Fire Retardant Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

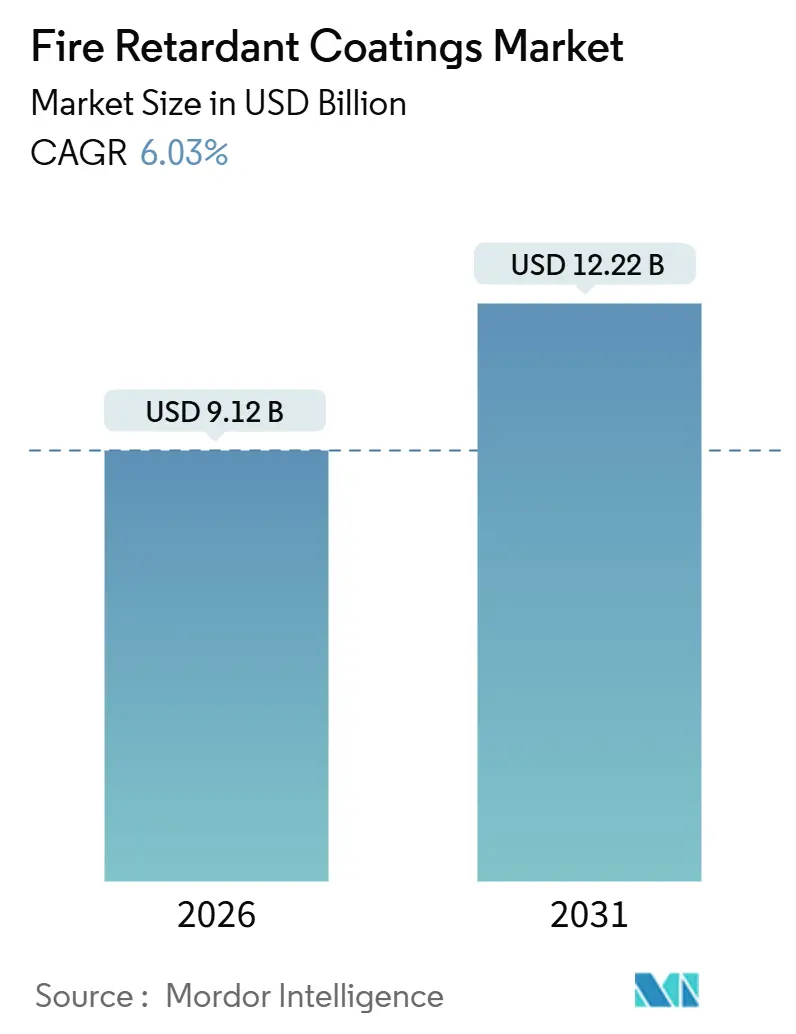

| Market Size (2026) | USD 9.12 Billion |

| Market Size (2031) | USD 12.22 Billion |

| Growth Rate (2026 - 2031) | 6.03% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fire Retardant Coatings Market Analysis by Mordor Intelligence

The Fire Retardant Coatings Market size is estimated at USD 9.12 billion in 2026, and is expected to reach USD 12.22 billion by 2031, at a CAGR of 6.03% during the forecast period (2026-2031). Heightened enforcement of fire-safety codes, accelerating infrastructure programs, and a decisive move toward low-VOC chemistries are sustaining healthy demand across construction, transportation, and energy assets. Asia-Pacific continues to anchor global volumes, yet the Middle East and Africa now deliver the fastest incremental gains, helped by mega-projects under Saudi Vision 2030 and LNG export terminals in Qatar. Technology preferences are shifting from solvent-borne systems toward water-borne and powder alternatives, while specialty silicone elastomers are carving out a share in high-temperature battery and aerospace uses.

