Flexible Pipe Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.32 Billion |

| Market Size (2031) | USD 1.69 Billion |

| Growth Rate (2026 - 2031) | 5.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flexible Pipe Market Analysis by Mordor Intelligence

The flexible pipe market size was valued at USD 1.26 billion in 2025 and estimated to grow from USD 1.32 billion in 2026 to reach USD 1.69 billion by 2031, at a CAGR of 5.02% during the forecast period (2026-2031). This growth is traced to deep- and ultra-deepwater exploration programs, rapid material innovation that mitigates corrosion, and expansion in pre-salt developments in Brazil and Guyana. Industry leaders are embedding fiber-optic sensors that deliver real-time integrity data, reducing downtime while lengthening asset life. Asia-Pacific holds the pre-eminent position, propelled by offshore programs in China, India, and Australia and supported by domestic manufacturing that lowers logistics costs. On the materials front, High-Density Polyethylene (HDPE) remains the default choice for operators, yet carbon-fiber and other composite solutions are gaining traction as weight-saving imperatives intensify. Accelerating vertical-integration strategies, such as the proposed Saipem–Subsea7 merger, are redrawing competitive lines by aligning engineering, procurement, construction, and installation (EPCI) capabilities inside one corporate umbrella.

Key Report Takeaways

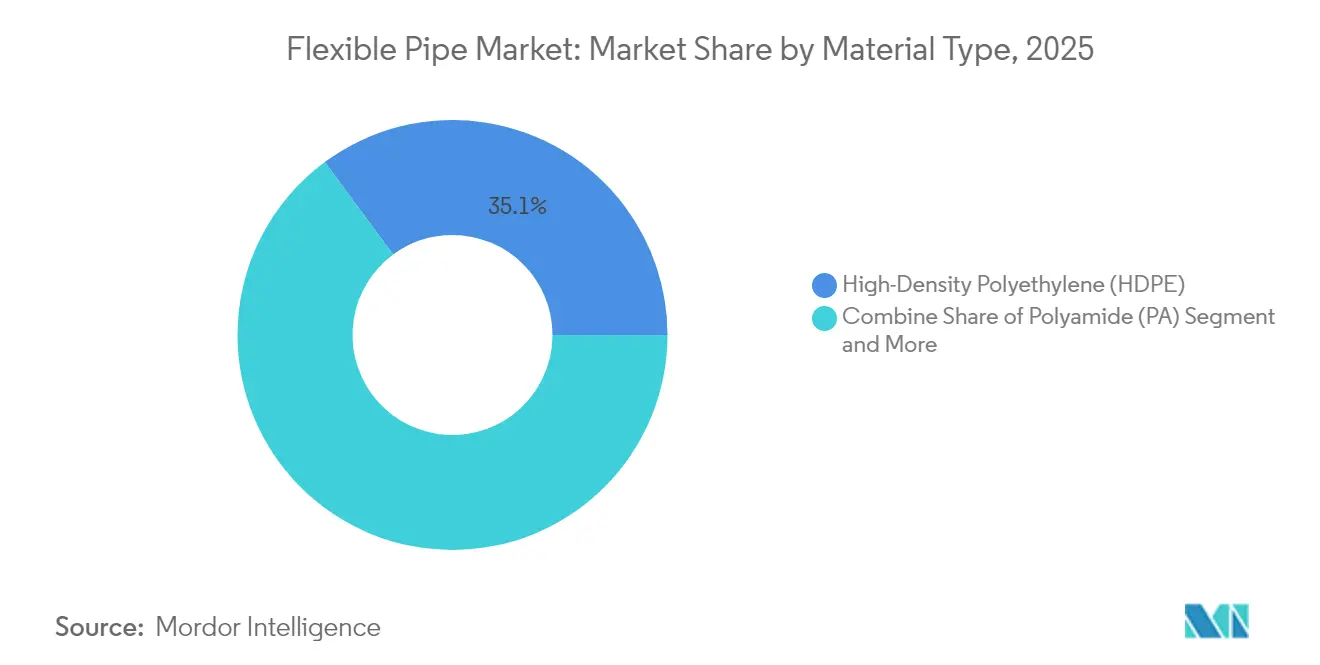

- By material type, HDPE led with 35.12% of flexible pipe market share in 2025, while Other Materials are set to expand at an 8.03% CAGR through 2031.

