| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 5.91 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Flip Chip Technology Market Analysis

The Flip Chip Technology Market is expected to register a CAGR of 5.91% during the forecast period.

The flip chip technology landscape is experiencing significant transformation driven by the increasing complexity of semiconductor packaging requirements and the push toward advanced packaging solutions. The industry has witnessed a surge in strategic partnerships and collaborations among key players, particularly in developing next-generation packaging solutions. For instance, in March 2023, Intel announced significant investments in advanced packaging facilities to support their IDM 2.0 strategy, demonstrating the industry's commitment to innovation in flip chip technology. The semiconductor industry's robust growth is evidenced by the record-breaking semiconductor unit shipments reaching 1,135.3 billion units in 2021, indicating strong demand for advanced chip packaging solutions.

The evolution of data center architectures and cloud computing infrastructure has created unprecedented demands for high-performance computing solutions, driving innovations in flip chip packaging technology. Cloud data center IP traffic reached 19,509 exabytes in 2021, necessitating more sophisticated chip packaging solutions to handle increased data processing requirements. This trend has led to the development of more advanced flip chip solutions that can support higher bandwidth, improved thermal management, and enhanced electrical performance for data center applications. The industry has responded with innovations in copper pillar technology and advanced substrate materials to meet these demanding requirements.

The market is witnessing a significant shift toward fan-out wafer level packaging (FOWLP) and embedded die technologies, representing the next frontier in flip chip innovation. Major manufacturers are increasing their investments in these emerging technologies to address the growing demand for smaller form factors and higher performance in electronic devices. The CMOS image sensor market, a key application area for flip chip technology, demonstrated robust growth reaching $22.8 billion in revenue in 2021, highlighting the expanding applications of flip chip technology in advanced imaging solutions. This growth has spurred development in specialized flip chip solutions optimized for sensor applications.

Raw material supply chain dynamics are playing an increasingly crucial role in shaping the flip chip technology market landscape. The industry is witnessing a transformation in material requirements, particularly in areas such as advanced substrate materials and bumping materials. Leading manufacturers are forming strategic partnerships with material suppliers to ensure consistent supply and develop new materials that can meet the demanding requirements of next-generation flip chip applications. The trend toward more environmentally sustainable packaging solutions has also led to innovations in lead-free solder materials and eco-friendly underfill materials, reflecting the industry's commitment to environmental responsibility while maintaining high performance standards.

Flip Chip Technology Market Trends

Increasing Demand for Wearable Devices

The proliferation of wearable devices across various applications has emerged as a significant driver for flip chip packaging technology adoption. These devices, including smartwatches, fitness tracking devices, and wearable medical devices like portable blood pressure monitors, calorie trackers, and heart rate monitors, require increasingly sophisticated semiconductor interconnect solutions. The technology's ability to enable miniaturization while maintaining high performance makes it particularly suitable for wearable applications. Flip chip packaging complements critical components of wearable devices, such as OLED power management devices, by simplifying power-supply circuitry and maximizing battery life for feature-rich portable products.

The growing sophistication of wearable devices has intensified the demand for high-performance LDOs (Low-Dropout Regulators) with state-of-the-art specifications that can fit into ultra-small packages. Flip chip packages are particularly advantageous in this context as they provide robust ESD (Electrostatic Discharge) protection, which is crucial for consumer wearables. These protective devices can safely absorb repetitive ESD strikes at maximum levels specified in international standards without performance degradation. The bidirectional configuration offers symmetrical ESD protection for data lines when AC signals are present, making them ideal for applications such as SIM card interfaces and capacitive touchscreen displays in wearable devices.

Understand The Key Trends Shaping This Market

Download PDF

Strong Growth in MMIC (Monolithic Microwave IC) Applications

The expanding applications of Monolithic Microwave ICs (MMICs) in various sectors, particularly in military, defense, and wireless communication infrastructure, are driving significant growth in flip chip packaging technology adoption. MMICs, operating in the frequency range of 300 MHz to 300 GHz, are crucial for microwave mixing, power amplification, low-noise amplification, and high-frequency switching applications. The technology's capability to enable higher frequency wideband operations through shorter electrical connections and small bumps makes it particularly valuable for MMIC devices operating at 60 GHz and above. For military and defense applications, MMICs are increasingly utilized in electronic warfare (EW), signals intelligence (SIGINT), and military communications.

