| Study Period | 2019 - 2030 |

| Market Volume (2025) | 0.42 gigawatt |

| Market Volume (2030) | 8.13 gigawatt |

| CAGR | 81.16 % |

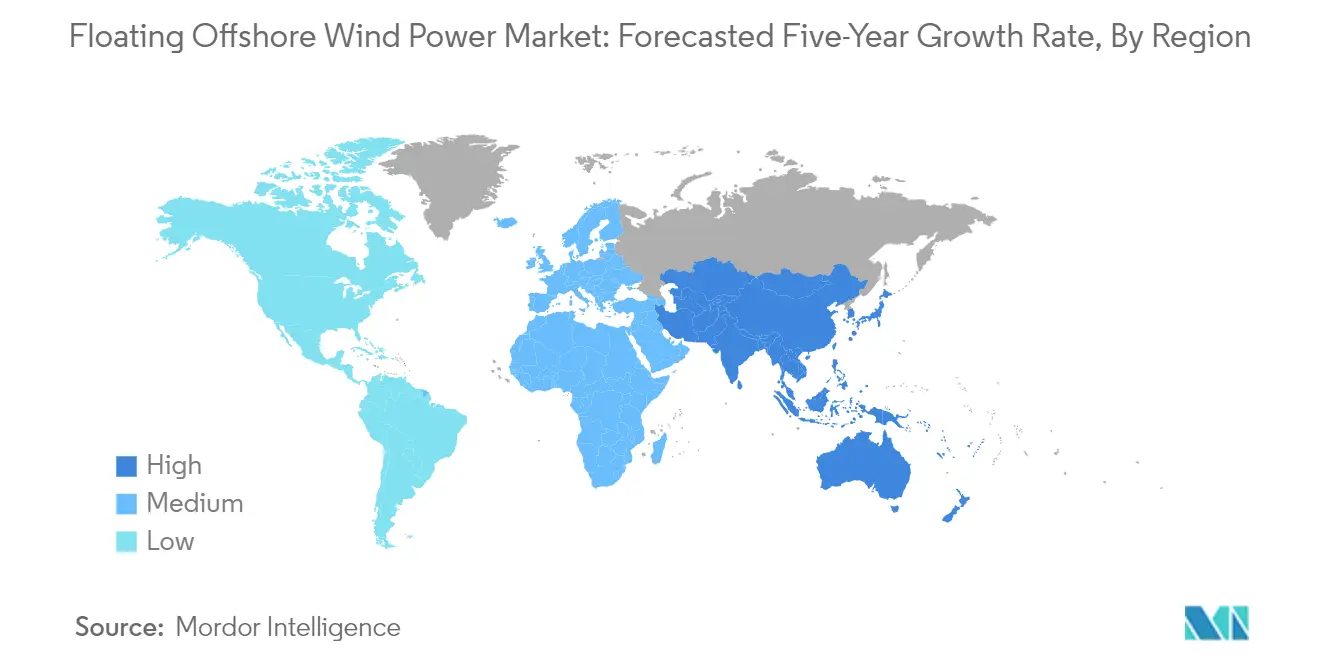

| Fastest Growing Market | Europe |

| Largest Market | Europe |

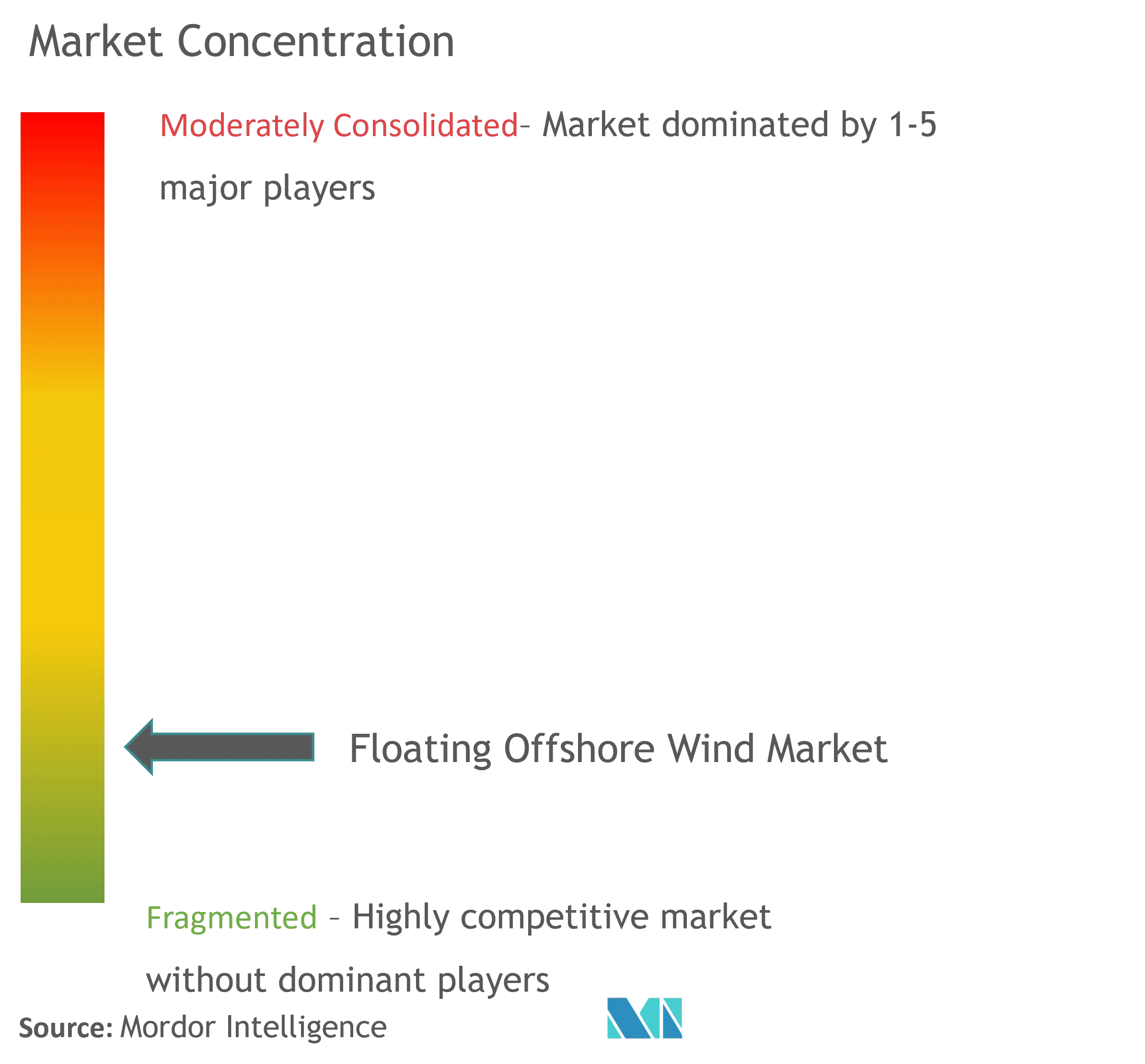

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Floating Offshore Wind Power Market Analysis

The Floating Offshore Wind Power Market size in terms of installed base is expected to grow from 0.42 gigawatt in 2025 to 8.13 gigawatt by 2030, at a CAGR of 81.16% during the forecast period (2025-2030).

The floating offshore wind power industry is experiencing an unprecedented transformation as governments and energy companies increasingly pivot towards sustainable energy solutions. This shift is particularly evident in the technological advancement of floating wind technology, which has evolved from experimental projects to commercially viable energy solutions. The industry has witnessed significant progress in foundation designs, with semi-submersible structures emerging as the dominant technology choice, accounting for nearly 80% of all floating projects announced through 2022. This technological maturity has enabled the development of larger floating wind turbines and more efficient power generation systems, contributing to the overall growth of the floating offshore wind energy sector.

Investment patterns in the floating offshore wind sector have shown remarkable momentum, with major energy companies and financial institutions making substantial commitments to project development. In May 2022, China demonstrated its technological prowess by deploying its largest floating wind turbine, the Fuyao platform, in the South China Sea, marking a significant milestone in the industry's development. The project showcases the increasing confidence in floating wind technology and its potential to harness wind resources in deeper waters. This trend is further evidenced by the final investment decision made by the EolMed partnership for their 30 MW Mediterranean Sea pilot wind farm, scheduled for commissioning in mid-2024.

The industry is witnessing a surge in strategic partnerships and collaborative ventures aimed at accelerating technological innovation and project development. These collaborations are particularly focused on developing more cost-effective floating foundation designs and improving installation methodologies. Australia's offshore wind sector exemplifies this potential, with studies indicating the country could generate up to 5,000 gigawatts of electricity from combined fixed and floating infrastructure. This vast potential has attracted numerous international developers and technology providers, leading to increased research and development activities in the sector.