- By structure, unbonded systems captured 45.08% revenue share in 2025; Reinforced Thermoplastic Pipes are forecast to advance at a 7.12% CAGR to 2031.

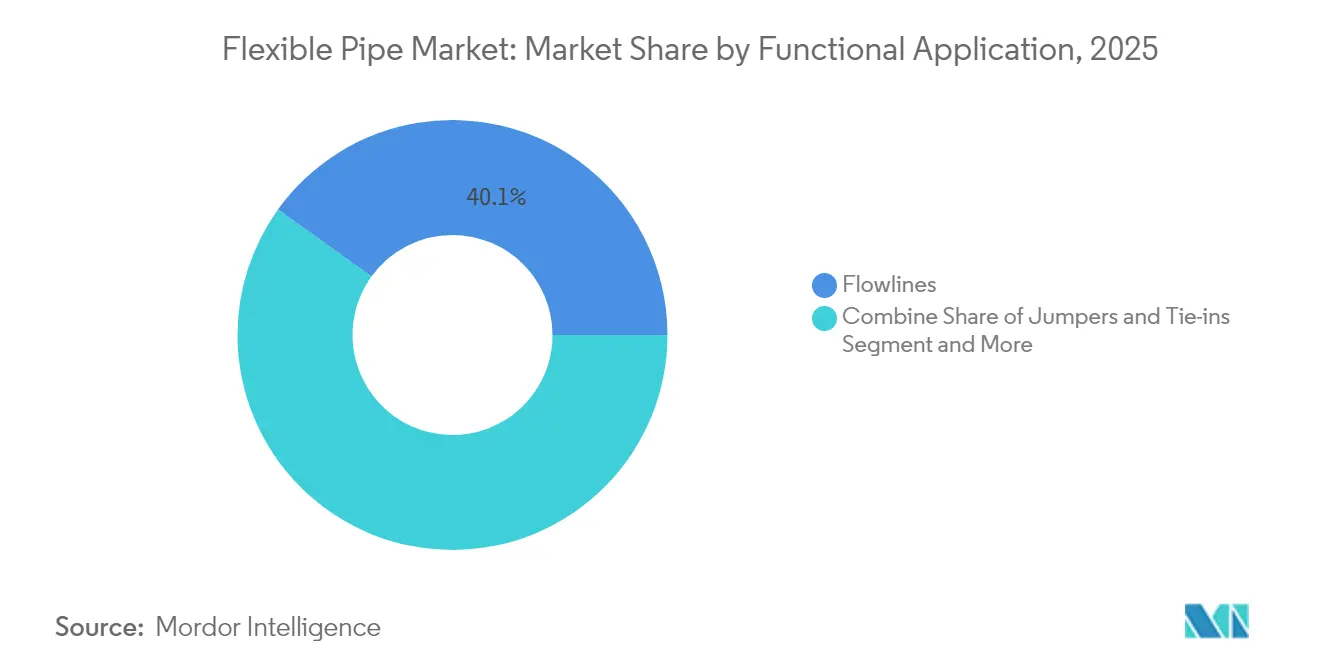

- By function, flowlines commanded 40.07% share of the flexible pipe market size in 2025, whereas jumpers and tie-ins are projected to grow 7.72% CAGR through 2031.

- By environment, offshore installations accounted for 59.74% of the 2025 flexible pipe market; onshore applications exhibit a 6.18% CAGR outlook to 2031.