The advancement in telecommunications and automotive applications has further accelerated the demand for MMIC-based chip scale package solutions. For instance, in automotive radar applications, SiGe transmit-receive phased-array chips operating at 76 to 84 GHz utilize controlled collapse chip connection (C4) bumping processes and are flip-chipped onto low-cost printed circuit boards, achieving impressive isolation between transmit and receive chains. The technology also addresses the growing demand for high bandwidth data access in commercial aircraft, both for business jets and major airliners. As new satellites supporting higher frequencies are being launched to enable increased bandwidth, the need for MMIC-based chip scale package solutions continues to grow, particularly in applications requiring superior electrical performance such as embedded processors, ASICs, and transceivers.

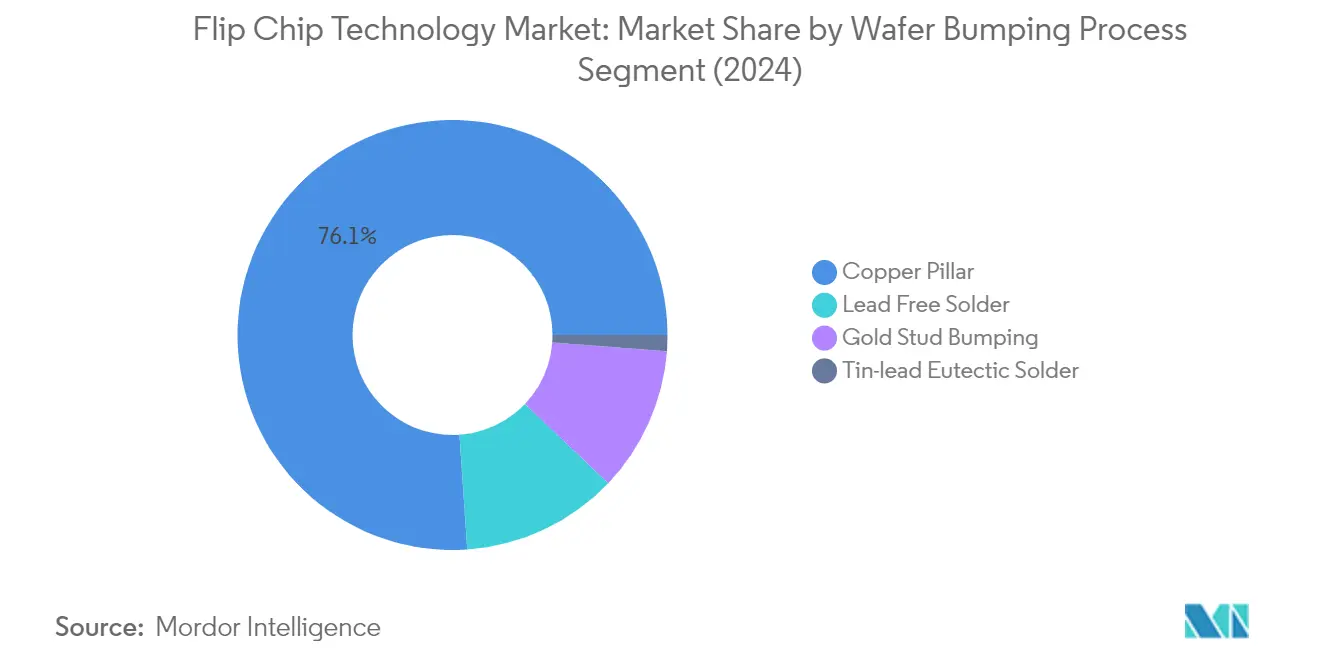

Segment Analysis: By Wafer Bumping Process

Copper Pillar Segment in Flip Chip Technology Market

Copper Pillar dominates the flip chip technology market, commanding approximately 76% of the total market share in 2024. This significant market position is attributed to its superior capabilities in enabling finer pitches down to 20μm, which is essential for advanced semiconductor applications. The technology provides greater control of joint diameter and standoff height compared to traditional solder bump, making it particularly valuable for mobile device manufacturers seeking smaller form factors. Major semiconductor manufacturers and outsourced semiconductor assembly and test (OSAT) providers have widely adopted copper pillar technology, especially in applications requiring high-performance computing and advanced packaging solutions. The technology's advantages in electrical performance, thermal conductivity, and improved electromigration resistance have made it the preferred choice for leading-edge processors and high-end electronic devices.

