Food Grade Lubricants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

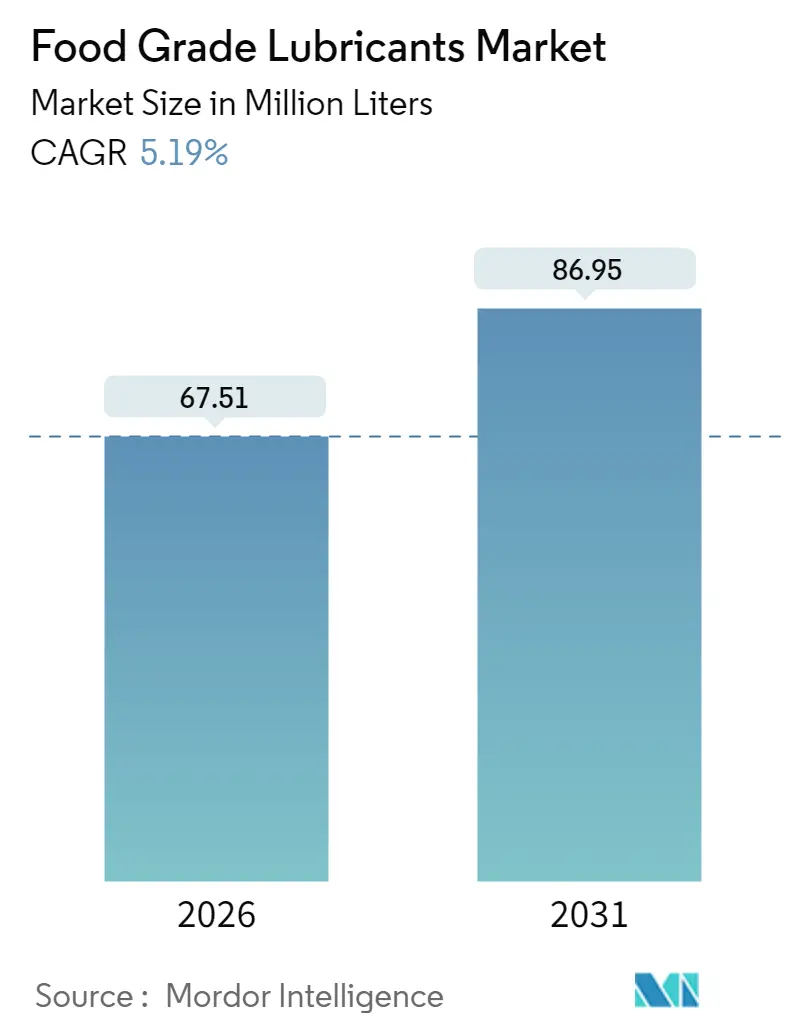

| Market Volume (2026) | 67.51 Million liters |

| Market Volume (2031) | 86.95 Million liters |

| Growth Rate (2026 - 2031) | 5.19% CAGR |

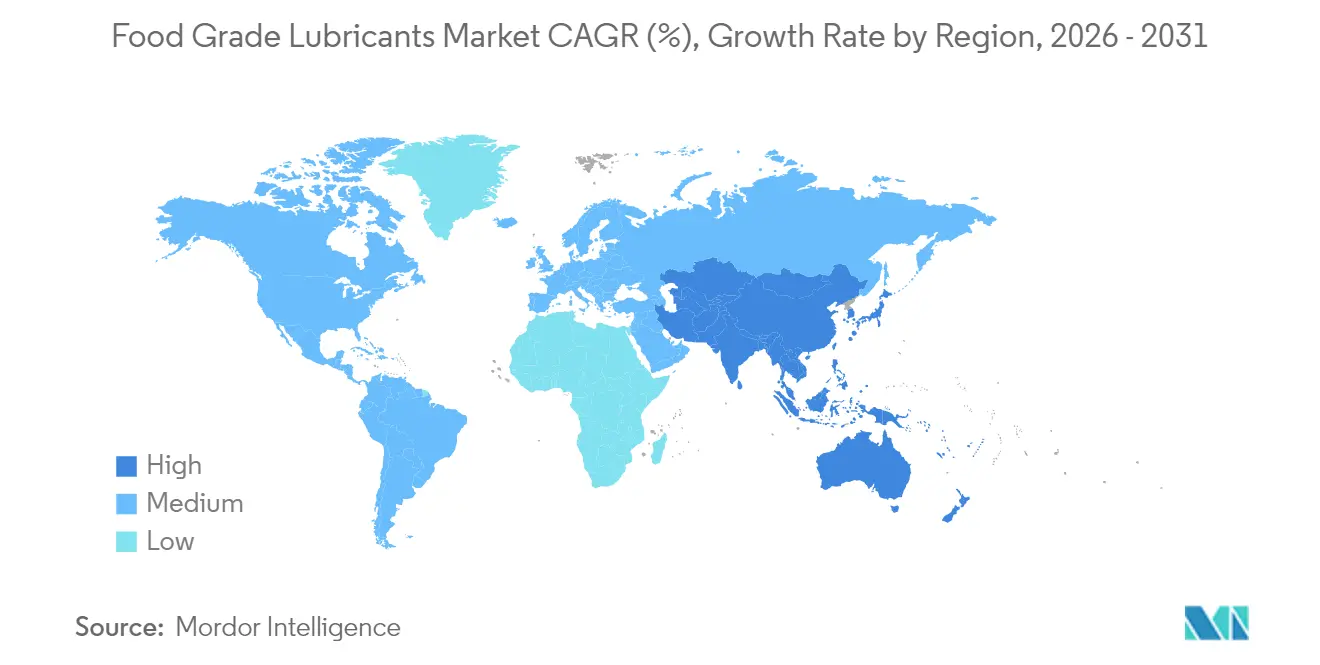

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

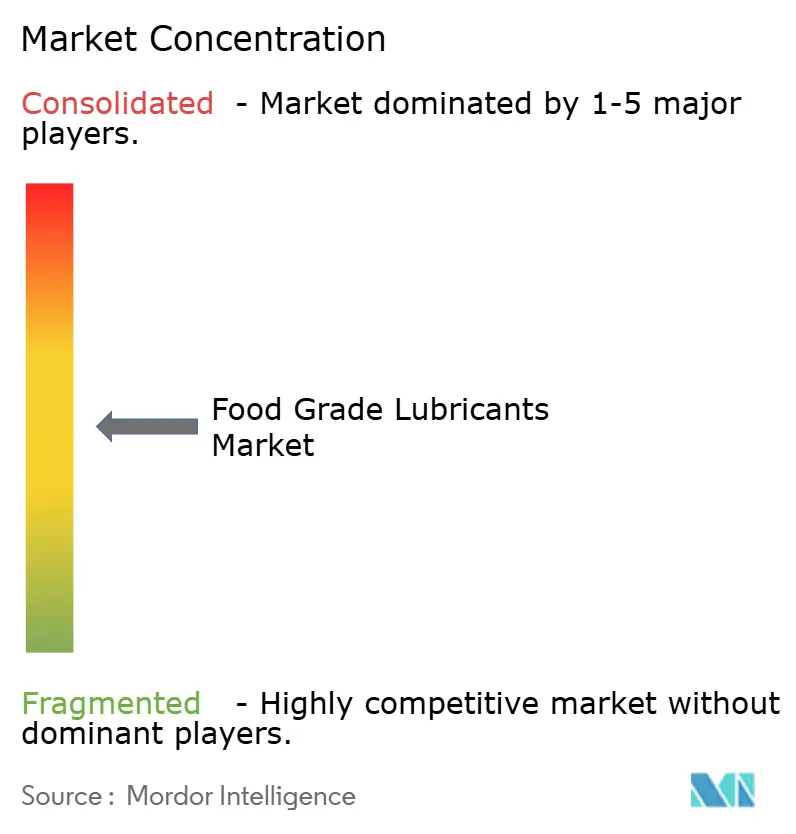

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Food Grade Lubricants Market Analysis by Mordor Intelligence

The Food Grade Lubricants Market was valued at 64.18 Million liters in 2025 and estimated to grow from 67.51 Million liters in 2026 to reach 86.95 Million liters by 2031, at a CAGR of 5.19% during the forecast period (2026-2031). The growth path mirrors stricter global food-safety regulations, faster factory automation, and the steady shift toward processed and ready-to-eat foods that demand safe, high-performance lubricants. Regulatory bodies in North America, Europe, and Asia are aligning on the phase-out of PFAS chemistries, pushing formulators toward synthetic and bio-based alternatives that meet both safety and sustainability targets. Established producers are turning deep compliance knowledge into a competitive moat, while equipment makers are specifying certified lubricants at the design stage to minimize contamination risk. Counterfeit “H1” products remain an operational threat, yet they also amplify the value proposition of traceable, fully certified solutions that safeguard brand reputation and reduce unplanned downtime.