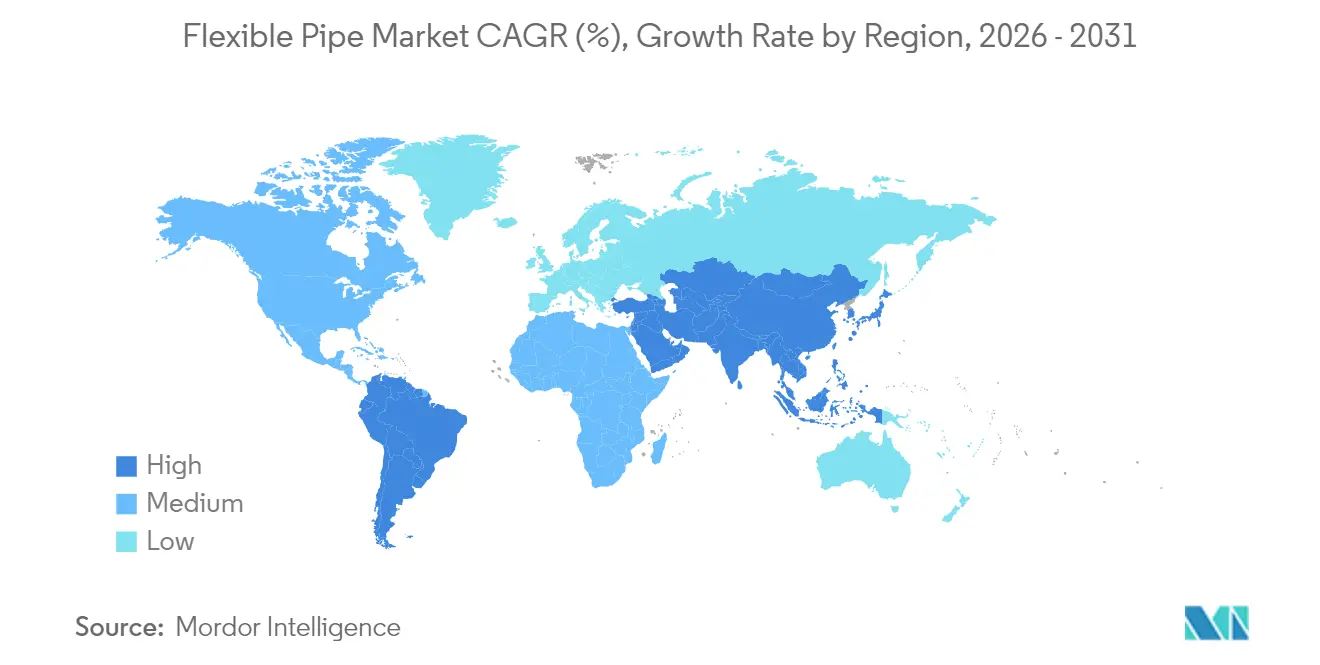

- By geography, Asia-Pacific held 37.78% of global revenue in 2025 and registers the highest regional CAGR at 8.01% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flexible Pipe Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Deep- and ultra-deepwater developments | +1.8% | Brazil, Guyana, Gulf of Mexico | Long term (≥ 4 years) |

| Steel-to-composite replacement | +1.2% | North Sea, Gulf of Mexico | Medium term (2-4 years) |

| SURF megaproject build-out | +0.9% | Brazil, Guyana, spillover West Africa | Medium term (2-4 years) |

| Carbon-fiber armouring for FPSOs | +0.6% | Global deepwater fields | Long term (≥ 4 years) |

| Embedded fiber-optic monitoring | +0.4% | Early roll-out in North Sea, Brazil | Short term (≤ 2 years) |

| Hydrogen / CO₂ transport via flexibles | +0.3% | Europe, North America, expansion to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Deep- and Ultra-Deepwater Developments

Operators are sanctioning projects beyond 1,500 m as rigid steel systems become uneconomic in complex seabed topography. Chevron’s Anchor field inaugurated 20 ksi subsea hardware that sets a new performance bar for the flexible pipe market.[1]Oil & Gas Journal, “Chevron Anchor pioneers 20K subsea development,” ogj.com Brazil’s pre-salt reservoirs impose CO₂-driven corrosion stresses at 2,900 m depth, favoring suppliers with proven composite technology. System-level contracting models such as TechnipFMC’s iEPCI compress schedules by up to 20%, reinforcing demand for integrated flexible solutions.