Lead-Free Solder Segment in Flip Chip Technology Market

The Lead-Free Solder segment represents a growing alternative in the flip chip technology market, with Sn-0.7Cu emerging as the optimal lead-free solder alloy for flip-chip interconnects. This segment is experiencing significant growth driven by stringent environmental regulations and increasing adoption in military applications. The technology's evolution focuses on enhancing reliability through improved solder joint properties and advanced manufacturing processes. Companies are investing in research and development to address challenges related to the relatively low melting temperature of lead-free solders, particularly in miniaturized and multi-function electronic devices. The segment's growth is further supported by the mandatory RoHS (Reduction of Hazardous Substances) certification requirements for electronic products, pushing manufacturers to transition from traditional solder bump methods.

Remaining Segments in Wafer Bumping Process

The remaining segments in the wafer bumping process market include Gold Stud Bumping and Tin-lead Eutectic Solder technologies. Gold Stud Bumping offers unique advantages such as no requirement for Under Bump Metallization (UBM) or special wafer preparation, making it particularly valuable for prototyping and specific applications in the RF and RFID sectors. Meanwhile, Tin-lead Eutectic Solder, despite its historical significance in electronic manufacturing, continues to see declining adoption due to environmental concerns and regulatory restrictions worldwide. These segments serve specific niche applications where their unique properties and characteristics make them the preferred choice for certain specialized electronic components and devices.

Segment Analysis: By Packaging Technology

BGA Segment in Flip Chip Technology Market

The Ball Grid Array (BGA) segment dominates the flip chip technology market, commanding approximately 58% market share in 2024, representing a significant portion of the overall market value. This segment encompasses various advanced packaging technologies including 2.1D, 2.5D, and 3D implementations that are crucial for high-performance computing applications. BGA packages are increasingly being adopted in the industry due to their superior heat conduction capabilities, higher pin density, and enhanced performance characteristics compared to traditional packaging solutions. The segment's growth is primarily driven by the rising demand for advanced packaging solutions in applications such as graphics processors, FPGAs, and high-performance computing systems. Additionally, the increasing adoption of BGA packages in automotive electronics, particularly for safety systems and advanced driver assistance systems (ADAS), has further strengthened its market position. The segment is also witnessing strong growth with an expected CAGR of around 7% from 2024 to 2029, driven by continuous innovations in 3D packaging technologies and increasing demand for high-density chip interconnect solutions.

CSP Segment in Flip Chip Technology Market

The Chip Scale Package (CSP) segment represents a significant portion of the flip chip technology market, offering unique advantages in terms of miniaturization and performance optimization. CSP technology has become increasingly important in modern electronic devices due to its ability to provide smaller footprints, reduced thickness, and improved electrical performance compared to traditional packaging solutions. The segment has gained particular traction in mobile devices, wearables, and other portable electronic applications where space constraints are critical. CSP's tolerance to die size changes and compatibility with automated soldering processes has made it a preferred choice for many manufacturers looking to optimize their production processes while maintaining high reliability standards. The technology's ability to combine the advantages of bare die assembly with the reliability of encapsulated devices has positioned it as a crucial solution for next-generation electronic devices.

Segment Analysis: By Product

Memory Segment in Flip Chip Technology Market

The memory segment represents a significant portion of the flip chip technology market, driven by the substantial demand from mobile devices and computing sectors, particularly servers. The capacity of DRAM in smartphones running on Android has reached up to 12GB, while server memory capacity has grown substantially. Memory manufacturers are increasingly adopting flip-chip technology over wire bonding due to its superior performance in high-frequency applications, enhanced reliability, and improved migration toward advanced process geometries. The technology offers cost benefits through simultaneous bonding of connections rather than one bond at a time, making it particularly attractive for high-volume memory production. Major memory manufacturers are strategically partnering with OSAT players while regional players are collaborating with global technology providers to strengthen their position in the market.