Key Report Takeaways

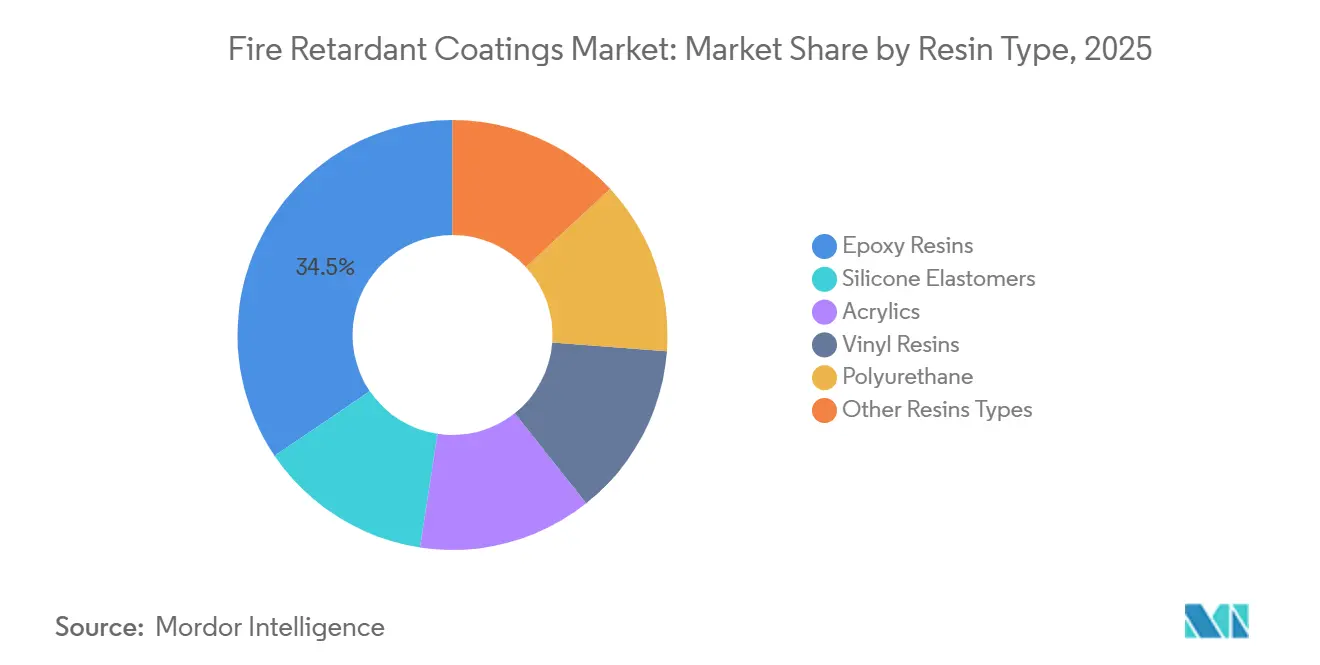

- By resin type, epoxy resins led with 34.48% of the fire retardant coatings market share in 2025, while silicone elastomers posted the highest forecast growth at 6.24% CAGR to 2031.

- By technology, water-borne systems accounted for 46.37% of the fire retardant coatings market size in 2025, and powder coatings are forecast to expand at a 6.18% CAGR through 2031.

- By coating type, intumescent products captured 58.62% revenue share in 2025; ablative and hybrid systems are expected to grow fastest at 6.31% CAGR between 2026-2031.