Replacement of Corroded Steel Lines with Composites

Annual offshore corrosion expenses reach USD 2.5 billion, elevating the economics of composite retrofits that sidestep cathodic protection. Saipem’s plastic-lined pipeline technology trims costs by 40% while sustaining 1,000 bar ratings. North Sea operators confront a 10,000 km legacy grid dating back pre-1990; flexible pipe systems slot into existing corridors without heavy-lift spreads, cutting retrofit downtime. Embedded sensors inside Baker Hughes’ non-metallic products feed integrity analytics that replace labor-intensive inspection rounds.

SURF Megaproject Pipeline in Brazil and Guyana

Petrobras alone has committed over USD 50 billion to subsea umbilicals, risers, and flowlines, including 77 km of high-specification flexible pipe for pre-salt tie-backs. Guyana’s Whiptail field requires 10 ksi, 1,600 m flexible jumpers that Strohm fabricates from carbon-fiber and PA12 to slash installation weight. Clustered demand fosters regional factories, exemplified by TechnipFMC’s new Asian plant, which shortens delivery cycles for Asia-Pacific orders.

Embedded Fibre-Optic Health Monitoring

Continuous integrity surveillance is migrating from topside assets into the pipe wall itself, with fibre-optic strands embedded between pressure and tensile layers capturing temperature, strain and vibration data along the entire length of the line. Early deployments in the North Sea and Brazil show operators cutting unscheduled riser shutdowns by up to 25% because anomaly detection algorithms flag fatigue hot spots months before failure. Real-time analytics shorten inspection campaigns and remove the need for periodic annulus vent testing, trimming annual OPEX by roughly USD 1 million for a typical FPSO spread. The monitoring layer also supplies live fatigue damage accumulation curves that allow dynamic re-rating of design life, enabling producers to defer costly replacement scopes without compromising safety. As digital twins mature, sensor-rich flexibles will feed field-wide optimisation platforms, creating a data-service revenue stream for pipe suppliers that extends beyond the initial sale. This capability underpins the +0.4% uplift on forecast CAGR attributed to the driver, especially in regions with strict uptime targets and high vessel day rates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-oil price volatility | -1.4% | North America, North Sea | Short term (≤ 2 years) |

| Higher upfront cost vs. rigid steel | -0.8% | Global, amplified in cost-sensitive | Medium term (2-4 years) |

| Polymer end-of-life recycling gaps | -0.6% | Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| Tight capacity for 20 ksi-rated pipes | -0.4% | Ultra-deepwater regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Oil Price Volatility Curbs CAPEX

Price swings in the USD 70–90 per-barrel band delay final investment decisions as boards now demand 18–24 months’ price stability before greenlighting offshore projects. [2]Dallas Fed, “Oil and gas industry shows discipline on CAPEX,” dallasfed.org Higher interest rates lift hurdle thresholds, further deferring sanctioning. [3]Financial Innovation, “Uncertainty about Interest Rates and Crude Oil Prices,” jfin-swufe.springeropen.comMature North Sea and Gulf of Mexico fields are particularly vulnerable because flexible pipes constitute up to 20% of total project CAPEX, rendering economics price sensitive.

Higher Upfront Cost Versus Rigid Steel

Flexible systems carry a 25–40% material premium, a hurdle heightened in short-distance projects where installation efficiencies do not offset cost gaps. High-pressure (more than 20 ksi) requirements are still capacity constrained, inflating delivery lead times and pushing some operators back toward steel.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: HDPE Retains Primacy as Composites Surge

Flexible pipe market size for HDPE reached USD 0.44 billion in 2025, translating into 35.12% revenue dominance. Operators value HDPE for cost-efficient extrusion, chemical inertia, and weld-free joints. Still, Other Materials—chiefly carbon-fiber and advanced polymers—record an 8.03% CAGR, outstripping incumbents as floating production systems chase mass savings to ease topside loading. University of Sydney forecasts CFRP waste streams hitting 500,000 t by 2030, intensifying circular-economy pressures that could redirect R&D toward recyclable resins.

