Market Size of Flexible Packaging Industry

| Study Period | 2019-2029 |

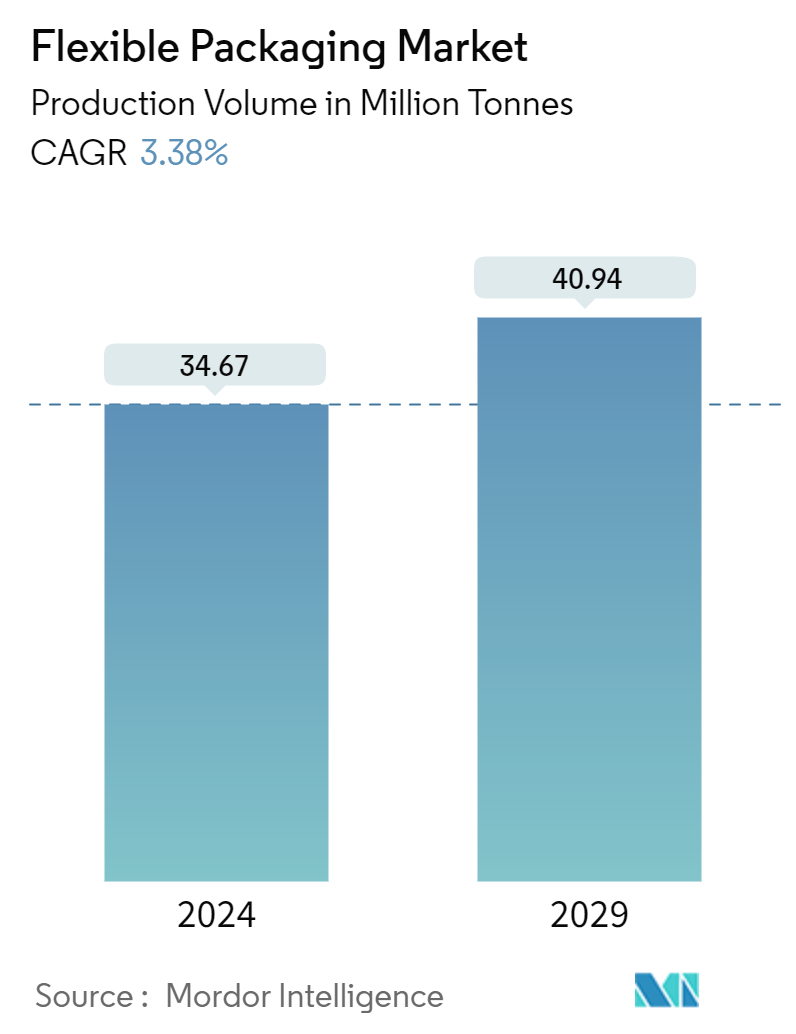

| Market Volume (2024) | 34.67 Million tonnes |

| Market Volume (2029) | 40.94 Million tonnes |

| CAGR (2024 - 2029) | 3.38 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Flexible Packaging Market Analysis

The Flexible Packaging Market size in terms of production volume is expected to grow from 34.67 Million tonnes in 2024 to 40.94 Million tonnes by 2029, at a CAGR of 3.38% during the forecast period (2024-2029).

The flexible packaging market is driven by a combination of factors, including increasing demand for convenient and lightweight packaging solutions, rising consumer awareness toward sustainability, and advancements in packaging technology for improved shelf life and product protection.

- Additionally, the versatility of flexible packaging in accommodating various shapes and sizes, its cost-effectiveness, and ease of transportation further contribute to its growth. As industries prioritize eco-friendly solutions and consumers seek convenience and functionality, the flexible packaging market is poised to expand.

- Higher retail sales often lead to market expansion, with new products entering the market and existing ones reaching broader audiences. Flexible packaging is adaptable to different product categories, making it suitable for various industries, including food and beverage, pharmaceuticals, personal care, and more. Thus, expanding retail sales could drive growth in multiple segments of the flexible packaging market.

- Polyethylene is primarily used for packaging plastic bags, plastic films, geomembranes, etc. It is a lightweight, partially crystalline, low moisture absorbent, thermoplastic resin that has high resistance to chemicals and sound-insulating properties. Low-density polyethylene (LDPE) is mainly used to manufacture plastic bags. LDPE polyethylene bags are soft and flexible, even at low temperatures, and are available in natural colors.

- Recycling and environmental considerations are essential when it comes to packaging. Plastic contamination in oceans and landfills are impacted by packaging trash. Plastic packaging affects the environment's plastic pollution. Plastic can affect marine life and ecosystems since it takes hundreds of years to disintegrate.

- It is expected that this trend will continue. Investments in the kraft paper mills will rise post-COVID-19. The increased use of paper packaging is largely due to the growing e-commerce sector and consumer interest in eco-friendly solutions.

Flexible Packaging Industry Segmentation

The study covers the flexible packaging market tracked in terms of consumption and is only limited to flexible packaging products made from plastic, paper, and aluminum foil. The market is tracked in terms of volume in million tons. This report analyzes the factors that impact geopolitical developments in the market based on the prevalent base scenarios, key themes, and end-user industries-related demand cycles. The estimates exclude the weight of the content that is or is to be packed inside the flexible packaging solution.

The flexible packaging market is segmented by material type (plastic [polyethylene (PE), bi-orientated polypropylene (BOPP), cast polypropylene (CPP), polyvinyl chloride (PVC), ethylene vinyl alcohol (EVOH)], paper, aluminum foil), product type (pouches, bags, films & wraps), end-user industry (food [frozen food, dairy products, fruits & vegetables, meat, poultry, & seafood, baked goods and snack foods, and candy & confections], beverage, pharmaceutical & medical, and household & personal care), and geography (North America [United States, Canada], Europe [United Kingdom, Germany, France, Italy, Spain, Turkey, Poland, Russia, Rest of Europe], Asia-Pacific [China, Japan, India Australia, Rest of Asia Pacific], Latin America [Brazil, Argentina, Mexico, Rest of Latin America], and the Middle East and Africa [United Arab Emirates, Saudi Arabia, South Africa, Egypt, Iran, Nigeria, and Rest of Middle East and Africa]). The market sizes and forecasts are provided in terms of value USD for all the above segments.

| By Material Type | ||||||||

| ||||||||

| Paper | ||||||||

| Aluminum Foil |

| By Product Type | |

| Pouches | |

| Bags | |

| Films & Wraps | |

| Other Product Types (Sachets, Sleeves, Blister Packs, Liners, Laminates, etc.) |

| By End-user Industry | |||||||||

| |||||||||

| Beverage | |||||||||

| Pharmaceutical and Medical | |||||||||

| Household and Personal Care | |||||||||

| Other End-user Industries (Tobacco, Chemical, and Agriculture, Among Others) |

| By Geography | ||||||||||

| ||||||||||

| ||||||||||

| ||||||||||

| ||||||||||

|

Flexible Packaging Market Size Summary

The flexible packaging market is experiencing significant growth, driven by the increasing demand for convenient, lightweight, and sustainable packaging solutions. This growth is further supported by advancements in packaging technology that enhance shelf life and product protection. The versatility of flexible packaging, which can accommodate various shapes and sizes, along with its cost-effectiveness and ease of transportation, makes it an attractive option for industries such as food and beverage, pharmaceuticals, and personal care. As consumer preferences shift towards eco-friendly and functional solutions, the market is poised for expansion. The rise in retail sales, coupled with the adaptability of flexible packaging to different product categories, is expected to drive growth across multiple segments.

In addition to the demand for flexible packaging, environmental considerations and recycling efforts are becoming increasingly important. The market is witnessing a trend towards the use of sustainable materials, such as kraft paper, driven by the growing e-commerce sector and consumer interest in eco-friendly solutions. Key players in the industry, including Amcor Group GmbH, Mondi Group, and Berry Global Inc., are actively engaging in product innovation and strategic partnerships to enhance their market position. These companies are investing in recycling capabilities and developing sustainable packaging solutions to meet the rising demand for high-performing, eco-friendly products. As the market continues to evolve, the focus on sustainability and innovation is expected to play a crucial role in shaping its future trajectory.

Flexible Packaging Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Buyers

-

1.2.2 Bargaining Power of Suppliers

-

1.2.3 Threat of Substitutes

-

1.2.4 Threat of New Entrants

-

1.2.5 Intensity of Competitive Rivalry

-

-

1.3 Industry Value Chain Analysis

-

-

2. MARKET SEGMENTATION

-

2.1 By Material Type

-

2.1.1 Plastic

-

2.1.1.1 Polyethene (PE)

-

2.1.1.2 Bi-orientated Polypropylene (BOPP)

-

2.1.1.3 Cast polypropylene (CPP)

-

2.1.1.4 Polyvinyl Chloride (PVC)

-

2.1.1.5 Ethylene Vinyl Alcohol (EVOH)

-

2.1.1.6 Other Plastic Types (PA, Bioplastics)

-

-

2.1.2 Paper

-

2.1.3 Aluminum Foil

-

-

2.2 By Product Type

-

2.2.1 Pouches

-

2.2.2 Bags

-

2.2.3 Films & Wraps

-

2.2.4 Other Product Types (Sachets, Sleeves, Blister Packs, Liners, Laminates, etc.)

-

-

2.3 By End-user Industry

-

2.3.1 Food

-

2.3.1.1 Frozen and Chilled Food

-

2.3.1.2 Dairy Products

-

2.3.1.3 Fruits and Vegetables

-

2.3.1.4 Meat, Poultry, and Seafood

-

2.3.1.5 Baked Goods and Snack Foods

-

2.3.1.6 Candy and Confections

-

2.3.1.7 Other Food Products

-

-

2.3.2 Beverage

-

2.3.3 Pharmaceutical and Medical

-

2.3.4 Household and Personal Care

-

2.3.5 Other End-user Industries (Tobacco, Chemical, and Agriculture, Among Others)

-

-

2.4 By Geography

-

2.4.1 North America

-

2.4.1.1 United States

-

2.4.1.2 Canada

-

-

2.4.2 Europe

-

2.4.2.1 United Kingdom

-

2.4.2.2 Germany

-

2.4.2.3 France

-

2.4.2.4 Italy

-

2.4.2.5 Spain

-

2.4.2.6 Turkey

-

2.4.2.7 Poland

-

2.4.2.8 Russia

-

-

2.4.3 Asia

-

2.4.3.1 China

-

2.4.3.2 Japan

-

2.4.3.3 India

-

2.4.3.4 Australia

-

-

2.4.4 Latin America

-

2.4.4.1 Brazil

-

2.4.4.2 Argentina

-

2.4.4.3 Mexico

-

-

2.4.5 Middle East and Africa

-

2.4.5.1 United Arab Emirates

-

2.4.5.2 Saudi Arabia

-

2.4.5.3 South Africa

-

2.4.5.4 Egypt

-

2.4.5.5 Iran

-

2.4.5.6 Nigeria

-

-

-

Flexible Packaging Market Size FAQs

How big is the Flexible Packaging Market?

The Flexible Packaging Market size is expected to reach 34.67 million tonnes in 2024 and grow at a CAGR of 3.38% to reach 40.94 million tonnes by 2029.

What is the current Flexible Packaging Market size?

In 2024, the Flexible Packaging Market size is expected to reach 34.67 million tonnes.