Key Report Takeaways

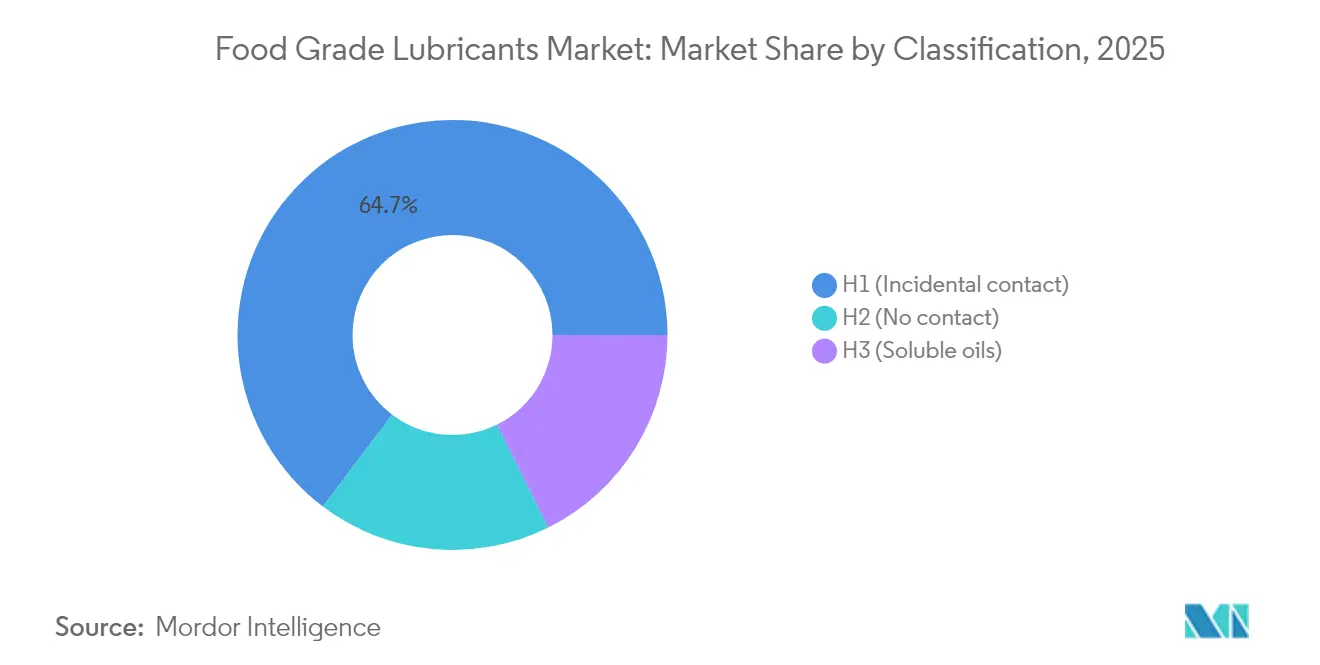

- By classification, H1 fluids held 64.70% of the food grade lubricants market share in 2025, while the same segment is forecast to post the highest growth at 5.52% CAGR through 2031.

- By base oil, mineral oil accounted for 52.08% share of the food grade lubricants market size in 2025; bio-based oils represent the fastest rising category at 5.86% CAGR through 2031.

- By product type, grease led with 39.10% revenue share in 2025; other product types together are projected to expand at a 6.01% CAGR to 2031.