Material innovators push flexible pipe market share gains by enhancing fatigue life and temperature windows. Advanced PA and PVDF layers deliver 130 °C service, expanding flexible deployment into high-HTHP wells. Thermoplastic composite pipes (TCP) marry carbon-fiber tensile casing with a PA12 liner to achieve zero corrosion and low-friction flow profiles. As deepwater activity scales, composite uptake is expected to raise Other Materials’ contribution to one-third of the flexible pipe market by 2031.

By Pipe Structure Type: Unbonded Dominance Persists, RTP Accelerates

Unbonded architectures accounted for 45.08% of global revenue in 2025, capitalizing on multilayered armor that decouples hoop and axial loads. Their repairability underpins preference in dynamic riser applications. Yet Reinforced Thermoplastic Pipes, devoid of metallic carcasses, expand 7.12% CAGR as operators target corrosion-free performance and lighter deck loads. FlexSteel’s spoolable RTP solutions eliminate anodes and coating campaigns, lowering OPEX in brownfield tie-ins.

Structural choice in the flexible pipe market hinges on fatigue, pressure, and chemical exposure profiles. Bonded pipes serve niche ultra-high-pressure flowlines but are handicapped by limited field repair options and higher cost. Innovations in aramid and glass-fiber winding, coupled with digital twins tracking fatigue accumulation, will allow RTP to penetrate riser duty where strength limits once blocked entry.

By Functional Application: Flowlines Sustain Core Revenue

Flowlines contributed USD 0.5 billion in 2025, equal to 40.07% of flexible pipe market share, reflecting their indispensability in well-to-facility transfer. Jumpers and tie-ins, however, post a 7.72% CAGR steered by modular field designs that enlarge inter-well connection counts. Offshore Magazine notes alliances are co-developing standardized jumper kits that quick-connect to manifold hubs, compressing installation windows.

Future growth in sacrificial application categories—export hoses for floating storage, or hybrid power umbilicals—suggests function-specific composites will be co-engineered with topside processing to unlock system efficiencies. Embedded fiber bragg grating sensors along jumpers illustrate how digital twins are migrating from topside to subsea, using data governance frameworks to optimize drawdown and mitigate slugging.

By Installation Environment: Offshore Retains Majority, Onshore Gains

Offshore settings commanded 59.74% of 2025 revenue, anchored by deep- and ultra-deepwater demand in Brazil, Guyana, and the Gulf of Mexico. Installation speeds—up to 3 km per day with reel-lay—keep flexible solutions cost-competitive despite higher unit prices. Onshore adoption, though smaller, is rising at 6.18% CAGR as midstream operators recognise spoolable composites cut trench width and traffic disruption. Regulatory interest in hydrogen pipelines furthers the case for non-metallic onshore flexibles able to withstand embrittlement.

Ultra-deepwater categories (>1,500 m) require 20 ksi ratings, a capacity that only a handful of mills currently supply. Lead-time constraints here elevate EPC risks and have led Petrobras and ExxonMobil to negotiate multi-year call-off agreements with qualified mills to guarantee slot allocation.

Geography Analysis

Asia-Pacific retained 37.78% of 2025 revenue on the back of South China Sea deepwater blocks and Australian LNG backfill programs. The region’s flexible pipe market size is forecast to rise at an 8.01% CAGR, outpacing all others. Government policy favoring local content spurs construction of regional manufacturing hubs, such as TechnipFMC’s plant in Southeast Asia that shortens reel-lay lead times for Chinese and Indian operators. Growing offshore wind deployment in Japan and Korea creates spill-over demand for subsea power cables and dynamic umbilicals, further nurturing composite capability cross-fertilization.

