| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 27.00 Billion |

| Market Size (2030) | USD 38.58 Billion |

| CAGR (2025 - 2030) | 7.40 % |

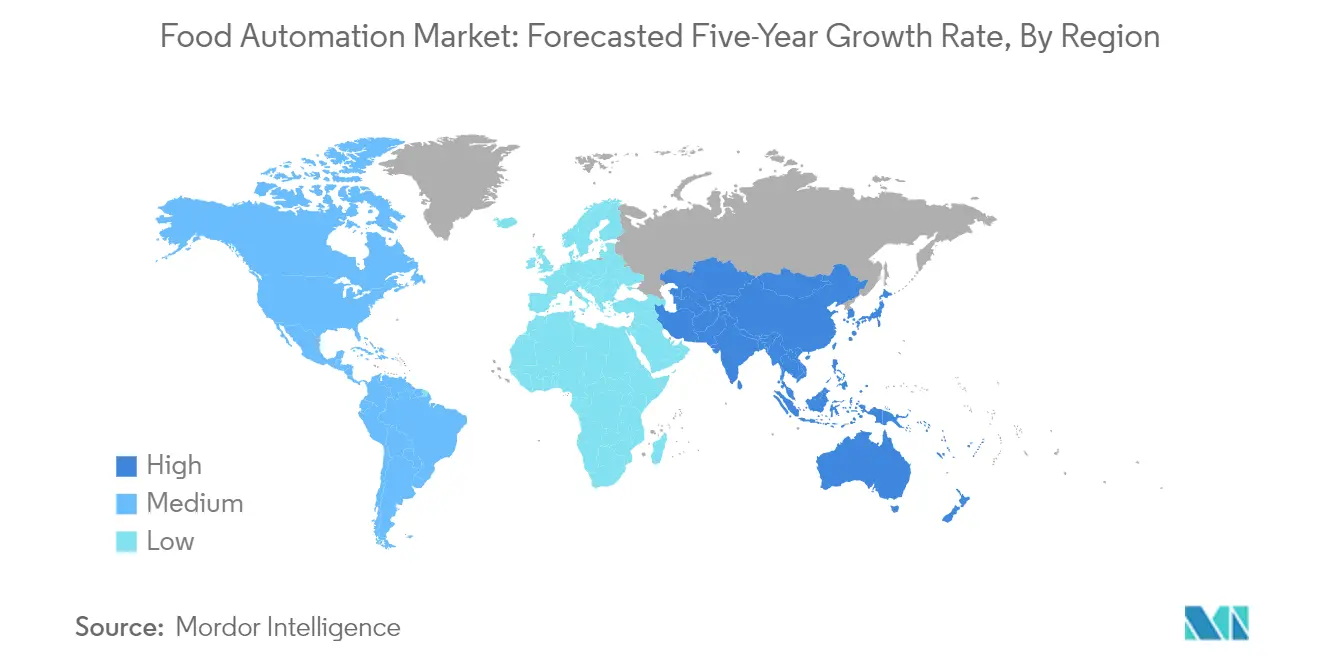

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Food Processing Automation Market Analysis

The Food Processing Automation Market size is estimated at USD 27.00 billion in 2025, and is expected to reach USD 38.58 billion by 2030, at a CAGR of 7.4% during the forecast period (2025-2030).

The food processing automation landscape is experiencing a significant transformation driven by technological advancements and changing consumer preferences. The beverage industry has emerged as a pioneering adopter of food industry automation and robotic solutions, enabling manufacturers to effectively combine slow batch production with high-speed filling operations. According to recent industry data, global beer production reached approximately 1.89 billion hectoliters in 2022, highlighting the massive scale of operations that require automated solutions. The integration of warehouse execution systems (WES) and process monitoring software with autonomous hardware has become increasingly prevalent, enabling real-time quality monitoring and predictive maintenance capabilities.

The dairy sector has witnessed substantial automation adoption, particularly in advanced markets. In the United States, milk production reached 226.6 billion pounds in 2022, demonstrating the scale of operations that necessitate automated solutions. Manufacturing facilities are increasingly implementing sophisticated control systems, robotics, and artificial intelligence to optimize production processes, enhance quality control, and ensure consistent output. This trend is particularly evident in Canada, where approximately 46% of food processors are actively investing in advanced and emerging technologies, with the food and beverage automation industry projected to grow by more than 11% by 2025.