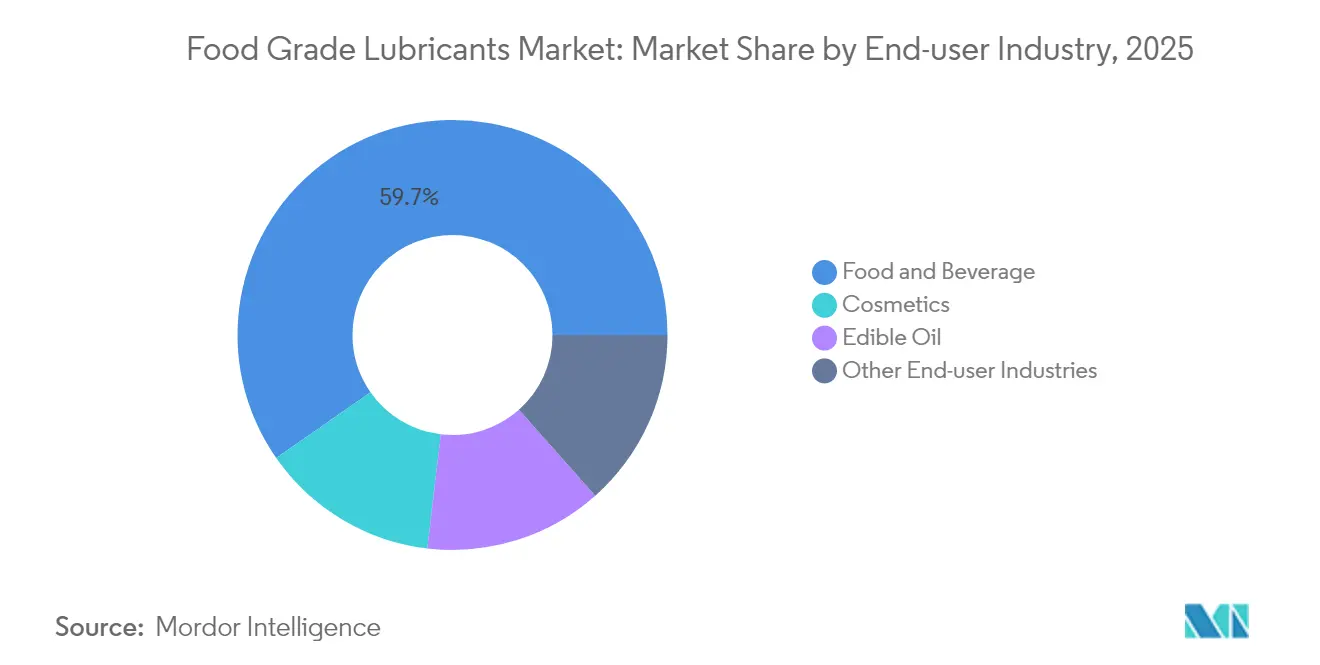

- By end-user industry, food and beverage processing commanded 59.70% of the food grade lubricants market size in 2025, whereas other end-user industries are set to grow at 6.05% CAGR over the same horizon.

- By geography, Europe held 38.80% revenue share in 2025, and Asia-Pacific is advancing at a 5.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Food Grade Lubricants Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing food-safety regulations tightening globally | +1.2% | Global, early North America and EU | Medium term (2-4 years) |

| Surge in demand for processed and ready-to-eat foods | +1.0% | APAC core, spill-over to MEA | Long term (≥4 years) |

| Rapid automation of food and beverage plants | +0.8% | Global, developed markets | Short term (≤2 years) |

| Expanding food processing infrastructure in developing regions | +0.7% | APAC, Latin America, MEA | Long term (≥4 years) |

| Phase-out of PFAS chemicals driving reformulation demand | +0.6% | North America and EU, expanding global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Food-Safety Regulations Tightening Globally

Governments are converging toward more rigorous food-contact rules, forcing lubricant suppliers to upgrade formulations or risk delisting. China’s updated GB 2760-2024 extends the country’s positive list and closes loopholes around processing aids, triggering demand for fully documented H1 fluids that align with NSF and ISO 21469 audits. In Europe, the EFSA evaluation of MOSH and MOAH has led processors to favor synthetic fluids that eliminate mineral-oil traces, while ISO 21469 certification now signals a higher assurance level than basic NSF registration. The U.S. FDA continues to police 21 CFR 178.3570, and more than 30 individual states have enacted PFAS bans that indirectly shape lubricant chemistry[1]United States Government, “21 CFR 178.3570 Lubricants With Incidental Food Contact,” ecfr.gov. Suppliers with global regulatory teams convert this complexity into value-added consulting for customers who lack in-house expertise. The cumulative effect lifts entry barriers and cements long-term contracts, fueling volume expansion across the food grade lubricants market.