North America follows as the second-largest region, underpinned by Gulf of Mexico ultra-deepwater sanctions that require 20 ksi flexible jumpers. Anadarko basin gathering lines and Permian hydrogen demonstration projects drive onshore spoolable adoption. Yet regional CAGR lags Asia-Pacific because the replacement wave in the Gulf is offset by plateauing discovery rates.

Europe shows balanced growth built on North Sea life-extension projects and nascent hydrogen backbone pilots across Norway and the United Kingdom. Strict decommissioning legislation accelerates removal of ageing steel, offering retrofit openings for flexible line substitution in tie-back schemes. Recycling mandates, however, require suppliers to propose closed-loop models for polymer recovery, potentially elevating total installed cost.

Middle East and Africa register rapid adoption as QatarEnergy’s North Field Compression Program and West Africa’s FPSO campaigns solicit corrosion-immune composites. Saipem’s USD 4 billion EPC award in Qatar confirms regional appetite for high-specification flowlines and optic-fiber-infused umbilicals. Turkey’s Sakarya Phase 2 calls for 158 km of 2,200 m-rated pipe, signalling Black Sea basin maturation. South America, anchored by Brazil’s pre-salt and Guyana’s Stabroek block, remains a central pillar, accounting for the bulk of global SURF backlogs and reinforcing manufacturers’ decision to co-locate spool-bases near Rio.

Regulatory Landscape

Standards and certification frameworks shape flexible pipe qualification, particularly for subsea applications. API Specification 17J (Edition 5, released May 2024 and effective May 2025) tightened requirements around design and manufacturing verification, including more stringent Independent Validation and Certification (IVA) expectations for unbonded flexible pipe systems. It also added further consideration for carbon capture, transport, and storage (CCS) service conditions. Operators typically require Type Approval and third-party certification against the API 17-series suite (including API 17J, 17K, and 17L1), so documentation, material traceability, and audit-ready manufacturing controls function as a practical gate to market.

Compliance is further influenced by end-use and customer specifications. National oil companies and major operators apply their own technical standards for procurement, testing, and acceptance of flexible pipes in deepwater developments. While EU Regulation (EU) 2025/40 on packaging and packaging waste (entered into force February 2025, applying from August 2026) sets recycled-content and circularity requirements for plastic packaging, those rules are distinct from energy-infrastructure flexible pipe applications. Within oil and gas flexible pipe qualification, and for emerging CO2 and hydrogen use cases, API-driven qualification and third-party assurance remain the primary regulatory and standards anchors.

Competitive Landscape

Consolidation is accelerating, driving moderate concentration in the flexible pipe market. Saipem and Subsea7’s proposed EUR 20 billion merger would assemble more than 60 construction vessels, enabling cradle-to-grave EPCI execution. TechnipFMC’s iEPCI platform has already trimmed tender-to-first-oil timelines by integrating tree, riser, and flowline packages within a single contract envelope, capturing premium margins through schedule certainty.

Strategy revolves around material science and digital enablement. NOV’s OptiFlex embeds fiber-optic strands along annulus layers, generating temperature and strain maps that feed predictive analytics, giving operators an early-maintenance warning system. Baker Hughes bundles non-metallic flexible pipes with its surface equipment portfolio to forge stickier customer relationships, while Strohm’s thermoplastic composite designs promise corrosion immunity and simplified lay-up for marginal field tie-backs.

Intellectual-property barriers remain high for 20 ksi composite carcasses and bonding techniques, yet regional spool-bases are proliferating, diluting shipping costs advantage formerly held by incumbents. Patent filings in smart materials and embedded sensing suggest differentiation will increasingly pivot on data services rather than pipe alone.

Flexible Pipe Industry Leaders

National Oilwell Varco (NOV)

GE Oil & Gas Corporation

TechnipFMC PLC

The Prysmian Group

Shawcor Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Deepwater SURF backlogs and Africa-focused project awards point to white space for suppliers that can deliver flexible flowlines and risers with shorter lead times and local execution. TechnipFMC contract wins tied to Eni’s Baleine Phase 3 in Cote d’Ivoire (July 2026) and Azule Energy’s Greater PAJ development offshore Angola (June 2026) reflect demand for integrated delivery models that combine engineering with flexible pipe supply, especially where installation schedules favor reel-lay and standardized subsea architectures. On the supply side, NOV’s USD 200 million expansion plan for its Açu, Brazil subsea flexible pipe facility (announced March 2026) signals how capacity additions and localization are being used to secure long-cycle programs in Brazil’s pre-salt and adjacent basins.