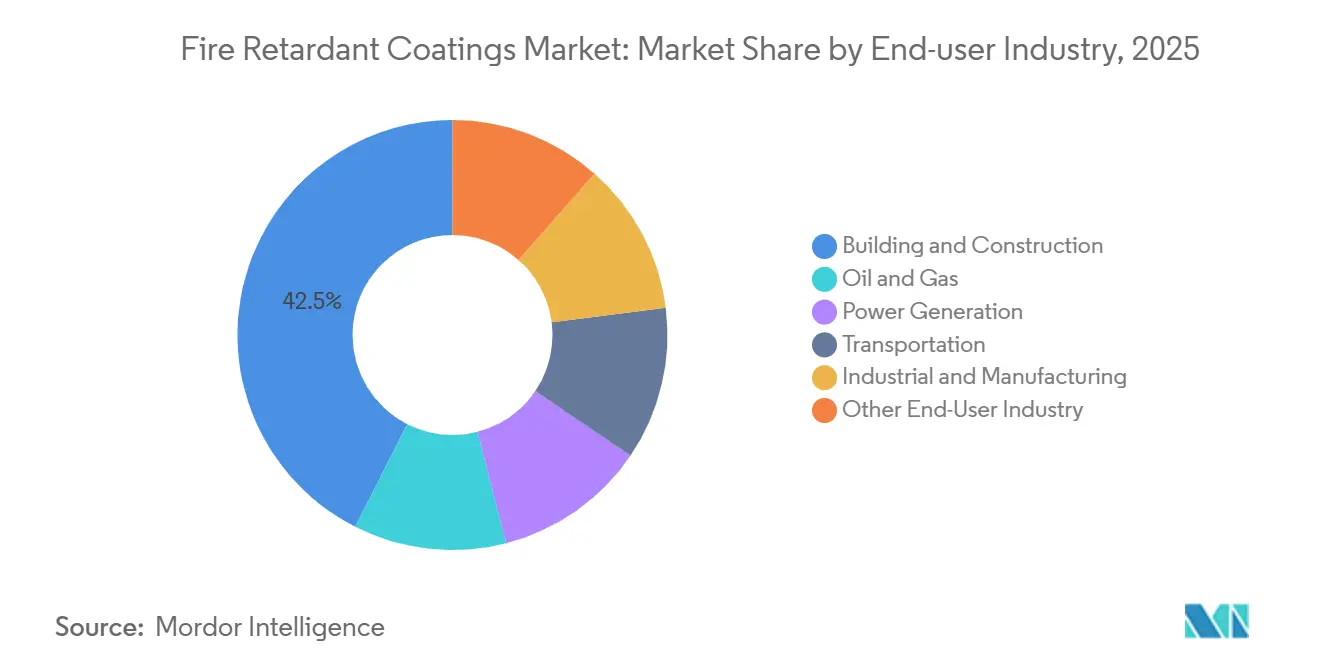

- By end-user industry, building and construction held 42.53% of the fire retardant coatings market size in 2025, while transportation is projected to deliver the quickest gains at 6.12% CAGR over the same period.

