| Study Period | 2019 - 2030 |

| Market Volume (2025) | 35.84 Million tonnes |

| Market Volume (2030) | 42.32 Million tonnes |

| CAGR | 3.38 % |

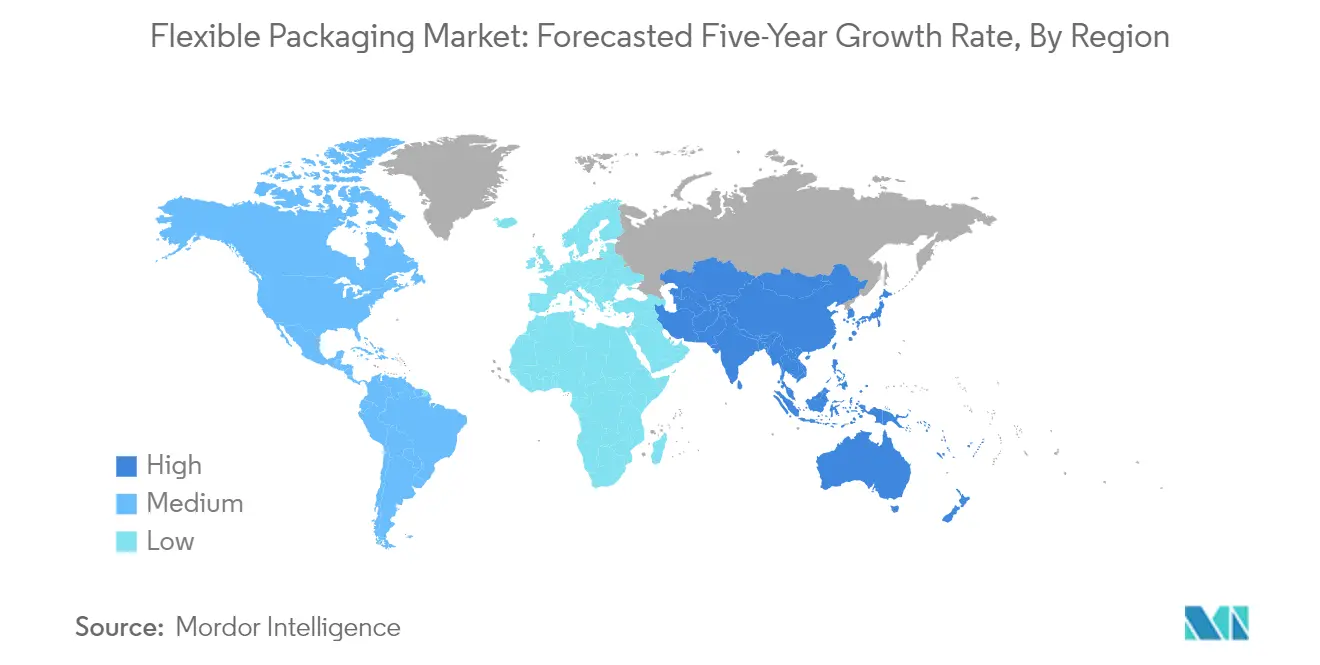

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

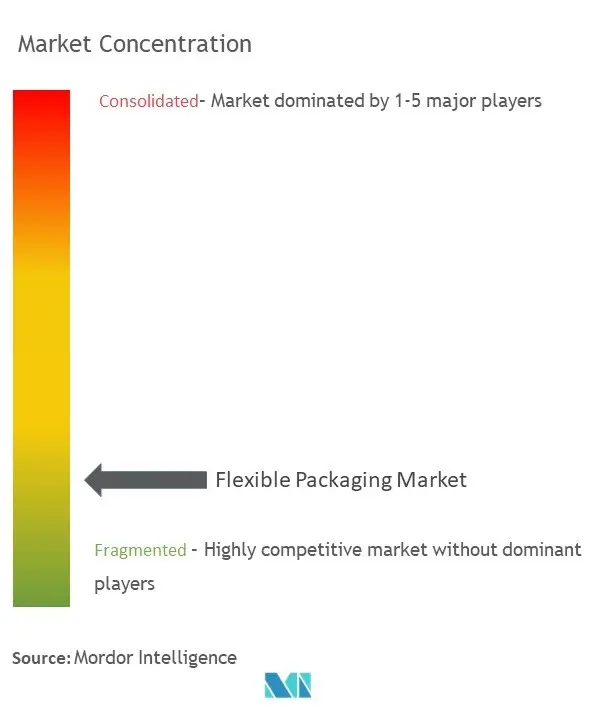

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Flexible Packaging Industry Analysis

The Flexible Packaging Industry in terms of production volume is expected to grow from 35.84 million tonnes in 2025 to 42.32 million tonnes by 2030, at a CAGR of 3.38% during the forecast period (2025-2030).

The flexible packaging industry is experiencing significant transformation driven by technological advancements and evolving consumer preferences. The federal government's allocation of resources to over two dozen technology hubs across the United States in October 2024, focusing on polymer research and sustainable materials, is reshaping the industry landscape. These hubs are driving improvements in materials science, creating more sustainable flexible packaging solutions that are cost-effective and high-performance. The integration of smart packaging technologies, including RFID tags, QR codes, and sensors, is enhancing traceability and quality control. According to the United States Census Bureau, retail sales reached USD 7,242.56 billion in 2023, indicating strong consumer demand and market expansion opportunities.

The Asia-Pacific region is witnessing remarkable innovations in packaging solutions, particularly in Japan and China. Japanese manufacturers are leading the way in retort pouch technology, with curry emerging as the dominant retort food pouch product, achieving a production volume of approximately 157.54 thousand tons in 2022. The industry is seeing increased adoption of advanced recycling processes, with companies like Toppan, Mitsui Chemicals Tohcello, and Mitsui Chemicals collaborating on pilot projects to recycle printed BOPP films into fresh, flexible packaging materials. These initiatives are establishing new benchmarks for horizontal recycling in the flexible packaging sector.

The Middle East is emerging as a significant hub for flexible packaging trends, particularly in sustainable solutions. In April 2023, Hotpack Global announced a substantial investment of SAR 1 billion (USD 266 million) to establish one of the world's largest sustainable packaging facilities in Saudi Arabia. The Dubai Department of Economy and Tourism reported 1.77 million visitors in January 2024, representing a 21% increase compared to January 2023, driving demand for convenient and sustainable packaging solutions. This growth is accompanied by increasing emphasis on eco-friendly materials and manufacturing processes.

The industry is witnessing a significant shift toward circular economy principles, with major players investing in recyclable and sustainable solutions. Companies are increasingly focusing on developing mono-material solutions and improving recycling infrastructure. For instance, in November 2023, JBM Packaging unveiled Hydroblox, an eco-friendly flexible packaging product offering a sustainable, water-repellent solution. The product demonstrates 200% greater water resistance compared to standard white woven paper, marking a significant advancement in sustainable flexible packaging technology. This trend is further supported by stringent regulations and growing consumer awareness about environmental impact.

Flexible Packaging Industry Trends

Increased Demand for Convenient Packaging

The growing urban lifestyle of consumers has significantly driven the demand for convenient packaging solutions. Consumers increasingly seek easy-to-use and lightweight packaging options, prompting vendors to design innovative solutions that meet changing demands while maintaining competitiveness in the growing organized retail market. The shift to lighter materials, such as flexible pouches, provides substantial energy-saving benefits while offering enhanced convenience for consumers.

The rise in supermarket and grocery store sales indicates a strong preference for convenient shopping experiences. According to the US Census Bureau, supermarket and other grocery store sales in 2023 reached USD 846.38 billion, up from USD 756.35 billion in 2021. This substantial growth provides a conducive environment for increased demand in convenient packaging solutions. The trend is further supported by the expansion of organized retail formats and the growing preference for ready-to-eat foods, driving innovation in packaging design to meet specific requirements such as maintaining product freshness, ease of use, and shelf appeal.

Understand The Key Trends Shaping This Market

Download PDF

Demand for Longer Shelf Life and Changing Lifestyles

Consumers increasingly seek products with extended shelf lives due to convenience and the desire to reduce food waste. Flexible packaging offers excellent barrier properties, protecting products from moisture, oxygen, light, and other external factors that can degrade quality and freshness. This extends the shelf life of various perishable goods such as food and beverages, pharmaceuticals, and personal care products. The trend is particularly evident in the frozen food sector, where according to the article by Frozen & Refrigerated Buyer, frozen appetizers and snack rolls accounted for USD 809.75 million in 2023, with pizza being the largest frozen food category with sales exceeding USD 1.5 billion.

The shift in consumer lifestyles, characterized by on-the-go consumption, smaller households, and a growing preference for convenience, has significantly influenced packaging demands. Flexible packaging meets these needs by providing lightweight, portable, and resealable options that fit busy lifestyles. According to the US Department of Agriculture, Germany's food landscape presents opportunities for exporters to tap into the market for plant-based foods, with the number of vegans reaching over 1.5 million in 2022. This demographic shift has led to increased demand for specialized packaging solutions that can maintain product freshness while offering convenience features such as resealable closures and portion-controlled packs.

Segment Analysis: By Material Type

Plastics Segment in Flexible Packaging Market

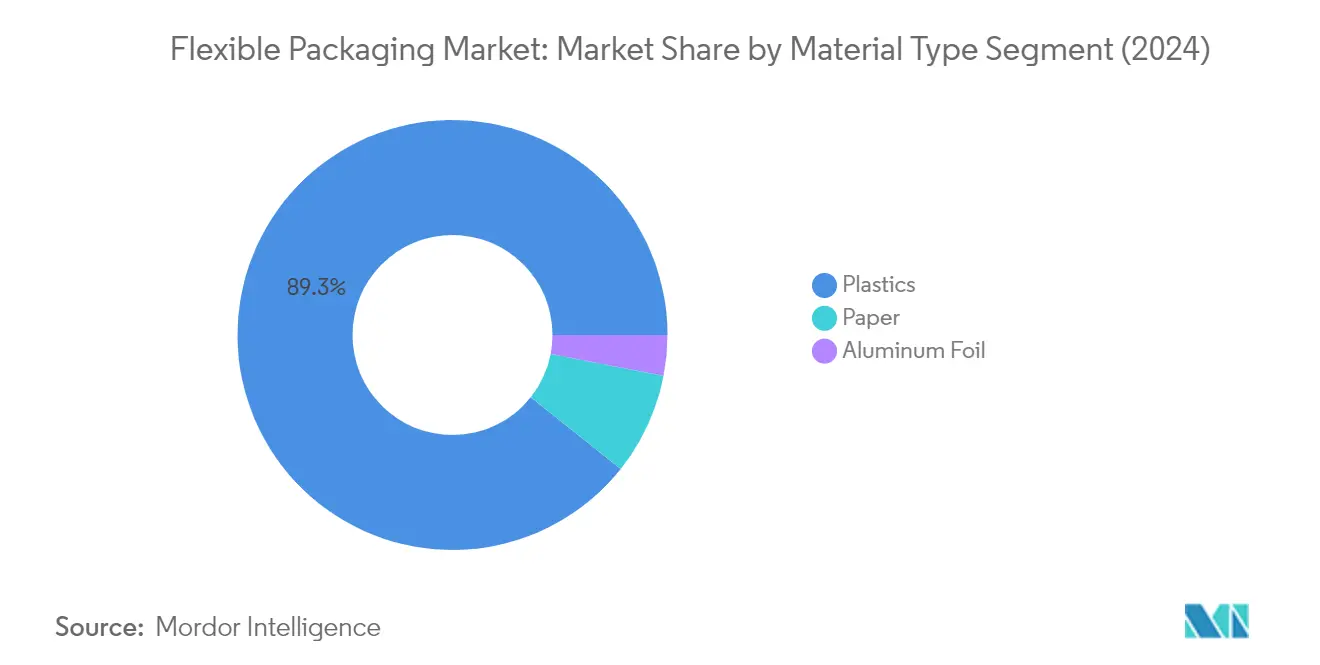

The plastics segment continues to dominate the flexible packaging market, commanding approximately 89% market share in 2024. This substantial market presence is attributed to plastics' versatile properties, including lightweight characteristics, durability, and superior barrier protection capabilities. The segment encompasses various materials such as polyethylene (PE), bi-oriented polypropylene (BOPP), cast polypropylene (CPP), polyvinyl chloride (PVC), and ethylene vinyl alcohol (EVOH). These materials find extensive applications across food packaging, pharmaceutical products, and consumer goods industries. The segment's dominance is further reinforced by technological advancements in packaging film manufacturing, enabling the production of high-performance packaging solutions that meet diverse industry requirements while maintaining cost-effectiveness.

Paper Segment in Flexible Packaging Market

The paper segment is emerging as the fastest-growing material type in the flexible packaging market, projected to grow at approximately 5% CAGR from 2024 to 2029. This accelerated growth is primarily driven by increasing environmental consciousness and stringent regulations against single-use plastics. Paper-based flexible packaging products are gaining significant traction due to their biodegradable and recyclable properties, aligning with sustainable packaging initiatives across various industries. The segment's growth is further supported by technological advancements in paper processing and coating techniques, enabling enhanced barrier properties and durability comparable to traditional packaging materials. Manufacturers are increasingly investing in research and development to improve paper-based packaging solutions, particularly focusing on moisture resistance and shelf-life extension capabilities.

Remaining Segments in Material Type

The aluminum foil segment plays a crucial role in the flexible packaging market, particularly in applications requiring superior barrier properties against moisture, light, and oxygen. This segment is especially vital in the pharmaceutical and food packaging industries, where product protection and extended shelf life are paramount. Aluminum foil's unique properties make it indispensable for certain applications, such as aseptic packaging and high-barrier pouches. The material's ability to provide complete barrier protection while maintaining product integrity has established its position as a premium packaging solution, particularly in sensitive product categories where protection against external factors is crucial.

Segment Analysis: By Product Type

Pouches Segment in Flexible Packaging Market

The flexible pouch segment dominates the flexible packaging market, commanding approximately 37% market share in 2024, while also emerging as the fastest-growing segment with a projected growth rate of around 4% during 2024-2029. The segment's prominence can be attributed to the growing food industry and private investments in developing flexible and fully compostable packaging. Flexible pouches offer significant advantages, including convenience, portability, and enhanced product protection, making them particularly popular in food, beverage, and consumer goods applications. The rise of e-commerce and changing consumer preferences towards convenient packaging solutions have further accelerated the adoption of pouches. Manufacturers are increasingly focusing on developing sustainable pouch solutions, with many companies introducing recyclable flexible packaging and mono-material options to align with environmental regulations and consumer demands. The segment's growth is also supported by technological advancements in pouch manufacturing, enabling features like resealable closures, spouts, and enhanced barrier properties.

Remaining Segments in Product Type

The films and wraps segment represents a substantial portion of the flexible packaging market, offering versatile solutions for various applications including food preservation, industrial packaging, and consumer goods. The segment's growth is driven by technological advancements in barrier properties and material innovations. The bags segment continues to maintain its significance in the market, particularly in applications such as retail, industrial, and agricultural packaging, with manufacturers focusing on developing sustainable and recyclable options. Other product types, including sachets, sleeves, and blister packs, cater to specific niche applications and contribute to the overall market diversity. These segments are witnessing continuous innovation in terms of material composition, design features, and sustainability aspects to meet evolving industry requirements and regulatory standards.

Segment Analysis: By End-User Industry

Food Segment in Flexible Packaging Market

The food segment maintains its dominant position in the flexible packaging market, commanding approximately 53% of the total market share in 2024. This substantial market share is driven by the increasing demand for convenient packaging solutions across various food categories, including frozen foods, dairy products, fruits and vegetables, meat, poultry, seafood, baked goods, and confectionery items. The segment's growth is particularly notable in the snack food and ready-to-eat meal categories, where flexible food packaging offers advantages such as extended shelf life, portion control, and easy storage. The rise in e-commerce food delivery and changing consumer preferences towards packaged food products has further strengthened the food segment's market position. Additionally, innovations in barrier properties and sustainable packaging solutions specifically designed for food applications have contributed to the segment's continued dominance in the flexible packaging market.

Pharmaceutical and Medical Segment in Flexible Packaging Market

The pharmaceutical and medical segment is emerging as the fastest-growing sector in the flexible packaging market, with a projected growth rate of approximately 6% during the forecast period 2024-2029. This remarkable growth is primarily driven by increasing healthcare expenditure, growing demand for unit-dose packaging, and stringent regulations regarding medical product safety and integrity. The segment's expansion is further supported by technological advancements in barrier properties and sterilization capabilities of flexible packaging materials. The rise in demand for convenient drug delivery systems and the growing preference for flexible packaging in medical device protection have created new opportunities for market growth. Additionally, the increasing focus on tamper-evident packaging and the need for extended shelf life in pharmaceutical products continue to drive innovation in this segment, making it the most dynamic sector in the flexible packaging market.

Remaining Segments in End-User Industry

The flexible packaging market's remaining segments, including beverage, household and personal care, and other end-user industries, each play significant roles in shaping the overall market landscape. The beverage segment continues to evolve with innovative pouch designs and sustainable packaging solutions for both alcoholic and non-alcoholic beverages. The household and personal care segment demonstrates strong potential, driven by the increasing demand for convenient, portable, and eco-friendly packaging solutions for products ranging from detergents to cosmetics. The other end-user industries segment, encompassing sectors such as tobacco, chemicals, and agriculture, contributes to market diversity through specialized packaging requirements and unique material specifications. These segments collectively drive innovation in flexible packaging materials, particularly in areas such as barrier properties, convenience features, and sustainable materials.

Flexible Packaging Market Geography Segment Analysis

Flexible Packaging Market in North America

The North American flexible packaging market demonstrates robust development across various end-user industries, particularly in the food and beverage, healthcare, and personal care sectors. The United States and Canada form the key markets in this region, with both countries showing significant advancements in sustainable packaging solutions and technological innovations. The region's growth is primarily driven by increasing consumer demand for convenient packaging solutions, rising e-commerce activities, and a growing emphasis on sustainable packaging alternatives.

Flexible Packaging Market in the United States

The United States dominates the North American flexible packaging market landscape, benefiting from its strong manufacturing base and technological advancements in packaging solutions. The country's market is characterized by significant investments in research and development, particularly in sustainable packaging solutions and innovative materials. The U.S. market holds approximately 90% share of the North American flexible packaging market in 2024, driven by robust demand from the food and beverage sector, pharmaceutical packaging requirements, and the growing e-commerce industry. The country's packaging industry employs over 79,000 people, reflecting its significant economic impact and scale of operations.

Flexible Packaging Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 5% during 2024-2029. The country's market is witnessing significant developments in sustainable packaging solutions, particularly in recyclable and biodegradable materials. Canadian manufacturers are increasingly focusing on eco-friendly packaging alternatives, driven by stringent environmental regulations and growing consumer awareness. The country's packaging industry is particularly strong in Ontario, which hosts the highest number of frozen food manufacturing establishments, followed by Quebec, British Columbia, and Alberta, contributing to the growing demand for flexible packaging solutions.

Flexible Packaging Market in Europe

Europe represents a mature market for flexible packaging, characterized by a strong emphasis on sustainability and technological innovation. The region encompasses diverse markets including Germany, the United Kingdom, France, Italy, Spain, Turkey, Poland, and Russia, each contributing uniquely to the overall market dynamics. European manufacturers are at the forefront of developing sustainable packaging solutions, driven by stringent EU regulations and increasing consumer awareness about environmental issues.

Flexible Packaging Market in Germany

Germany maintains its position as the largest flexible packaging market in Europe, commanding approximately 17% of the European market share in 2024. The country's market leadership is supported by its strong manufacturing base, technological advancement, and significant presence in the pharmaceutical packaging sector. Germany constitutes the major European pharmaceutical market and ranks as the fourth largest worldwide, driving substantial demand for flexible packaging solutions. The country's e-commerce penetration reaching around 80% further strengthens market growth.

Flexible Packaging Market in Italy

Italy emerges as Europe's fastest-growing flexible packaging market, with an expected growth rate of approximately 4% during 2024-2029. The country's market is witnessing significant developments in food packaging applications, particularly in the premium food segment. Italian companies are increasingly focusing on innovative packaging solutions that combine functionality with sustainability. The packaging industry has demonstrated remarkable resilience compared to other major industries, particularly excelling in food packaging and luxury goods segments.

Flexible Packaging Market in Asia-Pacific

The Asia-Pacific region represents a dynamic and rapidly evolving market for flexible packaging, encompassing major economies like China, Japan, India, and Australia. The region's growth is driven by rapid urbanization, changing consumer lifestyles, and increasing disposable income. The market is characterized by significant investments in manufacturing capabilities and technological advancements.

Flexible Packaging Market in China

China maintains its position as the largest flexible packaging market in Asia-Pacific, driven by its robust manufacturing sector and extensive end-user industry base. The country's market is characterized by significant investments in advanced manufacturing capabilities and a growing emphasis on sustainable packaging solutions. The pharmaceutical sector, in particular, has emerged as a key growth driver, with China securing the second position globally in pharmaceutical sales.

Flexible Packaging Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, driven by rapid urbanization, expanding retail infrastructure, and growing demand from various end-user industries. The country's flexible packaging industry is witnessing significant technological advancements and increasing investments in sustainable packaging solutions. The India flexible packaging market is particularly strong in food packaging, pharmaceutical packaging, and personal care products. The flexible packaging market size in India is expected to grow significantly, reflecting the dynamic nature of the flexible packaging industry in India.

Flexible Packaging Market in Latin America

The Latin American flexible packaging market encompasses key countries including Brazil, Argentina, and Mexico, each contributing to the region's diverse packaging landscape. The market is characterized by growing investments in manufacturing capabilities and increasing adoption of sustainable packaging solutions. Brazil emerges as the largest market in the region, while Mexico shows the fastest growth potential, driven by its strategic location and growing manufacturing base.

Flexible Packaging Market in Middle East & Africa

The Middle East & Africa region presents a growing market for flexible packaging, with key countries including the United Arab Emirates, Saudi Arabia, South Africa, Egypt, Iran, and Nigeria. The market is characterized by increasing investments in manufacturing capabilities and growing demand from various end-user industries. The United Arab Emirates leads the market in terms of growth rate, while Saudi Arabia maintains its position as the largest market in the region, driven by significant investments in food packaging and pharmaceutical sectors.

Get Analysis on Important Geographic Markets

Download PDF

Flexible Packaging Industry Overview

Top Companies in Flexible Packaging Market

The flexible packaging market features prominent flexible packaging companies like Amcor, Berry Global, Mondi, Sealed Air Corporation, and Huhtamaki, which are leading innovation and market development. These flexible packaging players are advancing through sustainable packaging solutions, including recyclable materials and bio-based alternatives, while simultaneously expanding their manufacturing capabilities across multiple regions. Strategic investments in research and development have enabled the introduction of high-performance films, barrier technologies, and smart packaging solutions that address evolving consumer needs. Companies are increasingly focusing on vertical integration and digital transformation to enhance operational efficiency and supply chain optimization. The industry witnesses continuous product innovation through proprietary technologies, particularly in areas such as modified atmosphere packaging, easy-open features, and extended shelf-life solutions, while maintaining a strong emphasis on reducing environmental impact through eco-friendly materials and processes.

Consolidation and Strategic Growth Drive Market

The flexible packaging market exhibits a moderately consolidated structure with global conglomerates maintaining significant flexible packaging market share through their extensive product portfolios and geographical presence. These major players leverage their technological capabilities, established distribution networks, and economies of scale to maintain competitive advantages, while regional specialists focus on niche markets and customized solutions. The industry landscape is characterized by a mix of multinational corporations with diverse packaging offerings and specialized firms focusing exclusively on flexible packaging solutions, creating a dynamic competitive environment that drives innovation and market development.

The market has witnessed substantial merger and acquisition activity as companies seek to expand their geographical footprint, enhance technological capabilities, and strengthen their market position. Major players are actively pursuing strategic acquisitions to enter new markets, acquire innovative technologies, and expand their product portfolios. These consolidation efforts are particularly focused on acquiring companies with complementary capabilities in sustainable flexible packaging solutions, advanced manufacturing technologies, or strong regional presence. The trend towards consolidation is expected to continue as companies seek to achieve operational synergies, expand their customer base, and enhance their competitive position in key markets.

Innovation and Sustainability Define Future Success

Success in the flexible packaging industry increasingly depends on companies' ability to develop sustainable solutions while maintaining cost competitiveness and performance standards. Market leaders are investing heavily in research and development to create innovative materials and designs that meet stringent environmental regulations while satisfying end-user requirements for functionality and convenience. Companies are also focusing on developing strategic partnerships across the value chain to ensure reliable raw material supply and enhance their recycling capabilities. The ability to offer comprehensive flexible packaging products, including design services, technical support, and customization options, has become crucial for maintaining market share and attracting new customers.

For emerging players and contenders, success lies in identifying and capitalizing on specific market niches while building strong relationships with key end-users. Companies must navigate increasing regulatory pressures regarding sustainability and recycling while managing the risk of substitution from alternative packaging solutions. The concentration of end-users in sectors such as food and beverage, healthcare, and personal care products necessitates a focused approach to customer relationship management and product development. Future success will depend on companies' ability to balance innovation with cost efficiency, while maintaining flexibility to adapt to changing market demands and regulatory requirements. The development of specialized capabilities in areas such as barrier properties, printing technologies, or specific application segments provides opportunities for differentiation and market penetration.

Flexible Packaging Industry Leaders

-

Amcor Group GmbH

-

Berry Global Inc.

-

Mondi PLC

-

Sealed Air Corporation

-

Huhtamaki Oyj

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Flexible Packaging Industry News

- February 2024: Amcor signed an agreement with Cadbury for the supply of 1,000 tons of post-consumer recycled plastic for the packaging of its core chocolate range, accelerating Cadbury's efforts to reduce its virgin plastic needs.

- February 2024: Mondi increased the production of its eco-friendly range of eco-friendly paper-based bags (EcoWicketBags). This helps align with the increasing demand for sustainable packaging within the HPC industry, especially for diapers and feminine hygiene products. Mondi is increasing the production of eco-friendly bags at its plant in Szada (Hungary) in order to take advantage of the group's integrated value chain, which includes in-house paper manufacturing, coating, and converting.

Flexible Packaging Industry Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of Substitutes

- 4.2.4 Threat of New Entrants

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increased Demand for Convenient Packaging

- 5.1.2 Demand for Longer Shelf Life and Changing Lifestyles

-

5.2 Market Challenges

- 5.2.1 Concerns Regarding the Environment and Recycling

6. MARKET SEGMENTATION

-

6.1 By Material Type

- 6.1.1 Plastic

- 6.1.1.1 Polyethene (PE)

- 6.1.1.2 Bi-orientated Polypropylene (BOPP)

- 6.1.1.3 Cast polypropylene (CPP)

- 6.1.1.4 Polyvinyl Chloride (PVC)

- 6.1.1.5 Ethylene Vinyl Alcohol (EVOH)

- 6.1.1.6 Other Plastic Types (PA, Bioplastics)

- 6.1.2 Paper

- 6.1.3 Aluminum Foil

-

6.2 By Product Type

- 6.2.1 Pouches

- 6.2.2 Bags

- 6.2.3 Films & Wraps

- 6.2.4 Other Product Types (Sachets, Sleeves, Blister Packs, Liners, Laminates, etc.)

-

6.3 By End-user Industry

- 6.3.1 Food

- 6.3.1.1 Frozen and Chilled Food

- 6.3.1.2 Dairy Products

- 6.3.1.3 Fruits and Vegetables

- 6.3.1.4 Meat, Poultry, and Seafood

- 6.3.1.5 Baked Goods and Snack Foods

- 6.3.1.6 Candy and Confections

- 6.3.1.7 Other Food Products

- 6.3.2 Beverage

- 6.3.3 Pharmaceutical and Medical

- 6.3.4 Household and Personal Care

- 6.3.5 Other End-user Industries (Tobacco, Chemical, and Agriculture, Among Others)

-

6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Italy

- 6.4.2.5 Spain

- 6.4.2.6 Turkey

- 6.4.2.7 Poland

- 6.4.2.8 Russia

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Australia

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Mexico

- 6.4.5 Middle East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.5.4 Egypt

- 6.4.5.5 Iran

- 6.4.5.6 Nigeria

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 Amcor Group Gmbh

- 7.1.2 Berry Global Inc.

- 7.1.3 Mondi PLC

- 7.1.4 Sealed Air Corporation

- 7.1.5 Huhtamaki Oyj

- 7.1.6 Uflex Limited

- 7.1.7 Coveris Management Gmbh

- 7.1.8 ProAmpac LLC

- 7.1.9 Wipf AG

- 7.1.10 Flexpak Services Llc

- 7.1.11 Sigma Plastics Group Inc.

- 7.1.12 KM Packaging Services Ltd

- 7.1.13 Sonoco Products Company

- 7.1.14 Arabian Flexible Packaging LLC

- 7.1.15 Gulf East Paper and Plastic Industries LLC

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Flexible Packaging Industry Industry Segmentation

The study covers the flexible packaging market tracked in terms of consumption and is only limited to flexible packaging products made from plastic, paper, and aluminum foil. The market is tracked in terms of volume in million tons. This report analyzes the factors that impact geopolitical developments in the market based on the prevalent base scenarios, key themes, and end-user industries-related demand cycles. The estimates exclude the weight of the content that is or is to be packed inside the flexible packaging solution.

The flexible packaging market is segmented by material type (plastic [polyethylene (PE), bi-orientated polypropylene (BOPP), cast polypropylene (CPP), polyvinyl chloride (PVC), ethylene vinyl alcohol (EVOH)], paper, aluminum foil), product type (pouches, bags, films & wraps), end-user industry (food [frozen food, dairy products, fruits & vegetables, meat, poultry, & seafood, baked goods and snack foods, and candy & confections], beverage, pharmaceutical & medical, and household & personal care), and geography (North America [United States, Canada], Europe [United Kingdom, Germany, France, Italy, Spain, Turkey, Poland, Russia, Rest of Europe], Asia-Pacific [China, Japan, India Australia, Rest of Asia Pacific], Latin America [Brazil, Argentina, Mexico, Rest of Latin America], and the Middle East and Africa [United Arab Emirates, Saudi Arabia, South Africa, Egypt, Iran, Nigeria, and Rest of Middle East and Africa]). The market sizes and forecasts are provided in terms of value USD for all the above segments.

| By Material Type | Plastic | Polyethene (PE) | |

| Bi-orientated Polypropylene (BOPP) | |||

| Cast polypropylene (CPP) | |||

| Polyvinyl Chloride (PVC) | |||

| Ethylene Vinyl Alcohol (EVOH) | |||

| Other Plastic Types (PA, Bioplastics) | |||

| Paper | |||

| Aluminum Foil | |||

| By Product Type | Pouches | ||

| Bags | |||

| Films & Wraps | |||

| Other Product Types (Sachets, Sleeves, Blister Packs, Liners, Laminates, etc.) | |||

| By End-user Industry | Food | Frozen and Chilled Food | |

| Dairy Products | |||

| Fruits and Vegetables | |||

| Meat, Poultry, and Seafood | |||

| Baked Goods and Snack Foods | |||

| Candy and Confections | |||

| Other Food Products | |||

| Beverage | |||

| Pharmaceutical and Medical | |||

| Household and Personal Care | |||

| Other End-user Industries (Tobacco, Chemical, and Agriculture, Among Others) | |||

| By Geography | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Turkey | |||

| Poland | |||

| Russia | |||

| Asia | China | ||

| Japan | |||

| India | |||

| Australia | |||

| Latin America | Brazil | ||

| Argentina | |||

| Mexico | |||

| Middle East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| South Africa | |||

| Egypt | |||

| Iran | |||

| Nigeria | |||

Need A Different Region or Segment?

Customize Now

Flexible Packaging Industry Research FAQs

How big is the Flexible Packaging Market?

The Flexible Packaging Market size is expected to reach 35.84 million tonnes in 2025 and grow at a CAGR of 3.38% to reach 42.32 million tonnes by 2030.

What is the current Flexible Packaging Market size?

In 2025, the Flexible Packaging Market size is expected to reach 35.84 million tonnes.

Who are the key players in Flexible Packaging Market?

Amcor Group GmbH, Berry Global Inc., Mondi PLC, Sealed Air Corporation and Huhtamaki Oyj are the major companies operating in the Flexible Packaging Market.

Which is the fastest growing region in Flexible Packaging Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Flexible Packaging Market?

In 2025, the Asia Pacific accounts for the largest market share in Flexible Packaging Market.

What years does this Flexible Packaging Market cover, and what was the market size in 2024?

In 2024, the Flexible Packaging Market size was estimated at 34.63 million tonnes. The report covers the Flexible Packaging Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Flexible Packaging Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Flexible Packaging Industry Research

Mordor Intelligence provides comprehensive market research and analysis of the flexible packaging market, offering detailed insights into market size, growth trends, and competitive dynamics. Our industry reports cover various segments including flexible plastic packaging, stretch film, packaging film, and flexible food packaging markets, with in-depth analysis of key players and emerging opportunities. The report includes detailed market statistics, industry outlook, and future growth projections, all available in an easy-to-read report PDF format that helps stakeholders make informed decisions.

Our consulting expertise extends beyond traditional market research to provide actionable insights for the flexible packaging industry. We assist companies in understanding regulatory compliance requirements, conducting technology scouting for sustainable packaging solutions, and analyzing raw material pricing intelligence crucial for flexible packaging companies. Our team specializes in supply chain analysis, helping businesses optimize their operations and identify potential bottlenecks. We also provide comprehensive competitor assessment, customer need analysis, and support in product positioning strategies, particularly valuable for companies developing recyclable flexible packaging solutions. Through extensive B2B surveys and market research, we help clients understand trends in flexible packaging and capitalize on emerging opportunities in this dynamic market.