Technology development is also opening up room in ultra-deepwater and corrosive service, where conventional solutions face weight, fatigue, and CO2 exposure constraints. Baker Hughes and Strohm’s May 2026 collaboration to develop and qualify a hybrid flexible pipe (combining thermoplastic composite pipe with traditional flexible pipe technology) indicates a route to higher-performance product tiers for tougher deepwater duty. Strohm’s May 2026 TCP flowline contract for a West Delta Deep Marine gas development offshore Egypt further demonstrates commercial pull for thermoplastic composite solutions beyond pilot deployments, supporting opportunities for suppliers that can scale qualification, certification, and manufacturing repeatability for composite and hybrid designs.

Recent Industry Developments

- July 2026: TechnipFMC was awarded a contract by Eni to supply flexible flowlines and risers for the Baleine Phase 3 development offshore Cote d’Ivoire. The award adds to TechnipFMC’s subsea execution footprint in West Africa and reinforces demand for integrated subsea delivery where flexible products help compress installation schedules.

- March 2026: NOV announced a USD 200 million investment to expand its subsea flexible pipe manufacturing facility in Açu, Brazil, with the project targeting roughly double capacity by late 2029. The expansion supports long-cycle deepwater programs in Brazil and strengthens NOV’s ability to compete on lead time and localization for pre-salt flexible pipe demand.

- September 2024: TechnipFMC secured subsea contracts from Petrobras for Brazil’s pre-salt fields, including flexible pipe scope for riser applications. The awards lock in multi-year manufacturing workload in a core demand center and highlight how operator procurement favors qualified suppliers with proven deepwater execution.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from flexible pipe systems used to transport fluids in industrial settings, including pipes deployed in offshore and onshore environments. Values reflect sales of flexible pipe products used across energy and other process applications.

Scope exclusions: Excluded from this sizing are rigid steel pipelines and standard corrugated piping used mainly in civil drainage and building plumbing.

Segmentation Overview

- By Material Type

- High-Density Polyethylene (HDPE)

- Polyamide (PA)

- Polyvinylidene Fluoride (PVDF)

- Others Material Type

- By Pipe Structure Type

- Unbonded Flexible Pipe

- Bonded Flexible Pipe

- Reinforced Thermoplastic Pipe (RTP)

- By Functional Application

- Flowlines

- Risers

- Jumpers and Tie-ins

- Export / Loading Hoses

- By Installation Environment

- Offshore

- Shallow Water (Less than 500 m)

- Deepwater (500-1500 m)

- Ultra-deepwater (More than 1500 m)

- Onshore

- Offshore

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the fact base for demand drivers and supply conditions that influence flexible pipe revenues. We referenced public sources such as energy statistics from agencies like the EIA and IEA, offshore activity and safety documentation from regulators like BSEE, and trade flows from UN Comtrade style customs statistics to gauge import reliance in key hubs.

To keep inputs anchored, we also reviewed company annual reports, investor presentations, project announcements, and reputable industry news for signals on offshore developments, subsea tiebacks, and pipeline spending cycles. Select paid subscriptions for company financials and intelligence, patent databases, and an import export shipment level database were used to cross-check product positioning, production footprints, and pricing direction. These sources are illustrative only, and other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with a mix of manufacturers, distributors, EPC participants, and end users that procure flexible pipe for offshore and onshore projects. We used these discussions to confirm what gets counted as a flexible pipe sale, validate typical application splits (for example, flowlines, risers, and jumpers), and pressure-test pricing and replacement cycles across major regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 15% | APAC: 50% |

| Mid tier: 53% | Functional/Unit leaders: 29% | EMEA: 31% |

| Smaller Players: 15% | Managers: 56% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where offshore and onshore pipe demand is reconstructed using project activity and installed base signals, and then translated into revenue using observed price bands. The totals are then corroborated through selective bottom-up approximations, like sampling supplier revenues, checking distributor channel feedback, and applying typical ASP multiplied by estimated meters installed for common applications.