Recent industry developments highlight the accelerating pace of automation adoption across various food processing segments. In 2023, significant investments were made in automated solutions, exemplified by HK Scan's EUR 4.6 million investment in automation levels at its Rauma, Finland poultry plant, aiming to achieve annual savings of EUR 3 million. Similarly, Coca-Cola launched a new Georgia facility featuring advanced 'mixed case palletizing' robotic technology, representing a USD 85 million investment that showcases the industry's commitment to cutting-edge automation solutions.

The industry is witnessing a notable shift toward integrated automation solutions that encompass multiple aspects of food processing and packaging. In 2023, Mettler-Toledo launched a fully automated, full-label inspection service for food manufacturers, while FZ Digital introduced cutting-edge automation and robotics technology to Singapore's F&B industry. These developments reflect the industry's focus on enhancing efficiency, ensuring product quality, and maintaining high safety standards through automated solutions. The trend is particularly evident in the beverage sector, where automated systems are being deployed to prevent fundamental mistakes in packaging, labeling, and handling processes.

Food Processing Automation Market Trends

Growing Emphasis on Food Safety and Rising Demand for Processed Food

The increasing emphasis on food safety and quality assurance has become a primary driver for automation in the food industry adoption. According to the US Centers for Disease Control and Prevention (CDC), 48 million people get sick, 128,000 are hospitalized, and 3,000 die due to diseases transmitted by contaminated food annually in the country. These alarming statistics have prompted food manufacturers to implement automated systems that can maintain consistent quality standards and minimize human contact during processing. Automation technologies, particularly in areas such as sorting, inspection, and packaging, help ensure compliance with stringent food safety regulations while reducing the risk of contamination.

The demand for processed food has witnessed substantial growth, driven by changing consumer lifestyles and increased urbanization. According to the Department of Commerce (India), in the fiscal year 2021, the export value of processed fruits, juices, and nuts from India was USD 780 billion, representing a significant increase from the previous fiscal year's USD 554 billion. This growing demand has necessitated the adoption of automated food processing solutions to enhance production efficiency and maintain consistent quality. Advanced processing technologies and automation solutions are being increasingly deployed to improve palatability, extend shelf-life, and ensure product safety while meeting the rising consumer demand for processed food products. The automation of various processes, from raw material handling to packaging and storage, has become crucial for manufacturers to maintain high production volumes while ensuring product quality and safety standards.