LED Segment in Flip Chip Technology Market

The Light Emitting Diode (LED) segment is experiencing rapid growth in the flip chip technology market, driven by increasing emphasis on energy conservation practices across regions. Flip chip technology offers significant cost and performance advantages over other packaging technologies, encouraging LED manufacturers to produce premium lighting products without compromising on quality. The technology enables better heat dissipation and current spreading performance, making it ideal for high-power LED applications. The adoption of flip chip LED (FCLED) in the automotive sector is gaining momentum due to increased interest in high-power LED modules among automobile manufacturers. The technology's ability to provide enhanced brightness and superior thermal management capabilities is driving its adoption across various applications including automotive lighting, display backlighting, and general illumination.

Remaining Segments in Flip Chip Product Segmentation

The flip chip technology market encompasses several other important segments including CMOS Image Sensors, System-on-Chip (SoC), Graphics Processing Units (GPU), and Central Processing Units (CPU). CMOS image sensors utilize flip chip packaging for smartphones and high-end imaging applications, benefiting from the technology's ability to enable miniaturization and improved performance. The SoC segment leverages flip chip technology for various applications including mobile devices and IoT implementations, while GPUs and CPUs were early adopters of the technology due to their high-performance requirements. These segments continue to drive innovation in flip chip technology, particularly in areas such as 3D packaging, heterogeneous integration, and advanced thermal management solutions.

Segment Analysis: By End User

Consumer Electronics Segment in Flip Chip Technology Market

The consumer electronics segment maintains its dominance in the flip chip technology market, commanding approximately 43% of the market share in 2024. This substantial market position is driven by the increasing adoption of flip chip technology in smartphones, tablets, laptops, and other portable electronic devices. The segment's growth is primarily attributed to the rising demand for miniaturization and high performance in electronic devices, coupled with the strong penetration of advanced packaging technology in consumer electronics. Manufacturers of leading-edge consumer electronics devices are increasingly adopting flip chip products for space and weight savings, functional integration, and cost advantages. The technology's ability to handle high power demands, distribute I/O effectively, and provide the cleanest electrical path for high-speed signals makes it particularly valuable in consumer electronics applications.

Telecommunications Segment in Flip Chip Technology Market

The telecommunications segment is emerging as the fastest-growing sector in the flip chip technology market, projected to grow at approximately 8% during 2024-2029. This remarkable growth is driven by the increasing deployment of 5G infrastructure and the rising demand for high-performance communication devices. The segment's expansion is fueled by applications such as cellular telecommunications that require flip chip packaging for its small form factor and superior high-frequency performance. Thermosonic flip chip technology is gaining significant traction in telecommunications applications, particularly in surface acoustic wave (SAW) filters. The ability to provide higher I/O connection in the area array satisfies the demands for high-end products, making it increasingly essential for networking and complex computing applications in the telecommunications sector.

Remaining Segments in End User Market Segmentation

The automotive sector is witnessing significant adoption of flip chip technology, particularly in infotainment systems, GPS modules, and radar applications, while the industrial sector leverages the technology for IoT devices and automation systems. The military and defense segment utilizes flip chip technology in radar systems and high-performance computing platforms, benefiting from its reliability and scalability. The medical and healthcare sector implements flip chip technology in various applications including pacemakers, retinal implants, and auditory devices, where miniaturization and reliability are crucial. Each of these segments contributes uniquely to the market's dynamics, driven by specific requirements for high performance, reliability, and advanced packaging solutions in their respective applications.

Flip Chip Technology Market Geography Segment Analysis

Flip Chip Technology Market in Taiwan

Taiwan has established itself as the dominant force in the global flip chip technology market, commanding approximately 51% of the market share in 2024. The country's semiconductor packaging industry, which started in the 1970s, has built a complete semiconductor supply chain encompassing IC design, wafer fabrication, IC packaging, and testing. Taiwan's success in the flip chip technology sector is supported by its robust infrastructure and strategic partnerships with global technology leaders. The country hosts numerous foundries and has collaborated with Japan for greater cooperation in the semiconductor market. Taiwan Semiconductor Manufacturing Co (TSMC), a key player in the market, has been actively expanding its advanced packaging capabilities and investing in cutting-edge technologies. The country's commitment to research and development, coupled with its focus on high-end manufacturing processes, has enabled it to maintain its leadership position in the industry. Taiwan's expertise in flip chip technology spans various applications, from mobile devices and computing systems to automotive electronics and IoT devices.