Surge in Demand for Processed and Ready-To-Eat Foods Requiring Food-Grade Lubricants

Dietary patterns are pivoting to convenience meals, single-serve packages, and omnichannel grocery models that rely on high-throughput machinery. Food Industry 5.0 concepts, such as AI-enabled predictive maintenance, shorten acceptable downtime windows; lubricants, therefore, must deliver longer drain intervals and contamination immunity to justify their selection. As product SKU counts rise, changeover frequency increases, pushing lubricants to tolerate variable loads and temperatures. This synergy between convenience food growth and factory automation amplifies lubricant demand volume as well as performance expectations across the food-grade lubricants market.

Rapid Automation of Food and Beverage Plants Intensifying Lubricant Duty Cycles

Manufacturers are retrofitting legacy lines with hygienic robots and autonomous conveyors. Stäubli and ABB now offer IP69k-rated robots requiring H1 greases that survive hot-water sanitation without losing viscosity. Predictive algorithms reschedule lubricant changes to avert micro-stoppages, but only premium synthetic fluids sustain film strength over extended intervals. Around-the-clock operation doubles mechanical contact events compared with semi-automated lines, accelerating lubricant consumption curves. Capital expenditures on automated kit gain board approval partly because high-grade lubricants reduce the life-cycle cost of critical bearings, chains, and actuators. Equipment makers increasingly supply start-up lubricant kits with OEM branding, ensuring the food-grade lubricants market embeds itself early in the asset life and locks in multi-year aftermarket streams.

Phase-Out of PFAS Chemicals Driving Reformulation Demand

Environmental agencies on both sides of the Atlantic have drafted sweeping PFAS bans. Lubricant makers are racing to validate replacements for PTFE-laden greases used in high-temperature ovens and vacuum sealers. FUCHS’s RHEOLUBE 460P and Interflon’s MicPol series deliver comparable load-carrying capacity without fluorinated additives. Plastics converters are adopting Baerlocher’s Baerolub AID as a PFAS-free processing aid, demonstrating cross-industry acceptance. The reformulation wave raises research and development hurdles for small private-label blenders, favoring incumbents with global labs and pilot plants. End-users that eliminate PFAS also earn sustainability credits from retailers and insurers, reinforcing the pull toward certified, fluorine-free offerings and expanding high-margin segments within the food-grade lubricants market.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price premium vs. conventional industrial oils | -0.8% | Global, more pronounced in price-sensitive emerging markets | Short term (≤ 2 years) |

| Limited user awareness and training in emerging economies | -0.3% | APAC, Latin America, MEA | Medium term (2-4 years) |

| Proliferation of counterfeit/non-certified "H1" products | -0.4% | APAC, Latin America, MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Price Premium Vs. Conventional Industrial Oils

Synthetic H1 fluids still carry a 25% surcharge relative to ordinary mineral oils, deterring small processors that operate on razor-thin margins[2]Nancy McGuire, “Bio-based Greases: Back to the Future,” stle.org. Bio-based greases, which make up only 1-5% of total volume, face steeper premiums despite biodegradability advantages. In regions with lower labor costs and longer equipment replacement cycles, management often delays lubricant upgrades until compelled by audits or large retail clients. The price hurdle is expected to erode gradually as local blending, higher base-oil yields, and competition compress margins across the food grade lubricants market.

Proliferation of Counterfeit/Non-Certified “H1” Products

Unauthorized products masquerading as H1 fluids undermine brand trust and can trigger costly recalls. The American Petroleum Institute has already flagged multiple cases of fraudulent labeling on motor oils, signaling similar risks for specialty food-contact products. Counterfeits proliferate in fragmented distribution channels where buyers lack quick tools to verify NSF listings. Legitimate suppliers are responding with QR-coded drum labels, blockchain batch tracing, and education campaigns delivered through OEM service networks. While stricter enforcement will eventually shrink illicit supply, in the interim, the practice exerts downward price pressure and complicates safety audits, limiting volume growth prospects for bona-fide producers inside the food-grade lubricants market.