Understand The Key Trends Shaping This Market

Download PDF

Segment Analysis: By Operational Technology and Software

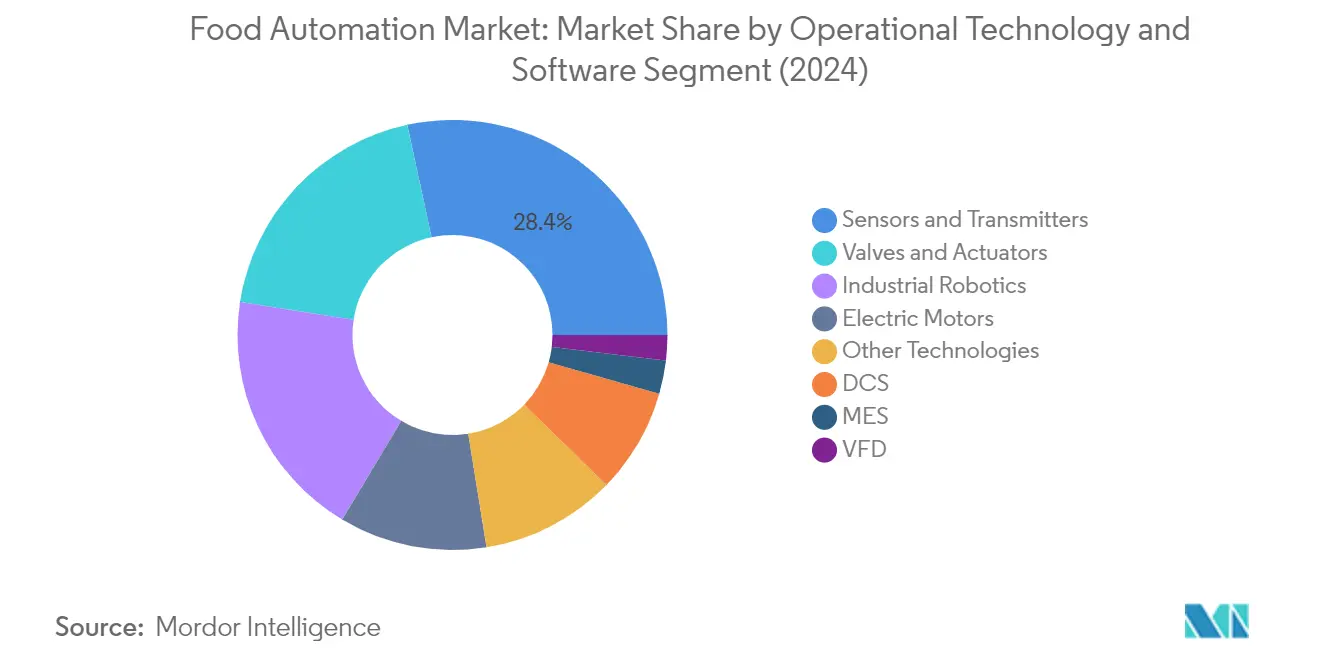

Sensors and Transmitters Segment in Food Automation Market

The sensors and transmitters segment dominates the food automation market, commanding approximately 28% market share in 2024, equivalent to USD 7,327.5 million. This segment's prominence is driven by the increasing adoption of IoT systems in food processing facilities, where sensors play a vital role in data collection, condition monitoring, and process optimization. The segment's growth is further accelerated by the development of advanced sensors with digital interfaces and enhanced functionality sets that enable users to operate more efficiently while reducing costs. Companies are increasingly focusing on developing sensors that contribute to food factory automation processes while being equipped with features like data collection and condition monitoring. For instance, in 2024, manufacturers are implementing high-resolution vision sensors for multiple inspections with a single image to generate rich data for process and quality control.

Remaining Segments in Food Automation Market

The food automation market encompasses several other significant segments including industrial robotics, valves and actuators, electric motors, distributed control systems (DCS), manufacturing execution systems (MES), and variable frequency drives (VFD). Industrial robotics has emerged as a crucial segment, particularly in applications such as packaging, palletizing, and material handling, while valves and actuators play a vital role in controlling fluid flow and pressure in food processing applications. Electric motors serve as the backbone of automation systems, powering various equipment from conveyor belts to mixing systems. DCS systems provide centralized control and monitoring capabilities, while MES solutions help optimize production processes and ensure quality control. VFD systems contribute to energy efficiency and precise motor control in food processing operations. Each of these segments brings unique capabilities and innovations to the food automation ecosystem, collectively driving the industry's technological advancement and operational efficiency.

Segment Analysis: By End-User Industry

Beverages Segment in Food Automation Market

The beverages segment dominates the global food automation market, commanding approximately 40% of the market share in 2024, equivalent to USD 10,212.3 million. This significant market position is primarily driven by the increasing market demand for both alcoholic and non-alcoholic beverages, which has encouraged vendors to adopt food processing robotics solutions to speed up production, packaging, and warehousing processes. The segment's dominance is further strengthened by the integration of warehouse execution systems (WES) and process monitoring software with autonomous hardware and production robots, enabling beverage manufacturers to access real-time data regarding quality and efficiency. Software solutions such as those tracking and improving beverage production processes have helped companies increase their output by up to 15% while reducing weekly unplanned downtime by about 65%.

Remaining Segments in Food Automation Market

The remaining segments in the food automation market include bakery and confectionery, dairy processing, meat, poultry, and seafood, fruits and vegetables, and other end-users. The bakery and confectionery segment holds a significant position with its extensive adoption of warehouse automation to minimize labor costs and product damage. The dairy processing segment focuses on complex production processes that require continuous monitoring and control. The meat, poultry, and seafood segment emphasizes automation for quality control and safety compliance, while the fruits and vegetables segment utilizes automation for sorting, grading, and packaging applications. These segments collectively contribute to the market's diverse application landscape, each addressing specific industry challenges and requirements through specialized food processing automation equipment solutions.