Flip Chip Technology Market in South Korea

South Korea is emerging as the fastest-growing market in the flip chip technology sector, with a projected growth rate of approximately 9% during 2024-2029. The country's semiconductor packaging industry has transformed from its initial focus on labor-intensive processes to becoming a global powerhouse in advanced chip manufacturing. The government's ambitious "K-Semiconductor Belt" program is designed to enhance chip-making technology and build the world's largest supply chain. This comprehensive value chain spans key manufacturing clusters across Seoul and Gyeonggi Province, attracting significant investments from major players like Samsung Electronics and SK Hynix. South Korean companies are increasingly investing in flip-chip ball grid arrays (FC-BGA) due to high demand in various applications. The country's strategic focus on developing advanced packaging technologies and its strong emphasis on research and development have positioned it as a crucial player in the global semiconductor ecosystem. South Korea's success is further bolstered by its robust export-oriented semiconductor industry and its ability to attract foreign investments in the sector.

Flip Chip Technology Market in China

China has emerged as a significant player in the flip chip technology market, driven by its comprehensive semiconductor ecosystem and strategic government initiatives. The country hosts a large number of companies with significant packaging and assembly operations, primarily concentrated in the Jiangsu, Guangdong, and Shanghai regions. Chinese players such as Jiangsu Changjiang Electronics Technology (JCET) have already established high-volume wafer bumping capabilities with advanced 12" wafer bumping lines. The country's flip chip market covers both bumping and assembly steps, with Chinese players demonstrating expertise in Cu pillar processes. Various industries, including automotive, wireless, computing, and other devices, have been qualified and integrated into the country's flip chip package offerings. China's commitment to developing its domestic semiconductor capabilities, coupled with favorable government policies and substantial investments in research and development, has strengthened its position in the global market.

Flip Chip Technology Market in United States

The United States maintains its position as a key player in the flip chip technology market, leveraging its leadership in research and development activities such as electronic design automation (EDA), core intellectual property (IP), and chip design. The country's semiconductor backend industry forms a crucial part of its economy, supporting millions of jobs and driving technological innovation. American companies have demonstrated particular strength in developing advanced packaging technologies using 3D-heterogeneous integration. The United States has maintained competitiveness in specific segments such as DRAM and 3D-NAND, with US firms at the cutting edge of advanced packaging technology. The country's focus on supply chain resilience and domestic semiconductor production has led to significant investments in manufacturing capabilities. The combination of strong research capabilities, technological innovation, and strategic government support continues to reinforce the United States' position in the global flip chip technology market.

Flip Chip Technology Market in Other Countries

The flip chip technology market extends beyond the major players to include several other significant countries, each contributing uniquely to the global ecosystem. Malaysia has established itself as a crucial hub in the semiconductor assembly and test supply chain, attracting investments from major global players and focusing on high-tech manufacturing capabilities. Singapore has emerged as Southeast Asia's important semiconductor manufacturing base, hosting numerous wafer fabrication plants operated by leading global chipmakers. Japan, with its strong technological foundation and historical significance in the semiconductor industry, continues to play a vital role in the market's development. These countries have developed specialized capabilities in different aspects of flip chip technology, from research and development to manufacturing and testing, creating a diverse and robust global supply chain. Their continued investments in infrastructure, technology development, and workforce training ensure the sustained growth and innovation of the flip chip technology market worldwide.

Get Analysis on Important Geographic Markets

Download PDF

Flip Chip Technology Industry Overview

Top Companies in Flip Chip Technology Market

The flip chip technology market features prominent players like Amkor Technology, UTAC Holdings, TSMC, Chipbond Technology, TF AMD Microelectronics, JCET, Powertech Technology, and ASE Industrial Holdings. These companies are heavily investing in research and development to advance their packaging and assembly capabilities, particularly in areas like copper pillar technology, wafer-level packaging, and system-in-package solutions. Strategic partnerships and collaborations have become increasingly common, especially for developing advanced packaging solutions for 5G, automotive, and high-performance computing applications. Companies are expanding their manufacturing footprint across Asia, particularly in Taiwan, China, and Malaysia, to capitalize on growing regional demand and establish proximity to major semiconductor manufacturing hubs. The industry is witnessing a trend toward integrated operations, where players are offering comprehensive solutions from wafer bumping to final testing, enabling better supply chain control and faster time-to-market.