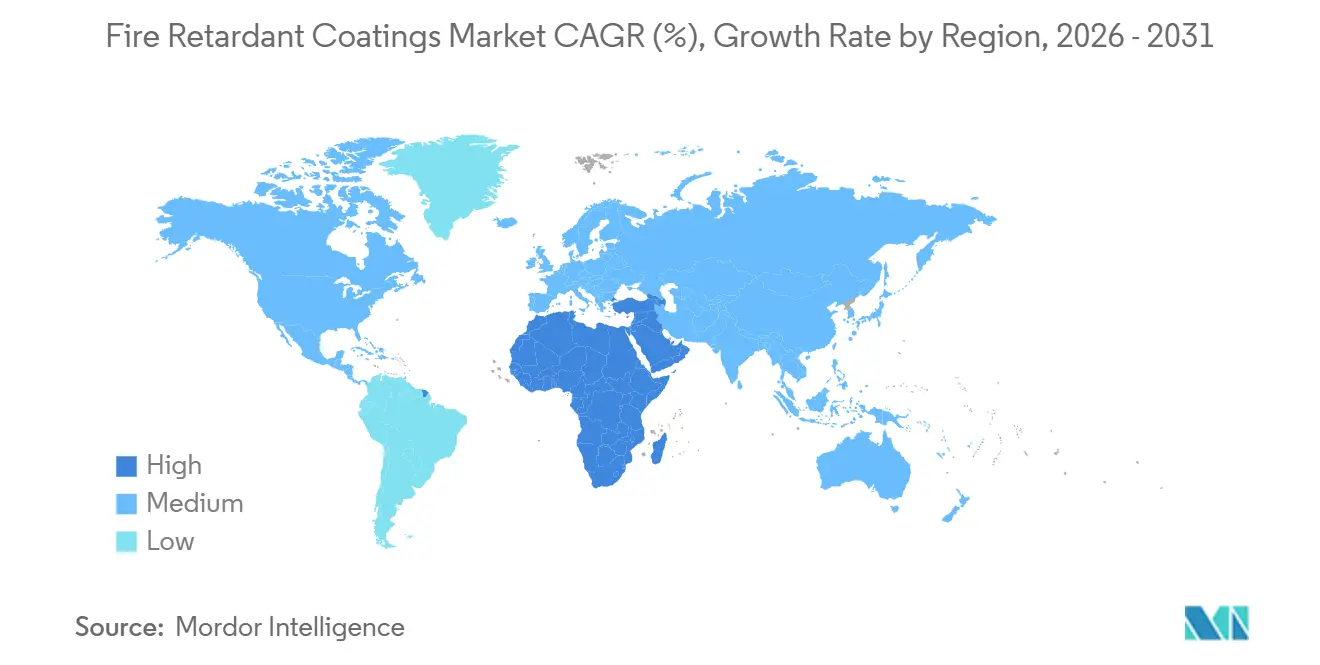

- By geography, Asia-Pacific dominated with 45.28% of global demand in 2025; the Middle-East and Africa are set to advance at a 5.94% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fire Retardant Coatings Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing construction activities across the globe | +1.8% | Asia-Pacific, Middle East, North America | Medium term (2-4 years) |

| Accelerating oil and gas infrastructure expansion | +1.2% | Middle East, North America, Asia-Pacific | Long term (≥4 years) |

| Stricter fire-safety regulations and building codes | +1.5% | Global | Short term (≤2 years) |

| Rising demand for passive fire protection in e-mobility and battery systems | +1.1% | Asia-Pacific, Europe, North America | Medium term (2-4 years) |

| Shift toward bio-based and halogen-free chemistries | +0.7% | Europe, North America, Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Increasing Construction Activities Across the Globe

In 2024, China’s construction output bolstered consistent demand for epoxy-based intumescent coatings that meet GB 14907-2018 standards for multi-story steel frames[1]National Bureau of Statistics of China, “Construction Output 2024,” stats.gov.cn. Meanwhile, as part of India’s Smart Cities Mission, large-scale municipal housing projects are now mandating water-borne formulas in line with the National Building Code. In Saudi Arabia, the NEOM, Red Sea, and Qiddiya projects have a combined requirement for coated steel, leading European suppliers to establish local blending facilities. In Europe and North America, the trend towards modular construction is leaning towards factory-applied powder intumescent layers, which significantly reduce on-site labor. This niche market currently sees competition from only a select few OEM applicators. As a result, the fire retardant coatings market is not just witnessing growth in square meters but is also benefiting from procedural shifts that emphasize high-efficiency chemistries.

Accelerating Oil and Gas Infrastructure Expansion

API Recommended Practice 752 (2024) now quantifies thermal hazards for permanent buildings in refineries, leading engineers to select ablative and hybrid systems able to withstand 1,100 °C hydrocarbon fires for four hours[2]American Petroleum Institute, “API RP 752 2024 Edition,” api.org . As LNG projects expand in Qatar and Saudi Arabia, the specification scope broadens. Simultaneously, North American shale operators are retrofitting legacy plants to align with the updated 49 CFR 194 emergency-response regulations. Powder coatings are becoming popular for cable trays and small-bore piping. These coatings not only reduce solvent exposure in confined spaces but also expedite turnaround times. While current adoption stands low, the passive fire-protection expenditure, supplier investments in training are poised to bridge this gap by 2028, thereby enlarging the market for fire-retardant coatings.

Stricter Fire-Safety Regulations and Building Codes

The United Kingdom’s Approved Document B amendments tighten char-thickness verification and impose third-party testing on all coatings used in new care homes. China’s upcoming GB 38031-2025 forces electric-vehicle makers to adopt silicone-rich barriers that delay thermal propagation by five minutes. The European Union’s Directive 2024/1275 integrates energy-performance targets with fire resilience, creating dual compliance pressure that accelerates uptake of halogen-free intumescents. Railway manufacturers face EN 45545 smoke-toxicity ceilings, pushing them toward phosphorus-based systems. Tighter rules in mature economies inspire Asian exporters to mimic certification pathways, thereby elevating global baseline quality and expanding the premium tier of the fire retardant coatings market.

