dairy Products

-

2.4.2 Poultry and Meat Products

-

2.4.3 Fruits & Vegetables

-

2.4.4 Bakery & Confectionery

-

2.4.5 Other Applications (Seafood, Convenience Food, Snacks and Side Dishes, Sauces, Dressings, and Condiments)

-

-

2.5 By Geography

-

2.5.1 North America

-

2.5.1.1 United States

-

2.5.1.2 Canada

-

-

2.5.2 Europe

-

2.5.2.1 Germany

-

2.5.2.2 France

-

2.5.2.3 United Kingdom

-

2.5.2.4 Spain

-

2.5.2.5 Italy

-

2.5.2.6 Rest of Europe

-

-

2.5.3 Asia-Pacific

-

2.5.3.1 China

-

2.5.3.2 Japan

-

2.5.3.3 India

-

2.5.3.4 Australia

-

2.5.3.5 Rest of Asia-Pacific

-

-

2.5.4 Rest of the World

-

-

Food Packaging Market Size FAQs

How big is the Food Packaging Market?

The Food Packaging Market size is expected to reach USD 367.04 billion in 2024 and grow at a CAGR of 4.16% to reach USD 450.01 billion by 2029.

What is the current Food Packaging Market size?

In 2024, the Food Packaging Market size is expected to reach USD 367.04 billion.