Market Structure Shows Regional Manufacturing Dominance

The flip chip technology market exhibits a relatively consolidated structure, dominated by large integrated device manufacturers (IDMs) and outsourced semiconductor assembly and test (OSAT) providers. Taiwan maintains a commanding position in the global market, followed by China and the United States, with these regions housing the majority of advanced packaging facilities. The market is characterized by high entry barriers due to substantial capital requirements and technical expertise needed for advanced packaging solutions. Major players are increasingly pursuing vertical integration strategies, offering end-to-end solutions from wafer fabrication to final testing, which has led to increased market consolidation.

The industry has witnessed significant merger and acquisition activity, particularly among Asian manufacturers looking to expand their technological capabilities and market reach. Companies are forming strategic alliances to combine their expertise in different aspects of the packaging process, from wafer bumping to advanced assembly techniques. The market structure is evolving with the emergence of specialized players focusing on specific applications like automotive electronics and mobile devices, while larger conglomerates maintain their dominance through comprehensive solution offerings and economies of scale.

Innovation and Integration Drive Market Success

For established players to maintain their market position, continuous investment in advanced packaging technologies and process innovations is crucial. Companies need to focus on developing solutions for emerging applications in 5G, artificial intelligence, and Internet of Things devices while maintaining cost competitiveness. Building strong relationships with both upstream suppliers and downstream customers is becoming increasingly important, as is the ability to offer customized solutions for different end-user segments. Successful incumbents are those who can balance technological advancement with operational efficiency while maintaining flexibility in their manufacturing processes.

New entrants and smaller players can gain market share by focusing on specialized market segments or emerging applications where established players may have less presence. Success factors include developing expertise in specific packaging technologies, forming strategic partnerships with larger players for technology access and market reach, and maintaining agility in responding to changing market demands. The industry's high customer concentration in sectors like mobile devices and computing requires players to diversify their customer base while building long-term relationships with key accounts. While substitution risk from alternative packaging technologies exists, the growing complexity of semiconductor devices continues to favor flip chip technology, though regulatory compliance, particularly in environmental standards, remains a critical consideration. The semiconductor packaging market is poised for growth as companies innovate to meet these demands, with chip packaging playing a crucial role in addressing the evolving needs of the industry.

Flip Chip Technology Market Leaders

-

Amkor Technology Inc.

-

UTAC Holdings Ltd

-

Taiwan Semiconductor Manufacturing Co. (TSMC)

-

Chipbond Technology Corporation

-

TF-AMD Microlectronics Sdn Bhd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Flip Chip Technology Market News

- July 2022 - Luminus Devices Inc, which is engaged in designing and making LEDs and solid-state technology (SST) light sources for illumination markets, announced the launch of MP-3030-110F flip-chip LEDs. The flip-chip design means no wire bond, creating higher reliability, along with enhanced sulfur resistance for robust performance ideal for horticulture applications and for outdoor and harsh lighting environment applications.

- March 2021 - TF-AMD Penang provided RM404,250 in research grants to UTU to carry out collaborative projects in automated robotics technology. This agreement will create a platform for both parties to collaborate on research and development in automated robotics, as well as seminars, lectures, and workshops that will facilitate knowledge sharing and network expansion and will also facilitate industrial internships and graduations for TAR students.

Flip Chip Technology Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increasing Demand for Wearable Devices

- 5.1.2 Strong Growth in MMIC (Monolithic Microwave IC) Applications

-

5.2 Market Challenge

- 5.2.1 Higher Costs Associated with the Technology

6. TECHNOLOGY SNAPSHOT

7. MARKET SEGMENTATION

-

7.1 By Wafer Bumping Process

- 7.1.1 Copper Pillar

- 7.1.2 Tin-Lead Eutectic Solder

- 7.1.3 Lead Free Solder

- 7.1.4 Gold Stud Bumping

-

7.2 By Packaging Technology

- 7.2.1 BGA (2.1D/2.5D/3D)

- 7.2.2 CSP

-

7.3 By Product (Only Qualitative Analysis)

- 7.3.1 Memory

- 7.3.2 Light Emitting Diode

- 7.3.3 CMOS Image Sensor

- 7.3.4 SoC

- 7.3.5 GPU

- 7.3.6 CPU

-

7.4 By End User

- 7.4.1 Military and Defense

- 7.4.2 Medical and Healthcare

- 7.4.3 Industrial Sector

- 7.4.4 Automotive

- 7.4.5 Consumer Electronics

- 7.4.6 Telecommunications

-

7.5 By Geography

- 7.5.1 China

- 7.5.2 Taiwan

- 7.5.3 United States

- 7.5.4 South Korea

- 7.5.5 Malaysia

- 7.5.6 Singapore

- 7.5.7 Japan

8. COMPETITIVE LANDSCAPE

-

8.1 Company Profiles*

- 8.1.1 Amkor Technology Inc.

- 8.1.2 UTAC Holdings Ltd

- 8.1.3 Taiwan Semiconductor Manufacturing Company Limited

- 8.1.4 Chipbond Technology Corporation

- 8.1.5 TF AMD Microlectronics Sdn Bhd

- 8.1.6 Jiangsu Changjiang Electronics Technology Co. Ltd

- 8.1.7 Powertech Technology Inc.

- 8.1.8 ASE Industrial Holding Ltd (Siliconware Precision Industries Co. Ltd)

9. INVESTMENT ANALYSIS

10. FUTURE OF THE MARKET

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Flip Chip Technology Industry Segmentation

Flip-chip technology is one of the oldest and most widely used techniques for semiconductor packaging. Flip-chip was originally introduced by IBM 30 years ago. Nevertheless, it is keeping up with the times and developing new bumping solutions to serve advanced technologies such as 2.5D and 3D. Flip chip is used for traditional applications, such as Laptops, Desktops, CPU, GPU, chipsets, etc.

| By Wafer Bumping Process | Copper Pillar |

| Tin-Lead Eutectic Solder | |

| Lead Free Solder | |

| Gold Stud Bumping | |

| By Packaging Technology | BGA (2.1D/2.5D/3D) |

| CSP | |

| By Product (Only Qualitative Analysis) | Memory |

| Light Emitting Diode | |

| CMOS Image Sensor | |

| SoC | |

| GPU | |

| CPU | |

| By End User | Military and Defense |

| Medical and Healthcare | |

| Industrial Sector | |

| Automotive | |

| Consumer Electronics | |

| Telecommunications | |

| By Geography | China |

| Taiwan | |

| United States | |

| South Korea | |

| Malaysia | |

| Singapore | |

| Japan |

Need A Different Region or Segment?

Customize Now

Flip Chip Technology Market Research FAQs

What is the current Flip Chip Technology Market size?

The Flip Chip Technology Market is projected to register a CAGR of 5.91% during the forecast period (2025-2030)

Who are the key players in Flip Chip Technology Market?

Amkor Technology Inc., UTAC Holdings Ltd, Taiwan Semiconductor Manufacturing Co. (TSMC), Chipbond Technology Corporation and TF-AMD Microlectronics Sdn Bhd. are the major companies operating in the Flip Chip Technology Market.

Which is the fastest growing region in Flip Chip Technology Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Flip Chip Technology Market?

In 2025, the Asia-Pacific accounts for the largest market share in Flip Chip Technology Market.

What years does this Flip Chip Technology Market cover?

The report covers the Flip Chip Technology Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Flip Chip Technology Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Flip Chip Technology Market Research

Mordor Intelligence delivers a comprehensive analysis of the flip chip technology industry. We leverage extensive expertise in semiconductor packaging and advanced packaging solutions. Our research thoroughly examines crucial technologies, including through silicon via, wafer level packaging, and ball grid array implementations. The report provides detailed insights into semiconductor assembly processes, chip interconnect methodologies, and advanced substrate developments. Particular focus is given to copper pillar and solder bump technologies. Our analysis encompasses the complete spectrum of semiconductor backend operations, including die attach processes and wafer bumping techniques.

Stakeholders gain valuable insights through our detailed examination of flip chip packaging innovations, semiconductor interconnect solutions, and controlled collapse chip connection methodologies. The report, available as an easy-to-download PDF, covers emerging trends in advanced IC packaging and chip scale package implementations. Our comprehensive analysis includes a detailed evaluation of C4 bump technology and semiconductor assembly and test processes. This provides crucial information for industry participants involved in flip chip assembly. The report also examines the evolving landscape of the semiconductor packaging industry and wafer level packaging market, offering strategic insights for decision-makers in the semiconductor interconnect market.