Segment Analysis

By Classification: H1 Fluids Cement Market Leadership while Elevating Safety Standards

H1 lubricants captured 64.70% of 2025 volume and are projected to widen their lead at 5.52% CAGR to 2031, cementing a dual role as dominant and fastest-growing segment in the food grade lubricants market share landscape. Processors favor H1 registration even for equipment deemed non-contact to offset contamination risk during maintenance or component failure. The food grade lubricants market size attributed to H1 products will therefore advance alongside more demanding ISO 21469 audits that now scrutinize biological as well as chemical hazards.

H2 fluids, once popular for sealed systems, now occupy a defensive niche as procurement teams prioritize universal compliance over theoretical exposure assessments. H3 soluble oils remain confined to specialized areas such as hook lubrication in meat plants where water-washability is paramount. The impending PFAS ban is indirectly reinforcing H1 loyalty because reformulated synthetics offer strong load capacity at wider operating temperatures, further eroding any perceived performance gap with H2 grades. As a result the classification mix is expected to tilt more heavily toward H1 throughout the forecast horizon, making certification expertise an indispensable pillar of competition within the food grade lubricants market.

Note: Segment shares of all individual segments available upon report purchase

By Base Oil: Mineral Oil Anchors Volume as Bio-Based Oils Accelerate

Mineral oil blends retained 52.08% share in 2025, securing their role as the volume anchor of the food grade lubricants market. The position rests on well-established supply chains, predictable additive response, and unit costs that suit high-volume bakeries and dairies. Even so, adoption of bio-based alternatives is running ahead of synthetics in percentage terms, clocking a 5.86% CAGR that outpaces the broader market. The food grade lubricants market size linked to bio-based products therefore remains small but is scaling quickly, propelled by corporate carbon targets and retailer pressure for “planet-friendly” sourcing.

Synthetic base stocks, though premium priced, attract processors running 24/7 automation where downtime risks dwarf fluid costs. Superior thermal range and resistance to aggressive cleaners extend drain intervals, slicing total lubricant-related maintenance tasks by double-digit margins in many plants.

By Product Type: Grease Dominance Endures Amid Rising Demand for Specialty Fluids

Grease held 39.10% share in 2025 owing to its indispensable role in bearings, gearboxes, and seals exposed to water, sugar dust, and frequent cleaning. Its thickening agents enable extended relubrication intervals and confer splash resistance, making it the default choice across bakeries, beverage bottlers, and confectionery lines. The food grade lubricants market size for greases will continue expanding in lockstep with conveyor installations and robotic pick-and-place stations that generate multi-directional loads.

Meanwhile compressor and chain oils form the fastest-expanding basket with a 6.01% CAGR outlook, reflecting wider adoption of spiral freezers, vacuum pumps, and high-speed ovens in automated facilities. Chain oils, in particular, must maintain film integrity under high loads while resisting carbon formation at temperatures topping 240 °C, a specification profile that favors high-tier synthetics.

By End-User Industry: Food and Beverage Core Remains Sturdy while Supply-Chain Equipment Surges

Food and beverage manufacturing absorbed 59.70% of 2025 volume, solidifying its role as the anchor sector for the food grade lubricants market. High-frequency operations, stringent audits, and the consumer backlash risk tied to contamination events ensure sustained investment in certified lubricants. The food grade lubricants market share will therefore stay skewed toward this sector through 2031 despite relative slowdown in mature economies.

Parallel growth momentum lies in packaging and logistics assets, forecast at 6.05% CAGR, as omnichannel retailing pushes producers to accommodate mixed package formats, shorter runs, and automated warehousing. Conveyor rollers, palletizers, and pick-to-light systems integrate food-contact zones, obliging operators to substitute general industrial greases with H1 equivalents.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Europe’s 38.80% share in 2025 stems from decades-old regulatory depth, dense processing infrastructure, and continuous improvement cultures that reward premium formulations. EFSA scrutiny of MOSH and MOAH pushes processors toward fully synthetic, low-aromatic blends, driving above-average unit prices and early adoption of PFAS-free options.

Asia-Pacific, though smaller today, registers the fastest pace at 5.74% CAGR, fueled by industrialization, dietary shifts, and tightening standards. China’s revised GB 2760-2024 elevates baseline compliance and favors multinational suppliers versed in multilayer certification. ASEAN food exporters are adopting international standards to gain EU and U.S. market access, broadening the addressable base for H1 fluids.