Segment Analysis: By Application

Packaging and Repackaging Segment in Food Automation Market

The packaging and repackaging segment dominates the food automation market as manufacturers increasingly adopt food robotics and automated food packaging solutions for food production and packaging processes. According to Food Safety Tech estimates, Chinese food and beverage clients invested approximately USD 196 million in robotic technology in 2024, while companies from the United States invested roughly USD 160 million, highlighting the segment's significant market share. The segment's leadership position is driven by several factors including the increasing need for supply chain integration, reduction in labor costs, and advancements in technologies such as wireless technology, autonomous control, and wearable computing. The adoption of digitization has enabled the use of cutting-edge technologies like cloud computing, sensors, virtualization, communication networks, robotics, and Industrial IoT, particularly in response to the rising demand for fresh, organic, and healthy foods and beverages. Major players in the F&B sector are emphasizing investment in digitalization to boost operational effectiveness and seize market opportunities.

Sorting and Grading Segment in Food Automation Market

The sorting and grading segment is experiencing rapid growth in the food automation market, driven by the increasing adoption of computer vision and artificial intelligence technologies. Modern sorting and grading systems utilize specialized algorithms in optical and visual grading systems to analyze multiple images of products across four key dimensions: size, shape, color, and external quality. The integration of deep learning and other modern methods has successfully countered the human factor dependence of traditional vision algorithms, enabling automatic learning and classification without manual tuning requirements. These advanced systems can handle various applications from fruit and vegetable sorting to complex quality control processes in food processing facilities. The segment's growth is further supported by the development of high-precision image recognition systems, automated quality inspection capabilities, and the increasing need for consistent product quality across the food processing industry.

Remaining Segments in Food Automation Market by Application

The palletizing segment continues to play a crucial role in the food automation market, particularly with the integration of robotic solutions and sensor-based systems that enhance quality and production throughput. The processing segment focuses on automating various food production tasks, incorporating artificial intelligence and machine learning to improve efficiency and product consistency. Other applications include specialized functions such as butchery and pick-and-place operations, which are increasingly being automated to improve precision and reduce manual labor requirements. These segments collectively contribute to the comprehensive automation ecosystem in the food industry, with each serving specific crucial functions in the overall food production and distribution chain. The adoption of these applications is driven by the industry's growing focus on efficiency, safety, and quality control in food processing automation operations.

Food Processing Automation Market Geography Segment Analysis

Food Automation Market in North America

North America represents a mature and technologically advanced market for food processing automation solutions, driven by stringent food safety regulations, high labor costs, and increasing demand for processed foods. The United States and Canada are the key markets in this region, with manufacturers increasingly adopting automation technologies to improve operational efficiency and maintain consistent product quality. The region benefits from a strong presence of major food automation companies and a well-established food processing industry market size infrastructure.

Food Automation Market in United States

The United States dominates the North American food automation industry, leveraging its extensive food processing industry in USA and technological capabilities. The country's food and beverage industry contributes significantly to its GDP, with automation playing a crucial role in maintaining high productivity levels. According to market analysis, the United States holds approximately 33% share of the global food automation global market in 2024. The country's focus on Industry 4.0 initiatives and IoT technologies in manufacturing has encouraged food processors to adopt advanced automation solutions, particularly in areas such as packaging, processing, and quality control.

Food Automation Market in Canada

Canada emerges as the fastest-growing market in the North American region, demonstrating strong potential for food automation adoption. The market is projected to grow at approximately 9% CAGR from 2024 to 2029. Canadian food processors are increasingly embracing automation solutions to address labor shortages and improve production efficiency. The country's robust food safety regulations and growing export-oriented food processing sector have been key drivers for automation adoption. Canadian manufacturers are particularly focusing on implementing advanced robotics and AI-driven solutions in their production facilities.

Food Automation Market in Europe

Europe represents a sophisticated market for food automation solutions, characterized by high technological adoption rates and stringent food safety standards. The region encompasses key markets including Germany, France, and the United Kingdom, each contributing significantly to the overall European food automation landscape. The European market benefits from strong research and development initiatives, particularly in Industry 4.0 technologies and robotics applications for food processing.

Food Automation Market in Germany

Germany stands as the largest food automation market in Europe, driven by its strong manufacturing base and technological leadership in industrial automation. The country accounts for approximately 26% of the European food automation market in 2024. German food manufacturers have been at the forefront of adopting advanced automation solutions, particularly in areas such as process control, packaging, and quality assurance. The country's emphasis on Industry 4.0 initiatives has further accelerated the adoption of smart manufacturing solutions in the food processing sector.

Food Automation Market in Germany - Growth Perspective

Germany continues to demonstrate robust growth potential, with the market expected to expand at approximately 8% CAGR from 2024 to 2029. The country's food processing sector is increasingly investing in advanced automation technologies to enhance productivity and maintain competitive advantage. German manufacturers are particularly focusing on implementing integrated automation solutions that combine robotics, artificial intelligence, and IoT capabilities. The strong presence of major automation solution providers and ongoing technological innovations continue to drive market growth.