Rising Demand for Passive Fire Protection in E-Mobility and Battery Systems

China’s GB 44240-2024 for energy-storage installations and the EU’s Regulation 2023/1542 both require coatings that prevent cell-to-cell thermal propagation for at least five minutes. Silicone elastomers, growing at 6.24% CAGR, outperform epoxies above 600 °C and remain pliable under cryogenic shock. Automotive OEMs in Germany and the United States increasingly specify powder-based barriers for underbody battery shields to eliminate VOCs and reduce mass. Retrofit programs for earlier EV bus fleets present an overlooked aftermarket. These shifts ensure that battery applications will be one of the most dynamic slices of the fire retardant coatings market over the next five years.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of low-cost substitutes | -0.9% | Global, higher in India, Southeast Asia, Africa | Short term (≤2 years) |

| Volatile epoxy and silicone raw-material prices | -0.6% | North America, Europe | Medium term (2-4 years) |

| Shortage of qualified applicators | -0.5% | North America, Europe, Japan, Australia | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Availability of Low-Cost Substitutes

In India, Indonesia, and Nigeria, cost-sensitive developers are increasingly opting for gypsum boards, which are more affordable compared to spray intumescents. While cementitious plasters offer a commendable four-hour fire rating, their weight limits their application in seismic retrofits. In a bid to enhance building safety, insurance firms have begun levying premium penalties on structures without certified coatings. This strategy is gradually tipping the scales in favor of intumescents, narrowing the price-performance divide. To maintain their market share, suppliers are now offering bundled services, including turnkey applications and multi-year warranties. By shifting the conversation from just the upfront material cost to the broader perspective of lifecycle economics, they're ensuring sustained demand in the fire retardant coatings sector.

Volatile Epoxy and Silicone Raw-Material Prices

In 2024, spot prices for Chinese epoxy resin dropped due to an oversupply of BPA. However, upstream producers are scaling back, hinting at potential price spikes when construction activities pick up. In Europe, prices for silicone elastomers remain elevated. This is largely attributed to the energy-intensive nature of their production and limited capacity. Phosphinate additives, sourced globally from only three suppliers, wield significant pricing power, which in turn squeezes margins for downstream users. In Latin America, smaller formulators are turning to lower-cost fillers as a hedge. Yet, this strategy often comes at a cost, risking the integrity of char and compliance with codes. While currency depreciation in emerging markets intensifies these challenges, major suppliers are countering by leveraging multi-year supply contracts. This strategy not only stabilizes their costs but also fortifies their stance in the expansive fire retardant coatings market.

Segment Analysis

By Resin Type: Epoxy Anchors Share While Silicone Targets Extremes

Epoxy resins sustained 34.48% of the fire-retardant coatings market share in 2025 due to robust adhesion and predictable intumescence. Silicone elastomers, expanding at 6.24% CAGR to 2031, answer battery-pack and aerospace needs beyond 600 °C, a temperature realm where epoxies lose structural integrity. Acrylics fill architectural niches, while polyurethane systems are emerging in spray-foam insulation with integrated fire barriers. Hybrid epoxy-silicone stacks are under pilot in German and Korean battery plants for 2027 launches. Such diversification enlarges supplier research and development pipelines and helps guard against commoditization in the fire retardant coatings market.

Epoxies remain cost-effective, yet their bisphenol-A feedstock lines up alongside environmental scrutiny, motivating formulators to explore lignin-based hardeners. Silicones, though premium-priced, offer unmatched thermal shock resistance, and their expanding use in e-mobility raises total consumption. Niche phenolics and polyesters continue to serve marine bulkheads and rail interiors, but their collective share slips as performance standards climb. Resin evolution, therefore, signals both risk and opportunity for stakeholders across the fire retardant coatings industry.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Water-Borne Formulations Dominate as Powder Coatings Accelerate

Water-borne products held 46.37% of 2025 revenue, aided by EU and California VOC caps of 250 g/L. Powder variants, although small share, are forecast to grow at a 6.18% CAGR, powered by automotive and appliance lines that favor single-pass, zero-solvent processes. Solvent-borne systems still serve maintenance jobs on corroded steel where surface prep is imperfect. Radiation-cured and high-solids blends occupy small niches in cold-weather or rapid-turnaround projects.

Powder intumescents require tight particle-size control and electrostatic tuning, challenges that only a limited number of suppliers have mastered. Nonetheless, the technology’s low waste rate and significant labor savings render a compelling total-cost argument. Extended humidity cure times remain the Achilles heel for water-borne layers in tropical regions, prompting formulators to add flash-rust inhibitors. As regulations tighten further, adoption curves will continue to support value growth in the fire-retardant coatings market.

By Coating Type: Intumescent Systems Dominate While Ablative Hybrids Gain

Intumescent products captured 58.62% in 2025 because 1-3 mm dry-film layers satisfy architects and engineers alike. Ablative and hybrid solutions are slated to rise 6.31% annually, addressing offshore and LNG sites where 1,100 °C exposures demand char durability beyond standard intumescents. Cementitious sprays remain cost-effective for ground-level structures but lose favor in high-rise and seismic zones due to weight penalties.

A recent design trend combines a thin intumescent primer for rapid swelling with an ablative topcoat, cutting system weight while meeting four-hour hydrocarbon tests under UL 1709. UV and moisture degradation outdoors push suppliers to develop silicone-modified seal coats that extend service life. Continuous innovation keeps the coating mix dynamic, reinforcing the growth trajectory of the fire retardant coatings market.

By End-User Industry: Construction Anchors Demand While Transportation Accelerates

Building and construction retained 42.53% of 2025 spending as codes worldwide require up to three hours of protection on exposed steel. Transportation is forecast to expand at a 6.12% CAGR through 2031, fueled by battery-fire mandates in EVs, EN 45545 compliance in railways, and flame-resistant composites in aircraft. Oil and gas demand rebounds with new petrochemical complexes and refinery upgrades. Power generation, both conventional and renewable, specifies coatings on cable trays and control rooms to prevent cascading failures. Manufacturing facilities, notably semiconductor fabs and food plants, install coatings on conveyors and storage racks where ignition sources converge. Sector diversity itself insulates the overall fire-retardant coatings market from cyclical swings in any single vertical.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific commanded a 45.28% share in 2025, bolstered by China's impressive construction output and India's ambitious National Infrastructure Pipeline. Japan's surge in retrofitting, coupled with South Korea's production of electric vehicles, has heightened the demand for silicone-rich formulations. Meanwhile, Southeast Asia is reaping the rewards of industrial park investments, a strategic move linked to supply-chain diversification. The Belt and Road initiative sees powder-coated prefab modules being shipped, expanding regional export flows, and integrating advanced coatings into projects in emerging markets.

North America is riding a wave of momentum, fueled by the United States' infrastructure law. This, alongside bridge rehabilitations and grid upgrades necessitating passive fire protection, underscores the region's robust activity. Canada's oil sands and Mexico's impressive vehicle assembly bolster these volumes. However, a notable shortage of certified applicators has led contractors to negotiate schedules months in advance. This scarcity sometimes results in project deferrals and creates spikes in demand, benefiting suppliers with agile mobile crews.

Europe's ambitious Renovation Wave is harmonizing fire safety with carbon reduction efforts across millions of properties. In Germany and the Nordics, there's a push for halogen-free formulas. While these add extra material costs, they offer insurers significant savings on risk premiums. Following the Grenfell incident, the UK has tightened its market entry with reforms mandating third-party product verification. France is championing bio-based retardants, aligning them with its low-carbon objectives. Meanwhile, sanctions have curtailed Russia's access to Western chemistries, prompting local producers to attempt reverse-engineering of epoxies, though with mixed results in quality.

The Middle East and Africa are the fastest-expanding regions at 5.94% CAGR. This surge is largely attributed to NEOM's colossal steel demands and the UAE's stringent high-rise codes, which mandate two-hour fire ratings. South Africa is modernizing its petrochemical sites in line with SANS 10177 standards. However, logistical challenges outside major provinces are hindering swift adoption. A scarcity of accredited test labs in many African nations means imported certifications are the norm. While this elevates costs, it also raises the bar for quality expectations.

South America is on the upswing. Brazil is enforcing the ABNT NBR 14432 standard for buildings taller than four stories, while Argentina's VOC restrictions are nudging factories towards water-borne systems. In the face of currency fluctuations, there's a trend of hedging and stockpiling raw materials. Chile's mining sector, emphasizing safety, mandates four-hour coatings on critical supports, spurring a niche demand for ablative products. Together, these developments are expanding the horizons of the fire retardant coatings market and diversifying its revenue streams.

Competitive Landscape

The fire retardant coatings market is moderately fragmented. The top five suppliers differentiate through bundled warranties, digital specification aids, and integrated corrosion-plus-fire packages that lower the total cost of ownership for asset managers. Regional challengers in China, India, and Brazil undercut on price by thinning additive loads and bypassing certification, yet insurance penalties and stricter building audits are eroding this strategy. Research and development efforts around lignin-derived binders and nano-silica reinforcements promise further product differentiation and sustainability advantages, reinforcing competitive edges within the fire retardant coatings market.

Fire Retardant Coatings Industry Leaders

Akzo Nobel N.V.

PPG Industries, Inc.

The Sherwin-Williams Company

Jotun

Hempel AS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Jotun announced the global launch of Jotachar 1709XT, the latest addition to its trusted Jotachar range of passive fire-protection coatings. The product is produced in Oman alongside the full Jotachar range.

- September 2024: PPG Industries, Inc. announced the launch of PPG Steelguard 951 epoxy intumescent fire protection coating in the Americas. This product is designed for advanced manufacturing facilities, including semiconductor plants, electric vehicle battery facilities, data centers, and other commercial infrastructure.

Global Fire Retardant Coatings Market Report Scope

Fire retardant coatings are non-combustible chemicals applied in residential, commercial, and industrial buildings to reduce the spread of fire. Fire retardants inhibit or delay the spread of fire by suppressing the chemical reactions in the flame.

The Fire Retardant Coatings Market is segmented by resin type, technology, coating type, end-user industry, and geography. By resin type, the market is segmented into silicone elastomers, epoxy resins, acrylic, vinyl resins, polyurethane, and other resin types. By technology, the market is segmented into water-borne, solvent-borne, powder coatings, and others. By coating type, the market is segmented into intumescent and cementitious. By end-user industry, the market is segmented into building and construction, oil and gas, power generation, transportation, industrial and manufacturing, and other end-user industries. The report also covers the market size and forecasts for the fire retardant coatings market in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Silicone Elastomers |

| Epoxy Resins |

| Acrylics |

| Vinyl Resins |

| Polyurethane |

| Other Resins Types |

| Water-borne |

| Solvent-borne |

| Powder Coatings |

| Others |

| Intumescent |

| Cementitious |

| Building and Construction |

| Oil and Gas |

| Power Generation |

| Transportation |

| Industrial and Manufacturing |

| Other End-User Industry |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Resin Type | Silicone Elastomers | |

| Epoxy Resins | ||

| Acrylics | ||

| Vinyl Resins | ||

| Polyurethane | ||

| Other Resins Types | ||

| By Technology | Water-borne | |

| Solvent-borne | ||

| Powder Coatings | ||

| Others | ||

| By Coating Type | Intumescent | |

| Cementitious | ||

| By End-user Industry | Building and Construction | |

| Oil and Gas | ||

| Power Generation | ||

| Transportation | ||

| Industrial and Manufacturing | ||

| Other End-User Industry | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the fire retardant coatings market?

The fire retardant coatings market size stands at USD 9.12 billion in 2026 and is forecast to reach USD 12.22 billion by 2031.

Which resin type holds the largest share?

Epoxy resins lead with 34.48% of 2025 revenue, favored for strong adhesion and predictable char formation.

Which application segment is growing fastest?

Transportation, driven by electric-vehicle battery safety and railway standards, is projected to grow at a 6.12% CAGR through 2031.

Which region is expanding most quickly?

The Middle-East and Africa are set to record a 5.94% CAGR, propelled by Saudi Vision 2030 and LNG infrastructure.

What new technologies are emerging?

Powder intumescent coatings with nano-silica reinforcement and bio-based binders derived from lignin are gaining commercial traction.