Inputs used in the model include offshore project count and timing, subsea tieback intensity, replacement and inspection driven demand, material mix shifts (for example, HDPE versus polyamide and other polymers), and average project level pipe length by application. Where direct volume indicators are thin for a country, we filled gaps using proxy indicators such as nearby offshore capex cycles and trade patterns, then confirmed reasonableness with expert feedback.

For forecasting, scenario analysis was used to reflect differences in offshore sanctioning pace and cost inflation, and assumptions were aligned to what interviewees expected for project pipelines and maintenance cycles. Growth rates were not applied as a single blanket factor, since price movement and installation activity can diverge by region and environment.

Data Validation & Update Cycle

Outputs are checked against independent signals like offshore activity momentum, announced field developments, and import and export movements in major supplying regions. When the model produces unusual jumps, the underlying drivers are re-checked, assumptions are revisited, and respondents are re-contacted if the variance cannot be explained by a known event.

Before sign-off, the work goes through multi-step internal review so calculation logic, units, and currency treatment remain consistent. The report is refreshed annually, and interim updates are made when material events occur, followed by a final pre-delivery review so clients receive the latest updated view.

Mordor Intelligence's Flexible Pipe Market Size Compared Against Other Published Estimates

Published market values for flexible pipe can look different because sources do not always count the same products, and they may anchor the math to different base years and price assumptions. Currency timing, inflation treatment, and how offshore project timing is mapped into annual demand can also move the number.

Rigid steel pipeline revenue sits outside Mordor Intelligence's scope, which narrows the total to flexible pipe sales tied to identified applications and deployment environments instead of the broader pipeline spending pool. Differences also come from how mixed portfolios are handled (for example, whether export hoses or adjacent composite tubing is bundled in), and whether a study uses a single CAGR over a long window rather than re-rating years where offshore sanctions slow down or speed up.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.32 B (2026) | |

| Global Consultancy A | USD 1.30 B (2024) | Uses an earlier base year and can blend offshore activity cycles differently, so the annualized demand timing may not match project sanction realities in 2025 to 2027. |

| Industry Research Group B | USD 1.12 B (2025) | Often applies broader average pricing and may not fully normalize currency and resin-linked price shifts across regions, which can compress the near-term value estimate. |

From the table, the spread is mainly explained by year selection and what is counted as flexible pipe revenue versus adjacent piping spend, and then by how pricing and currency are carried through the model. Our sizing stays traceable because each major driver is linked back to activity signals, price bands, and interview checks, which makes the steps easier to repeat when new projects or cost changes appear.

Key Questions Answered in the Report

What is the current size of the flexible pipe market?

The flexible pipe market size stands at USD 1.32 billion in 2026 and is forecast to reach USD 1.69 billion by 2031.

Which region leads the flexible pipe market?

Asia-Pacific holds the largest share at 37.78% in 2025, buoyed by deepwater projects in China, India, and Australia.

What material dominates flexible pipe production?

HDPE leads with 35.12% market share, yet composite alternatives such as carbon-fiber display the fastest growth trajectory.

How does crude-oil price volatility affect flexible pipe demand?

Price swings between USD 70–90 per barrel can delay offshore project sanctions, dampening near-term orders for new flexible pipe systems.

Which application segment is expanding the fastest?

Jumpers and tie-ins are projected to grow at a 7.72% CAGR as modular subsea field designs raise inter-connection requirements.

What competitive moves are reshaping the industry?

The planned Saipem–Subsea7 merger and TechnipFMC’s integrated iEPCI contracts illustrate the sector’s shift toward vertically integrated, digital-enabled project delivery models.

Page last updated on: