| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 14.51 Billion |

| Market Size (2030) | USD 17.51 Billion |

| CAGR (2025 - 2030) | 3.84 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Flexible Insulation Market Analysis

The Flexible Insulation Market size is estimated at USD 14.51 billion in 2025, and is expected to reach USD 17.51 billion by 2030, at a CAGR of 3.84% during the forecast period (2025-2030).

The flexible insulation industry is experiencing significant transformation driven by rapid urbanization and infrastructure development across major economies. The construction sector has shown remarkable resilience and growth, particularly in emerging markets, with Chile's construction GDP reaching CLP 3,038.64 billion in the third quarter of 2023. Sustainable building practices and green construction initiatives are gaining prominence globally, with developers increasingly focusing on energy-efficient building materials. The industry is witnessing a shift towards advanced insulation solutions that offer superior thermal and acoustic properties while maintaining flexibility and ease of installation.

The automotive and transportation sectors have emerged as significant consumers of flexible insulation materials, driven by the growing emphasis on vehicle efficiency and comfort. Argentina's automotive sector demonstrated strong growth with production reaching 610,715 units in 2023, marking a 13.7% increase from the previous year. The rise in electric vehicle manufacturing has created new opportunities for specialized insulation solutions, particularly in battery thermal management and noise reduction applications. Manufacturers are developing innovative insulation materials that meet the specific requirements of modern vehicle design while contributing to overall energy efficiency.

The commercial construction segment has shown robust activity, particularly in the hospitality sector. As of January 2023, Dubai alone had 85 hotel projects under construction, adding 23,549 hotel rooms to its capacity, indicating strong demand for flexible thermal insulation in commercial applications. Industrial applications continue to expand, with increasing requirements for pipe insulation, HVAC systems, and process equipment across manufacturing facilities. The focus on energy conservation and operational efficiency in industrial processes has led to greater adoption of advanced insulation solutions.

Technological advancements in insulation materials have significantly influenced market dynamics, with manufacturers investing in research and development to improve product performance. The consumer electronics sector has been a key driver of innovation, with the U.S. market alone generating USD 505 billion in retail revenue from consumer electronics sales in 2022. New developments in aerogel technology and composite materials have enabled the creation of thinner, lighter, and more effective insulation solutions. The industry is witnessing increased integration of smart materials and sustainable components in insulation products, responding to growing environmental concerns and regulatory requirements. The development of flexible acoustic insulation and flexible elastomeric insulation is also contributing to the diversification of the flexible insulation market.

Flexible Insulation Market Trends

Increasing Demand for Energy Efficiency from the Construction Industry

The construction industry's growing focus on energy efficiency and sustainable building practices is driving significant demand for flexible insulation materials. Flexible fiberglass insulation, composed of extremely fine glass fibers bonded with high-temperature binders, creates millions of tiny air pockets that provide excellent thermal and acoustic insulation properties. The material's eco-friendly manufacturing process, using renewable raw materials including sand, limestone, soda ash, and recycled glass cullet, aligns with the industry's sustainability goals. Construction activities are witnessing substantial growth, particularly in developed regions, with the United States recording a construction value of USD 1,978.7 billion in 2023, representing a 7.03% increase compared to 2022.

The implementation of stringent building energy codes and regulations worldwide is further propelling the adoption of flexible insulation solutions. For instance, in the United Kingdom, the government revised its energy efficiency standards in April 2023, prohibiting the underlease of non-domestic properties with an Energy Performance Certificate (EPC) rating below E in England and Wales. Similarly, Germany's Federal Ministry for Economic Affairs and Climate Action launched the 'Energy-efficient Refurbishment' program, providing 40% of the costs for new building or energy-efficient refurbishment of existing buildings. The construction sector is experiencing significant growth in sustainable projects, exemplified by Spain's government initiative to renovate more than 500,000 homes by 2026, with an allocation of EUR 6.8 billion from the EU's Next Generation Fund for building renovations.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Application of Flexible Piping Insulation

The expanding industrial sector is witnessing a surge in demand for flexible pipe insulation across various applications, particularly in oil and gas, chemical processing, and cryogenic systems. Flexible pipe insulation materials play a crucial role in maintaining operational efficiency, ensuring safety, and protecting assets in these industries. For instance, in March 2023, Argentina announced plans to resume oil exports to Chile along the Trasandino Argentina SA (OTASA) oil pipeline, with rehabilitation work expected to enable shipments of approximately 40,000 barrels per day. Additionally, in June 2023, the Italian and German governments agreed to proceed with the development of a planned gas pipeline that will facilitate both gas and hydrogen transportation between the two countries, spanning approximately 3,300 kilometers.

The growing investments in industrial infrastructure and expansion projects are further driving the demand for flexible pipe insulation. Baker Hughes opened a new chemicals manufacturing facility in Jurong Island, Singapore, in Q2 2022 to better serve oil and gas operators, LNG plants, refineries, petrochemical plants, and industrial sites in Asia-Pacific, Africa, and the Middle East. The versatility of flexible duct insulation materials is demonstrated in their application range, from high-temperature industrial processes to cryogenic applications. Fibrous glass insulation, which can be applied to the exterior of sheet metal ducts, housings, and plenums, offers effective insulation within a temperature range of -18°C to 232°C, making it suitable for various industrial applications including industrial ovens, heat exchangers, dryers, boilers, and pipe work.

Segment Analysis: Material

Fiberglass Segment in Flexible Insulation Market

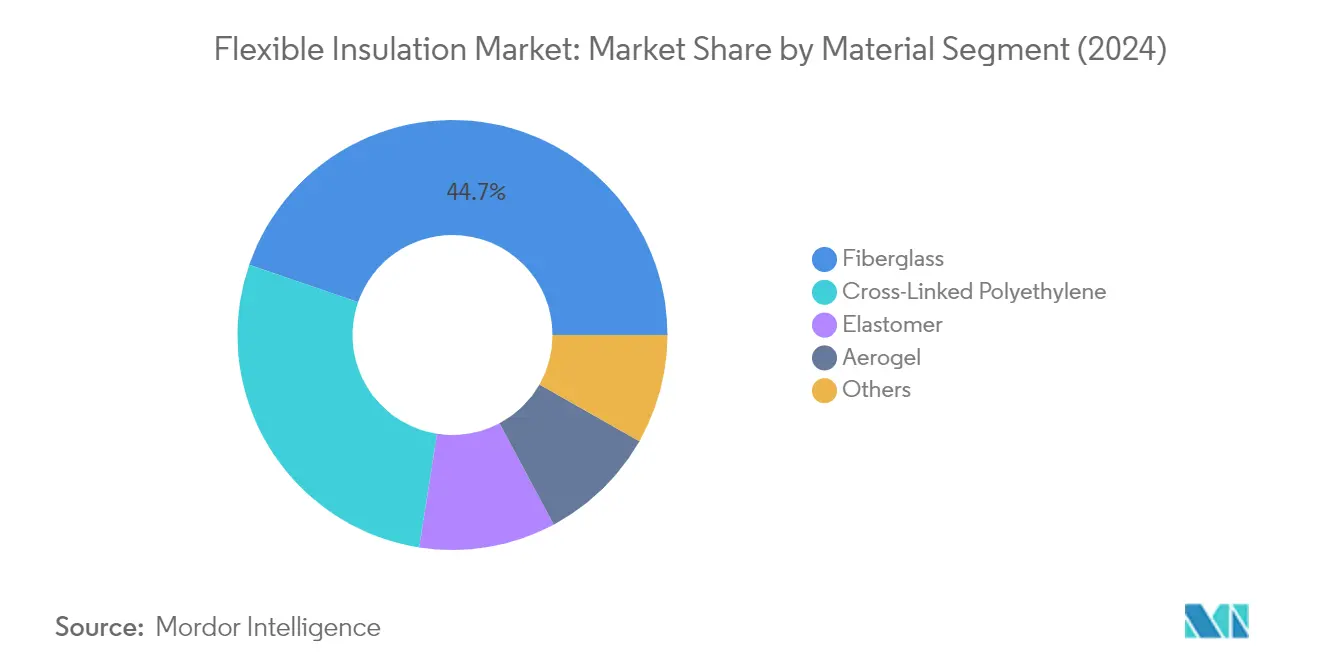

The flexible fiberglass insulation segment dominates the flexible insulation market, accounting for approximately 45% of the total market share in 2024. Fiberglass insulation consists of fine glass fibers bonded together to form a flexible mat or blanket, widely used for thermal insulation in residential and commercial buildings, HVAC ducts, pipes, and appliances. The material's popularity stems from its excellent thermal and acoustic properties, with the ability to trap millions of tiny air pockets that create superior insulation performance. Fiberglass is particularly valued for its non-corrosive nature, resistance to mold growth, and eco-friendly characteristics as it's manufactured from renewable raw materials. The material's versatility is demonstrated through its various forms, including blankets, loose-fill, rigid boards, and duct insulation, making it suitable for diverse applications across different sectors.

Aerogel Segment in Flexible Insulation Market

The aerogel segment is projected to experience the fastest growth in the flexible insulation market, with an expected CAGR of approximately 4% during the forecast period 2024-2029. Aerogel insulation, known as the world's lightest solid material, is gaining significant traction due to its exceptional thermal performance and unique properties. The material's advanced characteristics, including its ultra-low conductivity, high porosity, and superior performance in both cryogenic and high-temperature applications, are driving its increased adoption. The growing demand for aerogel insulation is particularly evident in specialized applications such as oil and gas pipelines, aerospace components, and industrial facilities where space constraints and thermal efficiency are critical factors. The material's ability to provide up to five times better thermal performance compared to competing insulation materials positions it as a premium solution for high-end applications.

Remaining Segments in Material Segmentation

The flexible insulation market's remaining segments include flexible elastomeric insulation, cross-linked polyethylene, and other materials, each serving specific applications and requirements. Cross-linked polyethylene offers excellent electrical insulation properties and is particularly valued in medium to high-voltage applications. Elastomer insulation materials provide superior flexibility and vibration dampening characteristics, making them ideal for HVAC systems and industrial applications. The 'Others' category encompasses various materials such as flexible ceramic fibers, flexible polyurethane foam, and vacuum insulated panels, each contributing to the market's diversity by addressing specific thermal, acoustic, and electrical insulation needs across different industries.

Segment Analysis: Insulation Type

Acoustic Insulation Segment in Flexible Insulation Market

The flexible acoustic insulation segment has emerged as both the largest and fastest-growing segment in the flexible insulation market, commanding approximately 52% of the total market share in 2024. This dominant position is attributed to its extensive application in residential construction for reducing noise transmission between adjoining rooms and preventing the transfer of airborne sounds like traffic noise and aircraft noise. The segment's growth is further bolstered by its widespread use in commercial buildings, where acoustic insulation materials find extensive application in walls, floors, ceilings, wastewater pipes, and plant rooms. In the transportation sector, acoustic insulation is extensively utilized in automobiles, aircraft, military vehicles, and marine ships, offering both noise absorption and thermal insulation benefits in automotive engines and drivers' compartments. The segment is projected to maintain its leading position with the highest growth rate of around 4% during 2024-2029, driven by increasing urbanization and stringent noise pollution regulations across various industries.

Remaining Segments in Insulation Type

The flexible electrical insulation and flexible thermal insulation segments complete the market landscape, each serving distinct but crucial applications across various industries. Electrical insulation plays a vital role in covering cables and wires, protecting conductors from contact with each other and the surrounding environment, while offering excellent resistance to moisture and repeated impact. This segment is particularly important in applications where heat needs to be kept in or out, such as in freezers and refrigerators. The thermal insulation segment, while smaller in market share, remains essential for maintaining preferred environments and preventing heat loss from systems, offering significant benefits in energy cost reduction and increased energy efficiency. Both segments contribute significantly to the overall market growth through their applications in residential, commercial, and industrial sectors, particularly in regions with stringent energy efficiency regulations.

Flexible Insulation Market Geography Segment Analysis

Flexible Insulation Market in Asia-Pacific

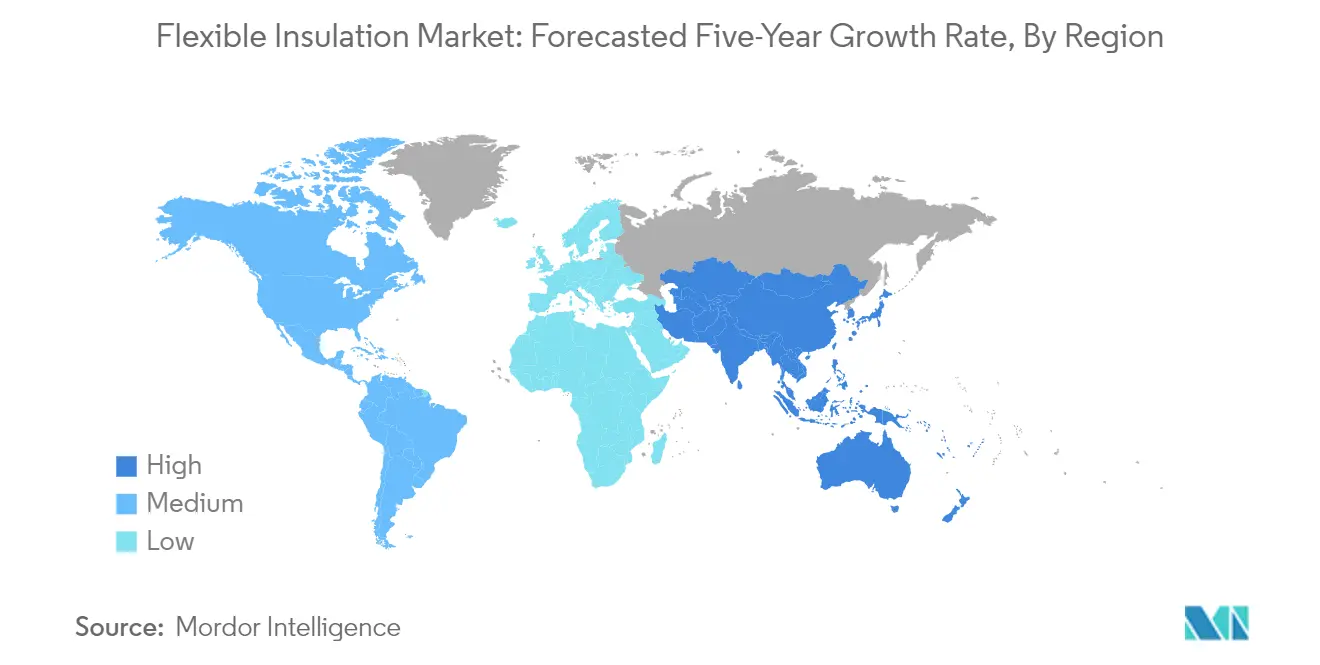

The Asia-Pacific flexible insulation market demonstrates robust growth driven by rapid industrialization and increasing construction activities across major economies. China leads the regional market with its extensive manufacturing base and construction sector growth, followed by significant contributions from India, Japan, and South Korea. The region's market is characterized by strong government initiatives promoting energy efficiency in buildings and industrial applications, particularly in emerging economies like India and China. Technological advancements in flexible insulation materials and growing awareness about energy conservation continue to shape market dynamics across the region.

Flexible Insulation Market in China

China dominates the Asia-Pacific flexible insulation market, holding approximately 42% of the regional market share in 2024. The country's market is primarily driven by extensive infrastructure development and stringent energy efficiency regulations. The government's focus on sustainable construction and green building initiatives has created substantial demand for flexible insulation materials. Major ongoing infrastructure projects, including metro lines and commercial developments, continue to boost market growth. The country's commitment to reducing energy consumption in buildings through improved insulation systems has led to increased adoption across both new construction and renovation projects.

Flexible Insulation Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 6% from 2024 to 2029. The country's rapid urbanization and expanding industrial sector are key drivers for market growth. The government's push towards energy-efficient building solutions and sustainable construction practices has created significant opportunities for flexible thermal insulation materials. The implementation of energy conservation building codes and growing awareness about thermal efficiency in industrial applications have further accelerated market expansion. India's focus on developing smart cities and modern infrastructure continues to drive demand for advanced insulation solutions.

Flexible Insulation Market in North America

The North American flexible insulation market showcases strong growth driven by technological advancements and an increasing focus on energy efficiency across industrial and commercial sectors. The region benefits from well-established construction standards and stringent energy regulations that mandate the use of high-quality flexible insulating material. The United States, Canada, and Mexico each contribute significantly to the regional market, with varying degrees of industrial development and construction activity influencing demand patterns.

Flexible Insulation Market in United States

The United States maintains its position as both the largest and fastest-growing market in North America, commanding approximately 59% of the regional market share in 2024, while demonstrating a projected growth rate of about 4% from 2024 to 2029. The country's market benefits from robust construction activity and stringent energy efficiency regulations. Significant investments in commercial and residential construction, coupled with growing awareness about energy conservation, continue to drive market growth. The implementation of advanced building codes and an increasing focus on sustainable construction practices further strengthen market development.

Flexible Insulation Market in Europe

The European flexible insulation market demonstrates steady growth driven by stringent energy efficiency regulations and an increasing focus on sustainable building solutions. Germany, the United Kingdom, France, and Italy represent key markets within the region, each contributing significantly to market development. The region's commitment to reducing carbon emissions and improving building energy performance continues to drive innovation in insulation technologies.

Flexible Insulation Market in Germany

Germany maintains its position as the largest market for flexible insulation in Europe, driven by its robust industrial sector and strong emphasis on energy-efficient building solutions. The country's comprehensive approach to energy conservation in construction and industrial applications has created sustained demand for flexible electrical insulation materials. The government's commitment to achieving climate-neutral building stock has spurred investments in advanced insulation solutions.

Flexible Insulation Market in United Kingdom

The United Kingdom emerges as the fastest-growing market in Europe, driven by increasing renovation activities and stringent building energy performance requirements. The country's focus on reducing carbon emissions through improved building efficiency has created significant opportunities for flexible insulation materials. Growing awareness about energy conservation and government initiatives supporting sustainable construction continue to drive market expansion.

Flexible Insulation Market in South America

The South American flexible insulation market shows steady development, influenced by growing industrial activities and increasing awareness about energy efficiency. Brazil emerges as both the largest and fastest-growing market in the region, followed by Argentina. The region's market growth is primarily driven by expanding construction activities and industrial development, particularly in Brazil's manufacturing and commercial sectors.

Flexible Insulation Market in Middle-East and Africa

The Middle-East and Africa flexible insulation market demonstrates significant potential, driven by rapid infrastructure development and increasing industrial activities. Saudi Arabia leads the regional market as the largest country, while also showing the fastest growth rate. The region's market is characterized by extensive construction activities in commercial and industrial sectors, particularly in Saudi Arabia and South Africa, coupled with growing awareness about energy efficiency in building systems.

Get Analysis on Important Geographic Markets

Download PDF

Flexible Insulation Industry Overview

Top Companies in Flexible Insulation Market

The global flexible insulation market features prominent players like Knauf Group, Owens Corning, Armacell, Saint-Gobain, and Johns Manville leading the industry through differentiated strategies. These companies are increasingly focusing on developing sustainable and energy-efficient products while expanding their manufacturing footprint across strategic locations worldwide. Product innovation remains central to competitive advantage, with companies investing heavily in R&D to develop advanced flexible insulating material solutions that meet evolving environmental regulations and energy efficiency standards. Operational excellence is being pursued through the digitalization of manufacturing processes and supply chain optimization, while strategic partnerships with distributors and contractors strengthen market presence. Geographic expansion, particularly in emerging markets, coupled with customized product offerings for specific regions, demonstrates the industry's commitment to market penetration and growth.

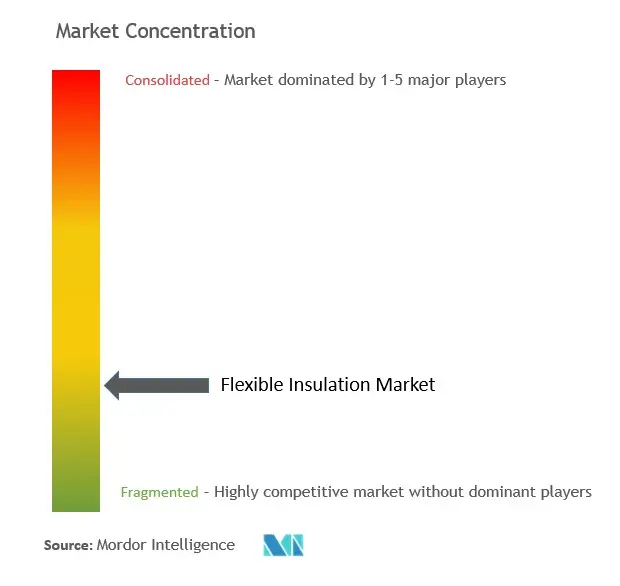

Fragmented Market with Strong Regional Players

The flexible insulation market exhibits a fragmented structure where global conglomerates operate alongside specialized regional manufacturers, creating a diverse competitive landscape. Major players leverage their extensive distribution networks, broad product portfolios, and strong brand recognition to maintain market positions, while regional players compete through local market expertise and customized solutions. The industry witnesses a mix of vertically integrated companies controlling raw material supply chains and specialized manufacturers focusing on specific market segments or applications.

Market consolidation activities are primarily driven by larger players seeking to expand their geographic presence and technological capabilities through strategic acquisitions. Companies are increasingly focusing on acquiring businesses that complement their existing product portfolios or provide access to new markets and customer segments. The competitive dynamics are further shaped by the presence of diversified building materials companies that view flexible insulation as a strategic growth segment within their broader portfolio.

Innovation and Sustainability Drive Future Success

Success in the flexible insulation market increasingly depends on companies' ability to develop innovative, sustainable products while maintaining cost competitiveness. Incumbent players must focus on expanding their eco-friendly product lines, investing in advanced manufacturing technologies, and strengthening their distribution networks to maintain market leadership. Building strong relationships with key stakeholders across the value chain, from raw material suppliers to end-users, becomes crucial for maintaining competitive advantage. Companies need to demonstrate clear value propositions through superior product performance, technical support, and after-sales service.

For contenders looking to gain market share, specialization in specific applications or regional markets offers a viable strategy for growth. The ability to respond quickly to changing customer needs and regulatory requirements while maintaining operational efficiency will be crucial. Companies must also consider the growing influence of sustainability regulations and energy efficiency standards in shaping market dynamics. The threat of substitution from alternative insulation technologies necessitates continuous innovation and clear differentiation strategies, while increasing end-user awareness about energy efficiency creates opportunities for companies with strong sustainability credentials.

Flexible Insulation Market Leaders

-

Saint-Gobain

-

Johns Manville

-

Owens Corning

-

Knauf Group

-

Armacell

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Flexible Insulation Market News

- The recent developments pertaining to the major players in the market are covered in the complete study.

Flexible Insulation Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Market Drivers

- 4.1.1 Increasing Demand for Energy Efficiency from the Construction Industry

- 4.1.2 Increasing Application of Flexible Piping Insulation

- 4.1.3 Other Drivers

-

4.2 Market Restraints

- 4.2.1 Availability of Alternatives

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Value)

-

5.1 By Material

- 5.1.1 Aerogel

- 5.1.2 Cross-Linked Polyethylene

- 5.1.3 Elastomer

- 5.1.4 Fiberglass

- 5.1.5 Other Materials

-

5.2 By Insulation Type

- 5.2.1 Acoustic Insulation

- 5.2.2 Electrical Insulation

- 5.2.3 Thermal Insulation

-

5.3 By Geography

- 5.3.1 Asia - Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Market Ranking Analysis

- 6.2 Strategies Adopted by Leading Players

-

6.3 Company Profiles

- 6.3.1 Altana AG

- 6.3.2 Armacell

- 6.3.3 Cabot Corporation

- 6.3.4 Etex Group

- 6.3.5 Fletcher Insulation

- 6.3.6 Johns Manville

- 6.3.7 Kingspan Group

- 6.3.8 Knauf Insulation

- 6.3.9 Owens Corning

- 6.3.10 Saint-Gobain

- 6.3.11 Superlon Holdings Berhad

- 6.3.12 Thermaxx Jackets

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Opportunity for Aerogel Insulation in Electric Vehicles

- 7.2 Other Opportunities

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Flexible Insulation Industry Segmentation

Flexible insulation is a type of insulation composed of materials such as fiberglass, aerogel, XLPE, and elastomers that offer insulation against noise, high temperatures, etc.

The flexible insulation market is segmented by material, insulation type, and geography. By material, the market is segmented into aerogel, cross-linked polyethylene, elastomer, fiberglass, and others. By insulation type, the market is segmented into acoustic insulation, electrical insulation, and thermal insulation. The report also covers the market size and forecasts for flexible insulation in 15 countries across major regions. For each segment, the market sizing and forecasts are done on the basis of revenue (USD).

| By Material | Aerogel | ||

| Cross-Linked Polyethylene | |||

| Elastomer | |||

| Fiberglass | |||

| Other Materials | |||

| By Insulation Type | Acoustic Insulation | ||

| Electrical Insulation | |||

| Thermal Insulation | |||

| By Geography | Asia - Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Flexible Insulation Market Research FAQs

How big is the Flexible Insulation Market?

The Flexible Insulation Market size is expected to reach USD 14.51 billion in 2025 and grow at a CAGR of 3.84% to reach USD 17.51 billion by 2030.

What is the current Flexible Insulation Market size?

In 2025, the Flexible Insulation Market size is expected to reach USD 14.51 billion.

Who are the key players in Flexible Insulation Market?

Saint-Gobain, Johns Manville, Owens Corning, Knauf Group and Armacell are the major companies operating in the Flexible Insulation Market.

Which is the fastest growing region in Flexible Insulation Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Flexible Insulation Market?

In 2025, the Europe accounts for the largest market share in Flexible Insulation Market.

What years does this Flexible Insulation Market cover, and what was the market size in 2024?

In 2024, the Flexible Insulation Market size was estimated at USD 13.95 billion. The report covers the Flexible Insulation Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Flexible Insulation Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Flexible Insulation Market Research

Mordor Intelligence provides a comprehensive analysis of the flexible insulation industry, drawing on our extensive experience in industrial materials research. Our latest report explores the full range of flexible insulating material applications. This includes flexible duct insulation and flexible pipe insulation, as well as specialized solutions like flexible foam insulation and flexible elastomeric insulation. The analysis of the pliable insulation market covers both traditional and emerging applications. We focus particularly on bendable insulation technologies that are transforming industrial and commercial applications.

The report, available as an easy-to-download PDF, offers stakeholders detailed insights into the flexible thermal insulation, flexible acoustic insulation, and flexible electrical insulation segments. Our analysis highlights emerging trends in flexible fiberglass insulation and other innovative materials, providing valuable insights for industry participants. The comprehensive coverage of the flexible insulation market includes a detailed regional analysis, an evaluation of the competitive landscape, and future growth projections. This makes it an essential tool for decision-makers in the insulation industry.