| Study Period | 2019 - 2030 |

| Market Volume (2025) | 83.17 Million tons |

| Market Volume (2030) | 101.34 Million tons |

| CAGR | 4.03 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Flat Glass Market Analysis

The Flat Glass Market size is estimated at 83.17 million tons in 2025, and is expected to reach 101.34 million tons by 2030, at a CAGR of 4.03% during the forecast period (2025-2030).

The flat glass industry has witnessed significant transformation in manufacturing capabilities and technological integration across global production facilities. According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), global vehicle production reached 93.54 million units in 2023, marking a 10.26% increase from 2022, which has substantially influenced automotive glass manufacturing patterns. This surge in production has prompted manufacturers to enhance their operational efficiency through advanced automation and smart manufacturing processes. Companies are increasingly adopting Industry 4.0 technologies, including AI-driven quality control systems and automated handling equipment, to optimize production workflows and reduce waste.

Technological advancements in flat glass manufacturing have focused heavily on energy efficiency and product innovation. Manufacturers are developing sophisticated coating technologies that enhance the glass's thermal insulation properties while maintaining optimal light transmission. The industry has seen remarkable progress in developing smart glass solutions that can dynamically adjust their properties based on environmental conditions. These innovations extend beyond traditional applications, with manufacturers introducing new products specifically designed for emerging applications in solar energy and electric vehicles.

Sustainability has emerged as a central theme in the flat glass industry, with manufacturers implementing comprehensive environmental initiatives. In March 2024, Guardian Glass's Bascharage plant commenced operations with a new furnace that enhances energy efficiency by approximately 25% while reducing emissions. Companies are increasingly investing in recycling infrastructure and developing processes to incorporate higher percentages of cullet in production, significantly reducing energy consumption and carbon emissions. The industry is also witnessing a growing emphasis on water conservation and waste reduction throughout the manufacturing process.

Regional trade dynamics and production capabilities have undergone substantial shifts, particularly in Asia-Pacific markets. China's automotive sector has demonstrated remarkable growth, with car output exceeding 30.16 million units in 2023, representing an 11.6% year-over-year increase. This regional growth has prompted significant investments in production capacity and technological capabilities. Manufacturers are strategically positioning their facilities to optimize supply chain efficiency and reduce transportation costs, while also investing in research and development centers to enhance their competitive advantage in high-value product segments.

Flat Glass Market Trends

Growing Investments in the Construction Sector

The construction sector is witnessing unprecedented levels of investment globally, driven by rapid urbanization and infrastructure modernization initiatives. According to the Institution of Civil Engineers, the volume of construction output is projected to surge by 85%, reaching a remarkable revenue of USD 15.5 trillion worldwide in the upcoming decade. This growth is being fueled by massive infrastructure projects, particularly in the Middle East, where developments like the Jeddah Central megaproject, valued at USD 20 billion, are transforming the urban landscape. The project, initiated in August 2022, encompasses the construction of four landmark structures—a museum, an opera house, a sports stadium, and a coral farm—along with over 17,000 residential units and more than 3,000 hospitality establishments. These developments significantly impact the building glass and construction glass markets, as the demand for high-quality architectural glass continues to rise.

The trend of increasing construction investments is further evidenced by significant government initiatives worldwide. In India, the government has allocated INR 10 lakh crore (USD 130.57 billion) to enhance the infrastructure sector, as announced in the Union Budget 2022-23. Similarly, Saudi Arabia's Ministry of Municipal and Rural Affairs and Housing is spearheading ambitious housing projects worth over SAR 65 billion (USD 17.3 billion), announced in September 2023. These investments are complemented by private sector developments, such as the USD 48 million expansion of Morumbi Shopping Mall in Sao Paulo, Brazil, announced in December 2023, which will add 13,141 square meters to the existing structure, further boosting the commercial glass market.

Increasing Demand from the Automotive Sector

The automotive industry's robust growth and transition towards electric vehicles are creating substantial demand for flat glass products. According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), global vehicle production reached approximately 93.54 million units in 2023, marking a significant 10.26% increase from 2022's production of about 84.83 million units. This growth is accompanied by major investments in the sector, exemplified by Stellantis's announcement in March 2024 to invest BRL 30 billion (approximately USD 5.98 billion) between 2025 and 2030 in South America, marking the largest investment ever recorded in the Brazilian and broader South American automotive landscape. The increasing use of automotive glass market products is evident as manufacturers seek advanced safety glass solutions to meet evolving industry standards.

The industry is witnessing a significant shift towards electric vehicle production, driving innovations in automotive glass applications. In October 2023, the Public Investment Fund (PIF) and Hyundai Motor Company formed a joint venture to establish a cutting-edge vehicle manufacturing plant in Saudi Arabia, with plans to produce 50,000 vehicles annually, including both internal combustion engines and electric vehicles. Similarly, Germany, currently the second-largest electric vehicle manufacturer globally, produced 1.2 million electric cars in 2023, with projections indicating a 19% increase to 1.45 million units in 2024. These developments are complemented by substantial investments in automotive manufacturing facilities, such as Meta Platforms Inc.'s January 2024 announcement of a USD 800 million data center campus in Hoosier State, featuring a 700,000-square-foot facility scheduled for completion by 2026. The demand for innovative glazing solutions in the automotive glass market continues to rise as manufacturers adapt to new technological advancements.

Segment Analysis: Product Type

Annealed Glass Segment in Flat Glass Market

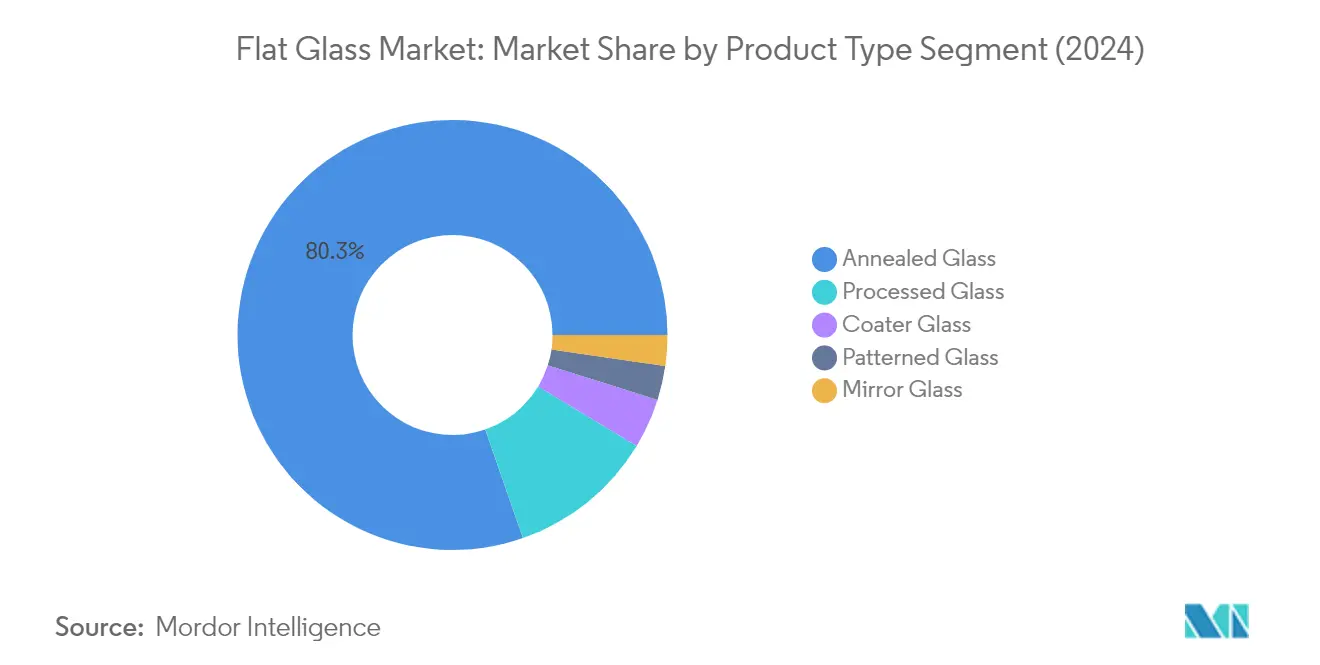

Annealed glass dominates the global flat glass market, commanding approximately 80% of the total market share in 2024. This substantial market presence can be attributed to its versatility and widespread applications across various industries. Annealed glass serves as the foundation for most glass products, being manufactured through the standard float process where glass is gradually cooled to reduce internal stresses. The segment's dominance is particularly evident in the construction sector, where it is extensively used in window glass, doors, and basic glazing applications. The segment's strength lies in its cost-effectiveness, ease of processing, and ability to serve as a base material for further processing into more specialized glass products.

Processed Glass Segment in Flat Glass Market

The processed glass segment is emerging as the fastest-growing category in the flat glass market, projected to grow at approximately 5% CAGR from 2024 to 2029. This robust growth is driven by increasing demand for enhanced safety glass, security, and energy efficiency in both construction and automotive applications. The segment encompasses various value-added products, including laminated glass, tempered glass, and insulated glass units. The growth is particularly fueled by stringent building codes and safety regulations across developed economies, coupled with the rising adoption of energy-efficient building materials. The automotive industry's shift towards safer and more sophisticated glass solutions further accelerates this segment's expansion.

Remaining Segments in Product Type

The flat glass market's remaining segments include coater glass, mirror glass, and patterned glass, each serving specific market niches. Coater glass, which includes reflective and low-E glass products, plays a crucial role in energy-efficient building solutions. Mirror glass continues to maintain its position in both decorative and functional applications across residential and commercial sectors. Patterned glass, while representing a smaller market share, remains important for decorative and privacy applications in both architectural and interior design contexts. These segments collectively contribute to the market's diversity and ability to meet specialized end-user requirements across various industries.

Segment Analysis: End-User Industry

Building and Construction Segment in Flat Glass Market

The building and construction segment dominates the flat glass market, commanding approximately 81% of the total market share in 2024. This substantial market presence is primarily driven by extensive applications in facade glass, windows, doors, facades, and interior design elements. The segment's dominance is further reinforced by significant construction projects worldwide, particularly in emerging economies. For instance, in Saudi Arabia, the government unveiled housing projects surpassing USD 17.3 billion in September 2023, while India's DLF announced an investment of around USD 421.44 million for a new luxury housing project in Gurugram. The growing trend toward energy-efficient buildings and sustainable construction practices has also bolstered the demand for specialized flat glass products like low-E glass and insulated glass units in this sector.

Solar Glass Segment in Flat Glass Market

The solar glass segment is emerging as the fastest-growing segment in the flat glass market, projected to expand at a CAGR of approximately 7% during 2024-2029. This remarkable growth is primarily driven by increasing global investments in renewable energy infrastructure and ambitious solar power installation targets across various countries. For instance, Germany aims to have 215 GW of installed solar capacity by 2030, while India has approved 50 solar parks with an aggregate capacity of around 37,490 MW. The segment's growth is further supported by technological advancements in solar glass manufacturing, with companies like Borosil Renewables enhancing their production capabilities to meet the rising demand. The increasing adoption of building-integrated photovoltaics (BIPV) and the growing focus on sustainable energy solutions continue to drive innovation and expansion in this segment.

Remaining Segments in End-User Industry

The automotive and other end-user industries segments complete the flat glass market landscape, each serving distinct applications and requirements. The automotive segment remains a crucial market driver, with applications ranging from windshields and windows to sunroofs, particularly benefiting from the growing electric vehicle market and advanced automotive designs. The other end-user industries segment encompasses diverse applications in electronics, appliances, and furniture, where flat glass is utilized for display screens, household appliances, and decorative purposes. Both segments continue to evolve with technological advancements and changing consumer preferences, contributing to the overall market dynamics through specialized product requirements and innovative applications.

Flat Glass Market Geography Segment Analysis

Flat Glass Market in Asia-Pacific

The Asia-Pacific region dominates the global flat glass market, driven by rapid urbanization, increasing construction activities, and growing automotive production. China leads the regional market, followed by Japan and South Korea, while India shows promising growth potential. The ASEAN countries, particularly Malaysia, Thailand, and Indonesia, are witnessing significant investments in construction glass and infrastructure development. The region's market dynamics are shaped by technological advancements in manufacturing processes and increasing demand for energy-efficient building materials.

Flat Glass Market in China - Regional Leader

China maintains its position as the largest flat glass market in Asia-Pacific, accounting for approximately 55% of the regional market share in 2024. The country's dominance is supported by its robust construction sector and ambitious infrastructure development plans. China's automotive industry, being the world's largest, significantly contributes to automotive glass demand. The nation has witnessed substantial investments in float glass production facilities, with approximately 119 facilities operating with a combined daily capacity of 164,885 tons. The government's focus on sustainable building practices and energy efficiency standards continues to drive innovation in flat glass manufacturing.

Flat Glass Market in India - Fastest Growing Market

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 7% during 2024-2029. The country's rapid urbanization, growing middle-class population, and increasing investments in infrastructure development are driving this growth. India's automotive sector expansion and government initiatives promoting solar glass installations have created additional demand channels. The country hosts around 18 flat glass locations with 30 furnaces, demonstrating significant manufacturing capabilities. Recent investments in new production facilities and technological upgrades are positioning India as a key player in the regional flat glass market.

Flat Glass Market in North America

North America represents a mature market for flat glass, characterized by technological advancement and high-quality standards in manufacturing. The region's market is primarily driven by renovation activities, automotive production, and increasing adoption of energy-efficient building solutions. The United States dominates the regional landscape, while Canada and Mexico contribute significantly through their growing construction and automotive sectors. The region's focus on sustainable building practices and energy conservation has led to increased demand for specialty glass products.

Flat Glass Market in United States - Regional Leader

The United States maintains its position as the largest flat glass market in North America, commanding approximately 75% of the regional market share in 2024. The country's market is supported by robust construction activity, particularly in the commercial and residential sectors. The nation's automotive industry, being the second-largest globally, significantly drives demand for automotive glass products. The presence of major manufacturers and continuous technological innovations in glass production has strengthened the country's market position.

Flat Glass Market in United States - Fastest Growing Market

The United States also leads in terms of growth rate in North America, with an expected growth rate of approximately 3% during 2024-2029. This growth is driven by increasing investments in sustainable building solutions and the rising demand for energy-efficient tempered glass products. The country's focus on solar glass development and electric vehicle production is creating new opportunities for flat glass manufacturers. The government's emphasis on infrastructure development and building energy efficiency standards continues to support market expansion.

Flat Glass Market in Europe

Europe's flat glass market is characterized by its strong focus on innovation and sustainability, particularly in energy-efficient building solutions. The region's market is supported by strict building regulations regarding energy efficiency and safety standards. Germany leads the European market, while countries like France, Italy, and the United Kingdom contribute significantly to regional demand. The automotive sector, particularly the growing electric vehicle segment, continues to drive demand for laminated glass products.

Flat Glass Market in Germany - Regional Leader

Germany maintains its position as the largest flat glass market in Europe, driven by its robust automotive manufacturing sector and stringent building energy efficiency requirements. The country's leadership in electric vehicle production and renewable energy installations creates sustained demand for specialized glass products. German manufacturers continue to invest in research and development, focusing on innovative glass solutions for both construction and automotive applications.

Flat Glass Market in Germany - Fastest Growing Market

Germany also leads the growth trajectory in Europe, supported by its ambitious renewable energy targets and automotive sector transformation. The country's commitment to sustainable building practices and energy efficiency drives demand for advanced glass products. The expansion of solar energy installations and electric vehicle production facilities continues to create new opportunities for flat glass manufacturers.

Flat Glass Market in South America

The South American flat glass market is experiencing steady growth, driven by urbanization and infrastructure development projects. Brazil emerges as both the largest and fastest-growing market in the region, followed by Argentina. The region's automotive sector expansion and increasing focus on energy-efficient building solutions are creating new opportunities for flat glass manufacturers. Government initiatives promoting sustainable construction practices and renewable energy installations are expected to further drive market growth.

Flat Glass Market in Middle East & Africa

The Middle East & Africa region shows promising growth potential in the flat glass market, driven by extensive construction activities and infrastructure development projects. Saudi Arabia emerges as both the largest and fastest-growing market in the region, followed by South Africa. The region's focus on sustainable building practices and growing investments in solar energy projects create significant opportunities for flat glass manufacturers. The automotive sector's development and increasing adoption of energy-efficient building solutions further support market growth.

Flat Glass Industry Overview

Top Companies in Flat Glass Market

The global flat glass market is led by established players like AGC Inc., Xinyi Glass Holdings, Saint-Gobain, Nippon Sheet Glass Co. Ltd, and Şişecam Group, who collectively dominate the industry landscape. These flat glass companies are increasingly focusing on sustainable manufacturing practices, with significant investments in carbon-neutral production technologies and energy-efficient processes. Product innovation efforts are centered around developing specialized coatings for enhanced performance, particularly in solar control and energy efficiency applications. Operational agility is demonstrated through strategic facility modernization and capacity expansion projects across key markets, particularly in Asia-Pacific and Europe. Companies are strengthening their market positions through vertical integration strategies, from raw material sourcing to distribution networks, while also pursuing collaborative ventures for technological advancement and market expansion.

Consolidated Market with Strong Regional Players

The flat glass market exhibits a partly consolidated structure, characterized by the presence of both global conglomerates and specialized regional manufacturers. Global leaders maintain their dominance through extensive manufacturing networks, advanced technological capabilities, and strong distribution channels spanning multiple continents. These companies leverage their scale to offer comprehensive product portfolios serving diverse end-user industries, from construction and automotive to solar energy applications. The market also features numerous regional players who have established strong footholds in their respective territories through specialized product offerings and a deep understanding of local market dynamics.

Recent years have witnessed significant merger and acquisition activities, primarily aimed at geographical expansion and technological capability enhancement. Companies are strategically acquiring local manufacturers to penetrate new markets and strengthen their regional presence. Vertical integration has emerged as a key trend, with major players acquiring businesses across the value chain to optimize costs and ensure supply chain stability. Joint ventures and collaborations, particularly in emerging markets, are becoming increasingly common as companies seek to combine their technological expertise with local market knowledge.

Innovation and Sustainability Drive Future Success

Success in the flat glass industry increasingly depends on companies' ability to align with sustainability trends and technological advancement. Market leaders are investing heavily in research and development to create innovative products that meet evolving environmental regulations and customer demands for energy-efficient solutions. The ability to offer customized solutions while maintaining cost competitiveness through operational efficiency has become crucial. Companies are also focusing on developing strong relationships with key end-user industries, particularly in the construction and automotive sectors, while expanding their presence in emerging applications like solar energy.

For new entrants and smaller players, success lies in identifying and serving niche market segments with specialized products and applications. The development of strong distribution networks and technical service capabilities is essential for maintaining market position. Companies must also carefully navigate the challenges posed by raw material price volatility and increasing environmental regulations. The ability to adapt to changing market dynamics, particularly in terms of end-user industry requirements and regional demand patterns, while maintaining product quality and competitive pricing, will be crucial for long-term success in the market.

Flat Glass Market Leaders

-

AGC Inc.

-

Xinyi Glass Holdings Limited

-

Saint-Gobain

-

Nippon Sheet Glass Co. Ltd

-

Şişecam

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Flat Glass Market News

- March 2024: Guardian Glass collaborated with Velux Group to develop tempered vacuum insulated glass (VIG). Under this agreement, Guardian and VELUX will collaborate to enhance their manufacturing processes and capabilities to satisfy the increasing demand for VIG.

- February 2023: AGC Inc. and Saint-Gobain announced collaboration on the design of a pilot breakthrough flat glass line that is expected to reduce direct CO2 emissions significantly. As part of this R&D project, AGC Inc.’s patterned glass production line in Barevka, Czech Republic, was decided to be entirely refurbished into a high-performing and state-of-the-art line that targets to be 50% electrified and 50% fired by a combination of oxygen and gas. This is a technical breakthrough compared to current technology used in flat glass furnaces fired by natural gas.

Flat Glass Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Growing Investments in the Construction Industry

- 4.1.2 Increasing Demand From the Automotive Industry

-

4.2 Restraints

- 4.2.1 Availability of Alternatives

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Volume)

-

5.1 Product Type

- 5.1.1 Annealed Glass

- 5.1.1.1 Clear Glass

- 5.1.1.2 Tinted Glass

- 5.1.2 Coater Glass

- 5.1.2.1 Reflective Glass

- 5.1.2.2 Low E Glass

- 5.1.3 Processed Glass

- 5.1.3.1 Laminated Glass

- 5.1.3.2 Tempered Glass

- 5.1.4 Mirror Glass

- 5.1.5 Patterned Glass

-

5.2 End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Automotive

- 5.2.3 Solar Glass

- 5.2.4 Other End-user Industries

-

5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 Adamant Holding Company

- 6.4.2 AGC Inc.

- 6.4.3 Cardinal Glass Industries Inc.

- 6.4.4 Central Glass Co. Ltd

- 6.4.5 China Glass Holdings Limited

- 6.4.6 Euroglas

- 6.4.7 Guardian Industries

- 6.4.8 Nippon Sheet Glass Co. Ltd

- 6.4.9 Phoenicia

- 6.4.10 Saint-Gobain

- 6.4.11 SCHOTT

- 6.4.12 Sisecam

- 6.4.13 Taiwan Glass Ind. Corp.

- 6.4.14 Vitro

- 6.4.15 Xinyi Glass Holdings Limited

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Opportunity in the Solar Energy

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Flat Glass Industry Segmentation

Flat glass is a type of glass initially produced in plane form. It is commonly used for windows, glass doors, transparent walls, and windscreens. Flat glass is sometimes bent after the plane sheet is produced for modern architectural and automotive applications.

The flat glass market is segmented by product type, end-user industry, and geography. The market is segmented by product type into annealed glass, coated glass, processed glass, mirror glass, and patterned glass. By end-user industry, the market is segmented into building and construction, automotive, solar glass, and other end-user industries. The report also covers the market sizes and forecasts for the flat glass market in 15 countries across major regions. For each segment, the market sizing and forecasts are done based on volume (tons).

| Product Type | Annealed Glass | Clear Glass | |

| Tinted Glass | |||

| Coater Glass | Reflective Glass | ||

| Low E Glass | |||

| Processed Glass | Laminated Glass | ||

| Tempered Glass | |||

| Mirror Glass | |||

| Patterned Glass | |||

| End-user Industry | Building and Construction | ||

| Automotive | |||

| Solar Glass | |||

| Other End-user Industries | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN Countries | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Flat Glass Market Research FAQs

How big is the Flat Glass Market?

The Flat Glass Market size is expected to reach 83.17 million tons in 2025 and grow at a CAGR of 4.03% to reach 101.34 million tons by 2030.

What is the current Flat Glass Market size?

In 2025, the Flat Glass Market size is expected to reach 83.17 million tons.

Who are the key players in Flat Glass Market?

AGC Inc., Xinyi Glass Holdings Limited, Saint-Gobain, Nippon Sheet Glass Co. Ltd and Şişecam are the major companies operating in the Flat Glass Market.

Which is the fastest growing region in Flat Glass Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Flat Glass Market?

In 2025, the Asia Pacific accounts for the largest market share in Flat Glass Market.

What years does this Flat Glass Market cover, and what was the market size in 2024?

In 2024, the Flat Glass Market size was estimated at 79.82 million tons. The report covers the Flat Glass Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Flat Glass Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Flat Glass Market Research

Mordor Intelligence provides comprehensive insights into the flat glass industry. We leverage extensive expertise in analyzing the float glass, sheet glass, and plate glass segments. Our research covers a wide range of applications, including automotive glass, construction glass, solar glass, and specialty glass. The report offers a detailed analysis of glazing industry trends. This includes processed glass manufacturing techniques, developments in the tempered glass industry, and innovations in laminated glass and insulated glass technologies.

Stakeholders in the architectural glass market, construction glass industry, and automotive glass industry benefit from our detailed market forecasts and industry analysis. This information is available in an easy-to-download report PDF. The research covers crucial segments such as residential glass, commercial glass, facade glass, and safety glass applications. It also examines emerging trends in window glass and toughened glass technologies. Our analysis provides valuable insights for manufacturers, suppliers, and end-users in the industrial glass and building glass sectors. We focus particularly on transparent glass innovations and developments in the specialty glass industry.