The market is characterized by an increasing emphasis on supply chain optimization and local content requirements, as countries seek to develop domestic manufacturing capabilities for floating wind components. This trend is driving the establishment of new production facilities and the development of specialized installation vessels designed specifically for floating wind projects. The industry is also seeing the emergence of innovative business models, with developers exploring hybrid projects that combine floating wind power with other renewable technologies or industrial applications. These developments are supported by improving project economics and growing investor confidence in the technology's commercial viability.

Floating Offshore Wind Power Market Trends

Increasing Water Depth of Offshore Wind Power Projects

The floating offshore wind power market is primarily driven by the increasing depth requirements for offshore wind power installations, as traditional fixed-bottom turbines face significant limitations. Conventional wind turbines, typically installed in water depths of up to 40 meters and as far as 80 kilometers from the shore, are restricted by their monopile or jacket foundations to waters less than 60 meters deep. This limitation has become particularly significant for markets with vast deep-water potential, such as Japan and the United States, where shallow-water sites are scarce. The deployment in deeper waters has opened new seabed areas for leasing and substantially increased the total potential capacity for offshore floating wind power installations, making floating foundations an increasingly viable solution for expanding offshore wind energy generation.

The technical and economic viability of deeper water installations has been demonstrated by recent groundbreaking projects. In August 2023, the world's largest floating wind farm, the Hywind Tampen Project, began operations approximately 140 kilometers off Norway's coast in depths ranging from 270 to 310 meters, featuring 11 floating wind turbines with a system capacity of 88 MW. This advancement is further supported by significant institutional backing, as evidenced by the US Department of Energy's Wind Energy Technologies Office's April 2024 announcement of a planned USD 48 million funding opportunity for offshore wind technologies, including floating platform research and development. The increasing depth capabilities have also attracted attention in regions like China, where approximately 60% of the offshore wind potential lies in water depths between 50 and 100 meters, compared to just 13% in depths less than 20 meters, highlighting the crucial role of floating wind technology in accessing these resources.

Understand The Key Trends Shaping This Market

Download PDF

Segment Analysis: By Water Depth

Deep Water Segment in Floating Offshore Wind Power Market

The deep water segment (greater than 60m depth) dominates the floating offshore wind power market, driven by the economic viability of floating wind turbine technology at these depths compared to fixed-base structures. This segment's prominence is evidenced by the concentration of most pilot projects and commercial floating wind installations operating at depths between 60-800 meters. The segment's leadership position is further strengthened by the fact that nearly 80% of Europe's total technical offshore wind resource lies in depths greater than 60 meters. Semi-submersible and spar-type technologies are particularly well-suited for these depths, with semi-submersible designs accounting for approximately 79.6% of all floating projects. The segment's growth is supported by significant investments in research and development, particularly in mature offshore wind markets like China, Japan, the United States, and Europe. The development of electrical infrastructure, including submarine HVDC connections, plays a crucial role in supporting deep water floating wind technology installations, as these projects are typically located further from the coast.

Transitional Water Segment in Floating Offshore Wind Power Market

The transitional water segment (30m to 60m depth) represents a unique market opportunity where both fixed and floating wind turbine types can be deployed. This segment primarily utilizes barge model designs, which offer the shallowest draft among all floating foundation types and are particularly suitable for operations in depths greater than 30m. The segment benefits from the flexibility in design and procurement options, as these barge-type floating turbines can be constructed using steel, concrete, or steel-concrete mixtures. The growth in this segment is particularly strong in European regions, with significant projects under development in the United Kingdom, Scandinavia, and France. However, the segment faces distinct challenges, including complications in mooring designs in relatively shallow waters and environmental impact considerations on continental shelves, which influence project development decisions and implementation strategies.

Remaining Segments in Water Depth Segmentation

The shallow water segment (less than 30m depth) represents a smaller portion of the floating offshore wind power market due to the preference for fixed-bottom wind turbines in these depths. This segment faces significant challenges, including higher technology costs compared to fixed-base alternatives and environmental concerns regarding impacts on coastal biodiversity. The segment's development is primarily concentrated in pilot and academic projects aimed at determining project feasibility, rather than commercial deployments. The environmental considerations are particularly critical in these areas due to their proximity to shore and the potential impact on coastal communities and marine ecosystems, making project approval and implementation more challenging compared to deeper water installations.

Floating Offshore Wind Power Market Geography Segment Analysis

Floating Offshore Wind Power Market in North America

The North American floating offshore wind power market holds approximately 1% of the global market share in 2024, reflecting its early stage of development in the region. The United States leads the regional market with significant potential for growth, particularly along its extensive coastlines. The Bureau of Ocean Energy Management (BOEM) has designated multiple Call Areas specifically for floating wind farm structures, including regions in Hawaii, California, and Oregon. The region's market is characterized by robust government support and policy frameworks, with states like California exclusively focusing on deep floating opportunities in areas such as Humboldt Bay and Morro Bay. The market is also witnessing substantial infrastructure development, with ports being upgraded to accommodate commercial-scale floating offshore wind power projects. Technical feasibility studies and resource assessments are being conducted in regions like Hawaii, Puerto Rico, and the Great Lakes, indicating expanding geographical coverage. The region's commitment to renewable energy targets and carbon reduction goals continues to drive market growth, supported by technological advancements aimed at cost reduction and efficiency improvements.

Floating Offshore Wind Power Market in Europe

Europe maintains its position as a pioneer in the floating offshore wind power market, demonstrating remarkable growth with approximately 63% CAGR from 2019 to 2024. The region's market is characterized by mature infrastructure, advanced technological capabilities, and strong regulatory frameworks. Countries like Norway, France, and the United Kingdom are at the forefront of floating wind farm technology development, with numerous commercial-scale projects in various stages of development. The market benefits from well-established supply chains, an experienced workforce, and sophisticated port infrastructure specifically designed for offshore wind power operations. European countries have implemented comprehensive marine spatial planning processes to optimize offshore wind deployment while considering environmental impacts and other maritime activities. The region's success is further supported by collaborative research initiatives, public-private partnerships, and cross-border cooperation in technology development. Strong political commitment to renewable energy transition and decarbonization goals continues to drive market expansion, while innovative financing mechanisms help facilitate project development.

Floating Offshore Wind Power Market in Asia-Pacific

The Asia-Pacific floating offshore wind power market is poised for exceptional growth, with a projected CAGR of approximately 146% from 2024 to 2027. The region's market is driven by ambitious renewable energy targets, particularly in countries like Japan, South Korea, and China. These nations are leveraging their extensive maritime experience and industrial capabilities to develop domestic floating wind power market technologies. The market is characterized by strong government support through feed-in tariffs, renewable energy certificates, and dedicated offshore wind development zones. Significant investments in port infrastructure and supply chain development are enhancing the region's capability to support large-scale floating wind deployments. The market benefits from the region's advanced shipbuilding and marine engineering expertise, which facilitates local manufacturing of floating platforms and associated components. Strategic partnerships between local and international players are accelerating technology transfer and project development capabilities. The region's deep waters and strong wind resources, combined with limited shallow water areas suitable for fixed-bottom installations, make floating wind technology particularly attractive.

Floating Offshore Wind Power Market in Rest of World

The Rest of World region represents an emerging market for floating offshore wind power, with significant untapped potential across South America, Africa, and the Middle East. Brazil leads the development in South America, leveraging its extensive coastline and favorable wind conditions for offshore wind energy deployment. The region benefits from increasing energy demand, supportive regulatory frameworks, and growing interest from international developers and investors. South Africa's market shows promise with multiple suitable regions identified for offshore wind development, while Saudi Arabia is exploring floating wind opportunities as part of its economic diversification strategy. These markets are characterized by growing renewable energy ambitions, although they face challenges related to infrastructure development and technical expertise. The region's development is supported by technology transfer from mature markets and increasing collaboration with experienced international partners. Despite being in early stages, these markets are expected to play an increasingly important role in the global floating offshore wind sector as technology costs decrease and local capabilities improve.

Get Analysis on Important Geographic Markets

Download PDF

Floating Offshore Wind Power Industry Overview

Top Companies in Floating Offshore Wind Power Market

The floating offshore wind power market features established players like Vestas, Siemens Gamesa, General Electric, and Equinor, leading in technological innovation and project development. Companies are increasingly focusing on developing proprietary floating foundation technologies and patented solutions to gain competitive advantages, as exemplified by innovations like BW Ideol's damping pool technology. Strategic partnerships and joint ventures have become crucial for market expansion, with companies collaborating across the value chain to share expertise and resources. Major players are investing heavily in research and development to optimize floating wind turbine designs, improve installation methodologies, and reduce overall project costs. Geographic expansion strategies are evident through participation in emerging markets, particularly in the Asia-Pacific and European regions, where companies are securing seabed leases and developing large-scale floating offshore wind power projects.

Dynamic Market with Strong Growth Potential

The floating wind power market exhibits a mix of large energy conglomerates and specialized renewable energy firms, creating a diverse competitive landscape. Global players like Equinor and Marubeni Corporation leverage their extensive energy sector experience and financial resources to develop large-scale projects, while specialized firms like BW Ideol focus on innovative floating wind technology. The market is experiencing increasing consolidation through strategic partnerships and joint ventures, particularly evident in major projects like the ScotWind leasing rounds and Asian offshore developments. Companies are forming consortiums to share technical expertise and financial risks, especially in emerging markets.

The industry is characterized by significant merger and acquisition activity, with established energy companies acquiring specialized floating wind technology providers to enhance their capabilities. Traditional energy companies are strategically diversifying into floating offshore wind to strengthen their renewable energy portfolios and maintain market competitiveness. The market structure encourages collaboration between technology providers, project developers, and utility companies, creating an interconnected ecosystem of stakeholders working together to advance floating offshore wind technology and project implementation.

Innovation and Partnerships Drive Market Success

Success in the offshore wind power industry increasingly depends on technological innovation, strategic partnerships, and operational efficiency. Incumbent companies are focusing on developing cost-effective floating foundation designs, improving installation methods, and optimizing maintenance procedures to reduce operational expenses. Market leaders are establishing strong supply chain networks and forming strategic alliances with local partners to navigate regulatory requirements and secure project approvals. Companies are also investing in digital technologies and smart monitoring systems to enhance operational performance and maintain competitive advantages.

For new entrants and contenders, success strategies include developing specialized technological solutions, forming partnerships with established players, and focusing on specific market niches. The market's future growth potential is supported by increasing government support for renewable energy and declining production costs, though regulatory frameworks and environmental considerations remain important factors. Companies must also address the challenges of end-user concentration in utility sectors and manage the risks associated with emerging alternative renewable technologies. The ability to secure long-term power purchase agreements and maintain strong relationships with key stakeholders will be crucial for sustained market success. Furthermore, advancements in offshore wind construction are pivotal in driving down costs and improving efficiency.

Floating Offshore Wind Power Market Leaders

-

General Electric Company

-

Vestas Wind Systems A/S

-

Siemens Gamesa Renewable Energy, S.A

-

Doosan Enerbility Co Ltd.

-

BW Ideol AS

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Floating Offshore Wind Power Market News

- November 2024: Mainstream Renewable Power, a global leader in wind and solar energy and predominantly owned by Aker Horizons ASA, announced that KF Wind, its joint venture with Ocean Winds, has clinched a Transmission Service Agreement (TSA) with Korea Electric Power Corporation (KEPCO). This agreement will channel 1,125 MW of clean energy from KF Wind’s floating offshore wind project, located off the coast of Ulsan, directly into Korea’s national grid. Once fully operational, the Ulsan floating offshore wind farm cluster, which includes KF Wind, is projected to generate approximately 6 GW. This milestone positions it as the world’s largest floating offshore wind area and underscores its significance in advancing Korea’s carbon neutrality objectives.

- November 2024: Hexicon, a Swedish offshore wind specialist, advanced its acquisition of the 1.1 GW 'MunmuBaram' floating offshore wind project. The company secured approval from Korea's Electricity Regulatory Commission to transfer two of the three necessary business licenses. The MunmuBaram project is a key component of a larger endeavor aiming to create the world's largest floating offshore wind power complex in the East Sea, situated off the coast of Ulsan, South Korea. This ambitious mega-project boasts a total planned capacity of 6.2 GW, which is on par with the output of six nuclear reactors. The initiative has attracted an investment of approximately USD 29 billion from both domestic and international entities. Positioned 70 km from Ulsan's coastline, the project will be managed by five special-purpose entities, with MunmuBaram being one of them.

Floating Offshore Wind Power Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Floating Offshore Wind Power Cumulative Installed Capacity Forecast, till 2029

-

4.3 Key Projects Information

- 4.3.1 Major Existing Projects

- 4.3.2 Upcoming Projects

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

-

4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Rising Investments in Offshore Wind Energy Projects

- 4.6.1.2 Advanced and Readily Accessible Offshore Wind Turbine Technologies

- 4.6.2 Restraint

- 4.6.2.1 Tough Competition from Alternate Renewable Energy Markets

- 4.7 Supply Chain Analysis

-

4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment Analysis

5. MARKET SEGMENTATION

-

5.1 By Water Depth (Qualitative Analysis Only)

- 5.1.1 Shallow Water (less than 30 m depth)

- 5.1.2 Transitional Water (30 m to 60 m depth)

- 5.1.3 Deep Water (higher than 60 m depth)

-

5.2 By Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 Germany

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Nordic Countries

- 5.2.2.7 Russia

- 5.2.2.8 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Malaysia

- 5.2.3.6 Vietnam

- 5.2.3.7 Thailand

- 5.2.3.8 Indonesia

- 5.2.3.9 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 Egypt

- 5.2.5.4 South Africa

- 5.2.5.5 Nigeria

- 5.2.5.6 Rest of the Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Collaboration and Joint Ventures

- 6.2 Strategies and SWOT Adopted by Leading Players

-

6.3 Company Profiles

- 6.3.1 Vestas Wind Systems AS

- 6.3.2 General Electric Company

- 6.3.3 Siemens Gamesa Renewable Energy SA

- 6.3.4 BW Ideol AS

- 6.3.5 Equinor ASA

- 6.3.6 Marubeni Corporation

- 6.3.7 RWE AG

- 6.3.8 Doosan Enerbility Co. Ltd

- *List Not Exhaustive

- 6.4 Market Ranking Analysis

- 6.5 List of Other Prominent Companies

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Developing Floating Offshore Wind Projects in Untapped Offshore Deep-water Prospects

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Floating Offshore Wind Power Industry Segmentation

Floating wind power is electricity made by an offshore wind turbine that is mounted on a floating structure. This lets the turbine make electricity in water depths where fixed-foundation turbines cannot work. Floating wind farms can make a big difference in the amount of sea area that can be used for offshore wind farms, especially in places where shallow water is not available.

The floating offshore wind power market is segmented by water depth (qualitative analysis only) and geography. By water depth, the market is segmented into shallow water (less than 30 m depth), transitional water (30 m to 60 m depth), and deep water (higher than 60 m depth). By Geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report also covers the sizes and forecasts of the floating offshore wind market across major regions. For each segment, market sizing and forecasts have been done based on installed capacity.

| By Water Depth (Qualitative Analysis Only) | Shallow Water (less than 30 m depth) | ||

| Transitional Water (30 m to 60 m depth) | |||

| Deep Water (higher than 60 m depth) | |||

| By Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordic Countries | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Malaysia | |||

| Vietnam | |||

| Thailand | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| Egypt | |||

| South Africa | |||

| Nigeria | |||

| Rest of the Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Floating Offshore Wind Power Market Research FAQs

How big is the Floating Offshore Wind Power Market?

The Floating Offshore Wind Power Market size is expected to reach 0.42 gigawatt in 2025 and grow at a CAGR of 81.16% to reach 8.13 gigawatt by 2030.

What is the current Floating Offshore Wind Power Market size?

In 2025, the Floating Offshore Wind Power Market size is expected to reach 0.42 gigawatt.

Who are the key players in Floating Offshore Wind Power Market?

General Electric Company, Vestas Wind Systems A/S, Siemens Gamesa Renewable Energy, S.A, Doosan Enerbility Co Ltd. and BW Ideol AS are the major companies operating in the Floating Offshore Wind Power Market.

Which is the fastest growing region in Floating Offshore Wind Power Market?

Europe is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Floating Offshore Wind Power Market?

In 2025, the Europe accounts for the largest market share in Floating Offshore Wind Power Market.

What years does this Floating Offshore Wind Power Market cover, and what was the market size in 2024?

In 2024, the Floating Offshore Wind Power Market size was estimated at 0.08 gigawatt. The report covers the Floating Offshore Wind Power Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Floating Offshore Wind Power Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Floating Offshore Wind Power Market Research

Mordor Intelligence delivers a comprehensive analysis of the floating offshore wind power industry. We leverage our extensive expertise in offshore renewable energy research. Our latest report examines the evolving landscape of FOW (Floating Offshore Wind) technology. It covers crucial developments in floating wind farms and floating wind turbine installations worldwide. The analysis provides detailed insights into offshore wind construction practices, floating wind technology advancements, and emerging trends in marine wind energy deployment.

Stakeholders in the floating wind power market gain access to detailed market intelligence through our easy-to-download report PDF. This report offers an in-depth analysis of floating offshore wind energy developments and growth projections. It provides valuable insights into offshore wind power industry dynamics, including comprehensive coverage of floating wind installation methodologies and operational best practices. Our research supports decision-makers in understanding the complexities of offshore wind energy systems. It also provides strategic recommendations for maximizing opportunities in the floating wind power sector.