Food Automation Market in Asia-Pacific

The Asia-Pacific region represents a dynamic and rapidly evolving market for food automation solutions, characterized by diverse market conditions across countries like China, India, and Japan. The region's food automation landscape is being shaped by increasing urbanization, rising labor costs, and growing demand for processed food products. Each country in the region presents unique opportunities and challenges, with varying levels of technological adoption and automation readiness.

Food Automation Market in China

China leads the Asia-Pacific food automation market, driven by its massive food processing industry and increasing focus on manufacturing automation. The country's food automation sector benefits from strong government support through initiatives like "Made in China 2025" and significant investments in industrial modernization. Chinese food manufacturers are rapidly adopting automation solutions to address labor challenges and improve production efficiency, particularly in areas such as packaging, processing, and quality control.

Food Automation Market in China - Growth Perspective

China continues to demonstrate exceptional growth potential in the food automation sector, maintaining its position as both the largest and fastest-growing market in the Asia-Pacific region. The country's food processing industry is undergoing rapid transformation through automation, driven by increasing labor costs and the need for consistent product quality. Chinese manufacturers are particularly focusing on implementing advanced robotics and AI-driven solutions, supported by strong domestic technology capabilities and government initiatives promoting industrial automation.

Food Automation Market in Latin America

Latin America represents an emerging market for food automation solutions, characterized by growing adoption of automation technologies across its food processing sector. The region's food automation landscape is being driven by increasing modernization of food processing facilities, rising labor costs, and growing demand for processed food products. While the market is still developing, manufacturers are increasingly recognizing the benefits of automation in improving productivity and maintaining consistent product quality. The region shows particular strength in areas such as beverage processing, meat processing, and dairy production automation.

Food Automation Market in Middle East & Africa

The Middle East & Africa region presents a growing market for food automation solutions, with increasing investments in food processing capabilities and automation technologies. The region's food automation sector is being driven by government initiatives to enhance food security and reduce dependence on imports. Manufacturers are increasingly adopting automation solutions to improve operational efficiency and maintain consistent product quality, particularly in areas such as dairy processing, beverage production, and packaging. The region shows significant potential for growth as food processors continue to modernize their facilities and adopt advanced automation technologies.

Get Analysis on Important Geographic Markets

Download PDF

Food Processing Automation Market Overview

Top Companies in Food Automation Market

The food automation companies market features prominent players including Schneider Electric, Rockwell Automation, Honeywell International, Emerson Electric, ABB, Mitsubishi Electric, Siemens, Yokogawa Electric, and Yaskawa Electric Corporation. These companies are actively pursuing product innovation through the development of advanced robotics, control systems, and IoT-enabled solutions specifically designed for food processing and packaging applications. The industry witnesses continuous strategic partnerships and collaborations to enhance technological capabilities and expand market reach, particularly in emerging economies. Companies are increasingly focusing on developing hygiene-compliant automation solutions, including food-grade robots, sanitary sensors, and clean-in-place systems. Operational agility is being achieved through the integration of digital twins, artificial intelligence, and machine learning capabilities into existing automation frameworks. Market leaders are also emphasizing the development of end-to-end automation solutions that can seamlessly integrate with existing food manufacturing infrastructure while ensuring compliance with food automation regulations.

Global Conglomerates Dominate Fragmented Market Structure

The food automation market exhibits a fragmented structure with a mix of global industrial conglomerates and specialized automation solution providers. Large multinational corporations leverage their extensive R&D capabilities, global distribution networks, and comprehensive product portfolios to maintain market leadership. These companies typically offer integrated solutions spanning multiple automation technologies, from basic control systems to advanced robotics and artificial intelligence-driven platforms. The market witnesses regular merger and acquisition activities as established players seek to acquire innovative startups and technology companies to enhance their technological capabilities and expand their product offerings.

The competitive landscape is characterized by the presence of both diversified industrial technology providers and specialized food processing automation companies. Regional players maintain a significant presence in specific geographical markets through their understanding of local requirements and established customer relationships. The industry sees continuous consolidation as larger players acquire smaller, specialized companies to gain access to specific technologies or regional markets. Companies are increasingly focusing on establishing strategic partnerships with system integrators and technology providers to enhance their service capabilities and market reach.

Innovation and Service Excellence Drive Growth

Success in the food industry automation systems market increasingly depends on companies' ability to deliver innovative, customizable solutions while maintaining high standards of service and support. Incumbent players are focusing on developing comprehensive automation platforms that integrate multiple technologies while ensuring ease of implementation and operation. Companies are investing in building strong service networks and technical support capabilities to provide rapid response times and minimize operational disruptions. The ability to offer solutions that address specific challenges in different food processing segments while ensuring compliance with evolving regulatory requirements has become crucial for maintaining market position.

Market contenders are gaining ground by focusing on specialized solutions for specific food processing applications and developing niche expertise. Companies are emphasizing the development of modular, scalable solutions that allow food manufacturers to gradually automate their operations based on their requirements and budget constraints. The industry witnesses increasing emphasis on developing solutions that address labor shortages while ensuring food safety and quality standards. Success factors include the ability to provide solutions that offer clear return on investment, minimize production downtime, and adapt to changing consumer preferences and regulatory requirements. Companies are also focusing on developing solutions that address sustainability concerns and energy efficiency requirements in food process automation operations.

Food Processing Automation Market Leaders

-

Schneider Electric SE

-

Rockwell Automation Inc.

-

Honeywell International Inc.

-

Emerson Electric Company

-

ABB Limited

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Food Processing Automation Market News

- Mar 2023: ForgeOS integrated with Rockwell's Logix controllers and design and simulation software by Rockwell and READY Robotics. The combination will make robot integration easier and reduce industrial automation deployment time to market.

- Jan 2023: Teway Food installed ABB's automated solution consisting of 10 IRB 6700 robots, 65 IRB 360 delta robots fast picking robots, three IRB 660 robots, and a 3D vision system to assist in identifying and locating products as they are fed to the line and upgraded its production line to meet the increasing demand for compound seasoning. TewayFood is the first company in the industry to use 3D vision-assisted robot positioning for feeding production lines as a result of these solutions.

Food Processing Automation Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

-

4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products and Services

- 4.3.5 Degree of Competition

- 4.4 Impact of COVID-19 on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Growing Emphasis on Food Safety and Rising Demand for Processed Food

-

5.2 Market Challenges

- 5.2.1 High Capital Investments

6. INDUSTRY STANDARDS AND REGULATIONS

7. MARKET SEGMENTATION

-

7.1 By Operational Technology and Software

- 7.1.1 Distributed Control System (DCS)

- 7.1.2 Manufacturing Execution Systems (MES)

- 7.1.3 Variable-frequency Drive (VFD)

- 7.1.4 Valves and Actuators

- 7.1.5 Electric Motors

- 7.1.6 Sensors and Transmitters

- 7.1.7 Industrial Robotics

- 7.1.8 Other Technologies

-

7.2 By End User

- 7.2.1 Dairy Processing

- 7.2.2 Bakery and Confectionary

- 7.2.3 Meat, Poultry, and Seafood

- 7.2.4 Fruits and Vegetables

- 7.2.5 Beverages

- 7.2.6 Other End Users

-

7.3 By Application

- 7.3.1 Packaging and Repackaging

- 7.3.2 Palletizing

- 7.3.3 Sorting and Grading

- 7.3.4 Processing

- 7.3.5 Other Applications

-

7.4 By Geography

- 7.4.1 North America

- 7.4.1.1 United States

- 7.4.1.2 Canada

- 7.4.2 Europe

- 7.4.2.1 United Kingdom

- 7.4.2.2 Germany

- 7.4.2.3 France

- 7.4.3 Asia

- 7.4.3.1 China

- 7.4.3.2 India

- 7.4.3.3 Japan

- 7.4.3.4 Australia and New Zealand

- 7.4.4 Latin America

- 7.4.5 Middle East and Africa

8. VENDOR MARKET SHARE ANALYSIS

- 8.1 Vendor Market Share Analysis (Excl. Industrial Robots)

- 8.2 Vendor Market Share Analysis for Industrial Robots

9. COMPETITIVE LANDSCAPE

-

9.1 Company Profiles

- 9.1.1 Schneider Electric SE

- 9.1.2 Rockwell Automation Inc.

- 9.1.3 Honeywell International Inc.

- 9.1.4 Emerson Electric Company

- 9.1.5 ABB Limited

- 9.1.6 Mitsubishi Electric Corporation

- 9.1.7 Siemens AG

- 9.1.8 Yokogawa Electric Corporation

- 9.1.9 Yaskawa Electric Corporation

- 9.1.10 GEA Group AG

- 9.1.11 Rexnord Corporation (Regal Rexnord Corporation)

- *List Not Exhaustive

10. INVESTMENT ANALYSIS AND OUTLOOK

**Subject to Availability

*** In the Final Report Asia, Australia and New Zealand will be Studied Together as 'Asia Pacific', the report will also include 'Rest of Europe', and 'Rest of the Asia-Pacific'.

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Food Processing Automation Market Industry Segmentation

Automation in the food industry simplifies the food packaging process, which includes food sorting and grading, packing, and managing processes. Automation is an effective solution for enterprises requiring an efficient solution for overcoming numerous challenges, such as enhancing productivity, improving yield, optimizing resource management, mitigating security risks, and improving asset management.

The food automation market is segmented by operational technology and software (distributed control systems (DCS), manufacturing execution systems (MES), variable-frequency drive (VFD), valves and actuators, electric motors, sensors and transmitters, and industrial robotics), end user (dairy processing, bakery and confectionery, meat, poultry, and seafood, fruits and vegetables, and beverages), application (packaging and repackaging, palletizing, sorting and grading, and processing), geography (North America (United States and Canada), Europe (United Kingdom, Germany, France, and Rest of Europe), Asia-Pacific (China, India, Japan, and Rest of Asia-Pacific), Latin America, and Middle-East and Africa). The report offers the market size in value terms in USD for all the abovementioned segments.

| By Operational Technology and Software | Distributed Control System (DCS) | ||

| Manufacturing Execution Systems (MES) | |||

| Variable-frequency Drive (VFD) | |||

| Valves and Actuators | |||

| Electric Motors | |||

| Sensors and Transmitters | |||

| Industrial Robotics | |||

| Other Technologies | |||

| By End User | Dairy Processing | ||

| Bakery and Confectionary | |||

| Meat, Poultry, and Seafood | |||

| Fruits and Vegetables | |||

| Beverages | |||

| Other End Users | |||

| By Application | Packaging and Repackaging | ||

| Palletizing | |||

| Sorting and Grading | |||

| Processing | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Asia | China | ||

| India | |||

| Japan | |||

| Australia and New Zealand | |||

| Latin America | |||

| Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Food Processing Automation Market Research FAQs

How big is the Food Processing Automation Market?

The Food Processing Automation Market size is expected to reach USD 27.00 billion in 2025 and grow at a CAGR of 7.40% to reach USD 38.58 billion by 2030.

What is the current Food Processing Automation Market size?

In 2025, the Food Processing Automation Market size is expected to reach USD 27.00 billion.

Who are the key players in Food Processing Automation Market?

Schneider Electric SE, Rockwell Automation Inc., Honeywell International Inc., Emerson Electric Company and ABB Limited are the major companies operating in the Food Processing Automation Market.

Which is the fastest growing region in Food Processing Automation Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Food Processing Automation Market?

In 2025, the North America accounts for the largest market share in Food Processing Automation Market.

What years does this Food Processing Automation Market cover, and what was the market size in 2024?

In 2024, the Food Processing Automation Market size was estimated at USD 25.00 billion. The report covers the Food Processing Automation Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Food Processing Automation Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Food Processing Automation Market Research

Mordor Intelligence provides comprehensive industry analysis and market outlook for the food automation market, offering detailed insights into market size, growth trends, and competitive dynamics. Our research methodology combines extensive primary and secondary research to deliver accurate market forecasts and strategic insights about food processing automation, food robotics, and automated food production systems. The report pdf includes in-depth analysis of emerging technologies, regulatory frameworks, and market opportunities across key segments like food processing equipment and automated food packaging solutions.

Our consulting expertise extends beyond traditional market research to provide actionable intelligence for stakeholders in the food and beverage automation sector. We assist clients with technology scouting to identify cutting-edge food automation solutions, conduct detailed competition assessment of food automation companies, and provide strategic insights for new product launches in the food processing automation equipment space. Our team specializes in analyzing customer needs and behavior patterns specific to food factory automation, helping businesses optimize their automation strategies and maximize ROI. Through data aggregation and advanced analytics, we help clients navigate the complex landscape of automation in food processing industry and make informed decisions about technology investments and market expansion.