Fluid Power Equipment Market Size

| Study Period | 2022 - 2029 |

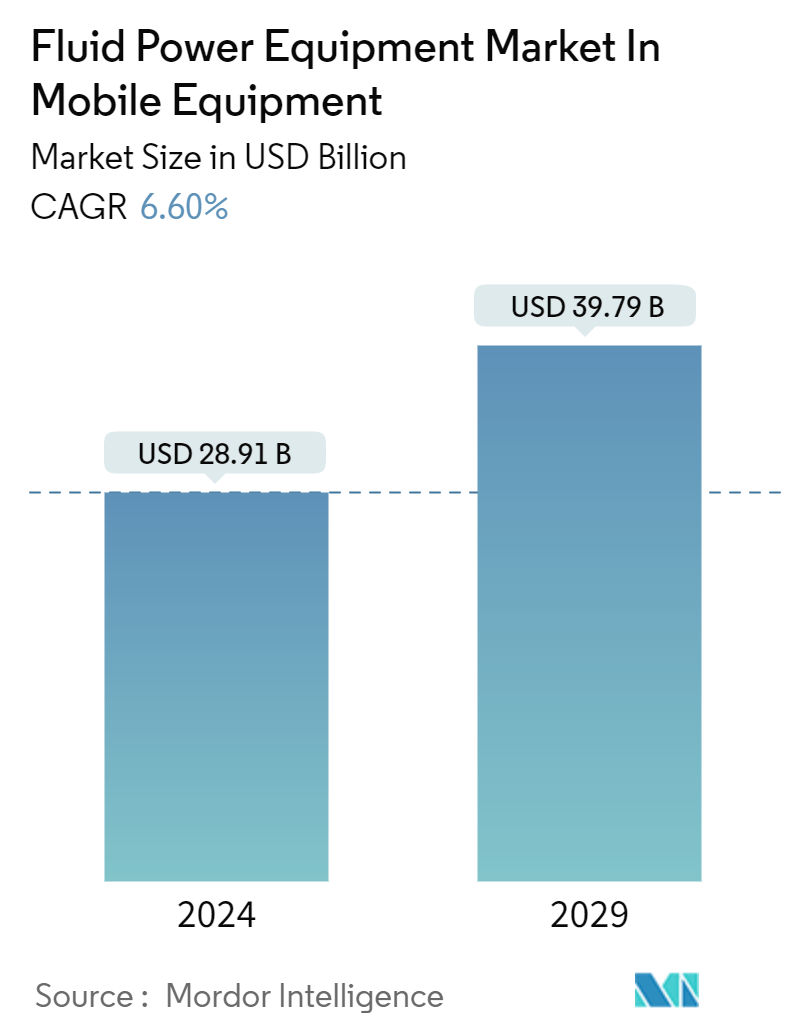

| Market Size (2024) | USD 28.91 Billion |

| Market Size (2029) | USD 39.79 Billion |

| CAGR (2024 - 2029) | 6.60 % |

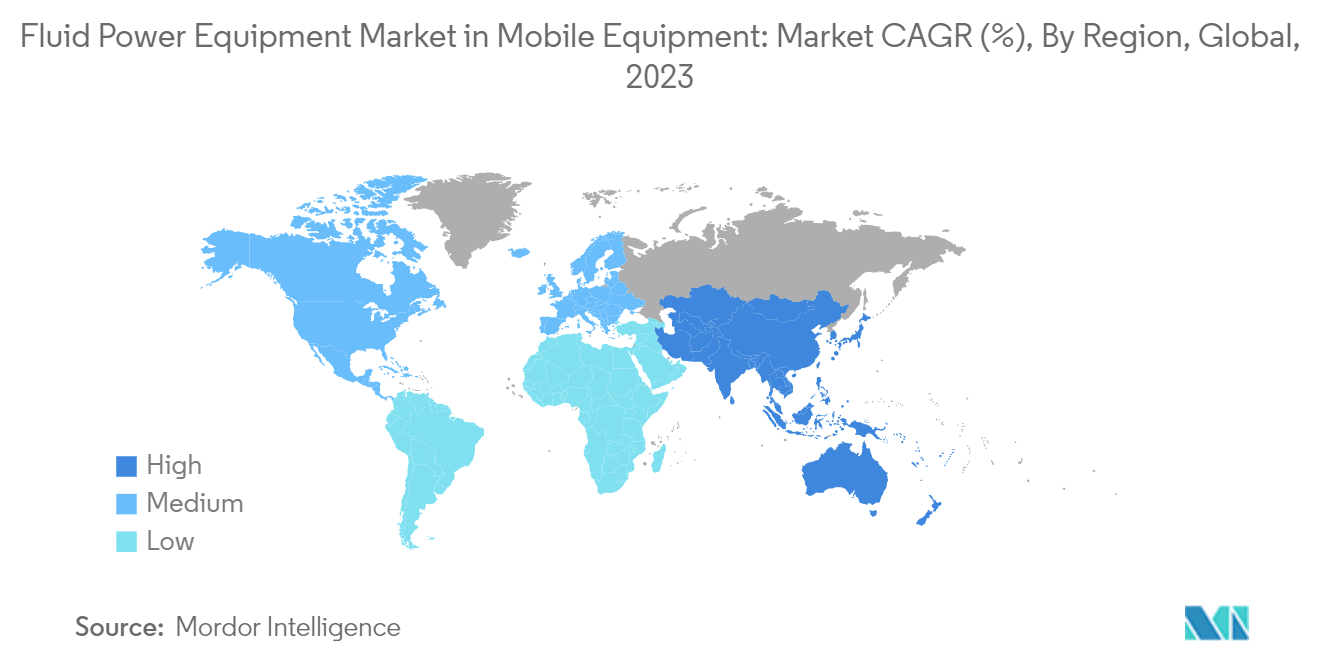

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

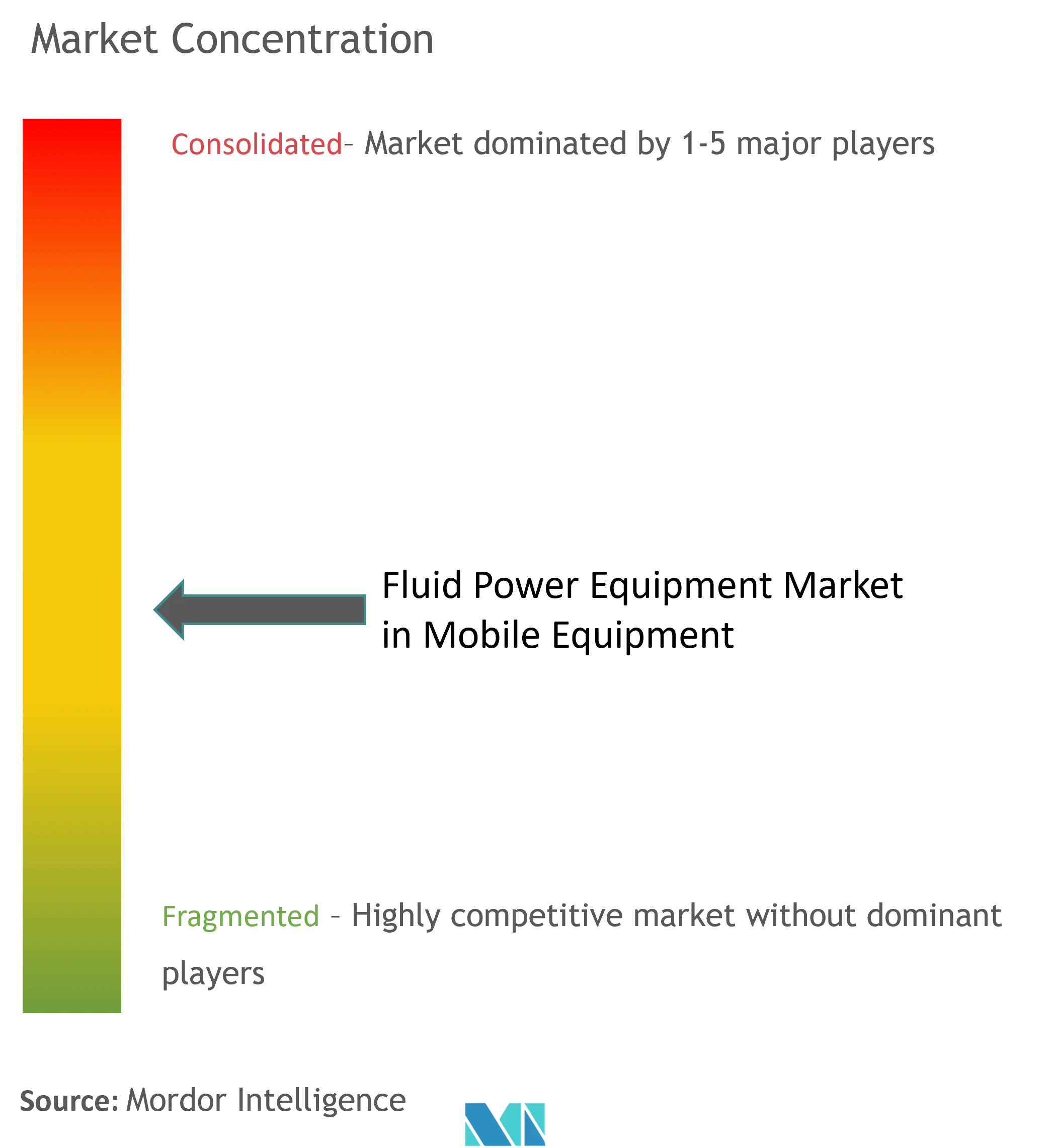

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Fluid Power Equipment Market Analysis

The Fluid Power Equipment Market In Mobile Equipment Industry is expected to grow from USD 28.91 billion in 2024 to USD 39.79 billion by 2029, at a CAGR of 6.60% during the forecast period (2024-2029).

- Fluid power equipment refers to devices and systems that utilize fluids, such as liquids or gases, to generate, control, and transmit power. This technology is widely used in several industries and applications like construction, manufacturing, transportation, and automation.

- Fluid power equipment can be primarily categorized into two types: hydraulic and pneumatic systems. Hydraulic systems use liquids, typically oil or water-based fluids, to transmit power, while pneumatic systems use compressed gases, such as air or nitrogen. The components of fluid power equipment include motors, pumps, valves, cylinders, filters, actuators, and others. These components work together to generate and control the fluid flow, allowing for energy conversion into mechanical work.

- Fluid power equipment, specifically hydraulics and pneumatics, is extensively used in mobile equipment within the material handling industry. One critical application of fluid power equipment in material handling is the operation of hydraulic lifts and cranes. Forklifts use hydraulic systems to raise and lower their forks, allowing for the movement of pallets and heavy loads. By utilizing hydraulic power, forklifts can perform these tasks easily and precisely, improving the efficiency and safety of material handling operations.

- Moreover, mobile equipment such as automated guided vehicles (AGVs) and aerial work platforms also utilize fluid power equipment. AGVs use hydraulic or pneumatic systems to power their propulsion, steering, and lifting mechanisms. These vehicles are widely employed in warehouses and distribution centers for transporting goods efficiently and autonomously.

- Aerial work platforms, commonly used in construction and maintenance activities, rely on fluid power equipment to provide stability, control, and precise movement in elevated work environments. The increasing automation across several industries is anticipated to aid the development of the market studied.

- Fluid power systems, such as hydraulic and pneumatic systems, offer high power-to-weight ratios and precise control, improving performance and productivity. Mobile equipment manufacturers constantly seek ways to enhance reduce downtime, operational efficiency, and increase overall productivity, driving the demand for fluid power equipment.

- Additionally, safety is a significant concern in the mobile equipment industry. Fluid power systems provide reliable and robust solutions for applications that require high force, speed, and control. Hydraulic braking systems, for example, offer superior stopping power and stability, ensuring the safe operation of vehicles and machinery. The industry's focus on safety regulations and the need for reliable equipment further drive the demand for fluid power systems in mobile equipment.

- Integrating intelligent control systems is anticipated to be a significant trend in fluid power equipment. With advancements in AI and ML, mobile equipment can utilize sophisticated control algorithms to optimize efficiency and performance. Intelligent control systems can monitor and adjust fluid power parameters in real-time, improving energy efficiency, reducing wear and tear, and enhancing overall equipment performance.

- The ongoing shift toward electrification in various industries is influencing the fluid power equipment in mobile equipment. Electric systems are cleaner, quieter, and more energy-efficient than their conventional hydraulic and pneumatic counterparts. As a result, manufacturers are exploring ways to incorporate electric actuators and motors in mobile equipment. Additionally, hybrid systems, combining fluid power and electric components, are gaining traction, offering the advantages of both technologies.

- However, the sophisticated technology and components involved in fluid power systems make them expensive to manufacture and purchase. This cost factor often deters potential buyers, significantly smaller businesses or individuals with limited budgets, from investing in fluid power equipment for their mobile equipment. These systems require skilled personnel for installation, maintenance, and repair. The lack of trained professionals or the need for specialized training can pose challenges for end users, limiting their ability to utilize and maintain fluid power equipment fully.

- The conflict between Russia and Ukraine will significantly impact the electronics industry. The conflict has already exacerbated the electronics and semiconductor supply chain disruption and the chip shortage that have affected the industry for some time. The disruption may result in volatile pricing for critical raw materials such as nickel, palladium, copper, titanium, and aluminum, resulting in material shortages. This, in turn, could impact the manufacturing of fluid power equipment.

Fluid Power Equipment Market Trends

The Construction Segment is Expected to Drive the Market's Growth

- Fluid power equipment plays a crucial role in the construction industry. Excavators are critical machines in the construction industry for digging, lifting, and moving heavy loads. Hydraulic systems power these versatile machines, allowing operators to perform tasks precisely and efficiently. Hydraulic cylinders control the activity of the boom and arm, enabling operators to extend, retract, and lift heavy materials.

- Hydraulic systems control the closing and opening of the bucket, allowing for efficient digging and dumping of materials. Fluid power equipment powers the tracks and swing mechanism, enabling the excavator to move and rotate smoothly.

- Additionally, cranes are essential for lifting and moving heavy loads on construction sites. Pneumatic systems use compressed air and are commonly employed in crane operations. Pneumatic cylinders provide the force required to lift and lower loads, ensuring safe and efficient operations. Pneumatic systems control the extension and retraction of the crane's boom, allowing for versatile reach and precision.

- Moreover, bulldozers are powerful machines used for earthmoving and leveling tasks on construction sites. Fluid power equipment controls the up and down movement of the bulldozer blade, allowing for efficient pushing and leveling of materials. Hydraulic systems also enable easy and precise steering control, enhancing maneuverability and productivity.

- With rapid urbanization and infrastructure projects worldwide, the demand for construction machinery and vehicles is rising. For instance, according to UN DESA, it is estimated that 78.9% of Germany's population will live in urban areas by 2030 and a further 84.3% by 2050. In September 2023, the German government announced to invest EUR 45 billion into the construction industry amid the housing crisis. To address the housing shortage, Berlin has committed to spending EUR 18 billion until 2027 on developing affordable housing, with additional state and federal government funding.

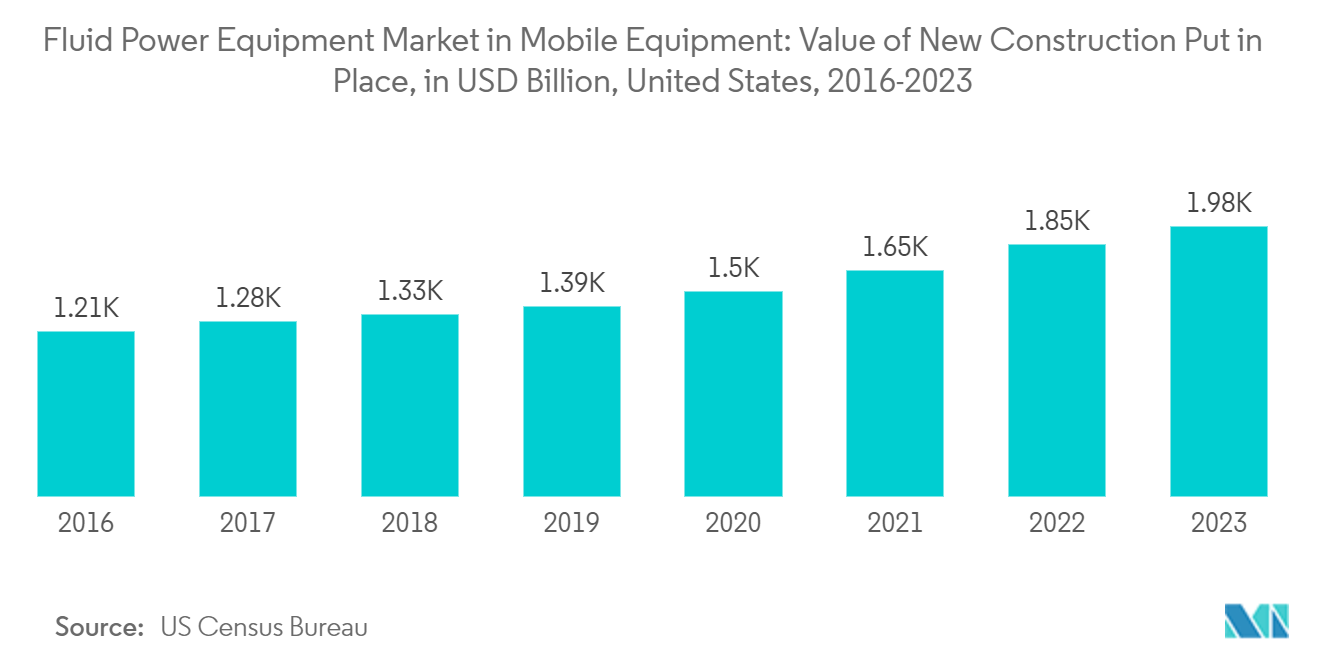

- According to the US Census Bureau, the value of overall construction output in the United States grew by over USD 131 billion in 2023, compared to the previous year. That refers to all construction activities, including the construction of buildings and infrastructure, as well as other specialized activities, such as roofing, HVAC, and plumbing installation. The increasing construction activities worldwide are likely to offer several opportunities for the growth of the market studied.

The Asia-Pacific Region is Expected to Witness a High Market Growth Rate

- Fluid power equipment plays a crucial role in the mobile equipment landscape in the Asia-Pacific region. With rapid urbanization and industrialization in countries like China, India, and Japan, the demand for construction and agriculture machinery has surged, driving the need for efficient fluid power systems.

- In the Asia-Pacific region, where construction and agriculture are major industries, fluid power equipment is essential for excavators, bulldozers, loaders, and other earthmoving equipment. These machines require precise control and high-power output, which can be achieved through hydraulic systems. Similarly, pneumatic systems are widely used in equipment like air compressors and drilling rigs.

- China's 14th Five Year Plan highlights new infrastructure projects in transportation, water systems, energy, and new urbanization. According to estimates by the International Trade Administration, the investment in latest infrastructure during the 14th Five Year Plan period (2021-2025) would reach approximately CNY 27 trillion (USD 4.2 trillion). The new plan accentuated nine crucial items for green building development and energy efficiency; it also comprises retrofitting more than 350 million square meters of buildings and constructing more than 50 million square meters of buildings that comsume net zero energy.

- The construction industry in China has witnessed an enormous increase due to sustainable construction policies. Over the past few years, a shift toward a service-led economy has also contributed to China's construction sector's growth. Investing in large-scale infrastructure projects has been an essential part of the Chinese government's strategy to boost growth. According to the National Bureau of Statistics of China, in 2022, the construction industry in China generated an output of over CNY 31 trillion, representing an increase of almost 100% from a decade ago. In 2020 and 2021, the construction industry in China generated an output of CNY 26.39 trillion and CNY 29.31 trillion, respectively. It is projected that the construction revenue in China will amount to approximately USD 4,159.03 billion by 2025.

- In the mining handling industry, excavators are commonly used for digging and loading materials. These machines use hydraulic systems to power their boom, arm, and bucket operations. The hydraulic cylinders in the excavator's boom and arm allow for precise control of digging depth and reach, while the hydraulic motors provide the necessary power for bucket movements. This fluid power technology enables excavators to efficiently extract and handle large quantities of ore and other materials in mining operations. Conveyor systems, which transport bulk materials from one location to another, often rely on hydraulic systems for efficient operation. Hydraulic cylinders are used to control the movement and positioning of conveyor belts, allowing for precise loading and unloading of materials. This fluid power technology ensures a continuous and reliable material flow, enhancing productivity in mining handling operations.

- According to MOSPI (Ministry of Statistics and Programme Implementation), at the end of FY2022, the mining industry's production in India increased by approximately 12%. The data for FY2023 indicated that the mining industry's production growth rate would be nearly 4.7%. The recovering mining industry in the Asia-Pacific region is likely to drive the development of the market studied .

Fluid Power Equipment Industry Overview

The fluid power equipment market in mobile equipment is a moderately fragmented market with the presence of major players like Kawasaki Precision Machinery, Bosch-Rexroth AG, Parker Hannifin Corporation, Danfoss AS, Eaton Corporation, and Hydac International GmbH. The market players are striving to innovate new products by way of extensive investments in R&D, collaborations, and mergers to cater to the evolving demands of consumers.

- November 2023: Danfoss Power Solutions showcased a range of hydraulic components and solutions for autonomy & electrification during Agritechnica 2023 – one of the most significant international events for the agriculture industry. The company exhibited its diverse range of electric, hydraulic, and fluid conveyance components for usage in agricultural equipment. It also featured its complete autonomy offering including its Autonomous Custom Engineering Services (ACES).

- March 2023: Parker Hannifin showcased a variety of its new technologies at IFPE 2023. It featured the company's latest and evolved products in smart electrification technology portfolio aimed at enabling battery-powered machines. Parker displayed its next-generation inverter with built-in functional safety. The Global Vehicle Inverter (GVI) utilizes the same hardware with two different software configurations to provide traction control or hydraulic work functions. The GVI inverter is claimed to be able to control an EHP Series Configured ePump, which comprises Global Vehicle Motor (GVM) directly coupled to a hydraulic pump.

Fluid Power Equipment Market Leaders

-

Kawasaki Precision Machinery

-

Bosch-Rexroth AG

-

Parker Hannifin Corporation

-

Danfoss AS

-

Eaton Corporation

*Disclaimer: Major Players sorted in no particular order

Fluid Power Equipment Market News

- February 2024: Power management company Eaton announced that its Mobility Group is expanding its mobile power products portfolio with the introduction of the Bezares 3960, 2500, and 500 series power takeoff (PTO) units, as well as APSCO APV and APG series directional hydraulic control valves. The new offerings are expected to be introduced at the Work Truck Show, March 5-8 in Indianapolis.

- July 2023: Bosch Rexroth opened a new plant in Querétaro, Mexico, with a vision to create more manufacturing capacity for mobile hydraulics and factory automation in North America and shorten delivery routes for customers in the region. The company claimed that it is investing about EUR 160 million in the new location and would create about 900 jobs by 2027. At its 42,000-square-meter, or 452,000-square-foot, plant in Querétaro, the company began manufacturing hydraulic pumps, motors, and valves for mobile machinery, like excavators, forklifts, and tractors, in June 2023.

Fluid Power Equipment Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Technological Trends

4.3 Industry Supply Chain Analysis

4.4 Industry Attractiveness - Porter's Five Forces Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

4.4.6 Threat of New Entrants

4.5 Impact of Macro Trends (Aftereffects of COVID-19, Supply Chain Issues, Economic Downturns, etc.) on the Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Growing Construction and Infrastructure Development

5.1.2 Growing Need for Increased Efficiency and Productivity

5.1.3 Increasing Advancements in Technology

5.2 Market Restraints

5.2.1 High Initial Cost of Fluid Power Equipment

6. MARKET SEGMENTATION

6.1 By Product Type

6.1.1 Hydraulics

6.1.1.1 Pumps

6.1.1.2 Motors

6.1.1.3 Valves

6.1.1.4 Cylinders

6.1.1.5 Accumulators and Filters

6.1.1.6 Other Product Types (Transmission, Fluid Connectors, etc.)

6.1.2 Pneumatics

6.1.2.1 Valves

6.1.2.2 Actuators

6.1.2.3 FRLs

6.1.2.4 Fittings

6.1.2.5 Other Product Types (Grippers, Guns, Positioners, and Nozzles)

6.2 By End-user Vertical

6.2.1 Construction

6.2.2 Agriculture

6.2.3 Material Handling

6.2.4 Mining

6.2.5 Other End-user Verticals (Commercial Vehicles, Marine, Municipal Vehicles, Drilling Machines and Other niche markets)

6.3 By Geography

6.3.1 North America

6.3.2 Asia

6.3.3 Europe

6.3.4 Latin America

6.3.5 Middle East and Africa

6.3.6 Australia and New Zealand

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 Kawasaki Precision Machinery

7.1.2 Bosch-Rexroth AG

7.1.3 Parker Hannifin Corporation

7.1.4 Danfoss AS

7.1.5 Eaton Corporation

7.1.6 Hydac International GmbH

7.1.7 HydraForce Inc.

7.1.8 Festo Corporation

7.1.9 SMC Corporation

- *List Not Exhaustive

7.2 Vendor Ranking Analysis

8. INVESTMENT ANALYSIS

9. FUTURE OUTLOOK OF THE MARKET

Fluid Power Equipment Industry Segmentation

Fluid power equipment encompasses devices and systems that harness fluids, like liquids or gases, to produce, regulate, and convey power. This technology finds extensive applications across various sectors, including construction, manufacturing, transportation, and automation. For market estimation, we have tracked the revenue generated from the sale of fluid power equipment and components offered by different market players for various applications. The market trends are evaluated by analyzing the investments made in product innovation, diversification, and expansion. The advancements in valves, pumps, motors, and actuators are also crucial in determining the growth of the market studied.

The fluid power equipment market in mobile equipment is segmented by product type (hydraulics [pumps, motors, valves, cylinders, accumulators, filters, and other product types], pneumatics [valves, actuators, FRLs, fittings, and other types]), end-user vertical (construction, agriculture, material handling, mining, and other end-user verticals), geography (North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Product Type | ||||||||

| ||||||||

|

| By End-user Vertical | |

| Construction | |

| Agriculture | |

| Material Handling | |

| Mining | |

| Other End-user Verticals (Commercial Vehicles, Marine, Municipal Vehicles, Drilling Machines and Other niche markets) |

| By Geography | |

| North America | |

| Asia | |

| Europe | |

| Latin America | |

| Middle East and Africa | |

| Australia and New Zealand |

Fluid Power Equipment Market Research FAQs

How big is the Fluid Power Equipment Market In Mobile Equipment Industry?

The Fluid Power Equipment Market In Mobile Equipment Industry size is expected to reach USD 28.91 billion in 2024 and grow at a CAGR of 6.60% to reach USD 39.79 billion by 2029.

What is the current Fluid Power Equipment Market In Mobile Equipment Industry size?

In 2024, the Fluid Power Equipment Market In Mobile Equipment Industry size is expected to reach USD 28.91 billion.

Who are the key players in Fluid Power Equipment Market In Mobile Equipment Industry?

Kawasaki Precision Machinery, Bosch-Rexroth AG, Parker Hannifin Corporation, Danfoss AS and Eaton Corporation are the major companies operating in the Fluid Power Equipment Market In Mobile Equipment Industry.

Which is the fastest growing region in Fluid Power Equipment Market In Mobile Equipment Industry?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Fluid Power Equipment Market In Mobile Equipment Industry?

In 2024, the North America accounts for the largest market share in Fluid Power Equipment Market In Mobile Equipment Industry.

What years does this Fluid Power Equipment Market In Mobile Equipment Industry cover, and what was the market size in 2023?

In 2023, the Fluid Power Equipment Market In Mobile Equipment Industry size was estimated at USD 27.00 billion. The report covers the Fluid Power Equipment Market In Mobile Equipment Industry historical market size for years: 2022 and 2023. The report also forecasts the Fluid Power Equipment Market In Mobile Equipment Industry size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Fluid Power Equipment Industry Report

Statistics for the 2024 Fluid Power Equipment In Mobile Equipment market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Fluid Power Equipment In Mobile Equipment analysis includes a market forecast outlook for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.