North America commands mature yet still dynamic demand, underpinned by FDA enforcement of incidental-contact rules and state-level PFAS bans that expedite formulation changeovers. Mexico’s processor base leverages NAFTA supply chains and requires dual-certified lubricants to satisfy cross-border audits.

South America, and the Middle-East and Africa remain early-stage, yet infrastructure spending and supermarket expansion are catalyzing upgrades from generic industrial oils to certified products. Brazil’s distribution partnership between Univar Solutions and Arxada underscores the race to establish credible supply in jurisdictions where counterfeit risk runs high.

Competitive Landscape

The food grade lubricants market remains moderately fragmented. Large multinationals such as ExxonMobil, FUCHS, Klüber Lubrication, TotalEnergies, and Petro-Canada capture the upper tier by virtue of proprietary additive chemistries, ISO 21469 plants, and global service footprints. These incumbents leverage vertical integration from base-oil production to on-site technical audits, delivering bundled value that offsets premium price points. Mid-tier specialists focus on regional coverage or niche applications such as high-temperature bakery chains, yet face rising CapEx needs to reformulate away from PFAS and to add NSF certification batches.

Food Grade Lubricants Industry Leaders

Condat

FUCHS

Exxon Mobil Corporation

Freudenberg SE

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: FUCHS completed the acquisition of the LUBCON Group, a manufacturer of high-performance specialty lubricants manufacturing products such as food-grade lubricants and more.

- October 2023: UMW Grantt International marked a significant step towards eco-friendly machinery operation with the introduction of a new biodegradable multi-purpose food-grade grease in the Malaysian market.

Global Food Grade Lubricants Market Report Scope

Food-grade lubricants are the kind of lubricants that protect against friction, corrosion, wear, oxidation, dissipating heat, and power transmission, as well as serve the purpose of a sealing effect in some cases. Food-grade lubricants are widely used in the food, beverages, and pharmaceutical industries. The food-grade lubricants market is segmented by food grade, product type, end-user industry, and geography. By food grade, the market is segmented into H1, H2, and H3. By product type, the market is segmented into grease, hydraulic fluid, gear oil, and other product types. By end-user industry, the market is segmented into food and beverage, cosmetics, edible oil, and other end-user industries. The report also covers the market size and forecasts for food-grade lubricants in 15 countries across the central regions. Each segment's market sizing and forecasts are based on revenue (USD million).

| H1 (Incidental contact) |

| H2 (No contact) |

| H3 (Soluble oils) |

| Mineral Oil |

| Synthetic Oil |

| Bio-based Oil |

| Grease |

| Hydraulic Fluid |

| Gear Oil |

| Other Products Types (Compressor Oil, Chain Oil, etc.) |

| Food and Beverage |

| Cosmetics |

| Edible Oil |

| Other End-user Industries (Packaging and Logistics Equipment, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Classification | H1 (Incidental contact) | |

| H2 (No contact) | ||

| H3 (Soluble oils) | ||

| By Base Oil | Mineral Oil | |

| Synthetic Oil | ||

| Bio-based Oil | ||

| By Product Type | Grease | |

| Hydraulic Fluid | ||

| Gear Oil | ||

| Other Products Types (Compressor Oil, Chain Oil, etc.) | ||

| By End-user Industry | Food and Beverage | |

| Cosmetics | ||

| Edible Oil | ||

| Other End-user Industries (Packaging and Logistics Equipment, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected size of the food grade lubricants market by 2031?

The market is anticipated to reach 86.95 million liters by 2031, expanding from 64.18 million liters in 2025 at a 5.19% CAGR.

Which lubricant classification holds the highest share today?

H1-certified lubricants dominate with 64.70% share in 2025, reflecting industry preference for incidental-contact safety.

Why are bio-based oils gaining traction in the food grade lubricants industry?

Bio-based oils are advancing at 5.86% CAGR because they help processors meet sustainability targets and comply with emerging PFAS and mineral-oil restrictions.

Which region is growing the fastest in the food grade lubricants market?

Asia-Pacific is the fastest-growing region, registering a 5.74% CAGR through 2031 due to rapid food factory build-outs and tightening local regulations.

How does the phase-out of PFAS chemicals affect lubricant suppliers?

Suppliers must reformulate away from fluorinated additives, creating first-mover advantages for companies that commercialize PFAS-free synthetics without performance loss.

Page last updated on: